|

市場調査レポート

商品コード

1628851

アジア太平洋の自動マテリアルハンドリングおよび保管システム:市場シェア分析、産業動向、成長予測(2025年~2030年)Asia Pacific Automated Material Handling And Storage Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の自動マテリアルハンドリングおよび保管システム:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

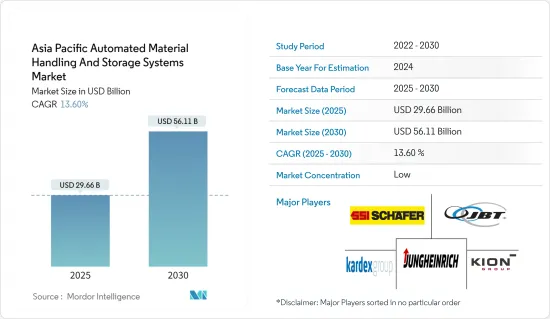

アジア太平洋の自動マテリアルハンドリングと保管システム市場規模は2025年に296億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.6%で、2030年には561億1,000万米ドルに達すると予測されます。

在庫管理単位(SKU)の急速な増加に伴い、卸売業者や流通業者は、十分な情報に基づいた業務上の意思決定を行うことが難しくなっています。このジレンマは、より効率的な労働力、設備、技術活用の差し迫った必要性を強調しています。自動マテリアルハンドリングシステムの必要性を高める主要要因には、コスト削減、労働効率の向上、スペースの最適化などがあります。

市場情勢は、製品タイプの急増と、より頻繁で少量の配送に対する需要を目の当たりにしています。自動化された配送オペレーションは、組織の注文精度を大幅に向上させ、多くの場合、数パーセントのポイント差をつけることができます。アジア太平洋市場の成長を後押ししているのは、都市化、eコマースの急増、技術プロバイダーの存在感です。これらのプロバイダーは、最先端のソリューションを提供し、競合を維持するために研究開発努力を強化しています。

アジア太平洋は世界のeコマース大国としての地位を固めています。この地位は、中国、インド、インドネシアなどの国々で急成長する中間所得層とモバイル機器への嗜好が相まって、この地域の小売eコマースの拡大によって強化されてきました。特に中国は、世界の小売eコマース売上高の40%という驚異的なシェアを誇っています。アジア太平洋のいくつかの国では、倉庫用地の利用可能性が減少しており、多層階施設や、より高く狭い通路へのシフトを促しています。これらの適応は、先進的マテリアルハンドリングシステムに対する需要を促進する態勢を整えています。

マテリアルハンドリングは、機械やロボットがますます個々の作業員に取って代わるようになり、過去70年間に大きな進化を確認してきました。この変革は産業の形を変えただけでなく、企業の成長にも拍車をかけており、特に自動車産業では10倍もの拡大を見せています。ウィスコンシン経済開発公社によれば、インドのような国々はマテリアルハンドリング機器への投資が著しく、MHE市場は同国の建設機械産業の約13%を占めています。タイ、フィリピン、ベトナムなどの東南アジア諸国では、製造業が急増し、雇用が拡大し、可処分所得が増加しています。こうした所得の増加と国際ブランドへの意識の高まりが相まって、現地倉庫の需要に拍車をかけています。

インドネシアは、産業用途でのロボット利用が顕著に増加するなど、自動化を急速に受け入れている国として際立っています。日本が供給国と消費国という2つの役割を担っていることから、インドネシアは貿易活動の活発化から利益を得ることができ、この地域のオートメーション需要をさらに促進します。

世界の産業情勢は、COVID-19の大流行とそれに伴う操業停止により、大きな混乱状況に直面しました。これらの混乱は、サプライチェーンの課題、原料不足、労働力不足、価格の変動、出荷のボトルネックに及んでおり、これらすべてが生産コストを膨張させ、予算を超過する恐れがあった。

アジア太平洋の自動マテリアルハンドリング&保管システム市場動向

組立ラインセグメントが市場の大幅な成長を確認する

- 組立ラインAGVは、自動車製造、馬車製造、航空宇宙、鉄道などの産業で主要用途を見出しています。電気自動車やハイブリッド車の生産台数の増加は、今後数年間で、これらのAGVの需要を促進するように設定されています。このシフトは、メーカーの柔軟性を高めるだけでなく、安全で費用対効果の高いオペレーションを確保しながら、市場の変化に迅速に対応することを可能にします。

