アジア太平洋の使い捨て包装:市場シェア分析、産業動向・統計、成長予測(2023年~2029年)

Asia Pacific Single-use Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2023 - 2029)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1550041

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

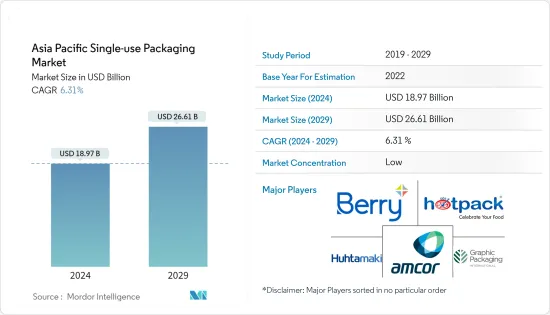

アジア太平洋の使い捨て包装の市場規模は、2024年に189億7,000万米ドルと推定され、2029年には266億1,000万米ドルに達すると予測され、予測期間(2024年~2029年)のCAGRは6.31%で成長する見込みです。

主なハイライト

- 金利上昇が成長の重荷となり、ロシアのウクライナ戦争が状況を悪化させるため、世界経済は減速すると予想されます。インフレは依然高水準で、米国と欧州の銀行の混乱は、すでに複雑化している経済環境にさらなる不確実性を加えています。アジアの内需は金融引き締めにもかかわらず底堅さを維持していますが、技術やその他の輸出に対する外需は冷え込んでいます。国際通貨基金(IMF)によれば、アジアの景気拡大は昨年の3.8%から4.6%へと加速しており、今年の世界経済成長の約70%をアジアが占めることになります。

- アジア太平洋には、中国やインドなど、フードサービスの需要が高い人口密集国や新興国が多くあります。その結果、使い捨て食品包装の需要は増加傾向にあり、今後数年間はこの地域で最も人気のある包装タイプになると予想されます。

- プラスチックは常に食品包装業界の重要な構成要素であり、消費者の利便性文化の基礎となっています。その低コストと高性能により、多くの外食・包装用途は段ボール、ガラス、金属といった従来の包装材料の代わりにプラスチックに切り替えてきました。この地域は、通常大量に必要とされる、家庭外や外出先での飲食品用包装製品の成長が見込まれています。例えば、使い捨て包装は、この地域ではクイックサービスレストランや施設のエンドユーザーにおける飲料水、お茶、コーヒー、トレイ、カトラリーなどの様々な用途に使用されています。

- さらに、この地域は、多くのエンドユーザー業界団体のおかげで、使い捨て包装市場の主要な投資家と採用者の一つです。包装食品の増加動向、レストランやスーパーマーケットの増加、ボトル入り飲料水や飲料消費の増加は、この地域の市場成長の重要な促進要因です。

- また、インドと中国の包装産業は急速なペースで成長しています。その背景には、複数の製造装置の導入、環境にやさしい材料、研究開発の重視の高まりがあります。その結果、魅力的で革新的な製品が手頃な価格で現地生産されています。「Make in India」のような政府の取り組みも、包装業界の成長を加速させると予想されます。

- パンデミックへの対応の結果、消費者の行動は大きく変化しました。バイヤーは以前よりも包装の汚染、衛生、持続可能性に関心を持つようになりました。パンデミックの間、消費者行動は使い捨ての箱、カトラリー、カップ、パッケージなどの使い捨て包装を使用する方向に傾くと予想されました。消費者のダイナミックなニーズと、包装の種類に対する重点的なアプローチは、パンデミック後も変わらないと思われます。したがって、アジアにおける使い捨て包装のパンデミック後の将来は、需要面で有望と思われます。

