|

市場調査レポート

商品コード

1550313

フランスのHVAC:市場シェア分析、産業動向、成長予測(2024年~2029年)France HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フランスのHVAC:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

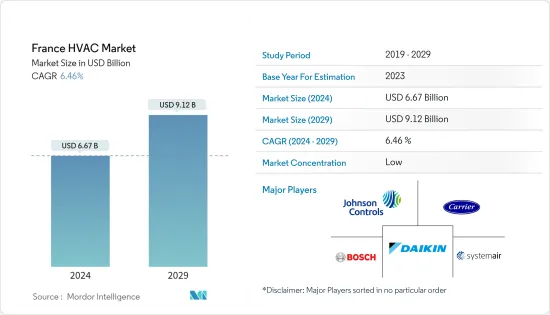

フランスのHVAC市場規模は2024年に66億7,000万米ドルと推定・予測され、2029年には91億2,000万米ドルに達し、予測期間(2024-2029年)のCAGRは6.46%で成長すると予測されます。

主なハイライト

- フランスは、建物のエネルギー性能に高い基準を設けるRTやREといった厳しいエネルギー効率規制を実施しています。これらの規制は、エネルギー消費量と二酸化炭素排出量を削減するため、エネルギー効率の高いHVACシステムの使用を促進しています。ユーロスタットによると、フランスの最終エネルギー需要は主に冷暖房(H&C)に起因しており、全体の45%を占めています。意外なことに、家庭が消費するエネルギーは全体の約30%で、産業部門を上回っています。エネルギー効率技術を改善するための政府の熱心な取り組みは、フランスのHVAC市場を前進させると思われます。

- フランスにおけるHVACシステムの需要は、気候変動、都市化、生活水準の向上を背景に、着実に増加しています。オフィスビルや小売スペースを含む商業部門も、HVACシステムの市場拡大に貢献しています。さらに、既存の建物の改築や改修の動向は、最新の省エネ技術に合わせたHVACのアップグレードの必要性を高めています。

- 同国は、主に都市人口の増加により、HVAC機器とサービスに対する大きな需要を生み出し、市場成長に大きく貢献しています。2023年、フランスの総人口は6,800万人を超えました。同年、フランスで最も人口が多かったのはイル・ド・フランス地方でした。INSEEによると、1,200万人以上のフランス国民がイル・ド・フランスに住んでいます。イル・ド・フランス地方に次いで、南部のオーヴェルニュ=ローヌ=アルプ地方とヌーヴェル・アキテーヌ地方が続いた。

- さらに、新しい産業施設、オフィスビル、集合住宅、データセンター、先端技術製造スペースの需要が急増しています。同国では複数の企業がオフィススペースを拡張しており、HVAC機器とサービスに対する高い需要がさらに生まれると思われます。

- インフレとサプライチェーンの混乱は原材料費を押し上げ、HVACシステムの製造コストに直接影響を与えます。特に、鉄鋼、銅、アルミニウムのような必須素材は大幅なコスト上昇を目の当たりにしており、HVACメーカーにさらなる負担を強いています。その結果、中小規模のHVAC企業は利幅の制限に直面し、利益に直接影響を与え、研究開発(R&D)への投資能力を妨げています。これがひいては市場の成長性を阻害しています。

- フランスのマクロ経済情勢に休息はありません。地政学的緊張が高まる中、高止まりするインフレと金利、そして迫り来る景気後退の懸念に直面しました。このような不確実性を背景に、消費者はさまざまなセクターで警戒感を強めています。市場の反発は予想されるもの、その時期と軌道はあいまいなままです。加えて、古いシステムを効率的な新しいものに改修するための経済的インセンティブを提供するプログラムが、市場の成長を後押ししています。

フランスのHVAC市場の動向

住宅部門が著しい成長を遂げる

- 同市場の成長は、ガスよりも電気暖房システムへの強い嗜好、ヒートポンプに移行した国内空調産業、1世帯あたり最大1万ユーロ(1万884.45米ドル)を支給するFranceRenovのような助成金制度を含む、ヒートポンプ設置を促進する政府イニシアチブの実施といった要因に起因します。新築住宅の新しいエネルギー効率基準も、フランスの成果に一役買っています。さらに、フランスにおける住宅建設の増加が市場を牽引すると予想されます。

