砂糖包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Sugar Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1630428

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

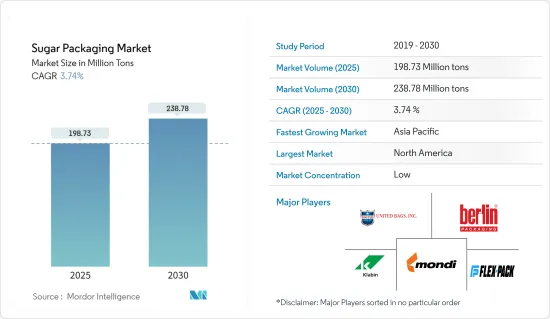

砂糖包装の市場規模は2025年に1億9,873万トンと推定され、予測期間(2025-2030年)のCAGRは3.74%で、2030年には2億3,878万トンに達すると予測されます。

主なハイライト

- 砂糖はバルクと小売の両方の目的で様々な形態で包装されているため、市場は特にフレキシブル包装への顕著なシフトを目の当たりにしています。アクティブ包装やスマート包装といった包装技術の革新のおかげで、砂糖のフレキシブル包装は実現可能であるだけでなく、賞味期限を延ばすこともできます。

- 有機砂糖や特殊砂糖の需要が高まるにつれ、特殊包装の必要性が高まっています。これにより、輸送中や保管中にこれらの高価値製品の保護が保証されます。さらに、貿易が世界化するにつれ、異なる国や地域の多様な要件を満たす標準化されたパッケージング・ソリューションが急務となっています。

- USDAによると、オーストラリアの砂糖生産量は緩やかに増加し、2022年と2023年には440万トンに達します。2022/23年のサトウキビ生産量は3,300万トンと推定されます。この生産量の増加は、収穫面積の拡大と関連しており、収穫面積は5,000ヘクタール増加し、35万ヘクタールに達しました。

- 健康志向が高まる市場において、砂糖のマーケティングは大きなハードルを乗り越えています。消費者は知らず知らずのうちに糖分の多い製品を選んでいるかもしれないが、未加工の砂糖を購入する際には複数の要素を考慮します。その結果、砂糖袋市場は、砂糖の魅力を高め、使いやすさを確保するために、革新的なパッケージング・ソリューションに多額の投資を行っています。

- 紙袋の主な素材である紙は、手頃な価格で入手しやすいです。しかし、紙袋に入った砂糖はダメージを受けやすいです。しかし、紙袋に入った砂糖は傷みやすく、迅速で便利な輸送を可能にします。その防水性と防湿性は、大きな利点として際立っています。さらに、紙袋は販売、保管、消費を簡素化します。さらに、紙袋は分解性が高いため、エコロジカル・フットプリントを最小限に抑えることができます。

- 着色された錫の鉄は、鉄の箱の包装材料として好まれています。円筒形、長方形、楕円形、五角形などの形があるこれらの箱は、その耐久性、確実な密封性、耐破損性で有名です。鉄の箱の包装の明るい外観と鮮やかな色は、砂糖の魅力を高めるだけでなく、その頑丈さを強調します。砂糖に限らず、鉄製ボックスはお菓子のパッケージにもよく使われ、多くの大手パッケージング・ギフト・お菓子メーカーが製品の品質を示すために活用しています。

- ビニール袋は砂糖包装の頂点に君臨し、最も一般的に使用されるオプションです。防湿性、防水性に優れ、費用対効果も高いため、人気があります。砂糖の生産者は、透明なものと色つきのもの両方があるこれらの袋を選ぶことが多いです。特にカラフルなラップは、砂糖の視覚的魅力を高めることができ、老舗菓子メーカーも新進菓子メーカーもこの戦略を採用しています。しかし、大きな懸念が立ちはだかる。これらのプラスチック袋は、深刻化するプラスチック汚染の一因となっているのです。砂糖包装機はプラスチック袋と紙袋の両方を巧みに扱い、最新技術によって安定した性能を約束するため、多用途性が光る。