- 自動車産業は過去10年間、電気自動車やハイブリッド車の採用よって革命を示しました。この変革は、自動車生産の複雑さを著しく増大させました。進化する安全規制や産業標準と相まって、自動車産業では自動化の必要性が高まっています。主要優先事項には、輸送中の人為的ミスによって引き起こされることの多い製品破損の削減、ワークステーション間でのシャーシハンドリングのスピード向上、組立ライン作業員とのインタラクションの促進などがあります。これらの要件を効果的に満たす組立ラインAGVは、自動車産業における自動化の要となっています。

- さらに、自動車産業では、エンジンやギアボックスから燃料システムやポンプに至るまで、さまざまな部品を製造するために自動組立ラインが活用されています。ロボット工学と視覚技術を活用することで、メーカーは人間工学に基づいた効率的な製品ラインを構築することができ、迅速な組み立てを確保しながら、労働力を危険な状況から守ることができます。その結果、安全への懸念が自動車産業全体の自動化を後押ししています。

- Automotive Skill Development Council(ASDC)の報告書「自動車セクターにおける人的資源とスキル要件(2026年)」によると、インドは2026年までに自動車産業で4,508万人を雇用すると予測されています。この労働力の急増は、現在のスキルセットの再評価を要求しており、自動車設計、ロボット工学、IoT、AIなどのセグメントにおけるスキルアップの必要性を強調しています。伝統的役割が進化するにつれて、産業では自動化への推進が高まっている

- この需要の高まりに対応するため、多くの市場参入企業が製造能力を拡大するだけでなく、新しい製品ラインを導入しています。例えば、北米のオートメーション・エンジニアリングで著名なApplied Manufacturing Technologies(AMT)は、2024年3月、最新のイノベーションであるROBiNを発表しました。ロボット誘導システムと名付けられたROBiNは、倉庫でのマテリアルハンドリングに革命を起こすことを目的とし、効率とスループットの向上を約束します。先進的なマテリアルハンドリングと最先端の自律移動ロボット(AMR)で高い評価を得ているAMTのROBiNは、産業に大きなインパクトを与える準備が整っています。

自動化とマテリアルハンドリングの需要を促進するインダストリー4.0投資

- 空港への投資は、旅行者に時間とお金の両方を使ってもらえるような快適な環境を作ることの価値を各国が理解しているため、世界の評価を得ています。チェックインから搭乗まで、あらゆる規模の空港で普及しているコンベアや仕分けシステムは、プロセスを効果的に合理化し、全体的な顧客体験を向上させます。現在、多くの空港がベンダーと協働して自律型ロボットを導入しているが、これは荷物の移動効率を高めるだけでなく、運営コストを削減する動きでもあります。例えば、ロジスティクスオートメーションのスペシャリストであるヴァンダーランデ・ダッチ社は、最近、香港空港と提携し、自律型手荷物搬送車の検査運用を開始しました。

- インドと中国は、国内航空接続の増加と一人当たりGDPの上昇に牽引され、地域の航空情勢における極めて重要な参入企業として際立っています。ICAOは、アジア太平洋だけで国内航空路線の70%を占めていると指摘しています。

- 予測では、今後数年間、中国の航空市場は力強い成長軌道を描く。特に、中国のトップ3航空会社である中国国際航空、中国南方航空、中国東方航空は、世界ランキングの上昇を目指し、意欲的な機材拡大目標を掲げています。さらに、上海と北京の主要空港は、大規模な拡大構想を積極的に推進しています。

- Chinese Tourism Outbound Research Instituteによると、中国からの出国者数は2030年までに約4億人に達し、世界の出国者数の4分の1を占める可能性があるといいます。この急増に対応するため、空港は先進的なシステムを導入する必要があり、この動きは予測期間を通じて市場の成長をプラスに導くと予想されます。

- 逆に、パンデミックを契機に、多くの空港が旅客検査やウイルス封じ込めにロボットを導入するようになりました。例えば、韓国の仁川空港(Incheon Airport)のスマートエアポート・チームは、ロボット工学と自動運転車両を活用して、移動が困難な乗客(PRM)の体験を向上させています。

アジア太平洋の自動マテリアルハンドリング&貯蔵システム産業概要

アジア太平洋の自動マテリアルハンドリングと保管システム市場は、主にこのセグメントに参入する参入企業が多いため、激しい競合関係にあります。この競争を形成している主要要因には、高い参入障壁、企業集中の進行、市場浸透率の上昇などがあります。市場に参入している主要参入企業には、Kardex Group、KION Group、JBT Corporation、Jungheinrich AG、Daifuku、BEUMER Group GmbH &Co.KGです。