- 例えば、フランスは2023年9月、従来の住宅用燃料・ガスヒーターからヒートポンプへの移行を率先して推進し、これらの機器の国内産業の確立を目指しました。このイニシアチブは、フランスの包括的な複数年環境戦略の極めて重要な部分を形成しています。同国は、最後の数基となった石炭火力発電所の閉鎖を検討し、火力エンジンから電気自動車へのシフトを積極的に提唱し、ヒートポンプを家庭の主要な暖房ソリューションとして推進しています。

- 二酸化炭素排出量を減らしたいという願望と環境問題に対する意識の高まりから、住宅所有者は環境に優しいHVACシステム、エネルギー効率が高く再生可能エネルギーに基づくHVACソリューション、例えばヒートポンプや太陽光発電システムなどに投資するようになり、これらは同国で普及しつつあります。Inseeによると、フランスでは2023年1~10月の間に、床面積ベースで非住宅よりも多くの住宅が建設されました。

- 同国の住宅用HVAC部門では、エネルギー効率の高い冷暖房システムに対する需要が一貫して増加しています。この成長は主に、エネルギーコストの上昇と、エネルギー効率の高い住宅への改築を奨励する政府のインセンティブによって推進されています。例えば、フランス政府は2024年4月、7万5,000戸の中級住宅を開発するための資金として約10億ユーロ(10億9,000万米ドル)を正式に割り当てた。このイニシアチブは、今後3年間で全国で50万戸の住宅増設が急務となっていることに対処するための、より広範な戦略の一環です。

HVAC機器が大きな市場シェアを占めると予想される

- フランスでは、建物のエネルギー効率規制や環境基準が厳しく、これがHVAC機器の需要を押し上げています。ビルの運営者や所有者は、エネルギー効率の高い冷暖房システム、換気ソリューション、空気品質管理技術を導入することで、これらの規制を遵守しなければならないです。規制要件を満たし、エネルギー性能目標を達成する必要性は、エネルギー効率のアップグレード、改修、適合評価に焦点を当てたHVAC機器に対する大きな需要を生み出しています。

- 例えば、フランスは2027年までに、国内で年間100万台のヒートポンプの新規生産を目標としています。需要を強化するため、政府はヒートポンプを屋根に設置するための規制や行政手続きの合理化を計画しており、官僚的なハードルを減らすという広範なアジェンダと一致しています。MaPrimeRenovや省エネ証明書のようなイニシアチブを継続することで、消費者のヒートポンプ購入を支援します。

- 2023年9月、フランス政府はヒートポンプへの補助金を増額する計画を発表しました。これは、ヒートポンプの購入にかかる純費用が、特に低所得者層にとって、ガス暖房機と同水準になるようにすることを意図したものです。さらに、政府は国内ヒートポンプ産業の強化に向けて積極的に取り組んでおり、年間100万台までの製造能力を目標に掲げています。

- 例えば、2023年初頭のデータに基づくEHPAの欧州における住宅用ヒートポンプの補助金報告書では、フランスでは不動産所有者が補助金を受ける資格があることが強調されています。既存物件に設置する場合、これらの補助金は、地上熱源ヒートポンプでは最高1万5,000ユーロ(16326.67米ドル)、空気熱源ヒートポンプでは最高9,000ユーロ(9,796米ドル)に達する可能性があります。多くのヒートポンプの生産は、複数の産業セグメントにまたがるHVAC機器の需要を刺激しています。

フランスのHVAC産業の概要

フレンチHVAC市場は断片化されており、Johnson Controls International PLC、Carrier Corporation、Robert Bosch GmbH、Daikin Industries Ltd、System Air ABといった大手企業が存在します。フランスのHVAC市場の有力企業は、製品提供を強化し、持続可能な競争優位性を獲得するために、提携、合併、技術革新、投資、買収などの戦略を採用しています。

- 2024年4月三菱電機は、フランスを拠点とする著名な空調グループであるAircaloを買収することで、欧州におけるHVACRのプレゼンスを強化する構えです。この戦略的な動きは三菱のポートフォリオを強化し、より広範なハイドロニックシステムへの対応を可能にします。これらのシステムは、温室効果ガスの排出削減に焦点を当てた、効率的で環境に優しい冷暖房ソリューションに対する市場の需要の高まりに対応するために設計されています。

- 2023年12月ソネパールは、空調および治療ソリューションを販売するフランスのHydeclim社を買収しました。この買収は、太陽光発電に特化したAlliantz社、(暖房・換気・空調)に特化したCD Sud社など、ソネパールが最近フランスで行った買収に続くものです。Hydeclim社を買収することで、ソネパールはHVAC分野での存在感を強め、特にフランス西部と北部に重点を置き、空調・暖房設備業者への提案の幅を広げています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 税額控除プログラムによる省エネ奨励を含む政府の支援規制