砂糖包装市場の動向

プラスチック素材が大きな市場シェアを占める

- Nichrome Packaging Solutionsによると、プラスチック包装はその比類ない機能性により大きな市場シェアを占めています。プラスチックソリューションの中でも、軟質プラスチック包装は硬質プラスチック包装に比べて原材料の使用量が70%少ないことが特徴です。

- 2023年4月にFeedback Organizationが報告したように、スーパーマーケットは主要な砂糖販売業者として英国市場を独占しています。これらの小売業者はかつて、単に消費者の需要に応えるだけだと主張していたが、それ以来、この姿勢を放棄しています。調査は一貫して、スーパーマーケットの「小売業者力」にスポットを当ててきました。スーパーマーケットは、食品生産者と消費者の橋渡しをする仲介業者です。その支配力は、供給者と顧客の双方を制限し、食品の売買における選択肢を狭めています。この影響力は、わずか5社のスーパーマーケットが小売市場シェアの75%以上を支配していることからも明らかです。スーパーマーケットは、その「バイヤー・パワー」を活用し、サプライヤーに条件を指示し、在庫の選択、品質、量、包装、価格決定に影響を与えます。このダイナミズムは、プロクター・アンド・ギャンブル、ネスレ、ユニリーバのような業界大手にも当てはまる。スーパーマーケットが砂糖の売上を伸ばすと同時に、砂糖のパッケージ、特にパウチや小袋のような柔軟な形態のパッケージの需要も高めています。クイックサービスレストランやコーヒーショップの成長は、砂糖小袋の需要をさらに増大させています。

- 耐湿性、費用対効果、色や透明性によるブランディングの可能性から砂糖メーカーに支持され、フレキシブルなプラスチック袋で砂糖を包装する傾向が強まっています。

- にもかかわらず、市場関係者はプラスチック包装の代替品に関心を寄せています。バイオプラスチックの採用が増加しており、従来のプラスチック包装に対する大きな課題となっています。予測期間中、リサイクル可能で再生可能な素材がプラスチック包装に取って代わる可能性があります。

- Logistex Ltd.は、コンテナによるブラジルの砂糖輸出が、「コンテナ・エルゲドン」運動の影響を受け、2年間の小康状態を経て、2023年に回復することを強調しています。この出荷量の増加は、ブラジルの砂糖生産量の増加と海上運賃の低下と一致しています。さらに、世界の他の主要砂糖生産国が直面した課題によって、ブラジルの市場リーダーシップはさらに強固なものとなった。

- 逆に、インドは収穫の課題に直面し、特にエタノール生産へのシフトに伴い、砂糖輸出市場への再参入をためらっていました。このため、ブラジルが優位性を主張する道が開かれたのです。国内生産者はバルク輸送を好んだが、コンテナ輸送は依然として輸出に不可欠であり、しばしば複雑な交渉や高付加価値を伴う。

- 2023年、ブラジルの砂糖のコンテナ輸出量は294万トンに達したと、海事代理店ウィリアムズは指摘しています。これはブラジルの総輸出量の9.4%を占め、前年比90.1%増という著しい伸びを示しました。この数字は、総出荷量の10.7%を占めた2017年のピーク298万トンに並ぶ勢いだった。コンテナへの積み込みの前に、これらの砂糖は通常、ジュートなどの天然素材やプラスチックで編まれたフレキシブルな袋やサックに梱包され、プラスチック製の内張りが施されることが多いです。

アジア太平洋地域が最も高い成長を遂げる

- アジア太平洋地域は、食品包装とブランド化における顕著な技術革新によって成長をリードしています。さらに、この地域の消費者は砂糖菓子類の贅沢な体験に高い価値を置いています。

- 人口の増加、所得水準の向上、ライフスタイルの進化、メディアの影響力の高まり、堅調な経済が包装需要を煽っています。この分野は、この地域で最も重要で急速に拡大している分野のひとつです。特に、インドの大手格付け会社であるCare Ratingsは、インドの紙生産量の49%以上がパッケージング専用であることを強調しています。