- 2024年2月、著名な世界的フットウェア・アパレルブランドであるSkechers USAは、自動保管・検索システム(ASRS)の主要企業であるハイ・ロボティクスと提携し、東京都港区に最新の物流拠点を開設しました。ハイ・ロボティクスの最先端自動倉庫技術を活用することで、スケッチャーズは倉庫業務を強化し、フルフィルメントを加速させ、正確な注文処理を実現しています。

- 2024年1月、Fujitsu LimitedとYE DIGITAL CORPORATIONは、日本の物流産業における労働力不足に取り組み、サステイナブルサプライチェーンを強化することを目的とした協業を発表しました。このパートナーシップは、物流センターの効率化で知られるFujitsuのWMSサービスと、倉庫業務の自動化を目的としたYE DIGITALのWES MMLogiStationの活用に重点を置いています。Fujitsuは、WMSサービスの提供だけでなく、新規物流センター建設や既存物流センターの業務改革などの計画支援も行い、自動化設備の導入を促進します。施設管理を効率化することで、オペレーションの自動化を推進し、物流センター全体のパフォーマンスを向上させることを目指します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- COVID-19の産業エコシステムへの影響

- 市場促進要因

- 市場成長を後押しする技術進歩の増加

- インダストリー4.0投資が自動化とマテリアルハンドリングの需要を牽引

- eコマースの急成長

- 市場抑制要因

- 初期コストの高さ

- 熟練労働者の不足

第5章 市場セグメンテーション

- 製品タイプ

- ハードウェア

- ソフトウェア

- サービス

- 機器タイプ

- 移動ロボット

- 無人搬送車(AGV)

- 自動フォークリフト

- 自動牽引/トラクター/タグ

- ユニットロード

- 組立ライン

- 特殊用途

- 自律移動ロボット(AMR)

- 自動保管・検索システム(ASRS)

- 固定通路

- カルーセル

- 垂直リフトモジュール

- 自動コンベア

- ベルト

- ローラー

- パレット

- オーバーヘッド

- パレタイザー

- 従来型

- ロボット

- 仕分けシステム

- 移動ロボット

- エンドユーザー産業

- 空港

- 自動車

- 飲食品

- 小売/倉庫/配送センター/物流センター

- 一般製造業

- 医薬品

- 郵便・小包

- 電子・半導体製造

- その他

- 国名

- 中国

- 日本

- インドネシア

- インド

- オーストラリア

- タイ

- 韓国

- シンガポール

- マレーシア

- 台湾

- その他のアジア太平洋

第6章 競合情勢

- 企業プロファイル

- Daifuku Co. Ltd

- Kardex Group

- KION Group

- JBT Corporation

- Jungheinrich AG

- SSI Schaefer AG

- VisionNav Robotics

- System Logistics

- BEUMER Group GmbH & Co. KG

- Interroll Group

- Witron Logistik

- Kuka AG

- Honeywell Intelligrated Inc.

- Murata Machinery Ltd

- Toyota Industries Corporation

第7章 投資分析

第8章 市場機会と今後の動向

The Asia Pacific Automated Material Handling And Storage Systems Market size is estimated at USD 29.66 billion in 2025, and is expected to reach USD 56.11 billion by 2030, at a CAGR of 13.6% during the forecast period (2025-2030).

With the rapid growth in stock-keeping units (SKUs), wholesalers and distributors are finding it difficult to make informed decisions about operations. This dilemma underscores the pressing need for more efficient labor, equipment, and technology utilization. Key factors driving the need for automated material-handling systems include cost savings, enhanced labor efficiency, and space optimization.

The market landscape is witnessing a surge in product variety and a demand for more frequent, smaller deliveries. Automated distribution operations can significantly boost an organization's order accuracy, often by several percentage points. The Asia-Pacific market's growth is propelled by urbanization, surging e-commerce sales, and a robust technology provider presence. These providers are intensifying their R&D efforts to offer cutting-edge solutions and maintain a competitive edge.

Asia-Pacific has cemented its position as a global e-commerce powerhouse. This status has been bolstered by the region's expanding retail e-commerce, driven by a burgeoning middle-income group in countries like China, India, and Indonesia, coupled with a fondness for mobile devices. Notably, China commands a staggering 40% share of global retail e-commerce sales. In several Asia-Pacific nations, the availability of warehouse land is dwindling, prompting a shift toward multi-story facilities and taller, narrower aisles. These adaptations are poised to fuel the demand for advanced material handling systems.

