|

市場調査レポート

商品コード

1550234

ドイツのHVAC:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Germany HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツのHVAC:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

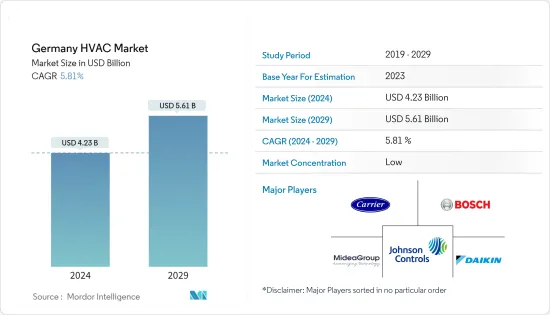

ドイツのHVAC市場規模は2024年に42億3,000万米ドルと推定・予測され、2029年には56億1,000万米ドルに達し、予測期間(2024-2029年)のCAGRは5.81%で成長すると予測されます。

主なハイライト

- ドイツの市場拡大要因として、高度な監視システム、スマート技術、ビルオートメーションシステムの採用、コスト削減とメンテナンスの重視、HVACシステムのメンテナンスと個別サービスの向上などが分析されています。

- エネルギー効率とグリーン経済の成熟市場としてすでに認知されているドイツは、エネルギーの多様化への取り組みを倍増させ、HVACやその他の分野で気候変動課題に取り組むための規制や技術を導入しています。例えば、政府は2024年以降、新しい持続可能な暖房システムの費用の最大70%を負担すると発表しており、これによって人々は申請を待つことができるようになるかもしれないです。このように、エネルギー効率の高いHVACソリューションの導入に政府が力を入れるようになったことが、同国のHVAC市場の役割をさらに後押ししています。

- さらに、ドイツのBAFAが提供するヒートポンプへの補助金は、連邦経済・輸出管理局が管理しています。この補助金は、設置費用総額の最大50%をカバーするもので、一戸建て住宅には最大3,000ユーロ、集合住宅には最大6,000ユーロが支給されます。

- 新しいHVAC技術を既存の建物インフラに統合することは、複雑で費用がかかる可能性があります。特に古い建物では、アップグレードを妨げるような問題が存在する可能性があります。さらに、エネルギーコストの上昇は、エネルギー効率の高いシステムに対する需要を促進するもの、エネルギー価格の変動は不確実性を生み、投資決定に影響を与えることもあります。従来のエネルギー源への依存は、より持続可能なHVACソリューションへの移行を遅らせ、市場の成長を妨げる可能性があります。

- エネルギー効率の高いHVACシステムの採用を促進する政府の取り組みや補助金のようなマクロ経済要因は、重要な役割を果たしています。省エネ条例(EnEV)やグリーンビルディングへの奨励金といった政策は、最新のエネルギー効率の高いHVACシステムの需要を促進しています。さらに、古いシステムを新しく効率的なものに改修するための財政的インセンティブを提供するプログラムが、市場の成長を後押ししています。

ドイツのHVAC市場動向

住宅部門が大きな市場シェアを占める

- ドイツでは、エネルギー効率の高い冷暖房システムに対する需要の高まりから、住宅向けのHVACシステムが成長しています。エネルギーコストの上昇と、エネルギー効率の高い住宅のアップグレードに対する政府の優遇措置がこの成長を後押ししています。例えば、ドイツでは2023年9月に、効率基準が厳しくなくても新築住宅が税額控除の対象となった。この税額控除により、新築プロジェクトは投資費用の6%を初年度の税金から相殺できるようになった。対象期間は、2023年10月1日から2029年9月30日までに着工されるプロジェクトに及ぶ。

- ドイツは、ほぼゼロ・エネルギー・ビルの開発を奨励する規制を導入し、ヒートポンプのような効率的なエネルギー源を利用することでエネルギー効率を高めるよう住宅建設を後押ししています。ヒートポンプは、一戸建て住宅やテラスハウスで熱源として一般的に採用されており、集合住宅でも利用が拡大しています。