- アジア太平洋地域、特に飲食品分野では、いくつかの規制が包装業界を監督しています。主な規制には、1956年食品混入防止法、2011年プラスチック廃棄物(管理および取り扱い)規則、2011年食品安全基準(包装および表示)規則などがあります。

- 食品分野での紙・パルプ使用に関する規制が予想され、市場を押し上げる構えです。例えば、インドの食品安全基準局は、食品包装における紙の役割を強化することを目的とした新しい包装規制を展開しました。さらに、BIS規格IS 4664:1986は食品包装に再生パルプを使用することを認めており、インドの砂糖包装における紙の存在感を高めることになります。

- 米国農務省対外農業サービスによると、2023/2024年サイクルのインドの砂糖生産量は約3,400万トンです。インドの砂糖生産は長年に渡り浮き沈みがあるもの、ブラジルに次ぐ世界第2位の砂糖生産国であることに誇りを持っています。2023-2024年サイクルで、インドの内閣経済委員会(CCEA)は、ジュート包装を重視する新基準を承認しました。具体的には、2023-24年のジュート年基準では、食品穀物包装の100%と砂糖包装の20%にジュート袋を使用することが義務付けられています。

砂糖包装業界の概要

本調査では、砂糖の生産量を素材タイプと製品タイプに基づいて世界的に考察しています。砂糖はバルクと小売の両方で様々な形態で包装されるため、フレキシブル包装へのシフトが顕著です。アクティブパッケージングのような新技術は、この傾向を促進するだけでなく、砂糖の貯蔵寿命を延ばします。プラスチックは、その比類ない機能性により包装市場を独占しています。フレキシブル・プラスチック包装は、プラスチック・ソリューションの中でも際立っており、リジッド包装に比べ原材料の使用量が70%少ないです。

砂糖包装市場は適度に断片化されています。市場のプレーヤーは、シェアを拡大し収益を増大させるために、幅広い製品のカスタマイズを提供しています。主なプレーヤーとしては、Mondi Group、United Bags Inc、FlexPack、Klabin S.A.、Berlin Packagingなどが挙げられます。各社は、ニーズの高まりにより、この市場でのイノベーションを通じて持続可能な競争優位性を獲得しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- インド、中国、EU地域などの主要国における砂糖消費量の着実な増加

- カスタマイズされた包装形態と持続可能な素材に対する需要の高まり

- 市場抑制要因

- メーカーが直面する運用面および規制面の懸念

第6章 市場セグメンテーション

- 製品タイプ別

- 軟包装

- 袋およびパウチ

- 小袋

- 袋

- その他の軟包装

- 硬包装

- 瓶と容器

- 軟包装

- 材料別

- プラスチック

- 紙

- その他の材料

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- アジア

- インド

- 中国

- 日本

- タイ

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Mondi Group

- United Bags Inc.

- FLexPack

- Berlin Packaging

- Grupo Bio Pappel

- Swiss Pack Limited

- Packman Industries

- TedPack Company Limited

- Klabin S.A.

- Shri Salasar Plastics

第8章 投資分析

第9章 市場の将来

目次

The Sugar Packaging Market size is estimated at 198.73 million tons in 2025, and is expected to reach 238.78 million tons by 2030, at a CAGR of 3.74% during the forecast period (2025-2030).

Key Highlights

- The market is witnessing a notable shift towards flexible packaging, especially as sugar is being packaged in various formats for both bulk and retail purposes. Thanks to innovations in packaging technologies, such as active and smart packaging, flexible packaging for sugar is not only feasible but also extends its shelf life.

- With the rising demand for organic and specialty sugars, there's an increasing need for specialized packaging. This ensures the protection of these high-value products during transportation and storage. Moreover, as trade becomes more globalized, there's a pressing need for standardized packaging solutions that meet the varied requirements of different countries and regions.

- According to USDA, Australia's sugar production is set to see a modest rise, reaching 4.4 million tons for the years 2022 and 2023. In the 2022/23 cycle, sugarcane production is estimated at 33.0 million tons. This increase in output is linked to an expansion in the harvested area, which has grown by 5,000 hectares to reach 350,000 hectares.

