|

市場調査レポート

商品コード

1694043

欧州の車載半導体:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Automotive Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の車載半導体:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

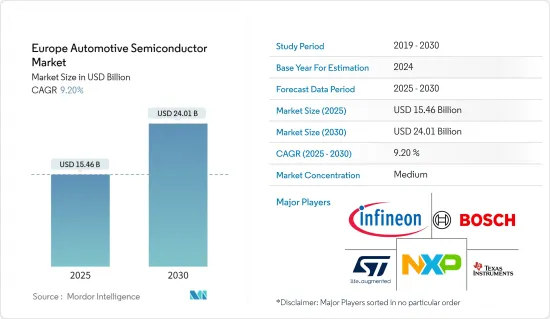

欧州の車載半導体市場規模は2025年に154億6,000万米ドル、2030年には240億1,000万米ドルに達すると予測、予測期間中(2025~2030年)のCAGRは9.2%。

主要ハイライト

- 車載半導体は、車載産業に特化して設計・使用される半導体チップの一種です。これらのチップは、車載の様々な電子部品やシステムの機能において重要な役割を果たしています。安全システム、インフォテインメントシステム、エンジン制御ユニット、センサなど、多くの機能や特徴に電力を供給し、制御する役割を担っています。

- 車載半導体は、車載が技術的に高度化するにつれて、ますます重要性を増しています。自律走行、電動パワートレイン、コネクティッド・カーシステムなどの先進技術を統合するために不可欠です。これらの半導体は、耐久性、信頼性、過酷な環境での動作能力など、車載産業特有の要件を満たすように設計されています。

- 車載半導体の主要用途のひとつに、ADAS(先進運転支援システム)があります。これらのシステムは、センサ、カメラ、プロセッサを使用して、車両の安全性を高め、リアルタイムでドライバーを支援します。半導体は、アダプティブクルーズコントロール、車線維持支援、自動緊急ブレーキ、死角検出、歩行者検出などの機能を実現し、運転をより安全にして事故のリスクを低減します。

- 半導体は、車載の先進的インフォテインメントシステムの開発において重要な役割を果たしています。これらのシステムは、エンターテインメント、ナビゲーション、通信機能をシームレスに統合します。車載半導体は、タッチスクリーン、音声認識、接続オプション、マルチメディア再生を可能にし、運転体験をパーソナライズされた接続されたものに変えます。

- 欧州では車載用半導体産業への投資が増加しており、市場開拓を後押ししています。例えば、2023年8月、Robert Bosch GmbH、TSMC、NXP Semiconductors NV、Infineon Technologies AGは、ドイツのドレスデンにあるESMC(European Semiconductor Manufacturing Company GmbH)に共同で投資し、先進的な半導体製造サービスを提供する計画を発表しました。ESMCは、急成長する車載と産業部門の将来的な生産能力要件をサポートする300mmファブ建設に向けた実質的な一歩を踏み出すとしています。

- このプロジェクトは、欧州チップ法の枠組みの下で設計されています。計画されているウエハー工場は、TSMCの28/22ナノメーターのプレーナーCMOSと16/12ナノメーターのFinFETプロセス技術で月産4万枚(12インチ)の生産能力を持ち、先進的なFinFETトランジスタ技術で欧州の半導体製造エコシステムを強化し、約2,000人のハイテク専門職の直接雇用を創出すると予想されています。ESMCは、2024年後半に工場の建設を開始し、2027年末の生産開始を目指しています。

- 半導体は車載の接続性を実現し、コネクテッドカー技術の基盤を形成します。半導体は無線通信システムに電力を供給し、車両が他の車両(V2V)、インフラ(V2I)、インターネット(V2X)と接続できるようにします。この接続性によってリアルタイムのデータ交換が容易になり、交通情報の更新、遠隔車両診断、無線アップデート、さらには自律走行機能などの機能が実現します。

- 環境の持続可能性への関心が高まり、二酸化炭素排出量を削減する必要性が高まる中、電気車載(EV)は欧州で絶大な人気を博しています。EVは、電源管理、バッテリー管理、モーター制御システムにおいて半導体技術に大きく依存しています。EVの需要が増え続けるにつれ、車載半導体の需要も増加しています。

