中国のデジタル貨物輸送:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

China Digital Freight Forwarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1630392

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

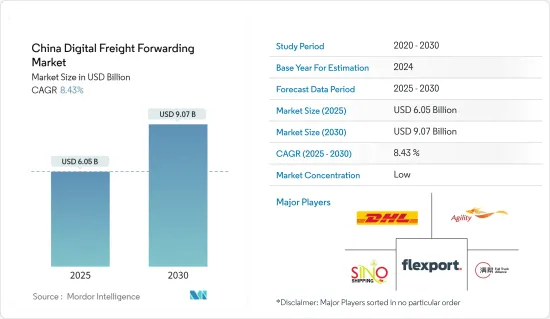

中国のデジタル貨物輸送市場規模は2025年に60億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.43%で、2030年には90億7,000万米ドルに達すると予測されます。

中国のデジタル貨物輸送市場分析は、中国国内における従来の貨物輸送プロセスを合理化・強化するためのデジタル技術の応用に焦点を当てています。貨物輸送は、海上、航空、鉄道、トラックなどの輸送モードを利用し、荷主に代わって国境を越えた貨物の出荷を組織化し、促進することを含みます。オンラインプラットフォーム、ソフトウェア、先進的データ分析を採用することで、中国のデジタル貨物輸送はこのプロセスを近代化し、輸送のさまざまな側面を最適化しています。

近年、中国のデジタル貨物輸送市場は、2023年に中国交通運輸省が言及したように、eコマース・ブームとリアルタイムロジスティクスソリューションに対する需要の高まりによって、著しい成長を遂げています。

中国政府によると、2023年には上海、深セン、寧波・舟山が最もコンテナ取扱量の多い港湾として世界をリードし、上海の取扱量は3,600万TEUを超え、寧波・舟山が3,500万TEUで僅差で続き、深センは2,700万TEUを超えました。この急増は、中国の経済回復と港湾インフラの拡大を浮き彫りにし、地域貿易と世界貿易の両方を後押ししています。2023年9月までに、中国の港湾は合計で2億3,000万TEUを超え、前年比5.2%増となります。中国のデジタル貨物輸送市場が拡大するにつれて、国内外の企業が技術を活用して業務を最適化し、コストを削減しています。

中国のデジタル貨物輸送市場の動向

eコマースセグメントの台頭が市場を牽引

中国のeコマース産業の急成長にはいくつかの要因があります。中国政府は、eコマースとデジタル経済を強化するための一連の施策を展開しており、特にインターネットインフラの強化と起業家精神の促進に重点を置いています。

モバイル技術の進歩とインターネット接続の普及により、eコマースは中国全土で利用可能かつアクセスしやすいものとなり、消費者と事業主双方に利益をもたらしています。さらに、消費者はアリペイやウィーチャットペイといった多様なモバイル決済ソリューションの利便性を享受し、シームレスなオンライン取引を促進しています。

産業専門家によると、2023年には、中国は収益面で世界の貨物輸送市場の6.0%を占める。2030年を展望すると、米国が収益面で世界市場を独占する構えです。アジア太平洋では、中国の貨物輸送市場が2030年までに売上高でトップに立っています。アジア太平洋で最も急成長している市場として認識されているインドは、2030年までに177億3,210万米ドルの評価を達成する勢いです。

航空貨物輸送の増加が市場を牽引する見込み

中国のデジタル貨物輸送市場は、技術の進歩と効率的で費用対効果の高いロジスティクスソリューションへのニーズの高まりにより、急速な変貌を遂げつつあります。同市場は、荷送人と運送事業者の双方によるデジタルプラットフォームとソリューションの採用拡大が追い風となり、今後数年間で大きな成長を遂げる展望です。

産業の専門家によると、航空輸送は最も迅速な輸送手段のひとつであり、生鮮品や緊急配送が必要な高額商品など、一刻を争う商品の輸送に最適だといいます。物流における航空輸送の第一の利点は、配達の速さです。

2023年、中国の越境eコマース製品の輸出入額は2兆3,800億人民元(3,283億米ドル)で、前年比15.6%増加しました。税関総署によると、クロスボーダーeコマース用に輸出された製品だけでも1兆8,300億人民元(2,500億米ドル)に達し、前年比で20%近く増加しました。

中国のデジタル貨物輸送産業概要

本レポートでは、中国のデジタル貨物輸送市場で事業を展開する主要企業を取り上げています。市場競争は激しく、どの参入企業も主要シェアを占めていないです。市場はセグメント化されており、予測期間中に成長すると予想されます。中国のデジタル貨物輸送市場の主要企業には、DHL、Flexport、Agility Logistics、Freightosが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- バリューチェーン/サプライチェーン分析

- 投資シナリオに関する洞察

- 政府の規制と取り組みに関する洞察

- オンライン貨物輸送とデジタルプラットフォームにおける技術開発概要

- 中国におけるeコマース物流と貨物輸送概要

- 地政学とパンデミックが市場に与える影響

第5章 市場力学

- 促進要因

- 政府の一帯一路構想

- 貨物物流における5G技術の統合

- 抑制要因

- 物流市場の細分化

- 地政学的貿易障壁

- 機会

- カーボンニュートラルな物流目標

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 顧客の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第6章 市場セグメンテーション

- 輸送形態別

- 海洋

- 航空

- 道路

- 鉄道

- 企業タイプ別

- 中小企業

- 大企業と政府

第7章 競合情勢

- 市場集中度概要

- 企業プロファイル

- Flexport

- Youtrans

- Full Truck Alliance(Manbang group)

- Agility Logistics Pvt. Ltd(Shipa Freight)

- Twill

- Freightos

- DHL Group

- Kuehne+Nagel International AG

- FreightBro

- Cogoport

- SINO SHIPPING

- DB Schenker

- MOOV

- WICE Logistics*

- その他の企業

第8章 市場の将来展望

第9章 付録

- マクロ経済指標(GDP分布、活動別)

- 経済統計-運輸・倉庫業の経済への貢献

目次

The China Digital Freight Forwarding Market size is estimated at USD 6.05 billion in 2025, and is expected to reach USD 9.07 billion by 2030, at a CAGR of 8.43% during the forecast period (2025-2030).

