|

市場調査レポート

商品コード

1636141

米国の航空貨物輸送:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)US Air Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の航空貨物輸送:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

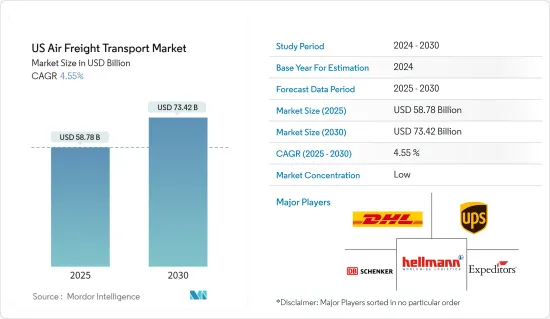

米国の航空貨物輸送市場規模は2025年に587億8,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは4.55%で、2030年には734億2,000万米ドルに達すると予測されます。

主要ハイライト

- 米国の航空貨物輸送市場は、主にeコマース活動の急増とFMCG需要の急増によって牽引されています。

- eコマースの爆発的成長が航空貨物需要を牽引し続けています。この急成長により、迅速な配送に対するニーズが高まり、ロジスティクスプロバイダーは迅速な配送に対する消費者の期待に応えるため、その能力を強化し、業務を合理化する必要に迫られています。

- 2024年6月、米国と世界の目的地を結ぶ航空貨物は2023年比で5%増加し、合計で103万6,907トンとなりました。米国の航空会社はこの国際貨物の47%の輸送を担当し、チャーター便が全体の21%を占めました。

- 2024年6月までの1年間で、米国貨物の主要な国際ゲートウェイは中国、韓国、日本、香港、ドイツでした。上位25カ国の市場のうち、14カ国で貨物輸送量が増加し、11カ国で減少しました。特に、減少した市場の中ではベルギーが2023年比で12%の急減を記録しました。米国旗のシェア動態は様々で、14の市場で減少、4つの市場で横ばい、他の7つの市場で増加しました。

- 技術の進歩は航空貨物のオペレーションを大きく変え、効率性と信頼性を向上させています。2024年7月、Siemens・デジタルインダストリーズソフトウェアは、米国を拠点とする航空宇宙企業のNatilusがSiemens Xceleratorスイートを業務に統合したことを明らかにしました。革新的なブレンデッド・ウイングボディの航空機で世界のサプライチェーンに革命を起こすというビジョンを持つNatilusは、Siemensのソフトウェアを活用することで、最初のプロトタイプの開発期間を半分に短縮しました。

米国の航空貨物輸送市場の動向

国際貿易需要の高まりを受け、米国の航空貨物市場は成長へ

2024年、米国の航空貨物輸送市場は、景気回復、eコマースの拡大、地政学的力学の変化などの要因によって、国際貿易需要が大幅に増加する見込みです。

近年、米国のeコマース部門はかつてない成長を遂げています。2023年までに売上高は1兆米ドルの大台を突破し、AmazonやWalmartのような産業大手に加え、EtsyやeBayのような小規模なプラットフォームにも後押しされました。

2023年には、米国のカナダとメキシコとの貨物貿易額は1兆5,700億米ドルに達しました。この貿易は総重量24億8,470万トンを占めています。貨物の重量は2022年から8.8%増加したが、北米貨物のドル換算額は2023年も安定していました。

米国は25年以上にわたり、「オープンスカイ」施策を通じて国際航空市場の拡大を支持してきました。これらの二国間協定や多国間協定は、政府による各国間の航空会社の運航制限を撤廃するものです。これらの協定は、許可される航空会社の数、就航できる路線、採用できる価格戦略、利用しなければならない航空機を規定するものです。さらに、これらの協定は米国と外国の航空会社間の協力を促進し、米国の貨物・速達便輸送会社が貨物や小包をシームレスに輸送できるようにします。オープンスカイの範囲は旅客航空と貨物航空にまたがり、定期便とチャーター便の両方をカバーしています。これまでに米国は、あらゆる大陸と発展段階にまたがる125以上のパートナーとオープンスカイ協定を結んでいます。

