|

市場調査レポート

商品コード

1550300

中国のHVAC:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)China HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のHVAC:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

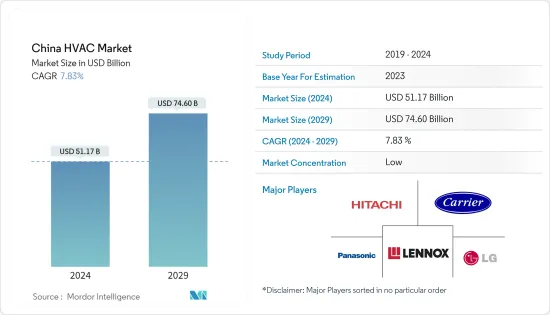

中国のHVAC市場規模は2024年に511億7,000万米ドルと推定され、2029年には746億米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは7.83%で成長する見込みです。

主なハイライト

- HVACシステムは、産業、住宅、商業施設における快適な環境づくりに不可欠な役割を果たしています。オフィス環境では、温度を調整し、適切な換気を確保することで、従業員の生産性と福利厚生を高めると同時に、不十分な湿度管理に関連する健康リスクを軽減します。

- 中国では、膨大な数の人々が農村部から都市部に移住しており、住宅、商業建設、インフラに対する政府および民間の支出が増加しています。新しいビルの建設は、暖房、換気、空調システムの新しい設備設置に対する大きな需要を生み出しています。

- 同国政府は、建物のエネルギー効率を高めるため、住宅部門の拡大と工業用・商業用建物の改修に力を入れており、HVACの需要をさらに促進しています。例えば、2024年4月、中国工業情報化部(MIIT)は他の6つの部門と共同で、「産業部門における設備更新促進のための実施計画」を最近発表しました。

- この戦略計画は、技術進歩と経済成長の重要な側面に焦点を当て、製造業の競争力と持続可能性の向上に対する中国のコミットメントを示すものです。産業設備の近代化に重点が置かれていることは、主要な政策目標としての意義を強調しています。

- さらに、工業用ボイラーの大幅な需要急増により、国内のHVAC需要は増加しています。中国は世界の製造拠点として急速に台頭しており、その人口の多さは、飲食品、消費財、繊維などの産業に有利な成長見通しをもたらしています。この重要な要因が、近い将来、中国の産業用ボイラー市場の成長を促進すると予想されます。

- HVACシステムは、住宅の大きさ、HVACの種類、ブランド、人件費、気候、ダクトの大きさ、エネルギー効率など、さまざまな要素で構成されています。これらの構成要素により、全体的なコストが大きくなり、市場成長の妨げとなっています。

- 中国のHVAC市場は断片化されており、多数のプレーヤーが小さな市場シェアを占めています。中国のHVAC市場で事業を展開するベンダーは、主に新製品開発、戦略的提携、買収、拡大する顧客需要に対応するための事業展開に注力しており、市場の成長をさらに後押ししています。

- 例えば、ダイキンは2024年1月、環境適応性や省エネ性、基本性能の向上に優れた低GWP(地球温暖化係数)冷媒R32の採用など、空調機器に求められる7つの機能を強化することで、業界トップレベルの省エネ性能を実現し、環境負荷や作業負荷の低減にも貢献する可変冷媒フロー(VRF)システム「VRV」7シリーズの発売を発表しました。

- さらに、中国のHVAC市場は、政府の規制やエネルギー効率の高い機器の導入を後押しする新たな取り組みなど、マクロ経済要因の影響を強く受けています。住宅コストの上昇に伴い、中国全土の地方当局は土地の賃貸から多額の税外収入を得、その後その資金をインフラ構想に振り向けた。その結果、中国の建設部門は継続的な成長を遂げ、市場の成長を後押ししました。

中国のHVAC市場の動向

HVAC機器セグメントが大きな市場シェアを占める

- 中国の産業部門が急速に成長していることが、最も大きなシェアを占めている主な要因の一つです。また、同国では都市化と商業化が進んでおり、HVAC機器の需要が高まると予想されています。さらに、可処分所得の上昇と生活水準の向上が快適な居住空間への需要を促進し、これが市場成長の原動力となります。

- 中国におけるエアコンの需要は、さまざまな製品オプションの利用可能性、継続的な技術の進歩、メディア・グループのような重要なプレイヤーの存在など、いくつかの要因によって増加しています。