- 欧州の車載工業会(ACEA)によると、欧州におけるバッテリー電気車載(BEV)とプラグインハイブリッド電気車載(PHEV)の販売台数は、2022年第2四半期の55万9,810台から2023年第3四半期には75万7,830台に増加しました。このようなEV需要の増加は、調査対象市場の成長に有利な機会を提供すると考えられます。

- しかし、開発・生産コストが高いことが、調査対象市場の成長にとって大きな障壁となっています。複雑な製造プロセスと検査要件がこれらの半導体を高価なものにしており、製造業者と消費者の両方にとっての値ごろ感を制限しています。

- さらに、ロシアとウクライナの紛争は半導体産業に大きな影響を与えると予想されます。この紛争は、以前から産業に影響を及ぼしている電子・半導体サプライチェーンの問題やチップ不足をすでに悪化させています。この混乱は、ニッケル、パラジウム、銅、チタン、アルミニウムといった重要な原料の価格変動をもたらし、材料不足を招く可能性があります。これはひいては、車載半導体の製造に影響を与える可能性があります。

欧州の車載半導体市場動向

乗用車セグメントが市場成長を牽引する展望

- 車載半導体は、乗用車内のさまざまな安全システムに応用されています。これらの半導体は、アンチロックブレーキシステム(ABS)、エレクトロニック・スタビリティコントロール(ESC)、先進運転支援システム(ADAS)を制御するパワーエレクトロニクスモジュールに使用されています。パワーフローを正確にモニタリング・調整することで、これらのシステムは車両の安定性、トラクション、総合的な安全性を向上させています。

- さらに、車載半導体は乗用車内の電力管理において重要な役割を果たしています。これらの半導体は、DC-DCコンバータ、電圧レギュレータ、その他の電力制御モジュールに使用され、効率的な配電と電気エネルギーの最適利用を保証しています。

- これらの小さな電子部品は、車両内のさまざまなシステムに統合され、先進的安全機能を実現し、より安全な運転体験を保証します。乗用車の安全性における車載半導体の主要用途のひとつに、アンチロック・ブレーキシステム(ABS)があります。ABSはセンサとマイクロコントローラによって車輪速度をモニタリングし、急ブレーキ時の車輪のロックを防止します。ブレーキ圧を素早く調節することで、車載半導体は車両の安定性を維持し、横滑りを防止して事故のリスクを低減します。

- また、エレクトロニック・スタビリティコントロール(ESC)システムにも採用されています。ESCは、センサ、加速度計、マイクロコントローラを使用して車両の力学をモニタリングし、個々の車輪に選択的にブレーキをかけます。車載半導体は、リアルタイムのデータ処理と精密な制御を可能にし、車両の安定性を高め、危険な状況での制御不能を防ぎます。

- 欧州における車載生産の増加は、車載半導体の需要を増加させる可能性が高いです。例えばOICAによると、フランスでは2023年に約150万台の車載が生産され、そのうち68.2%が乗用車でした。2022年にはフランスで約130万台の車載が生産されました。

- さらに、コネクテッドカー技術の普及は、ユーザーと車載との関わり方を一変させました。インフォテインメントシステムからADAS(先進運転支援システム)に至るまで、コネクテッドカー技術は、シームレスな通信とデータ処理を可能にする半導体チップに依存しています。車載におけるインターネット接続、クラウドサービス、データ分析の統合が進むにつれ、車載半導体の需要は飛躍的に伸びると予想されます。

高い市場成長率が期待されるドイツ

- 強力な車載産業で知られるドイツは、世界の車載半導体市場における主要参入企業の1つとしての地位を確立しています。車載メーカー、サプライヤー、技術企業の強固なエコシステムがあるドイツは、半導体開発と生産のハブとなっています。Infineon Technologies、Bosch、コンチネンタルAGなどの半導体企業は、ドイツで大きな存在感を示しています。これらの企業は、マイクロコントローラ、センサ、パワーマネージメントIC、接続性ソリューションなど、多様な車載半導体の生産を専門としています。