- この地域におけるプラスチック材料の広範な使用は、環境にかなりの脅威を与えており、各国政府と世界の規制機関はこの問題に対処するための措置を講じています。この問題に対処するため、インドなどの国々は、実用性が低く、ポイ捨ての可能性が高い特定された使い捨てプラスチック製品の生産、輸入、保管、流通、販売、使用を禁止しています。禁止品目のリストには、プラスチックの棒を含むイヤホン、風船用のプラスチックの棒、プラスチックの旗、キャンディーの棒、アイスクリームの棒、装飾用のサーモチョコレート、プラスチックの皿、コップ、グラス、カトラリー、フォーク、かき混ぜスティックが含まれています。スプーン、ナイフ、ストロー、トレイ、菓子箱を囲む包装・梱包用フィルム、招待状、タバコの箱、プラスチック製またはPVC製のバナーなど、100ミクロン未満というサイズ制限が設けられています。

アジア太平洋の使い捨て包装市場の動向

クイックサービスレストランが市場で大きなシェアを占める見込み

- インドでは、カフェチェーンがQSRよりも急成長しています。これは、メニューの価格が高いにもかかわらず、向上心のある若い消費者がカフェでの会合や交流を好むためです。例えば、インドのTim HortonsはAG Cafeとのジョイントベンチャーです。投資運用会社のゲートウェイ・パートナーズと小売・ファッション複合企業のアパレル・グループがAGカフェを所有しています。同社は2026年までにインドで120店舗を新規オープンする計画です。

- さらに、スターバックスとタタ・コンシューマー・プロダクツの合弁会社であるタタ・スターバックス(TST)は、2024年1月、2028年までにインドで1,000店舗の新規出店を計画し、従業員を倍増させると発表しました。地元チェーンが熾烈な競争を繰り広げている中でのことです。タタ・スターバックスは2012年10月に最初のカフェをオープンして以来、インドで事業を展開しており、これまでに390店舗をオープンしています。昨年度は71店舗でしたが、今年度は57店舗を追加しました。タタ・スターバックスは、インド全土のTier-2およびTier-3都市でのプレゼンスを拡大し、ドライブスルー、空港、24時間営業のカフェの数を拡大する計画です。

- 近年、食品業界は大きな変革期を迎えています。消費者はオンラインで食品を注文し、迅速に自宅まで配送してもらうことができます。フードデリバリー業界への変革の結果、顧客の注文のほとんどはレストランのアプリケーションやウェブサイトから直接行われるようになりました。その結果、レストランやその他の食品施設は、様々な方法でデジタル注文や食品配達を管理しています。単独で行っているところもあれば、Uber Eats、Swiggy、Zomatoといったサードパーティプラットフォームの利用も増えています。

- デジタル時代の文化は、オンラインで注文し、料理を配達する人々の数を増やしました。これは主に、ミレニアル世代とZ世代がほとんどの食事をオンラインで注文することに慣れているためです。この地域のより多くの人々がこの動向を採用するにつれて、オンライン注文と食品配達の市場規模は増加しています。例えば、Zomatoはインド有数のオンライン食品・食料品配達パートナーであり、同社の収益は2020年の3億7,000万米ドルから2023年には10億5,000万米ドルに拡大しました。その結果、使い捨て包装市場は市場の進化を認識し、それに応じて適応しています。

- インドと中国が都市化を続け、市民が近代的なライフスタイルを受け入れるにつれて、オンライン食品配達のニーズが大幅に高まっています。主要企業は、この増大する需要を満たし、それを活用しようと努力しています。注文をする際、顧客はチェン店食品の手頃な価格に留意しており、オンライン配達の需要の高まりと清潔な食品包装条件とが相まって、この地域での使い捨て包装製品の成功を確実なものにすると思われます。

中国が市場で大きなシェアを占めると予想される

- 中国のファーストフード部門は、都市化、座りがちなライフスタイルを持つ若い消費者層の増加、食生活の嗜好の変化などが相まって、近年かなりの拡大を経験しています。市場の自由化に向けた北京の継続的な取り組みがこの成長をさらに加速させ、外資にとって有利な市場を提供しています。

- 包装は常に飲食品の成功に重要な役割を果たしてきました。中国の包装産業は、一人当たり所得の増加、社会環境の変化、人口動態の変化の影響を受けています。新しい包装材料、プロセス、形態が必要とされています。