米国の電気機械・エレクトロニクス貿易:貿易赤字の中での成長の年

2024年8月、米国は198億米ドル相当の電気機械・電子機器を輸出したが、輸入は409億米ドルに達し、210億米ドルの貿易赤字となりました。2023年8月から2024年8月にかけて、米国のこのセグメントの輸出は23億2,000万米ドル(13.3%)増加し、175億米ドルから198億米ドルに増加しました。一方、輸入は32億6,000万米ドル(8.68%)増加し、376億米ドルから409億米ドルになりました。

2024年8月、米国は主にメキシコ(50億米ドル)、カナダ(24億4,000万米ドル)、中国(16億7,000万米ドル)、マレーシア(16億5,000万米ドル)、香港(7億200万米ドル)に電気機械・電子機器を輸出しました。逆に輸入は、中国(104億米ドル)、メキシコ(78億5,000万米ドル)、ベトナム(33億7,000万米ドル)、チャイニーズ・タイペイ(30億3,000万米ドル)、マレーシア(23億8,000万米ドル)からのものが多いです。

2024年8月の米国の電気機械・電子機器輸出の前年同月比増加は、メキシコ(3億8,300万米ドル、9.62%)、カナダ(3億5,000万米ドル、17.9%)、ポーランド(1億6,500万米ドル、122%)への出荷の増加によるところが大きいです。輸入側では、メキシコ(8億1,600万米ドル、14.3%)、タイ(6億8,700万米ドル、67.8%)、インド(5億2,100万米ドル、150%)からの購入が増加しました。

米国の航空貨物輸送産業概要

米国の航空貨物輸送市場はセグメント化されており、地域的な参入企業と国際的な参入企業が混在しています。同市場の主要企業には、DHL、United Parcel Services Inc.、Expeditors International、Hellmann Worldwide Logistics、DB Schenkerなどがあります。

各社が技術主導のソリューションを取り入れ、効率的な流通チャネルを模索するにつれ、産業における新たな機会をつかむための戦略的なポジションを確立していることがわかる。

2024年10月現在、DHL ExpressとDHL Global Forwardingは、International Airlines Group(IAG)の貨物取扱部門であるIAG Cargoと契約を更新し、サステナビリティへの取り組みを進めています。このパートナーシップにより、DHLのオペレーションにおいて、サステイナブル航空燃料(SAF)がさらに6,000万リットル使用されることになります。2024年と2025年にわたるこの契約更新により、温室効果ガス排出量を約16万5,000トンのCO2e削減が見込まれています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 市場の範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察と力学

- 市場概要

- 市場力学

- 促進要因

- 国境を越えた貿易関係の急増が市場を牽引

- 市場は経済成長によって大きく左右される

- 抑制要因

- 市場を阻害する地政学的要因

- 市場に影響を与える消費者行動

- 機会

- 市場を牽引する技術の進歩

- 促進要因

- 政府の取り組みと規制

- サプライチェーン/バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競合の程度

- 技術スナップショットとデジタル動向

- 航空輸送の主要品目について

- 航空運賃の詳細

- 航空貨物産業における重量貨物/プロジェクトロジスティクスのスポットライト

- 空港における主要グランドハンドリング機器に関する洞察

- 危険物の安全輸送に関する基準と規制のレビューと解説

- 航空貨物部門におけるコールドチェーンロジスティクス概要

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- サービス別

- 貨物輸送(貨物と郵便)

- 貨物フォワーディング

- その他付加価値サービス

- サービス別

- 配送

- 航空会社

- 郵便

- その他

- 仕向地別

- 国内

- 国際線

- キャリアタイプ別

- ベリーカーゴ

- 貨物船

第6章 競合情勢

- 市場集中度概要

- 企業プロファイル

- DHL

- United Parcel Services Inc.