- スマートシステムや再生可能エネルギーの統合を含むHVAC技術の革新

- 需要を支える建設・改修活動の増加

- 市場の課題

- エネルギー効率の高い高度なHVACシステムの初期コストの高さ

- 熟練労働者の不足

第6章 市場セグメンテーション

- 部品タイプ別

- HVAC機器

- 暖房機器

- 空調/換気機器

- HVACサービス

- HVAC機器

- エンドユーザー産業別

- 住宅

- 商業

- 産業用

第7章 競合情勢

- 企業プロファイル

- Johnson Controls International PLC

- Carrier Corporation

- Robert Bosch GmbH

- Daikin Industries Ltd

- System Air AB

- Flaktgroup Inc.

- LG Electronics Inc.

- BDR Thermea Group

- Mitsubishi Electric Hydronics & IT Cooling Systems SpA

- Danfoss Inc.

第8章 投資分析

第9章 市場の将来

The France HVAC Market size is estimated at USD 6.67 billion in 2024, and is expected to reach USD 9.12 billion by 2029, growing at a CAGR of 6.46% during the forecast period (2024-2029).

Key Highlights

- France has implemented stringent energy efficiency regulations, such as RT and RE, which set high standards for the energy performance of buildings. These regulations promote using energy-efficient HVAC systems to reduce energy consumption and carbon emissions. According to Eurostat, France's final energy demand is attributed mainly to heating and cooling (H&C), accounting for 45% of the total. Surprisingly, households consume approximately 30% of the country's energy, surpassing the industrial sector. The government's dedicated efforts to improve energy efficiency techniques will drive the French HVAC market forward.

- The demand for HVAC systems in France is steadily increasing, driven by climate change, urbanization, and rising living standards. The commercial sector, including office buildings and retail spaces, is also contributing to the growing market for HVAC systems. Moreover, the trend toward renovating and retrofitting existing buildings amplifies the necessity for HVAC upgrades, aligning with modern energy-saving technologies.

- The country is contributing considerably to market growth, primarily due to the increase in urban population, which generates significant demand for HVAC equipment and services. In 2023, the total population of France amounted to over 68 million. The Ile-de-France region was the most populous region in France in the same year. INSEE said more than 12 million French citizens lived in the Ile-de-France. The ile-de-France region was followed by the Auvergne-Rhone-Alpes and Nouvelle-Aquitaine regions in the southern part of the country.

- Furthermore, the demand for new industrial facilities, office buildings, multifamily properties, data centers, and advanced technology manufacturing spaces is soaring. Several organizations are expanding their office space in the country, which will further create high demand for HVAC equipment and services.

- Inflation and supply chain disruptions drive up raw material costs, directly impacting manufacturing costs for HVAC systems. Notably, essential materials like steel, copper, and aluminum are witnessing significant cost hikes, further burdening HVAC manufacturers. As a result, small- and mid-sized HVAC companies face margin limitations, directly impacting profits and hindering the ability to invest in R&D (research and development). This, in turn, hampers the market's growth potential.

- France's macroeconomic landscape saw no respite. It grappled with persistently high inflation and interest rates and looming fears of recession amid escalating geopolitical tensions. This backdrop of uncertainty has left consumers across various sectors exercising caution. While a market rebound is anticipated, its timing and trajectory remain ambiguous. In addition, programs offering financial incentives for retrofitting old systems with new, efficient ones boost market growth.

France HVAC Market Trends

Residential Sector to Witness a Significant Growth

- The growth of the market can be attributed to factors like a strong preference for electric heating systems over gas, a domestic air conditioning industry that has transitioned to heat pumps, and the implementation of government initiatives to promote heat pump installation, including grant schemes like FranceRenov which provides up to EUR 10,000 (USD 10,884.45) per household. New energy-efficiency standards for new homes have also played a role in France's achievements. Moreover, the rise in residential construction in France is expected to drive the market.

- For instance, in September 2023, France spearheaded a push to transition from traditional residential fuel and gas heaters to heat pumps, aiming to establish a domestic industry for these devices. This initiative forms a pivotal part of France's comprehensive, multi-year environmental strategy. The country is looking to retire its last few coal-fired power plants, actively advocating for a shift from thermal engines to electric vehicles and promoting heat pumps as the primary heating solution for households.

