米国の使い捨て包装:市場シェア分析、産業動向、成長予測(2025~2030年)

US Single Use Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 103 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644458

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

米国の使い捨て包装市場規模は2025年に276億9,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは2.72%で、2030年には316億7,000万米ドルに達すると予測されます。

同国では、利便性が高く印刷しやすいことから、使い捨て包装の需要が増加すると予想されています。使い捨てプラスチック包装は、二次汚染や病気を避けるために、いくつかの企業で必要とされています。使い捨て包装市場の拡大が加速すると考えられます。

主要ハイライト

- 小型で利便性の高い包装へのニーズの高まりと強い視覚的インパクトが、予測期間中の使い捨て包装の成長に寄与すると予想されます。使い捨て包装は、捨てられるかリサイクルされる前に一度だけ使用される製品のことです。プラスチック袋、ストロー、コーヒースターラー、ソーダや水のボトル、ほとんどの食品包装などがこれにあたる。

- 米国の軟質プラスチック包装産業は、直面するいくつかの包装課題に対して革新的な解決策を実施したため、健全な成長を目の当たりにしています。軟質包装・アソシエーション(FPA)によると、アメリカの消費者に受け入れられつつあることもあり、ブランドオーナーはパウチ、フィルム、バッグを包装ソリューションとして採用しつつあります。

- 製薬産業は、国内市場における使い捨てプラスチック包装の拡大を牽引しています。医療機器、消耗品、注射器、医薬品は、汚染の可能性を減らし、エンドユーザーの利益を守るため、使い捨てプラスチックで包装されることが多いです。さらに、ボトル入り飲料水、ソフトドリンク、アルコール飲料、レディトゥドリンク飲料、牛乳の需要増に対応するため、様々なサイズの包装の生産が増加していることから、使い捨てプラスチック飲料容器の市場は拡大すると予測されています。

- しかし、使い捨てプラスチック包装の増大する問題には、廃棄物や処分管理が含まれます。不適切な廃棄により、環境リスクとプラスチック廃棄物の増加が生じます。これはおそらく、同国の使い捨てプラスチック包装市場の妨げになると考えられます。

- 米国ではeコマースが大幅に加速しているが、これはCOVID-19の流行による閉鎖が原因です。しかし、このパンデミックは2020年初頭の小売売上高に打撃を与えました。このような要因は、米国の小売産業における軟質プラスチック包装の使用量にマイナスの影響を与えました。しかし、米国の小売セクターは2020年後半に大幅な急増を示し、この地域の使い捨て軟質プラスチック包装の使用量を回復させました。さらに、ロシア・ウクライナ戦争は包装エコシステム全体に影響を与えています。

米国の使い捨て包装市場動向

利便性と実用性の向上を提供する軟質な使い捨てプラスチック包装製品

- Biologicaldiversity.orgによると、米国民は年間1,000億枚のレジ袋を使用しており、その製造には1,200万バレル(19億785万リットル)の石油を必要とします。アメリカ人は一人当たり平均365枚のレジ袋を年間使用しています。デンマークの人々は、年間平均4枚のレジ袋を使用しています。

- さらに、コロナウィルスの蔓延により、そのバリア性から使い捨てプラスチックの採用が一時的に増加しました。主要使用者は、レストラン、食料品店、eコマース・ベンダーです。食料品店ではレジ袋の使用量が急増しています。家庭から出るゴミの量は、パンデミック前に比べて最大で50%増加しており、需要の増加を示しています。それでも、州がほぼ正常なシナリオを達成し次第、使い捨てプラスチックを禁止するためのプレコビッドの規制が確立され、これらの包装材の流通は沈静化すると予想されます。

- クイックサービスレストラン(QSR)において、使い捨て包装と再利用可能な食器を比較すると、使い捨てシステムには、特に二酸化炭素排出量と淡水消費量において利点があります。これらは、複数回使用する食器の洗浄、消毒、乾燥に必要なエネルギーと水によるものです。ベースライン・シナリオでは、ポリプロピレンをベースとするマルチユースシステムは、紙をベースとする使い捨てシステムに比べ、CO2排出量は2.5倍以上、淡水使用量は3.6倍でした。

- その結果、市場に参入するベンダーがリサイクル率の高い包装を導入したり、分解を助ける材料を取り入れたりすれば、使い捨てプラスチック市場は維持できる可能性があります。上記のような懸念から、バイオベースの使い捨てプラスチック製品を導入する新規参入企業が市場に参入しています。