- Expeditors International

- Hellmann Worldwide Logistics

- DB Schenker

- Kuehne+Nagel

- DSV

- Nippon Express

- Kerry Logistics

- Ceva Logistics*

- その他の企業

第7章 市場の将来

第8章 付録

- マクロ経済指標(GDP分布、活動別、運輸・倉庫業の経済への寄与度)

- 対外貿易統計-輸出と輸入(製品別)

- 主要輸出先と輸入原産国に関する洞察

The US Air Freight Transport Market size is estimated at USD 58.78 billion in 2025, and is expected to reach USD 73.42 billion by 2030, at a CAGR of 4.55% during the forecast period (2025-2030).

Key Highlights

- The US air freight transport market is mainly driven by the surge in e-commerce activities and surge in demand for FMCG.

- E-commerce's explosive growth continues to drive air freight demand. This surge has led to an increased need for prompt deliveries, pushing logistics providers to bolster their capabilities and streamline operations to align with consumer expectations for swift shipments.

- In June 2024, air freight between the US and global destinations rose by 5% from 2023, totaling 1,036,907 tons. US airlines were responsible for transporting 47% of this international freight, with charter services making up 21% of the total traffic.

- For the year ending June 2024, the leading international gateways for US freight were China, South Korea, Japan, Hong Kong, and Germany. Among the top 25 country markets, 14 saw an increase in freight traffic, while 11 experienced a decline. Notably, Belgium, among the declining markets, recorded the steepest drop at 12% compared to 2023. The US flag share dynamics varied: it decreased in 14 markets, remained steady in four, and saw an uptick in seven others.

- Technological advancements are significantly transforming air freight operations, improving efficiency and reliability. In July 2024, Siemens Digital Industries Software revealed that Natilus, a US-based aerospace firm, has integrated the Siemens Xcelerator suite into its operations. With a vision to revolutionize global supply chains via its innovative blended-wing-body aircraft, Natilus has leveraged Siemens software to slash its inaugural prototype's development time by half.

US Air Freight Transport Market Trends

US Air Freight Market Set for Growth Amid Rising International Trade Demand

In 2024, the US air freight transport market is poised for significant growth in international trade demand, driven by factors such as economic recovery, the expansion of e-commerce, and shifting geopolitical dynamics.

In recent years, the US e-commerce sector has witnessed unprecedented growth. By 2023, sales surpassed the USD 1 trillion mark, propelled by industry giants like Amazon and Walmart, alongside smaller platforms such as Etsy and eBay.

In 2023, US freight trade with Canada and Mexico reached a value of USD 1.57 trillion. This trade accounted for a total weight of 2,484.7 million tons. Although the weight of the freight saw an 8.8% increase from 2022, the dollar value of North American freight held steady in 2023.

For over 25 years, the United States has championed the expansion of international aviation markets through its "Open Skies" policy. These bilateral and multilateral agreements eliminate government-imposed limitations on airline operations between countries. They dictate the number of airlines permitted, the routes they can take, the pricing strategies they can adopt, and the aircraft they must utilize. Furthermore, these agreements foster collaboration between US and foreign airlines, enabling US cargo and express delivery carriers to transport freight and parcels seamlessly. The scope of Open Skies spans passenger and cargo aviation, covering both scheduled and charter flights. Thus far, the US has forged Open Skies agreements with over 125 partners, spanning every continent and developmental stage.

US Electrical Machinery and Electronics Trade: A Year of Growth Amidst a Trade Deficit

In August 2024, the US exported USD 19.8 Billion worth of electrical machinery and electronics, while imports reached USD 40.9 Billion, leading to a trade deficit of USD 21 Billion. From August 2023 to August 2024, US exports in this sector rose by USD 2.32 Billion (13.3%), climbing from USD 17.5 Billion to USD 19.8 Billion. In contrast, imports saw a USD 3.26 Billion (8.68%) uptick, moving from USD 37.6 Billion to USD 40.9 Billion.