- AHUの需要も、可燃性ガスを扱う工場やその他の作業環境で利用されることで増加しています。可燃性ガスを扱う場所では、電気機器から発生する火花が爆発につながる可能性があります。そのため、防爆装置やエアハンドリングユニットが導入されています。

- さらに、建設産業は中国経済の主要部門となっており、住宅開発やインフラ・プロジェクトによる後押しを主因として、中国GDPの約7%に貢献しています。

- そのため、工業、商業、住宅スペースの建設が増加し、HVAC機器とサービスの需要が高まると思われます。中国国家統計局によると、2023年の中国の建設産業の生産高は31兆人民元(4兆3,500億米ドル)を超え、10年前と比べてほぼ100%増加しました。

住宅セグメントが大きな市場シェアを占める

- 中国のHVAC市場は、住宅部門における空調機器需要の高まりによって成長しています。消費者の利便性と快適性への欲求の高まりとともに、地域の気温と湿度レベルの上昇により需要が拡大しています。

- さらに、政府は率先して国内の建物改修プロジェクトに投資しており、同国のHVACサービス・機器市場の需要をさらに押し上げています。例えば、中国政府は2023年11月、都市村の改修と手頃な価格の住宅プログラムに1,370億米ドルの資金を割り当てると発表し、弱体化する不動産市場を安定させるための最新の動きを示しました。

- さらに、エネルギー効率の改善を目的とした政府主導の建物改修プロジェクトが大幅に増加しており、中国のHVAC市場で牽引力を増しています。エネルギー効率の高い建物は、温室効果ガスの排出を削減し、住宅所有者のエネルギーコストを削減し、室内の空気の質を向上させ、それによって公衆衛生を促進することができます。

- 2023年、中国国家統計局の報告によると、中国のエアコン生産台数は2億3,300万台に達し、前年を約2,200万台上回った。中国は世界有数の家電生産国としての地位を維持し、市場の成長を支えました。

- さらに、中国南部の都市部では過去10年間に住宅暖房が大幅に増加し、持続可能性に関わる顕著な問題を引き起こしています。その結果、ヒートポンプはこの地域でますます普及し、中国全土で広く利用されるようになった。

- 空気熱源ヒートポンプと地上熱源ヒートポンプは市場でかなりのシェアを獲得しており、普及率も上昇しています。中国政府は、石炭から電気を作るプロジェクトなどの取り組みを通じて、この動向を後押ししてきました。中国におけるヒートポンプの人気の高まりは、市場の拡大を後押しすると予想されます。

- さらに、いくつかの地域プレーヤーが中国のHVAC市場でプレゼンスを拡大しており、市場の成長を支えています。例えば、2023年6月、パナソニックとシャオミは中国市場向けエアコンの製造に関する提携を発表しました。パナソニックは、その製造と品質管理の知識を活用して、シャオミのエアコン事業の成長をサポートする計画です。

中国のHVAC産業の概要

中国のHVAC市場は断片化されており、複数のプレーヤーで構成されています。各社は新製品の投入、事業の拡大、戦略的パートナーシップ、提携、合併、買収を行うことで、市場での存在感を高めようと絶えず努力しています。著名なプレーヤーには、日立製作所、Lennox International Inc.、パナソニック株式会社、LG Electronics Inc.、Carrier Corporationなどがあります。

- 2024年6月Carrier Corporationは、快適性とエネルギーソリューションのための新しいサービスベースのモデルの立ち上げを発表しました。キャリアが提供する「Cooling-as-a-Service」により、顧客はシステムや機器を購入する際に初期投資費用を負担する代わりに、性能の向上と継続的な支払いを確保することができます。この革新的な財務アプローチにより、顧客は本来の業務に専念することができ、キャリアの包括的な専門知識を活用して快適性と業務効率を確保することができます。

- 2024年5月ミディアはEVOX G3ヒートポンプシステムを発表。このEVOXシリーズの新型は、EVOX G3ヒートポンプとEVOX G3エアハンドリングユニット(AHU)で構成されます。1.5トンから5トンまでのサイズを取り揃えたMidea EVOX G3ヒートポンプには、Enhanced Vapor Injection(EVI)技術と多層熱交換器が搭載されており、過酷な気象条件下でも補助熱を必要とせず、信頼性の高い暖かさを保証します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 税額控除プログラムによる省エネ奨励を含む政府の支援規制

- エネルギー効率の高い機器に対する需要の増加

- 需要を支える建設・改修活動の増加

- 市場の課題

- エネルギー効率の高いシステムの初期コストの高さ

第6章 市場セグメンテーション

- コンポーネントタイプ別

- HVAC機器

- 暖房機器

- 空調・換気機器

- HVACサービス

- HVAC機器

- エンドユーザー産業別

- 住宅

- 商業

- 産業

第7章 競合情勢

- 企業プロファイル

- Johnson Controls International PLC

- Carrier Corporation

- Robert Bosch GmbH

- Daikin Industries Ltd

- Midea Group Co. Ltd

- System Air AB

- LG Electronics Inc.