- QSRにおける使い捨てのフードサービス包装は、世界的にペースの速い生活には欠かせないものとなっています。使い捨て包装により、外食産業は賢明で安全、かつコスト効率の良い方法で食事を包装することができ、同時に顧客には便利で効率的な食事の輸送方法を提供することができます。中国では、QSRブランドが店舗数を増やしています。KFCは2023年4月現在、9,650店舗を展開しています。マクドナルドは5,746店、サブウェイは613店、ドミノ・ピザは613店、バーガーキングは613店、タコベルは1,494店です。2000年代に入ると、いくつかの国内ファストフード・ブランドが中国市場に参入し始め、現代風にアレンジした中国風料理を提供しています。例えば、ダイコス、Yonghe King、味千ラーメンなどです。

- スターバックスは、コーヒーに加え、ペストリー、サンドイッチ、ラップなど、より幅広いフードメニューを提供することで、急成長するファストフード分野での存在感を高めるべく、メニューの多様化を進めてきました。メニューの多様化により、同社は使い捨ての箱、クラムシェル、紙コップを使用しています。さらに、中国におけるスターバックスの店舗数は2023年に6,804店舗に達し、2018年の3,521店舗から大幅に増加しました。

- 中産階級に入る中国人消費者の増加に伴い、国際的なファーストフードチェーンはかなりの成長を遂げる可能性を秘めています。中国のデリバリーやオンライン注文市場は拡大を続けており、多くの中国のファーストフード店は、顧客のニーズの変化に対応するために、そのオペレーションを適応させています。その多くは、デジタル・マーケティング・イニシアチブに多額の投資を行い、QSRやオンライン注文を容易にするため、環境に優しい使い捨て包装を採用しています。

アジア太平洋の使い捨て包装業界の概要

アジア太平洋の使い捨て包装市場は断片化されており、Berry Global Inc.、Amcor Group GmbH、Huhtamaki Oyj、Hotpack Packaging Industries LLCなど、複数の世界的・地域企業がこの競争の激しい市場空間で注目を集めようと争っています。この市場の特徴は、製品の差別化が低く、製品の普及が進み、競合が多いことです。

- 2023年8月:持続可能な包装ソリューションの開発と製造の世界的企業であるAmcorは、Phoenix Flexiblesの買収を発表し、急成長するインド市場に生産能力を追加しました。Phoenix Flexiblesはインドのグジャラート州に工場を持ち、食品、ホームケア、パーソナルケアなどの用途のフレキシブル包装販売で年間約2,000万米ドルの収益を上げています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度:ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- オンラインフードデリバリーサービスの動向

- クイックサービスレストランの増加

- 市場抑制要因

- 使い捨て包装用プラスチックの使用に対する規制

第6章 市場セグメンテーション

- 材料タイプ別

- 紙と板紙

- プラスチック

- ガラス

- その他の材料タイプ

- エンドユーザー産業別

- 食品

- 飲料

- パーソナルケア

- 医薬品

- その他エンドユーザー産業

- 国別

- 中国

- 日本

- インド

- オーストラリア・ニュージーランド

第7章 競合情勢

- 企業プロファイル

- Berry Global Inc.

- Amcor Group GmbH

- Huhtamaki Oyj

- Hotpack Packaging Industries LLC

- Graphic Packaging International LLC

- Detpak-Detmold Group

- Sonoco Products Company

- Oji Holdings Corporation

- Zhejiang Pando EP Technology Co.

第8章 投資分析

第9章 市場の将来

目次

The Asia Pacific Single-use Packaging Market size is estimated at USD 18.97 billion in 2024, and is expected to reach USD 26.61 billion by 2029, growing at a CAGR of 6.31% during the forecast period (2024-2029).

Key Highlights

- The global economy is expected to slow as rising interest rates weigh on growth and Russia's war in Ukraine worsens the situation. Inflation remains high, and banking turmoil in the United States and Europe has added more uncertainty to an already complicated economic environment. Asia's domestic demand has remained resilient despite monetary tightening, but external demand for technology and other exports is cooling. According to the International Monetary Fund, Asia will account for about 70% of global economic growth this year as the region's expansion accelerates to around 4.6% compared to 3.8% last year.