In August 2024, the US primarily exported electrical machinery and electronics to Mexico (USD 5 Billion), Canada (USD 2.44 Billion), China (USD 1.67 Billion), Malaysia (USD 1.65 Billion), and Hong Kong (USD 702 Million). Conversely, imports were predominantly sourced from China (USD 10.4 Billion), Mexico (USD 7.85 Billion), Vietnam (USD 3.37 Billion), Chinese Taipei (USD 3.03 Billion), and Malaysia (USD 2.38 Billion).

The year-on-year rise in US exports of electrical machinery and electronics in August 2024 was largely driven by boosts in shipments to Mexico (USD 383 million or 9.62%), Canada (USD 350 million or 17.9%), and Poland (USD 165 million or 122%). On the import side, the uptick was mainly due to increased purchases from Mexico (USD 816 million or 14.3%), Thailand (USD 687 million or 67.8%), and India (USD 521 million or 150%).

US Air Freight Transport Industry Overview

The US air freight transport market landscape is fragmented, with a mix of regional and international players. Key players in the market include DHL, United Parcel Services Inc., Expeditors International, Hellmann Worldwide Logistics, DB Schenker, etc.

As companies embrace technology-driven solutions and seek efficient distribution channels, they find themselves strategically positioned to seize emerging opportunities in the industry.

As of October 2024, DHL Express and DHL Global Forwarding are advancing their sustainability initiatives by renewing a contract with IAG Cargo, the cargo handling arm of International Airlines Group (IAG). This partnership will see the use of an extra 60 million liters of Sustainable Aviation Fuel (SAF) for DHL's operations. Spanning the years 2024 and 2025, the renewed contract is projected to cut down greenhouse gas emissions by roughly 165,000 metric tons of CO2e.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Market

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Surge in cross border trade relations driving the market

- 4.2.1.2 The market is significantly driven by economic growth

- 4.2.2 Restraints

- 4.2.2.1 Geopolitical factors hindering the market

- 4.2.2.2 Consumer Behaviour affecting the market

- 4.2.3 Opportunities

- 4.2.3.1 Technological advancements driving the market

- 4.2.1 Drivers

- 4.3 Government Initiatives and Regulations

- 4.4 Supply Chain/Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitute Products

- 4.5.5 Degree Of Competition

- 4.6 Technology Snapshot and Digital Trends

- 4.7 Spotlight on Key Commodities Transported by Air

- 4.8 Elaboration on Air Freight Rates

- 4.9 Spotlight on Heavy Cargo/Project Logistics in the Air Cargo Industry

- 4.10 Insights into Key Ground Handling Equipment in Airports

- 4.11 Review and Commentary on Standards and Regulations on the Safe Transport of Dangerous Goods

- 4.12 Brief on Cold Chain Logistics in the Air Cargo Sector

- 4.13 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Freight Transport (Cargo and Mail)

- 5.1.2 Freight Forwarding

- 5.1.3 Other Value-added Services

- 5.2 By Service

- 5.2.1 Forwarding

- 5.2.2 Airlines

- 5.2.3 Mail

- 5.2.4 Other Services

- 5.3 By Destination

- 5.3.1 Domestic

- 5.3.2 International

- 5.4 By Carrier Type

- 5.4.1 Belly Cargo

- 5.4.2 Freighter

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 DHL

- 6.2.2 United Parcel Services Inc.

- 6.2.3 Expeditors International

- 6.2.4 Hellmann Worldwide Logistics

- 6.2.5 DB Schenker

- 6.2.6 Kuehne + Nagel

- 6.2.7 DSV

- 6.2.8 Nippon Express

- 6.2.9 Kerry Logistics

- 6.2.10 Ceva Logistics*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity, Contribution of the Transport and Storage Sector to Economy)

- 8.2 External Trade Statistics - Exports and Imports, by Product

- 8.3 Insights into the Key Export Destinations and Import Origin Countries