The China Digital Freight Forwarding Market Analysis focuses on the application of digital technologies to streamline and enhance the traditional freight forwarding process within China. Freight forwarding involves organizing and facilitating the shipment of goods across international borders on behalf of shippers, utilizing ocean, air, rail, or truck transportation modes. By employing online platforms, software, and advanced data analytics, digital freight forwarders in China are modernizing this process, optimizing various facets of shipping.

In recent years, China's digital freight forwarding market has experienced significant growth, driven by e-commerece boom and incresing demand for real-time logistics solutions as mentioned by the Chinese Ministry of Transport in 2023.

According to the Government of China, in 2023, Shanghai, Shenzhen, and Ningbo-Zhoushan led the world as some of the busiest container ports, with Shanghai processing over 36 million TEUs, closely followed by Ningbo-Zhoushan at 35 million TEUs, and Shenzhen surpassing 27 million TEUs. This surge underscores China's economic recovery and its expanding port infrastructure, bolstering both regional and global trade. By September 2023, Chinese ports collectively managed over 230 million TEUs, reflecting a year-on-year uptick of 5.2%. As China's digital freight forwarding market expands, both domestic and international companies are harnessing technology to optimize operations and curtail costs.

China Digital Freight Forwarding Market Trends

Rise in E-Commerce Sector Driving the Market

Several factors have fueled the rapid growth of China's e-commerce industry. The Chinese government has rolled out a series of policies to bolster e-commerce and the digital economy, with a particular focus on enhancing internet infrastructure and promoting entrepreneurship.

With advancements in mobile technology and widespread internet connectivity, e-commerce has become both available and accessible across China, benefiting consumers and business owners alike. Furthermore, residents enjoy the convenience of diverse mobile payment solutions, such as Alipay and WeChat Pay, facilitating seamless online transactions.

According to industry experts, in 2023, China represented 6.0% of the global freight forwarding market in terms of revenue. Looking ahead to 2030, the U.S. is poised to dominate the global market in terms of revenue. Within the Asia Pacific region, China's freight forwarding market is set to take the lead in revenue by 2030. India, recognized as the fastest-growing market in the Asia Pacific, is on track to achieve a valuation of USD 17,732.1 million by 2030.

Increasing Air Cargo Shipments Expected to Drive the Market

The digital freight forwarding market in China is undergoing rapid transformation, driven by technological advancements and the growing need for efficient and cost-effective logistics solutions. The market is expected to achieve significant growth in the coming years, fueled by the increasing adoption of digital platforms and solutions by both shippers and carriers.

According to industrial experts, air transportation is one of the fastest modes of transportation available, making it ideal for transporting time-sensitive products, such as perishable goods and high-value items requiring urgent delivery. The primary advantage of air transport in logistics is the speed of delivery.

In 2023, China's imports and exports of cross-border e-commerce products were worth CNY 2.38 trillion (USD 328.3 billion), up 15.6 percent year-on-year. Products exported for cross-border e-commerce alone reached CNY 1.83 trillion (USD 0.25 trillion), up nearly 20 percent year-on-year, according to the General Administration of Customs.

China Digital Freight Forwarding Industry Overview

The report covers the major players operating in the Chinese digital freight forwarding market. The market is highly competitive, with none of the players occupying the major share. The market is fragmented, and it is expected to grow during the forecast. The major players in the Chinese digital freight forwarding market include DHL, Flexport, Agility Logistics, and Freightos.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Value Chain / Supply Chain Analysis

- 4.3 Insights on Investment Scenarios

- 4.4 Insights on Government Regulations and Initiatives

- 4.5 Brief on Technology Development in Online Freight Forwarding and Digital Platforms

- 4.6 Overview on E-commerce Logistics and Freight Forwarding in China

- 4.7 Impact of Geopolitics and Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Government's Belt and Road Initiative

- 5.1.2 Integration of 5G Technology in Freight Logistics

- 5.2 Restraints

- 5.2.1 Fragmentation in the Logistics Market

- 5.2.2 Geopolitical Trade Barriers

- 5.3 Opportunities

- 5.3.1 Carbon-Neutral Logistics Goals

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Customers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitutes

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Mode of Transportation

- 6.1.1 Ocean

- 6.1.2 Air

- 6.1.3 Road

- 6.1.4 Rail

- 6.2 By Firm Type

- 6.2.1 SMEs

- 6.2.2 Large Enterprises and Governments

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Flexport

- 7.2.2 Youtrans

- 7.2.3 Full Truck Alliance (Manbang group)

- 7.2.4 Agility Logistics Pvt. Ltd (Shipa Freight)

- 7.2.5 Twill

- 7.2.6 Freightos

- 7.2.7 DHL Group

- 7.2.8 Kuehne + Nagel International AG

- 7.2.9 FreightBro

- 7.2.10 Cogoport

- 7.2.11 SINO SHIPPING

- 7.2.12 DB Schenker

- 7.2.13 MOOV

- 7.2.14 WICE Logistics*

- 7.3 Other Companies

8 FUTURE OUTLOOK OF THE MARKET

9 APPENDIX

- 9.1 Macroeconomic Indicators (GDP Distribution, by Activity)

- 9.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日