- In a market increasingly focused on health, sugar marketing is navigating significant hurdles. While consumers might unknowingly choose products high in sugar, they consider multiple factors when purchasing unprocessed sugar. As a result, the sugar bag market is heavily investing in innovative packaging solutions to boost sugar's appeal and ensure user-friendliness.

- Paper, the go-to material for paper bags, is both affordable and easily sourced. Yet, sugar in paper bags is more prone to damage. Despite this vulnerability, paper bags enable quick and convenient transportation. Their waterproof and moisture-proof qualities stand out as significant advantages. Moreover, paper bags simplify selling, storage, and consumption. An added environmental perk of using paper for bags is its degradability, leading to a minimal ecological footprint.

- Tinted tin iron is the favored material for packaging in iron boxes. These boxes, available in shapes like cylinders, rectangles, ovals, and pentagons, are celebrated for their durability, secure sealing, and damage resistance. The bright appearance and vibrant colors of iron box packaging not only enhance sugar's appeal but also underscore its robustness. Beyond sugar, these iron boxes are a go-to for candy packaging, with many leading packaging, gift, and candy producers leveraging them to signify product quality.

- Plastic bags reign supreme in sugar packaging, being the most commonly used option. Their moisture-proof and waterproof nature, combined with cost-effectiveness, makes them a favorite. Sugar producers often opt for these bags, available in both transparent and colored variants. Colorful wraps, especially, can elevate sugar's visual allure, a strategy embraced by both established and budding confectionery makers. Yet, a major concern looms: these plastic bags contribute to the growing issue of plastic pollution. Versatility shines through as sugar packing machines adeptly handle both plastic and paper bags, and with modern technology, they promise consistent performance.

Sugar Packaging Market Trends

Plastic Material to Hold Significant Market Share

- According to Nichrome Packaging Solutions, plastic packaging holds a significant market share due to its unparalleled functionality. Among plastic solutions, flexible plastic packaging is notable for using 70% less raw material than its rigid counterpart.

- As reported by Feedback Organization in April 2023, supermarkets dominate the UK market as primary sugar sellers. While these retailers once claimed to merely respond to consumer demand, they've since abandoned this stance. Research has consistently spotlighted the 'retailer power' of supermarkets. Acting as intermediaries, they bridge food producers and consumers. Their dominance restricts both suppliers and customers, curtailing choices in buying and selling food. This influence is evident as just five supermarkets control over 75% of the retail market share. Leveraging their 'buyer power', supermarkets dictate terms to suppliers, influencing stock selection, quality, quantity, packaging, and pricing decisions. This dynamic holds even for industry giants like Procter & Gamble, Nestle, and Unilever. With supermarkets bolstering sugar sales, they're simultaneously driving up demand for sugar packaging, especially in flexible formats like pouches and sachets. The growth of quick-service restaurants and coffee shops has further amplified the demand for sugar sachets.

- There's a growing trend of packaging sugar in flexible plastic bags, favored by sugar manufacturers for their moisture resistance, cost-effectiveness, and branding potential through color or transparency.

- Despite this, market players are gravitating towards alternatives to plastic packaging. The rising adoption of bioplastics poses a significant challenge to traditional plastic packaging in the industry. Over the forecast period, recyclable and renewable materials are poised to potentially replace plastic packaging.

- Logistex Ltd. highlights a rebound in Brazilian sugar exports via containers in 2023, after a two-year lull, influenced by the "containergeddon" movement. This increase in shipments coincided with a rise in Brazil's sugar production and a decline in seafreight rates. Additionally, challenges faced by other major global sugar producers further cemented Brazil's market leadership.

- Conversely, India faced harvest challenges and was hesitant to re-enter the sugar export market, especially with its shift towards ethanol production. This opened the door for Brazil to assert its dominance. While national producers favored bulk shipping, container shipments remained vital for exports, often involving intricate negotiations and higher value additions.

