ラテンアメリカの航空貨物産業:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Latin America Air Freight Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690841

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

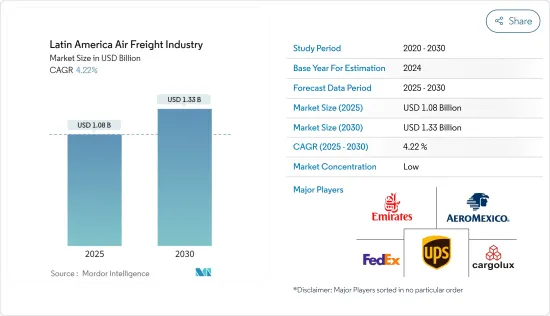

ラテンアメリカの航空貨物産業は、2025年の10億8,000万米ドルから2030年には13億3,000万米ドルに成長し、予測期間(2025-2030年)のCAGRは4.22%となる見込みです。

ラテンアメリカの航空貿易は、輸送能力の増強と新鮮なラテンアメリカ産生鮮品の世界の需要に伴って成長しています。しかし、旧態依然とした規制やインフラの伸び悩みが、ラテン南北アメリカがその潜在能力をフルに発揮する妨げとなっています。

業界の専門家によると、2022年8月、この地域の航空会社の貨物量は2021年8月と比較して9.0%増加しました。他の地域の中でも、ラテンアメリカは著しい成長率を示しました。この成長の主な要因は、新規路線とキャパシティーの提供です。また、同地域では今後数ヶ月間、航空貨物用の航空機への投資が増えると予想されます。輸送能力は24.3%増加しました。

前年比で最も堅調だったのはラテンアメリカの航空会社で、2022年から2023年にかけての国際線需要は1.9%増に対し2.0%増となりました。キャパシティも13.2%増(国際線は16.9%増)と大幅に増加しました。

航空貨物部門は、航空機の欠航、路線の削減、需要の落ち込みなど、いくつかの困難に見舞われています。一部の世界の航空貨物会社は、パンデミック(世界的大流行)と比較して需要が低迷していることを示しています。

過去2年間を特徴付けた消費者需要の活況とは対照的に、航空貨物部門は現在、時期に関係なく、顧客需要の減少に直面しています。いくつかの事情により、航空貨物会社は2022年の第4四半期は低迷すると予想しています。サプライチェーンの寸断、戦争の長期化、世界経済の減速、世界同時不況の可能性などです。

ラテンアメリカの航空貨物産業の市場動向

eコマースの成長により輸送サービスが増加

業界の専門家によると、国境を越えたeコマースは、物流業者にとって大きなビジネスチャンスのひとつです。この業界では、最新技術を活用し、不正防止ソリューションや認証技術を開発するための技術革新が継続的に行われており、重要なプレーヤー、加盟店、銀行は、本人認証のための生体認証データなどのソリューションを活用することで、オンラインショッピング利用者を識別できるようになっています。この成長の背景にはいくつかの要因があるが、最も重要なのは、購買を行うミレニアル世代の多さとスマートフォンの大量普及です。

ラテンアメリカでは、ソーシャル・コマースがeコマースを追い越し始めています。ブラジル、コロンビア、メキシコで実施された世論調査では、ラテンアメリカの買い物客の半数以上がソーシャル・コマースを利用していました。ソーシャル・コマースを、企業の公式サイトやアマゾン、ラッピ、メルカドリブレのようなマーケットプレース・サイトのような従来のeコマースと比較すると、ラテンアメリカでは後者が台頭しています。

専門家によると、ブラジル、コロンビア、メキシコの顧客の40%以上が、ソーシャルコマースの重要な利点として、支払い方法の選択肢が増えたことを挙げています。アルゼンチン、コロンビア、メキシコのソーシャルコマースの3分の1近くは、コンビニエンスストアの通貨クーポンを利用しています。これは、銀行振込、カード、PayPalに依存する以外に、技術に精通したソーシャルメディア・ユーザーでさえも、好ましい支払いオプションとして現金を好んでいることを示しています。2023年、2022年9月と比べ、南米の航空会社の貨物量は2.3%増加しました。前月と比較すると、6.2%の大幅な減少でした。2023年9月の輸送能力は、2022年の同月比で14.4%増加しました。

航空貨物産業の成長にとって重要な市場として発展するブラジル

ブラジルの税関・国境規制による航空貨物への支援は、2022年のE-freight Friendliness Index(EFFI)で世界第52位にランクされました。ブラジルの航空貨物輸送市場は、国内外への製品の移動における驚異的なスピードと安全性など、そのさまざまな利点により、大幅な成長を遂げています。