- ヒートポンプファンディングのようなHVAC機器に対する補助金に関するKfWの規制は、ドイツにおける再生可能ヒートポンプの設置を支援するためのものです。このプログラムでは、一戸建て住宅には最高5,000ユーロ、集合住宅には最高10,000ユーロの資金援助が提供されます。ドイツでは数多くのエネルギー会社がヒートポンプの使用を推奨しています。補助金は通常、設置費用全体の最大50%をカバーします。同市場における企業や政府によるこうした取り組みは、同国におけるHVACサービスの需要拡大を補完すると予想されます。

- 2023年には、ドイツの建設事情に大きな動向が現れました。新たに認可された建物の75%がヒートポンプを採用し始めたのです。認可された新築住宅のうち、76%がヒートポンプを主に使用することになります。さらに、2023年に竣工する約96,800棟の住宅のうち、65%近くがヒートポンプを主要な暖房ソリューションとして採用していることがデータから明らかになっています。

大きな市場シェアを占めるHVAC機器

- 地球温暖化の影響の増大が、HVAC機器の成長を促進しています。この動向は、気温の上昇によって空調設備が必要となるドイツのような国々で特に顕著です。

- ドイツでは、いくつかの古い建物が現代のエネルギー基準を満たすために改修を必要としており、HVACの改修とアップグレードの需要増につながっています。建物の改築や改修に対する政府の優遇措置が、この需要をさらに刺激しています。同国のインフラの老朽化により、交換や保守サービスが必要となり、継続的な需要を牽引しています。システムの効率と寿命を確保するための定期的なメンテナンス要件が、HVAC機器の需要に寄与しています。現在、ドイツの建物の約半数はガス暖房システムに依存しています。

- 例えば、2023年8月、建築エネルギー法(GEG)は、商業ビルおよび住宅における暖房のための再生可能エネルギー源の利用を段階的に促進することを目的としました。GEGの下では、すべての新しい暖房システムは、既存・新築を問わず、少なくとも65%のエネルギーを再生可能エネルギー源から得なければならないです。既存のシステムは稼動したままで、必要に応じて修理を受けることができます。特筆すべきは、2024年以降、同法は、水素互換性があればガスヒーターの設置を認め、将来的な転換を可能にすることです。

- ドイツはヒートポンプのような空調設備に多額の補助金を提供しています。EHPAによると、土地所有者は地上熱源ヒートポンプに最大18,000ユーロ、空気熱源ヒートポンプに最大15,000ユーロを受け取ることができます。2024年1月1日、ドイツ政府はBWPと共同で、より充実した資金調達オプションを導入しました。この新しい規定により、不動産所有者はヒートポンプを設置する際、最大21,000ユーロの補助金を利用できるようになった。特筆すべきは、これらの補助金はすべての人に門戸が開かれている一方で、低所得世帯にとっては特に有利であるということです。

ドイツHVAC産業の概要

ドイツのHVAC市場は断片化されており、Carrier Corporation、Robert Bosch GmbH、Midea Group、Johnson Controls International PLC、Daikin Industries Ltd.などの大手企業が存在します。同市場のプレーヤーは、パートナーシップ、合併、技術革新、投資、買収などの戦略を採用し、製品ラインナップを強化し、持続可能な競争優位性を獲得しています。

- 2024年1月ドイツのシュトゥットガルト近郊のゲルリンゲンに本社を置くアプレオナは、著名な換気・空調会社であるエアフォーオールの買収を完了しました。エアフォーオールはクリーンルームと研究所に特化し、主に自動車とヘルスケア分野のクライアントに対応しています。この戦略的買収により、アプレオナのテクニカル・システム・ポートフォリオが強化され、有利なドイツ南西部での足跡が大幅に強化されました。

- 2023年10月Vargas Investment Groupは、ヒートポンプを月額制で提供する消費者直販企業Airaを立ち上げました。9月にドイツでデビューし、ベルリンにトレーニングアカデミーを開設。Garant Warmesysteme社を買収したことで、Airaはその事業範囲をベルリン・ブランデンブルクからドイツのザクセンとバイエルンまで拡大しました。Airaの野心的な目標は、今後10年以内に欧州の500万世帯にヒートポンプを設置することであり、ドイツでは100万世帯の設置に重点を置いています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 需要を支える建設・改修活動の増加