- ITCによると、2021年のプラスチック廃棄物とスクラップの輸入額は約3億6,872万9,000米ドルで、前年比58.28%増となっており、プラスチック破片から使い捨てプラスチックへの転換の需要が増加していることを示しています。

医療と医薬品セグメントが著しい成長率を示す

- 使い捨て包装、プラスチックベースの包装材料の使用の増加、パンデミックの中での医療製品と包装の需要の増加は、世界的にプラスチック廃棄物の発生を大幅に急増させました。主要ニーズの一つは、衛生上の懸念から、RT-PCRを採用したコロナウイルス検査キットのプラスチックベースの部品を廃棄することでした。

- 使い捨てプラスチックは世界的に禁止されつつあるが、プラスチック袋や容器の再利用による二次汚染の懸念から、米国のような国ではCOVID-19パンデミックの間、使い捨てプラスチックの禁止を一時的に撤回または延期せざるを得なかった。さらに、ニューヨーク州では2020年3月に開始されたレジ袋の全面禁止が、パンデミックのため2020年5月に保留されました。カリフォルニア州とオレゴン州もビニール袋の禁止を中断し、コネチカット州、デラウェア州、ハワイ州、ニュージャージー州、ニューメキシコ州、オレゴン州、ワシントン州などは同様の禁止を延期しました。

- PPEの大半は、ポリウレタン(PU)、ポリプロピレン(PP)、ポリカーボネート(PC)、低密度ポリエチレン(LDPE)、ポリ塩化ビニル(PVC)などのポリマーでできています。PSとLDPEはほとんどリサイクルされないが、PETとHDPEは広くリサイクルされ、PVCとPPはリサイクルされないことが多いです。

- 環境への影響を考慮しつつ、膨大な医療のニーズに最適な効果的な材料が求められています。しかし、患者や従業員を保護するために必要な無菌性と衛生性を維持しながら、プラスチックに代わる適切かつ合理的な価格の代替品を特定することは困難です。人口の増加により、医療用品を大規模かつ時間通りに提供する能力に、さらなる負担がかかっています。従って、使い捨てプラスチックは医療セグメントで今後も大きなシェアを占めると予想されます。

- CMSによると、国民一人当たりの医療費は2028年に1万7,000米ドルを超えると予想されています。医療支出額の増加は、滅菌製品の採用を必要とすることにより、市場を牽引する可能性があり、使い捨て包装企業の数は、製薬部門で大きな成長を確認するために増加します。

米国の使い捨て包装産業概要

米国の使い捨て包装市場は、Dart Container Corporation、Georgia-Pacific LLC、Graphic Packaging International Inc、Novolexなど数社の有力企業が参入しているほか、新規参入企業もあり、適度に統合されています。各社は市場シェアを維持するために技術革新を続け、戦略的パートナーシップを結んでいます。

2022年7月、Georgia-Pacificのブロードウェイ工場は拡大のために5億米ドルの投資を受けました。この投資は、同社の消費者向けティシュとタオルの小売事業を大幅に改善するものです。スルー・エア・ドライ(TAD)技術を使って新しい製紙工場を建設し、関連インフラと変換ツールを追加します。Georgia-Pacificのプレミアムブランドは成長することができ、同社のプレミアムプライベートブランド製品や現在と将来の顧客の製品は、この変化によって支えられることになります。2024年が完成予定日

2022年4月、Georgia-Pacificは、ジョージア州マクドナーとペンシルベニア州ジョンズタウンに新しい施設を建設し、そこでリサイクル可能なオリジナルの紙パディング封筒を製造します。Georgia-Pacificは、フェニックス地域の同社工場に新たに増設された第3の生産ラインと組み合わせることで、より環境に優しいeコマース包装ソリューションに対する需要の高まりに対応するため、生産能力を3倍以上に増強しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業のサプライチェーン分析

- 産業の魅力-ポーターファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 主要規格と規制

- COVID-19の市場への影響評価

- 世界の使い捨て包装市場概要

第5章 市場力学

- 市場促進要因

- 軽量化とサステイナブルソリューション(紙ベースのカップなど)の使用への継続的動向

- 利便性と実用性の向上を提供する軟質な使い捨て包装製品

- 市場課題

- 使い捨てプラスチック包装製品の成長に対する主要抑制要因としての厳しい規制

- 使い捨てプラスチックによる環境問題の高まり

第6章 市場セグメンテーション

- 材料別

- 紙と板紙

- プラスチック

- アルミニウム

- その他

- エンドユーザー産業別

- 食品

- 飲料

- 医療医薬品

- パーソナルケア

- その他

第7章 競合情勢

- 企業プロファイル

- Dart Container Corporation

- Georgia-Pacific LLC

- Graphic Packaging International Inc.