Material handling has witnessed a profound evolution over the past seven decades, with machines and robots increasingly replacing individual workers. This transformation has not only reshaped the industry but also fueled the growth of enterprises, notably in the automotive industry, which has seen a tenfold expansion. Countries like India are significantly investing in material handling equipment, with the MHE market, as per the Wisconsin Economic Development Corporation, capturing around 13% of the country's construction equipment industry. Southeast Asian nations, including Thailand, the Philippines, and Vietnam, are witnessing a surge in manufacturing establishments, bolstering employment and, subsequently, disposable incomes. This rise in income, coupled with a growing awareness of international brands, is spurring demand for local warehouses.

Indonesia stands out as a nation swiftly embracing automation, with a notable uptick in robotic usage for industrial applications. Given Japan's dual role as both a supplier and a consumer, Indonesia stands to benefit from heightened trade activities, further propelling the region's automation demand.

The global industrial landscape faced significant disruptions due to the COVID-19 pandemic and ensuing lockdowns. These disruptions spanned supply chain challenges, raw material shortages, labor scarcities, fluctuating prices, and shipping bottlenecks, all of which threatened to inflate production costs and exceed budgets.

APAC Automated Material Handling & Storage Systems Market Trends

Assembly Line Segment to Witness Significant Growth in the Market

- Assembly-line AGVs find their primary application in industries like automobile manufacturing, coach-building, aerospace, and railways. The rising production of electric and hybrid vehicles is set to drive the demand for these AGVs in the coming years. This shift not only enhances manufacturers' flexibility but also enables them to swiftly adapt to market changes, all while ensuring safe and cost-effective operations.

- The automotive industry witnessed a revolution in the past decade with the introduction of electric and hybrid vehicles. This transformation has significantly increased the complexity of automobile production. Coupled with evolving safety regulations and industry standards, there is a growing need for automation in the automotive industry. Key priorities include reducing product damage, often caused by human error during transit, improving the speed of chassis handling between workstations, and facilitating interaction with assembly-line workers. Assembly line AGVs, meeting these requirements effectively, have become the cornerstone of automation in the automotive industry.

- Furthermore, in the automotive industry, automated assembly lines are utilized to craft various parts, ranging from engines and gearboxes to fuel systems and pumps. Leveraging robotics and vision technology, manufacturers can create ergonomic and efficient product lines, safeguarding their workforce from hazardous conditions while ensuring swift assembly. Consequently, safety concerns are propelling automation across the automotive landscape.

- According to a report by the Automotive Skill Development Council (ASDC), titled 'Human Resource and Skills Requirements in the Automotive Sector (2026),' India is projected to employ 45.08 million individuals in the automobile industry by 2026. This surge in the workforce demands a reevaluation of the current skill set, emphasizing the need for upskilling in areas like automotive design, robotics, IoT, and AI. As traditional roles evolve, the industry is witnessing a heightened push toward automation.

- To cater to this escalating demand, numerous market players are not only expanding their manufacturing capacities but also introducing new product lines. For instance, in March 2024, Applied Manufacturing Technologies (AMT), a prominent name in North America's automation engineering, unveiled its latest innovation, ROBiN. Termed the Robotic Induction System, ROBiN aims to revolutionize material handling in warehousing, promising heightened efficiency and throughput. With a strong reputation in advanced material handling and cutting-edge autonomous mobile robots (AMRs), AMT's ROBiN is poised to make a significant impact in the industry.

Industry 4.0 Investments Driving Demand for Automation and Material Handling

- Airport investments are gaining global recognition as nations understand the value of creating welcoming environments that encourage travelers to spend both time and money. From check-in to boarding, conveyors and sortation systems, prevalent in airports of all sizes, effectively streamline the process, enhancing the overall customer experience. Many airports are now collaborating with vendors to introduce autonomous robots, a move that not only boosts luggage transfer efficiency but also trims operational costs. For example, Vanderlande Dutch, a logistics automation specialist, recently partnered with Hong Kong Airport to trial autonomous baggage handling vehicles.

- India and China, driven by increasing domestic air connectivity and rising per capita GDP, stand out as pivotal players in the regional aviation landscape. Highlighting this, the ICAO notes that the Asia-Pacific region alone accounted for 70% of domestic air travel.

- Projections indicate a robust growth trajectory for the Chinese aviation market in the coming years. Notably, China's top three airlines-Air China, China Southern, and China Eastern-have set ambitious fleet expansion goals, aiming to elevate their global rankings. Furthermore, major airports in Shanghai and Beijing are actively pursuing extensive expansion initiatives.

- According to the Chinese Tourism Outbound Research Institute, Chinese outbound visits are set to reach around 400 million by 2030, potentially constituting a quarter of all global outbound travelers. To accommodate this surge, airports must deploy advanced systems, a move that is expected to drive market growth positively throughout the forecast period.