米国は、強固な商業関係と共同繁栄へのコミットメントにより、ブラジルにとって第2位の貿易相手国です。米国ブランドや製品に対する現地での需要が高いにもかかわらず、国内の法律や税制が複雑なため、輸出業者にとってはしばしば困難が伴います。したがって、ブラジルで輸出を成功させるには、現地の市場動向や規制について深い知識を持つことが不可欠です。ブラジルは2023年に米国から391億2,200万米ドル相当の商品を輸出し、448億800万米ドル相当の商品を輸入しています。

航空貨物の重要な利点の一つは、その信頼性です。天候がフライトスケジュールに影響することがあっても、毎日フライトがあるため、次のフライトに簡単に搭乗することができます。貨物の混載は、知識豊富な航空貨物フォワーディング・ビジネスによって支援されるかもしれないです。空港ターミナルでの集荷、通関、貨物配送、手頃な航空会社料金を組み合わせることで、物流管理を簡素化することができます。ベンダーはこの方法で、より迅速な輸送に集中することができます。

ラテンアメリカの航空貨物産業概要

ラテンアメリカの航空貨物産業は適度に断片化されています。しかし、この業界はフェデックス、UPS、エミレーツ航空などの大手企業によって支配されています。航空貨物輸送サービスに対する需要の高まりは、航空貨物サービスプロバイダーに新たな課題をもたらしました。eコマースもまた、航空貨物をサプライチェーン全体の可視性と透明性の向上に向けて後押ししており、ブラジルが最も重要な市場となっています。アズールのような企業は、アマゾンのような電子小売業者との提携や協力を通じて、同国でのプレゼンス拡大に注力しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析方法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場概要

- 市場力学

- 促進要因

- 新規航空路線の拡大と輸送能力の増強

- 温度変化に敏感な製品の恒常的な輸送ニーズ

- 抑制要因

- 市場の不確実性

- 機会

- 複数のソフトウェア・ソリューションの導入

- 促進要因

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 政府の規制と取り組み

- サプライチェーン/バリューチェーン分析

- 技術スナップショットとデジタル動向

- 航空輸送される主要商品のスポットライト

- 航空貨物運賃の詳細

- 空港の主要地上処理設備に関する洞察

- 危険物の安全輸送に関する基準と規制のレビューと解説

- 航空貨物セクターにおけるコールドチェーンロジスティクスの概要

- COVID-19が市場に与える影響

第5章 市場セグメンテーション

- サービス別

- 輸送

- フォワーディング

- その他のサービス

- 仕向地別

- 国内

- 国際

- キャリアタイプ別

- ベリーカーゴ

- 貨物船

- 国別

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- その他ラテンアメリカ

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- FedEx(Federal Express)

- United Parcel Service

- Emirates Skycargo

- Aeromexico

- Cargolux

- LATAM Cargo

- Qatar Airways

- Azul Cargo Express

- Kuehne+Nagel

- IAG Cargo

- Avianca Cargo

- DHL

- United Airlines

- American Airlines

- Delta Airlines

- Copa Airlines*

- その他の企業

第7章 市場機会と今後の動向

第8章 付録

目次

The Latin America Air Freight Industry is expected to grow from USD 1.08 billion in 2025 to USD 1.33 billion by 2030, at a CAGR of 4.22% during the forecast period (2025-2030).

The air trade in Latin America is growing with increased capacity addition and demand for fresh Latin American perishable goods across the globe. However, the archaic regulations and slow growth in infrastructure are hindering the continent from realizing its full potential.

As per the industry experts, in August 2022, the region had a 9.0% increase in freight volumes for airlines compared to August 2021. Among other areas, Latin America witnessed a significant growth rate. The growth is mainly attributed to the offering of new routes and capacity. The region is also expected to invest more in aircraft for air cargo in the upcoming months. The capacity increased by 24.3%.

The most robust year-on-year performance was achieved by Latin American carriers, with a 2.0% increase in demand for international operations between 2022 and 2023 compared to +1.9%. Capacity also significantly increased by 13.2% (+16.9% for international operations).

The air freight sector is experiencing several difficulties, including planes being grounded, routes being cut, and a drop in demand. Certain global air freight corporations indicate a slackened demand compared to the pandemic.

In contrast to the booming consumer demand that characterized the preceding two years, the air freight sector is currently facing a decline in customer demand, notwithstanding the time of year. Due to several circumstances, air freight companies anticipate a subdued fourth quarter in 2022. These included the broken supply chain, the protracted war, the slowdown of the world economy, and the possibility of a worldwide recession.

Latin America Air Freight Industry Market Trends

Growth of E-commerce Increases The Transport Service

As per industry experts, cross-border e-commerce is one of the significant opportunities for logistics providers due to the lower density of physical retail space, limited product availability, high penetration of smartphones, and purchase savings throughout the region. The industry continuously innovates to leverage the latest technologies and develop fraud protection solutions and authentication technologies that allow vital players, merchants, and banks to identify online shoppers by leveraging solutions such as biometric data for identity authentication. Several factors are behind this growth, the most important being the large numbers of millennials making purchases and the massive proliferation of smartphones.