- 補助金、税額控除プログラムによる省エネ奨励金など、政府による支援規制

- 市場の課題

- エネルギー効率の高いシステムの初期コストの高さ

- 熟練労働者の不足

第6章 市場セグメンテーション

- 部品タイプ別

- HVAC機器

- 暖房機器

- 空調・換気機器

- HVACサービス

- HVAC機器

- エンドユーザー産業別

- 住宅

- 商業

- 産業

第7章 競合情勢

- 企業プロファイル

- Carrier Corporation

- Robert Bosch GmbH

- Midea Group Co. Ltd

- Johnson Controls International PLC

- Daikin Industries Ltd

- System Air AB

- LG Electronics Inc.

- Mitsubishi Electric Hydronics & IT Cooling Systems SpA

- Flaktgroup Inc.

- Danfoss Inc.

第8章 投資分析

第9章 市場の将来

The Germany HVAC Market size is estimated at USD 4.23 billion in 2024, and is expected to reach USD 5.61 billion by 2029, growing at a CAGR of 5.81% during the forecast period (2024-2029).

Key Highlights

- The factors contributing to the expansion of the market in Germany being analyzed include the adoption of advanced monitoring systems, smart technologies, and building automation systems, a greater emphasis on cost savings and maintenance, and improved maintenance and personalized services for HVAC systems.

- Already acknowledged as a mature market for energy efficiency and a green economy, Germany is doubling its efforts in energy diversification and introducing regulations and technologies to tackle climate challenges in HVAC and other sectors. For instance, the government has announced that it would cover up to 70% of the costs of new and sustainable heating systems from 2024, which may let people wait with the applications. Thus, increasing government focus on installing energy-efficient HVAC solutions further drives the role of the HVAC market in the country.

- In addition, the subsidy for heat pumps provided by BAFA in Germany is administered by the Federal Office for Economic Affairs and Export Control. It covers up to 50% of the total installation cost, with a maximum of EUR 3,000 for single-family residences and EUR 6,000 for multi-family homes.

- Integrating new HVAC technologies with existing building infrastructure can be complex and expensive. Issues may exist, especially in older buildings, which can deter upgrades. In addition, although rising energy costs drive demand for energy-efficient systems, fluctuating energy prices can also create uncertainty, impacting investment decisions. Dependence on traditional energy sources can slow the transition to more sustainable HVAC solutions, thus hindering the market's growth.

- Macroeconomic factors like government initiatives and subsidies promoting the adoption of energy-efficient HVAC systems play a significant role. Policies like the energy saving ordinance (EnEV) and incentives for green buildings drive the demand for modern, energy-efficient HVAC systems. In addition, programs offering financial incentives for retrofitting old systems with new, efficient ones boost market growth.

Germany HVAC Market Trends

Residential Sector to Hold Significant Market Share

- The country's HVAC systems in residential settings have been growing due to increased demand for energy-efficient heating and cooling systems. Rising energy costs and government incentives for energy-efficient home upgrades drive this growth. For instance, in September 2023, in Germany, newly constructed homes qualified for tax credits, even without stricter efficiency standards. These credits allowed new building projects to offset 6% of the investment costs against taxes in the initial year. The eligibility window spans projects commencing construction between October 1, 2023, and September 30, 2029.

- Germany has introduced regulations to encourage the development of nearly zero-energy buildings, thereby pushing residential structures to enhance energy efficiency by utilizing efficient energy sources like heat pumps. Heat pumps are commonly employed as heat sources in single-family homes and terraced houses, and their usage is also progressively expanding in apartment buildings.

- The KfW regulation for subsidies on HVAC equipment, such as heat pump funding, is designed to support the installation of renewable heat pumps in Germany. The program offers financial support of up to EUR 5,000 for single-family homes and up to EUR 10,000 for multi-family housing. Numerous energy companies in Germany are advocating for the use of heat pumps. The subsidies usually cover up to 50% of the entire installation expenses. Such initiatives by the companies and government in the market are expected to complement the demand growth for HVAC services in the country.