- Novolex

- Pactiv LLC

- Snapsil Corporation

- Berry Global Inc.

- Amcor Plc

- PPC Flexible Packaging LLC

- Fuling Plastic USA, Inc.

第8章 投資分析

第9章 市場の将来

目次

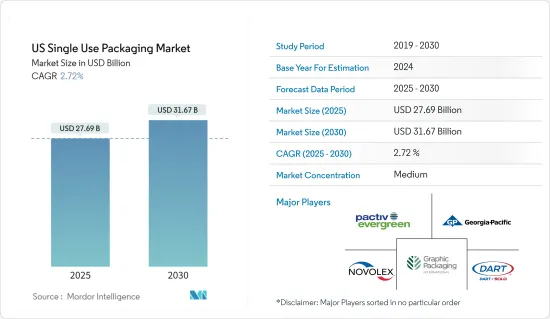

The US Single Use Packaging Market size is estimated at USD 27.69 billion in 2025, and is expected to reach USD 31.67 billion by 2030, at a CAGR of 2.72% during the forecast period (2025-2030).

The demand for single-use packaging in the country is anticipated to increase due to its high convenience and printability. Single-use plastic packaging is required by several businesses to avoid cross-contamination and disease. It will accelerate the expansion of the market for single-use packaging.

Key Highlights

- The increasing need for small and more convenient packaging and a strong visual impact is expected to contribute to the growth of single-use packaging over the forecast period. Single-use packaging is for products used only once before they are thrown away or recycled. These items are plastic bags, straws, coffee stirrers, soda and water bottles, and most food packaging.

- The United States' flexible plastic packaging industry is witnessing healthy growth as it implemented innovative solutions for the several packaging challenges it faced. According to the Flexible Packaging Association (FPA), brand owners are adopting pouches, films, and bags as a go-to packaging solution, partly due to rising acceptance by American consumers.

- The pharmaceutical industry is driving the expansion of single-use plastic packaging in the nation's market. Medical equipment, supplies, syringes, and medications are frequently packaged in single-use plastic since it decreases the possibility of contamination, protecting the end-users interests. Further, the market for single-use plastic beverage containers is predicted to expand due to the rising production of various package sizes to meet the growing demand for bottled water, soft drinks, alcoholic beverages, ready-to-drink beverages, and milk.

- However, growing issues with single-use plastic packaging include waste and disposal management. Environmental risks and a rise in plastic waste result from improper disposal. It will probably hamper the market for single-use plastic packaging in the country.

- The United States has witnessed a significant acceleration in e-commerce, driven by lockdowns imposed due to the outbreak of COVID-19. However, the pandemic made a dent in retail sales at the start of 2020. Such factors negatively impacted the usage of flexible plastic packaging in the US retail landscape in the respective months. However, the retail sector in the United States witnessed a significant surge in late 2020, which bounced back the usage of single-use flexible plastic packaging in the region. Further, the Russia-Ukraine war has an impact on the overall packaging ecosystem.

US Single Use Packaging Market Trends

Flexible Single-use Plastic Packaging Products Offering Increased Convenience and Utility

- According to Biologicaldiversity.org, American citizens use 100 billion plastic bags annually, which require 12 million barrels (1907.85 million liters) of oil to manufacture. Americans use an average of 365 plastic bags per person per year. People in Denmark use an average of four plastic bags per year.

- Moreover, the spread of coronavirus has temporarily increased the adoption of single-use plastic due to its barrier properties. The primary users are restaurants, grocery stores, and e-commerce vendors. Grocery stores have sharply increased plastic bag usage. Households are generating up to 50% more waste by volume than pre-pandemic, indicating increased demand. Still, as soon as the state achieves near-normal scenarios, the pre-covid established regulations to ban single-use plastics are expected to subside the circulation of these packaging materials.

- In comparing single-use packaging to reusable tableware in quick-service restaurants (QSR), single-use systems have their advantages, particularly in carbon emissions and freshwater consumption. These are due to the energy and water needed to wash, sanitize, and dry multi-use tableware. In the baseline scenario, the polypropylene-based multi-use system generated over 2.5 times more CO2 emissions and used 3.6 times the amount of freshwater than the paper-based single-use system.

- As a result, the market for single-use plastics might sustain if the vendors in the market introduce packaging with higher recycling rates or include materials that help in decomposition. The above concerns have led to the entry of new players in the market that are introducing bio-based single-use plastic products.