- The desire to lower carbon footprints and the rising awareness of environmental concerns lead homeowners to invest in eco-friendly HVAC systems, energy-efficient and renewable energy-based HVAC solutions, such as heat pumps and solar-powered systems, which are becoming more popular in the country. According to Insee, more residential buildings were constructed in terms of floor space in France during the first 10 months of 2023 than non-residential buildings.

- The country's residential HVAC sector has seen a consistent uptick in demand for energy-efficient heating and cooling systems. This growth is primarily propelled by escalating energy costs and government incentives that encourage energy-efficient home upgrades. For instance, in April 2024, the French government officially allocated nearly EUR 1 billion (USD 1.09 billion) to fund the development of 75,000 intermediate housing units. This initiative is part of a broader strategy to address the pressing need for 500,000 more homes nationwide in the coming three years.

HVAC Equipment is Expected to Hold Significant Market Share

- France has stringent energy efficiency regulations and environmental standards for buildings, which drive the demand for HVAC equipment. Building operators and owners must comply with these regulations by implementing energy-efficient heating and cooling systems, ventilation solutions, and air quality management technologies. The need to meet regulatory requirements and achieve energy performance targets creates a significant demand for HVAC equipment focused on energy efficiency upgrades, retrofits, and compliance assessment.

- For instance, by 2027, France targets an annual production of one million new heat pumps within its borders. To bolster demand, the government plans to streamline the regulatory and administrative procedures for installing heat pumps on roofs, aligning with its broader agenda of reducing bureaucratic hurdles. Continuing initiatives like MaPrimeRenov and energy-saving certificates will aid consumers in purchasing heat pumps.

- In September 2023, the French government announced plans to increase subsidies for heat pumps. This move is intended to ensure that the net cost of purchasing a heat pump aligns with that of a gas heater, particularly for low-income families. Additionally, the government is actively working toward bolstering the domestic heat pump industry, with a target capacity set at manufacturing up to 1 million units annually.

- For instance, the EHPA's subsidies for residential heat pumps in Europe report, based on data from early 2023, highlights that property owners are eligible for grants in France. When installed in existing properties, these grants can reach up to EUR 15,000 (USD 16326.67) for ground-source heat pumps and up to EUR 9,000 (USD 9796.00) for air-source heat pumps. The production of many heat pumps stimulates demand for HVAC equipment across multiple industry segments.

France HVAC Industry Overview

The Frech HVAC market is fragmented, with the presence of major players like Johnson Controls International PLC, Carrier Corporation, Robert Bosch GmbH, Daikin Industries Ltd, and System Air AB. Prominent players in the French HVAC market are adopting strategies, including partnerships, mergers, innovations, investments, and acquisitions, to enhance product offerings and gain sustainable competitive advantage.

- April 2024: Mitsubishi Electric is poised to bolster its European HVACR presence by acquiring Aircalo, a prominent air conditioning group based in France. This strategic move enhances Mitsubishi's portfolio, enabling it to cater to a broader spectrum of hydronic systems. These systems are designed to address the rising market demand for heating and cooling solutions that are both efficient and environmentally friendly, focusing on reducing greenhouse gas emissions.

- December 2023: Sonepar acquired Hydeclim, a French company that distributes air conditioning and treatment solutions. This acquisition follows Sonepar's recent acquisitions in France, including Alliantz, focusing on photovoltaics, and CD Sud, specializing in (heating, ventilation, and air conditioning). By acquiring Hydeclim, Sonepar bolstered its presence in the HVAC sector, broadening its air conditioning and heating installers offerings, explicitly focusing on Western and Northern France.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Supportive Government Regulations Including Incentives for Saving Energy through Tax Credit Programs

- 5.1.2 Innovations in HVAC Technology Including Smart Systems and Renewable Energy Integration

- 5.1.3 Increased Construction and Retrofit Activity to Aid Demand

- 5.2 Market Challenges

- 5.2.1 The High Upfront Cost of Energy-efficient and Advanced HVAC Systems

- 5.2.2 Skilled Labor Shortages

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning/Ventilation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End-user Industry

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Johnson Controls International PLC

- 7.1.2 Carrier Corporation

- 7.1.3 Robert Bosch GmbH

- 7.1.4 Daikin Industries Ltd

- 7.1.5 System Air AB

- 7.1.6 Flaktgroup Inc.

- 7.1.7 LG Electronics Inc.

- 7.1.8 BDR Thermea Group

- 7.1.9 Mitsubishi Electric Hydronics & IT Cooling Systems SpA

- 7.1.10 Danfoss Inc.