In Latin America, social commerce is starting to overtake e-commerce. More than half of the Latin American shoppers polled in Brazil, Colombia, and Mexico engaged in social commerce. Comparing social commerce to traditional e-commerce, such as official corporate websites or marketplace websites like Amazon, Rappi, or MercadoLibre, the latter is gaining ground in Latin America.

More than 40% of customers from Brazil, Colombia, and Mexico cited the increased selection of payment options as a critical advantage of social commerce, as per experts. Nearly one-third of social commerce transactions in Argentina, Colombia, and Mexico involved currency coupons from convenience stores. It demonstrates that, besides relying on bank transfers, cards, and PayPal, even tech-savvy social media users favor cash as their preferred payment option. In 2023, compared to September 2022, the cargo volume increased by 2.3% for South American carriers. Compared to the previous month, this was a significant decrease in performance by 6.2%. In September 2023, capacity increased by 14.4% compared with the corresponding month in 2022.

Brazil Evolving As An Important Market For The Growth In The Air Freight Industry

Brazil's assistance of air cargo through its customs and border regulations ranked 52nd in the E-freight Friendliness Index (EFFI) globally in 2022. The air cargo transportation market has grown considerably in the country due to its various benefits, such as incredible speed and safety in the movement of products inside and outside the country.

The United States is Brazil's second-largest trading partner due to a solid commercial relationship and a commitment to joint prosperity. The complexity of domestic legislation and tax rules frequently makes it difficult for exporters despite the high local demand for U.S. brands and products. To achieve export success in Brazil, it is therefore essential to have an in-depth knowledge of local market trends and regulations. Brazil exported goods worth USD 39,122 million and imported goods worth USD 44,808 million in 2023 from the US.

One of the critical advantages of air freight is its dependability. Even though weather conditions can affect flight schedules, the availability of daily flights makes it simple to board the following trip. Consolidating shipments might be assisted by a knowledgeable air freight forwarding business. Combining airport terminal pickup, customs brokerage, cargo delivery, and affordable air carrier rates can help simplify logistics administration. Vendors can then concentrate more on expedited shipping in this fashion.

Latin America Air Freight Industry Industry Overview

The Latin American air freight industry is moderately fragmented. However, the industry is dominated by major players like FedEx, UPS, Emirates, and many more. The growing demand for air freight transportation services has opened new challenges for air cargo service providers. E-commerce also pushes air cargo toward greater visibility and transparency throughout the supply chain, with Brazil being the most significant market. Companies like Azul focus on expanding their presence in the country via collaborations and partnerships with e-retailers like Amazon.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Method

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Overview

- 4.3 Market Dynamics

- 4.3.1 Drivers

- 4.3.1.1 Extension of new air routes and capacity

- 4.3.1.2 Constant Need to Transport Temperature-Sensitive Products

- 4.3.2 Restraints

- 4.3.2.1 Market Uncertainty

- 4.3.3 Opportunities

- 4.3.3.1 Implementation of Several Software Solutions

- 4.3.1 Drivers

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Government Regulations and Initiatives

- 4.7 Supply Chain/Value Chain Analysis

- 4.8 Technology Snapshot and Digital Trends

- 4.9 Spotlight on Key Commodities Transported by Air

- 4.10 Elaboration on Air Freight Rates

- 4.11 Insights into Key Ground Handling Equipment in Airports

- 4.12 Review and Commentary on Standards and Regulations on the Safe Transport of Dangerous Goods

- 4.13 Brief on Cold Chain Logistics in the Air Cargo Sector

- 4.14 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Services

- 5.1.1 Transport

- 5.1.2 Forwarding

- 5.1.3 Other Services

- 5.2 By Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 By Carrier Type

- 5.3.1 Belly Cargo

- 5.3.2 Freighter

- 5.4 By Country

- 5.4.1 Brazil

- 5.4.2 Mexico

- 5.4.3 Argentina

- 5.4.4 Colombia

- 5.4.5 Rest of Latin America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 FedEx (Federal Express)

- 6.2.2 United Parcel Service

- 6.2.3 Emirates Skycargo

- 6.2.4 Aeromexico

- 6.2.5 Cargolux

- 6.2.6 LATAM Cargo

- 6.2.7 Qatar Airways

- 6.2.8 Azul Cargo Express

- 6.2.9 Kuehne + Nagel

- 6.2.10 IAG Cargo

- 6.2.11 Avianca Cargo

- 6.2.12 DHL

- 6.2.13 United Airlines

- 6.2.14 American Airlines

- 6.2.15 Delta Airlines

- 6.2.16 Copa Airlines*

- 6.3 Other Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日