- In Asia-Pacific, there are many densely populated countries and emerging economies where food services are in high demand, such as China and India. As a result, the demand for single-use food packaging is on the rise, and it is expected to become the most popular type of packaging in the region over the next few years.

- Plastic has always been a key component of the food packaging industry, which is the basis of the consumer's convenience culture. Due to their low cost and high performance, many food service and packaging applications have switched to plastics instead of traditional packaging materials such as corrugated paper boards, glass, and metals. The region is expected to grow in packaging products for out-of-home and on-the-go food and beverage products that are usually required in large quantities. For instance, single-use packaging is used in the region for various applications for drinking water, tea, coffee, trays, and cutleries in quick-service restaurants and institutional end users.

- Further, the region is one of the major investors and adopters of the single-use packaging market, owing to many end-user industry organizations. The growing trend of packed meals, the increasing number of restaurants and supermarkets, and increasing bottled water and beverage consumption are significant driving factors of the regional market's growth.

- In addition, the packaging industry in India and China is growing at a rapid pace. This is due to the introduction of multiple manufacturing units, environmentally friendly materials, and increased emphasis on R&D. The result is attractive and innovative products that are produced locally at an affordable price. Government initiatives such as 'Make in India' are also expected to accelerate the growth of the packaging industry.

- As a result of the response to the pandemic, consumer behavior significantly changed. Buyers are more concerned about packaging contamination, hygiene, and sustainability than before. During the pandemic, consumer behavior is expected to become more inclined toward using single-use packaging such as disposable boxes, cutlery, cups, and packages. Consumers' dynamic needs and focused approach toward the type of packaging will remain even after the pandemic. Therefore, the post-pandemic future for single-use packaging in Asia looks promising in terms of demand.

- The widespread use of plastic materials in the region has posed a considerable threat to the environment, and governments and global regulatory bodies are taking steps to address this issue. To address this issue, countries such as India have banned the production, import, storage, distribution, sale, and use of identified single-use plastic products, which are of low utility and have a high littering potential. The list of prohibited items includes earbuds containing plastic sticks, plastic sticks for balloons, plastic flags, candy sticks, ice-cream sticks, thermocol for decoration, plastic plates, cups, glasses, cutlery, forks, and stirrers. Spoons, knives, straws, trays, wrapping or packing films surrounding sweet boxes, invitation cards, cigarette packets, and plastic or PVC banners, all smaller than 100 microns.

Asia Pacific Single-use Packaging Market Trends

Quick Service Restaurants are Expected to Hold a Significant Share in the Market

- Cafe chains are growing faster than QSRs in India because young, aspirational consumers prefer to meet and socialize in cafes despite the high menu prices. For instance, Tim Hortons in India is part of a joint venture with AG Cafe. Gateway Partners, an investment manager, and Apparel Group, a retail and fashion conglomerate, own AG Cafe. The company plans to open 120 new stores in India by 2026.

- Further, Tata Starbucks (TST), a Starbucks-Tata Consumer Products joint venture, announced on January 2024 that it plans to open 1,000 new cafes in India by 2028 and will double its workforce. This comes when local chains are competing fiercely. Tata Starbucks has been operating in India since October 2012, when it opened its first cafe, and has so far opened 390 stores. It has added 57 stores this fiscal year, while it had 71 stores in the previous year. Tata Starbucks plans to expand its presence in tier-2 and tier-3 cities across India and expand its number of drive-through, airport, and 24/7 cafes.

- In recent years, the food industry has undergone a major transformation. Consumers can order food online and have it shipped to their residences quickly. As a result of the alterations made to the food delivery industry, most customer orders are now being placed directly from restaurants' applications or websites. As a result, restaurants and other food establishments manage digital ordering and food delivery in various ways. Some are doing it independently, while there has been an increase in the use of third-party platforms such as Uber Eats, Swiggy, and Zomato.

- The digital age culture has increased the number of people ordering and delivering food online. This is mainly because Millennials and Generation Z are used to ordering most of their food online. As more people in this region adopt this trend, the size of the online order and food delivery market is increasing. For instance, Zomato is one of India's leading online food and grocery delivery partners, and the company's revenue expanded to USD 1.05 billion in 2023 from USD 0.37 billion in 2020. As a result, the single-use packaging market is recognizing the evolution of the market and adapting accordingly.