- Mitsubishi Electric Corporation

- Danfoss A/S

- Lennox International Inc.

- Hitachi Ltd

- Panasonic Corporation

第8章 投資分析

第9章 市場の将来

The China HVAC Market size is estimated at USD 51.17 billion in 2024, and is expected to reach USD 74.60 billion by 2029, growing at a CAGR of 7.83% during the forecast period (2024-2029).

Key Highlights

- HVAC systems play an essential role in creating comfortable environments in industrial, residential, and commercial structures. In office settings, they regulate temperatures, ensure adequate ventilation, and, in turn, boost employee productivity and well-being while mitigating health risks linked to inadequate humidity control.

- In China, a huge number of people have been migrating from rural areas to cities, which is raising government and private spending on housing, commercial construction, and infrastructure. New building constructions are creating significant demand for new equipment installations of heating, ventilation, and air-conditioning systems.

- The government in the country is focusing on expanding the residential sector and renovating industrial and commercial buildings to increase the energy efficiency of the buildings, further propelling the demand for HVAC. For instance, in April 2024, the Implementation Plan for Promoting Equipment Renewal in the Industrial Sector was recently introduced by China's Ministry of Industry and Information Technology (MIIT) in collaboration with six other departments.

- This strategic plan focuses on key aspects of technological advancement and economic growth, showcasing China's commitment to improving competitiveness and sustainability in the manufacturing industry. The emphasis on industrial equipment modernization highlights its significance as a primary policy objective.

- Moreover, the demand for HVAC in the country is increasing due to a significant surge in demand for industrial boilers. China is rapidly emerging as a global manufacturing hub, and its large populations offer lucrative growth prospects for industries such as food & beverages, consumer goods, textiles, and more. This crucial factor is expected to drive the growth of the industrial boilers market in China in the near future.

- An HVAC system comprises various components, including home size, HVAC type, brand, labor expenses, climate, ductwork size, and energy efficiency. These components result in a significant overall cost, which hampers market growth.

- The HVAC market in China is fragmented, with a large number of players occupying a small market share. Vendors operating in the China HVAC market mainly focus on new product development, strategic partnership, acquisition, and expansion to meet the growing customer demand, further supporting the market growth.

- For instance, in January 2024, Daikin announced the launch of variable refrigerant volume (VRV) 7 series variable refrigerant flow (VRF) systems that realize the industry's top-level energy-saving performance by strengthening seven features required by air conditioning equipment, for example, adopting low-global warming potential (GWP) refrigerant R32 that is excellent in environmental adaptability and energy savings and in improving basic performance, and also contributes to reducing the environmental burden and the workload.

- Furthermore, the HVAC market in China is highly affected by macroeconomic factors such as government regulations and new initiatives to boost the adoption of energy-efficient equipment. With the rise in housing costs, local authorities throughout China obtained significant non-tax income from land leases and subsequently allocated the funds toward infrastructure initiatives. As a result, the construction sector in the nation experienced ongoing growth, thus fuelling the market growth.

China HVAC Market Trends

HVAC Equipment Segment Holds Significant Market Share

- The fast-increasing industrial sector in China is one of the primary causes responsible for the most significant share. It is also anticipated that growing urbanization and commercialization in the country will raise demand for HVAC equipment. Additionally, rising disposable income and a higher standard of life drive demand for pleasant living spaces, which will drive market growth.

- The demand for air conditioners in China is increasing due to several factors, such as the availability of various product options, continuous technological advancements, and the presence of significant players like Media Group.

- The demand for AHUs is also increasing as they are utilized in factories and other work environments that deal with flammable gases. In areas with flammable gases, sparks produced by an electrical apparatus could lead to an explosion. Hence, explosion-resistant devices or air-handling units are implemented in these settings.