- In 2023, Brazil's containerized sugar exports reached 2.94 million tons, as noted by maritime agency Williams. This constituted 9.4% of Brazil's total exports and marked a remarkable 90.1% increase from previous years. The figure was on the verge of matching the 2017 peak of 2.98 million tons, which represented 10.7% of total shipments. Before container loading, these sugars are typically packaged in flexible bags or sacks made from woven natural materials like jute or woven plastic, frequently featuring a plastic inner lining.

Asia-Pacific to Witness Highest Growth

- The Asia-Pacific region leads in growth, driven by notable innovations in food packaging and branding. Additionally, consumers in this region place a high value on the indulgent experience of sugar confectionery.

- Rising population, increasing income levels, evolving lifestyles, heightened media influence, and a robust economy are fueling the demand for packaging. This sector stands out as one of the most vital and rapidly expanding in the region. Notably, Care Ratings, a leading credit rating agency in India, highlights that over 49% of the country's paper production is dedicated to packaging.

- Several regulations oversee the packaging industry in the Asia-Pacific, particularly in the food and beverage sectors. Key regulations include the Prevention of Food Adulteration Act of 1956, the Plastic Waste (Management and Handling) Rules of 2011, and the Food Safety and Standards (Packaging and Labelling) Regulations of 2011.

- Anticipated regulations on paper and pulp usage in the food sector are poised to boost the market. For example, India's Food Safety and Standards Authority has rolled out new packaging regulations, aiming to bolster paper's role in food packaging. Furthermore, the BIS standard IS 4664: 1986, which allows recycled pulp in food packaging, is set to enhance paper's prominence in India's sugar packaging.

- As per the USDA Foreign Agricultural Service, India produced around 34 million metric tons of sugar in the 2023/2024 cycle. While sugar production in India has seen its ups and downs over the years, the nation proudly stands as the world's second-largest sugar producer, trailing only Brazil. In the 2023-2024 cycle, India's Cabinet Committee on Economic Affairs (CCEA) approved new norms emphasizing jute packaging. Specifically, the 2023-24 Jute Year norms mandate that jute bags must be used for 100% of food grains and 20% of sugar packaging.

Sugar Packaging Industry Overview

The study considers sugar production globally based on material type and product type. As sugar is packaged in various formats for both bulk and retail, there's been a notable shift towards flexible packaging. New technologies, like active packaging, not only facilitate this trend but also extend the shelf life of sugar. Plastic dominates the packaging market due to its unmatched functionality. Flexible plastic packaging stands out among plastic solutions, utilizing 70% less raw material than its rigid counterpart.

The sugar packaging market is moderately fragmented. Players in the market are offering extensive product customization to increase their share and augment their revenue. Some of the key players are Mondi Group, United Bags Inc, FlexPack, Klabin S.A., Berlin Packaging and more. The companies have a sustainable competitive advantage through innovations in this market, owing to the growing need.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Steady Increase in the Consumption of Sugar in Major Countries such as India, China and EU Regions

- 5.1.2 Rising Demand for Customized Packaging Formats and Sustainable Materials

- 5.2 Market Restraints

- 5.2.1 Operational and Regulatory Concerns Faced by the Manufacturers

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Flexible Packaging

- 6.1.1.1 Bags and Pouches

- 6.1.1.2 Sachets

- 6.1.1.3 Sacks

- 6.1.1.4 Other Flexible Packaging Types

- 6.1.2 Rigid Packaging

- 6.1.2.1 Jars and Containers

- 6.1.1 Flexible Packaging

- 6.2 By Material Type

- 6.2.1 Platsic

- 6.2.2 Paper

- 6.2.3 Other Material Type

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.3 Asia

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Thailand

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Mondi Group

- 7.1.2 United Bags Inc.

- 7.1.3 FLexPack

- 7.1.4 Berlin Packaging

- 7.1.5 Grupo Bio Pappel

- 7.1.6 Swiss Pack Limited

- 7.1.7 Packman Industries

- 7.1.8 TedPack Company Limited

- 7.1.9 Klabin S.A.

- 7.1.10 Shri Salasar Plastics

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日