- According to the ITC, in 2021, the value of imports of plastic waste and scrap amounted to around USD 368.729 million, a 58.28% growth in imports from the previous year, indicating the demand for an increase in the transformation of plastic debris to single-use plastic.

Healthcare and Pharmaceutical Segment to Witness Significant Growth Rates

- The growing usage of single-use packaging, plastic-based packaging materials, and the increasing demand for medical products and packaging amid the pandemic has significantly spiked plastic waste generation worldwide. One primary need was disposing plastic-based parts of the coronavirus testing kits employing RT-PCR for hygienic concerns.

- Although single-use plastics are increasingly banned worldwide, concerns of cross-contamination by reusing plastic bags and containers have forced countries like the United States to temporarily revoke or defer bans on single-use plastics during the COVID-19 pandemic. Further, a statewide ban on plastic bags in New York initiated in March 2020 was put on hold in May 2020 owing to the pandemic. California and Oregon also suspended their bans on plastic bags, while Connecticut, Delaware, Hawaii, New Jersey, New Mexico, Oregon, Washington, etc., postponed similar prohibitions.

- The majority of PPEs are made up of polymers like polyurethane (PU), polypropylene (PP), polycarbonate (PC), low-density polyethylene (LDPE), and polyvinyl chloride (PVC). PS and LDPE are rarely recycled plastics; PET and HDPE are widely recycled, while PVC and PP are often not recycled.

- An effective material is needed to meet the vast healthcare needs best while considering its influence on the environment. However, maintaining the degree of sterility and sanitation necessary for protecting patients and employees while identifying appropriate and reasonably priced alternatives to plastic is difficult. The growing population puts extra strain on the ability to provide medical supplies on a large scale and on time. Thus, it is anticipated that single-use plastics will continue contributing significant shares in the healthcare sector.

- According to the CMS, national health expenditure per capita is expected to exceed USD 17,000 in 2028. The increase in the health expenditure values may drive the market by necessitating the adoption of sterilizing products increasing the number of single-use packaging companies to witness significant growth in the pharmaceutical sector.

US Single Use Packaging Industry Overview

The single-use packaging market in the United States is moderately consolidated, with new firms entering the market as well as the entry of a few dominant firms, including Dart Container Corporation, Georgia-Pacific LLC, Graphic Packaging International Inc, Novolex, and others. The firms keep innovating and entering strategic partnerships to retain their market share.

In July 2022, Georgia-Pacific's Broadway mill received an investment of USD 500 million for expansion. The expenditures will significantly improve the company's retail consumer tissue and towel business. Through-air-dried (TAD) technology is being used to construct a new paper mill and add related infrastructure and conversion tools. Georgia-Pacific's premium brands will be able to grow, and their premium private label products, as well as those of present and future clients, will be supported by the changes. 2024 is the projected completion date.

In April 2022, Georgia-Pacific constructed new facilities in McDonough, Georgia, and Jonestown, Pennsylvania, where they will manufacture an original, recyclable paper-padded envelope. Georgia-Pacific has more than tripled its capacity to help satisfy the rising demand for more environmentally friendly e-commerce packaging solutions when paired with the newly increased manufacturing capacity of a third production line at the company's factory in the Phoenix region.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter Five Forces

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key Standards and Regulations

- 4.5 Assessment of Impact of COVID-19 on the Market

- 4.6 Overview of the Global Single-use Packaging Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Ongoing Trend Toward Lightweight and Use of Sustainable Solutions (such as Paper-based Cups)

- 5.1.2 Flexible Single-use Packaging Products Offering Increased Convenience and Utility

- 5.2 Market Challenges

- 5.2.1 Stringent Regulations as Major Impediment to the Growth of Single-use Plastic Packaging Products

- 5.2.2 Rising Environmental Concerns due to Single-use Plastic

6 Market Segmentation

- 6.1 By Material

- 6.1.1 Paper and Paperboard

- 6.1.2 Plastics

- 6.1.3 Aluminium

- 6.1.4 Other Materials

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Healthcare and Pharmaceutical

- 6.2.4 Personal Care

- 6.2.5 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dart Container Corporation

- 7.1.2 Georgia-Pacific LLC

- 7.1.3 Graphic Packaging International Inc.

- 7.1.4 Novolex

- 7.1.5 Pactiv LLC

- 7.1.6 Snapsil Corporation

- 7.1.7 Berry Global Inc.

- 7.1.8 Amcor Plc

- 7.1.9 PPC Flexible Packaging LLC

- 7.1.10 Fuling Plastic USA, Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 103 Pages

- 納期

- 2~3営業日