- Conversely, the pandemic prompted many airports to deploy robots for passenger screening and virus containment. For instance, South Korea's Incheon Airport's Smart Airport team has been leveraging robotics and automated vehicles to enhance the experience for passengers with reduced mobility (PRMs).

APAC Automated Material Handling & Storage Systems Industry Overview

The Asia-Pacific market for automated material handling and storage systems is fiercely competitive, primarily due to the significant number of players in the arena. Key factors shaping this competition include high exit barriers, increasing firm concentration, and rising market penetration rates. Some of the key players operating in the market are Kardex Group, KION Group, JBT Corporation, Jungheinrich AG, Daifuku Co. Ltd, and BEUMER Group GmbH & Co. KG.

- In February 2024, Skechers USA, a prominent global footwear and apparel brand, partnered with Hai Robotics, a top player in automated storage and retrieval systems (ASRS), to inaugurate its latest distribution hub in Minato City, Tokyo, Japan. By leveraging Hai's cutting-edge automated goods-to-person technology, Skechers is enhancing its warehouse operations, accelerating fulfillment, and ensuring precise order processing.

- In January 2024, Fujitsu Limited and YE DIGITAL CORPORATION announced a collaboration aimed at tackling labor shortages and bolstering sustainable supply chains in Japan's logistics industry. The partnership focuses on leveraging Fujitsu's WMS services, known for enhancing distribution center efficiency, alongside YE DIGITAL's WES MMLogiStation, which is designed to automate warehouse operations. Fujitsu will not only provide its WMS services but also offer planning support for constructing new distribution centers and transforming operations at existing ones, aiming to ease the adoption of automated facilities. By streamlining facility management, the companies aim to drive operational automation and enhance overall distribution center performance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Impact of COVID-19 on the Industry Ecosystem

- 4.5 Market Drivers

- 4.5.1 Increasing Technological Advancements Aiding Market Growth

- 4.5.2 Industry 4.0 Investments Driving Demand for Automation and Material Handling

- 4.5.3 Rapid Growth of E-commerce

- 4.6 Market Restraints

- 4.6.1 High Initial Costs

- 4.6.2 Unavailability of Skilled Workforce

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 Equipment Type

- 5.2.1 Mobile Robots

- 5.2.1.1 Automated Guided Vehicle (AGV)

- 5.2.1.1.1 Automated Forklift

- 5.2.1.1.2 Automated Tow/Tractor/Tug

- 5.2.1.1.3 Unit Load

- 5.2.1.1.4 Assembly Line

- 5.2.1.1.5 Special Purpose

- 5.2.1.2 Autonomous Mobile Robots (AMR)

- 5.2.2 Automated Storage and Retrieval System (ASRS)

- 5.2.2.1 Fixed Aisle

- 5.2.2.2 Carousel

- 5.2.2.3 Vertical Lift Module

- 5.2.3 Automated Conveyor

- 5.2.3.1 Belt

- 5.2.3.2 Roller

- 5.2.3.3 Pallet

- 5.2.3.4 Overhead

- 5.2.4 Palletizer

- 5.2.4.1 Conventional

- 5.2.4.2 Robotic

- 5.2.5 Sortation System

- 5.2.1 Mobile Robots

- 5.3 End-user Industry

- 5.3.1 Airport

- 5.3.2 Automotive

- 5.3.3 Food and Beverage

- 5.3.4 Retail/Warehousing/Distribution Centers/Logistic Centers

- 5.3.5 General Manufacturing

- 5.3.6 Pharmaceuticals

- 5.3.7 Post and Parcel

- 5.3.8 Electronics and Semiconductor Manufacturing

- 5.3.9 Other End-user Industries

- 5.4 Country

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 Indonesia

- 5.4.4 India

- 5.4.5 Australia

- 5.4.6 Thailand

- 5.4.7 South Korea

- 5.4.8 Singapore

- 5.4.9 Malaysia

- 5.4.10 Taiwan

- 5.4.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Daifuku Co. Ltd

- 6.1.2 Kardex Group

- 6.1.3 KION Group

- 6.1.4 JBT Corporation

- 6.1.5 Jungheinrich AG

- 6.1.6 SSI Schaefer AG

- 6.1.7 VisionNav Robotics

- 6.1.8 System Logistics

- 6.1.9 BEUMER Group GmbH & Co. KG

- 6.1.10 Interroll Group

- 6.1.11 Witron Logistik

- 6.1.12 Kuka AG

- 6.1.13 Honeywell Intelligrated Inc.

- 6.1.14 Murata Machinery Ltd

- 6.1.15 Toyota Industries Corporation