- Furthermore, the construction industry has become a key sector of China's economy, contributing to approximately 7 % of the country's GDP, largely due to the boost from housing developments and infrastructure projects.

- Thus, the growing construction of industrial, commercial, and residential spaces in the country will increase the demand for HVAC equipment and services. According to the National Bureau of Statistics of China, in 2023, the construction industry in China generated an output of over CNY 31 trillion (USD 4.35 trillion), representing an increase of almost 100 % from a decade ago.

Residential Segment Holds Significant Market Share

- The HVAC market in China is growing owing to the rising demand for air conditioning equipment in the residential sector. The demand is growing due to rising temperatures and humidity levels in the area, along with consumers' increasing desire for convenience and comfort.

- Moreover, the government is taking the initiative and investing in building renovation projects in the country, further driving the demand for the country's HVAC services and equipment market. For instance, in November 2023, the government of China announced allocating USD 137 billion in affordable financing for urban village renovation and affordable housing programs, marking its latest move to stabilize the weakening property market.

- Additionally, there has been a significant increase in government-led building renovation projects aimed at improving energy efficiency, which is gaining traction in the China HVAC market. Energy-efficient buildings can reduce greenhouse gas emissions, decrease homeowners' energy costs, and enhance indoor air quality, thereby promoting public health.

- In 2023, China's National Bureau of Statistics reported that the country's production volume of air conditioners reached 233 million units, approximately 22 million units higher than the previous year. China maintained its position as one of the leading global producers of consumer electronics, thus supporting the market's growth.

- Moreover, there has been a substantial rise in residential space heating in urban Southern China over the past ten years, bringing about notable sustainability issues. Consequently, heat pumps have become increasingly popular in the area and are extensively utilized throughout China.

- Air-source and ground-source heat pumps have gained a considerable share of the market and are experiencing an increasing acceptance rate. The Chinese government has been instrumental in driving this trend forward through initiatives such as the coal-to-electricity project. The growing popularity of heat pumps in China is expected to bolster the market's expansion.

- Furthermore, several regional players are expanding their presence in the country's HVAC market, thus supporting the market growth. For instance, in June 2023, Panasonic and Xiaomi announced a partnership to manufacture air conditioners for the Chinese Market. Panasonic plans to leverage its manufacturing and quality control knowledge to support Xiaomi's growing air conditioning operations.

China HVAC Industry Overview

The China HVAC market is fragmented and consists of several players. Companies continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic partnerships, collaborations, mergers, and acquisitions. Some of the prominent players include Hitachi Ltd, Lennox International Inc., Panasonic Corporation, LG Electronics Inc., Carrier Corporation, and many more.

- June 2024: Carrier Corporation announced the launch of a new service-based model for comfort and energy solutions. Carrier's Cooling-as-a-Service offering enables customers to secure extended performance and consistent payments instead of facing an initial capital expense for system or equipment acquisitions. This innovative financial approach empowers customers to concentrate on their primary operations, leveraging Carrier's comprehensive expertise to ensure comfort and operational effectiveness.

- May 2024: Midea introduced the EVOX G3 heat pump system. This new iteration of the EVOX series consists of the EVOX G3 Heat Pump and EVOX G3 Air Handling Unit (AHU). Available in sizes ranging from 1.5-ton to 5-ton units, the Midea EVOX G3 heat pumps are equipped with Enhanced Vapor Injection (EVI) technology and a multi-layer heat exchanger, guaranteeing reliable warmth without the need for auxiliary heat, even in extreme weather conditions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Supportive Government Regulations Including Incentives for Saving Energy through Tax Credit Programs

- 5.1.2 Increasing Demand for Energy Efficient Devices

- 5.1.3 Increased Construction and Retrofit Activity to Aid Demand

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Energy Efficient Systems

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning /Ventilation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End-user Industry

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Johnson Controls International PLC

- 7.1.2 Carrier Corporation

- 7.1.3 Robert Bosch GmbH

- 7.1.4 Daikin Industries Ltd

- 7.1.5 Midea Group Co. Ltd

- 7.1.6 System Air AB

- 7.1.7 LG Electronics Inc.

- 7.1.8 Mitsubishi Electric Corporation

- 7.1.9 Danfoss A/S

- 7.1.10 Lennox International Inc.

- 7.1.11 Hitachi Ltd

- 7.1.12 Panasonic Corporation