- In 2023, a significant trend emerged in Germany's construction landscape: 75% of newly approved buildings began featuring heat pumps. Out of the total new residential constructions approved, 76% were set to rely predominantly on heat pumps. Furthermore, data reveals that nearly 65% of the approximately 96,800 residential buildings completed in 2023 embraced heat pumps as the primary heating solution.

HVAC Equipment to Hold Significant Market Share

- The increasing effects of global warming are driving the growth of HVAC equipment. This trend is especially pronounced in countries such as Germany, where soaring temperatures require air conditioning.

- Several older buildings in Germany require renovation to meet modern energy standards, leading to increased demand for HVAC retrofitting and upgrades. Government incentives for building renovations and retrofits further stimulate this demand. The country's aging infrastructure necessitates replacement and maintenance services, driving ongoing demand. Regular maintenance requirements to ensure system efficiency and longevity contribute to the demand for HVAC equipment. Presently, approximately half of Germany's buildings rely on gas heating systems.

- For instance, in August 2023, the Building Energy Act (GEG) aimed to incrementally boost the utilization of renewable energy sources for heating in commercial and residential buildings. Under the GEG, all new heating systems must derive at least 65% of the energy from renewable sources, whether in existing or new constructions. Existing systems can remain operational and undergo repairs as needed. Notably, post-2024, the act will allow for the installation of gas heaters, provided they are hydrogen-compatible, allowing for potential conversion in the future.

- Germany offers substantial grants for HVAC equipment like heat pumps. According to EHPA, landowners can receive up to EUR 18,000 for ground-source heat pumps and up to EUR 15,000 for air-source heat pumps. On January 1, 2024, the German government, in collaboration with the BWP, introduced enhanced funding options. Under these new provisions, property owners can now access a maximum subsidy of EUR 21,000 when installing a heat pump. Notably, while these grants are open to all, they are especially advantageous for low-income families.

Germany HVAC Industry Overview

The German HVAC market is fragmented, with the presence of major players like Carrier Corporation, Robert Bosch GmbH, Midea Group Co. Ltd, Johnson Controls International PLC, and Daikin Industries Ltd. Players in the market are adopting strategies such as partnerships, mergers, innovations, investments, and acquisitions to enhance the product offerings and gain sustainable competitive advantage.

- January 2024: Apleona, headquartered in Gerlingen near Stuttgart, Germany, finalized its acquisition of Air for All, a prominent ventilation and air conditioning company. Air for All specializes in cleanrooms and laboratories and caters primarily to clients in the automotive and healthcare sectors. This strategic move bolsters Apleona's technical systems portfolio and significantly enhances its footprint in the lucrative southwest region of Germany.

- October 2023: Vargas Investment Group launched Aira, a direct-to-consumer company that provides heat pumps through a monthly subscription model. Aira debuted in Germany in September, inaugurating a training academy in Berlin. By acquiring Garant Warmesysteme, Aira extended its reach from Berlin-Brandenburg to Saxony and Bavaria in Germany. Aira's ambitious goal is to install heat pumps in 5 million European households within the next decade, with a significant focus on 1 million installations in Germany.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Construction and Retrofit Activity to Aid Demand

- 5.1.2 Supportive Government Regulations Including Subsidies, Incentives for Saving Energy through Tax Credit Programs

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Energy Efficient Systems

- 5.2.2 Shortage of Skilled Labour

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning /Ventilation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End-user Industry

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Carrier Corporation

- 7.1.2 Robert Bosch GmbH

- 7.1.3 Midea Group Co. Ltd

- 7.1.4 Johnson Controls International PLC

- 7.1.5 Daikin Industries Ltd

- 7.1.6 System Air AB

- 7.1.7 LG Electronics Inc.

- 7.1.8 Mitsubishi Electric Hydronics & IT Cooling Systems SpA

- 7.1.9 Flaktgroup Inc.

- 7.1.10 Danfoss Inc.