- The need for online food delivery has grown significantly as India and China continue to urbanize and citizens embrace a modern lifestyle. Significant companies are striving to meet this increasing demand and capitalize on it. When making an order, customers are mindful of the affordability of joint food, and the rising demand for online delivery coupled with clean food packaging conditions will ensure the success of single-use packaging products in the region.

China is Expected to Hold a Significant Share in the Market

- The fast-food sector in China has experienced considerable expansion in recent years due to a combination of urbanization, growing demographic of young consumers with a sedentary lifestyle, and changing dietary preferences. Beijing's ongoing efforts to liberalize the market have further amplified this growth, providing a lucrative market for foreign investment.

- Packaging has always played an important role in the success of food and beverages. The Chinese packaging industry is affected by increasing per capita income, the changing social environment, and changing demographics. New packaging materials, processes, and forms are needed.

- Single-use food service packaging in QSRs has become vital to a globally fast-paced life. Single-use packaging allows food service establishments to package meals in a sensible, safe, and cost-effective manner while providing customers with a convenient and efficient way to transport meals. In China, QSR brands are increasing the number of outlets. KFC has 9,650 outlets as of April 2023. McDonald's, Subway, Domino's Pizza, Burger King, and Taco Bell have 5,746, 613, 613, and 1,494 outlets, respectively. At the beginning of the 2000s, several domestic fast-food brands began to enter the Chinese market, providing Chinese-style cuisine with a contemporary twist. Examples of such brands include Dicos, Yonghe King, and Ajisen Ramen.

- In addition to coffee, Starbucks has been diversifying its menu offerings to include a broader range of food items, including pastries, sandwiches, and wraps, to expand its presence in the rapidly growing fast-food sector. Due to the diversification of the menu, the company uses single-use boxes, clamshells, and paper cups. Furthermore, Starbucks stores in China reached 6,804 in 2023, significantly increasing from 3,521 stores in 2018.

- With the increasing number of Chinese consumers entering the middle class, international fast-food chains have the potential to experience considerable growth. The Chinese delivery and online ordering market continues to expand, and many Chinese fast-food establishments are adapting their operations to meet the changing needs of their customers. Many are investing heavily in digital marketing initiatives and adapting environmentally friendly single-use packaging to facilitate QSR and online ordering.

Asia Pacific Single-use Packaging Industry Overview

The Asia-Pacific single-use packaging market is fragmented, with several global and regional players, such as Berry Global Inc., Amcor Group GmbH, Huhtamaki Oyj, and Hotpack Packaging Industries LLC, vying for attention in this contested market space. This market is characterized by low product differentiation, growing product penetration, and high competition.

- August 2023 - Amcor, a global player in developing and manufacturing sustainable packaging solutions, announced the acquisition of Phoenix Flexibles, adding capacity to the fast-growing Indian market. Phoenix Flexibles has a plant in Gujarat, India, and generates around USD 20 million in annual revenue from flexible packaging sales for applications such as food, home care, and personal care.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industrial Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Ongoing Trend of Online Food Delivery Services

- 5.1.2 Increasing Number of Quick-Service Restaurants

- 5.2 Market Restraints

- 5.2.1 Regulations Toward the Use of Plastics for Single Use Packaging

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Paper and Paperboard

- 6.1.2 Plastic

- 6.1.3 Glass

- 6.1.4 Other Material Types

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Personal Care

- 6.2.4 Pharmaceutical

- 6.2.5 Other End-user Industries

- 6.3 By Country

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 India

- 6.3.4 Australia and New Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Berry Global Inc.

- 7.1.2 Amcor Group GmbH

- 7.1.3 Huhtamaki Oyj

- 7.1.4 Hotpack Packaging Industries LLC

- 7.1.5 Graphic Packaging International LLC

- 7.1.6 Detpak - Detmold Group

- 7.1.7 Sonoco Products Company

- 7.1.8 Oji Holdings Corporation

- 7.1.9 Zhejiang Pando EP Technology Co.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日