- ドイツの半導体企業は、車載メーカー、研究機関、新興企業としばしば協力し、技術革新を促進し、技術進歩を推進し、時価総額を高めています。

- 例えば、2024年1月、Infineon Technologies AGとGlobalFoundriesは、InfineonのAURIX TC3x 40ナノメーター車載マイクロコントローラとパワーマネージメントと接続性ソリューションの供給に関する新たな複数年契約を発表しました。この追加生産能力は、2024~2030年にかけてのInfineonの事業成長確保に貢献するものと期待されています。この協業の中心は、次世代車載システムの厳しい安全セキュリティ要件を満たしながら、ミッションクリティカルな車載アプリケーションを実現するために設計された高信頼性の組み込み不揮発性メモリー技術ソリューションであると主張しています。

- 欧州では車載生産台数が増加しており、同市場の需要が拡大する可能性が高いです。例えば、国際車載工業会(OICA)によると、2023年にはドイツが欧州最大の車載生産国となり、約410万台が生産されました。

- 電気車載(EV)や自律走行システムに対する需要の高まりが、これらのアプリケーション特有の要件を満たすための特殊半導体の開発を後押ししています。例えば、Kraftfahrt-Bundesamt(連邦車載交通局-KBA)によると、ドイツで新たに登録される電気車載の数は近年大幅に増加しており、2022年の47万559台から2023年には52万4,219台に増加します。

- ドイツの車載メーカーは、車載のエネルギー効率を向上させようと絶えず努力しています。半導体技術は、より効率的な電力管理と制御システムを可能にし、その結果、エネルギー消費が減少し、全体的な効率が向上します。燃費と排ガスに関する規制が強化される中、エネルギー効率に優れたソリューションに貢献する車載半導体の需要は今後も増え続けると考えられます。

- 自律走行は交通の未来であり、半導体はこの技術革命の中心にあります。これらのコンポーネントは、自律走行車が周囲の環境を認識、解釈、対応できるようにする先進的センサ、カメラ、LiDAR、レーダー、AIプロセッサに電力を供給します。半導体は複雑な意思決定アルゴリズムを促進し、自律走行システムの安全性と信頼性を確保します。ドイツの半導体企業は、車両が周囲の状況を認識し、リアルタイムでインテリジェントな意思決定を行うことを可能にするセンサ、ビジョンシステム、AIチップの開発の最前線にいます。

欧州の車載半導体産業概要

欧州の車載半導体市場は、NXP Semiconductors NV、Infineon Technologies AG、STMicroelectronics NV、Texas Instruments Inc、Robert Bosch GMBH、Micron Technology Inc.などの著名な市場参入企業が存在する半固定市場です。市場参入企業は、消費者の進化する需要に応えるため、研究開発への大規模な投資、提携、合併によって新製品の革新に努めています。

- 2024年1月、Texas Instrumentsは、車載の安全性とインテリジェンスを高めるために設計された新しい半導体を発表しました。AWR2544 77GHzミリ波レーダーセンサチップは、衛星レーダー・アーキテクチャ向けに設計されており、ADASにおけるセンサフュージョンと意思決定を改善することで、より先進的自律性を実現します。

- 2023年8月、欧州最大級の半導体受託製造・設計企業であるSTMicroelectronicsNVと、米国の車載部品サプライヤーであるボルグワーナーは、SiC技術をボルグワーナーのVIPERパワーモジュールに統合することで提携しました。この統合は、Volvo・カーズの2030年までの完全な車両電化への移行を支援するためのものです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- COVID-19、後遺症、その他のマクロ経済動向の市場への影響

第5章 市場力学

- 市場の促進要因

- 車載生産台数の増加とEVSの普及

- 政府規制による先進安全・快適システムへの需要拡大

- 市場抑制要因

- 高機能化に伴うコスト増

第6章 市場セグメンテーション

- 車種

- 乗用車

- ディスクリート

- オプトエレクトロニクス

- センサとアクチュエータ

- ロジック

- メモリー

- アナログIC

- マイクロ

- 小型商用車

- ディスクリート

- オプトエレクトロニクス

- センサとアクチュエータ

- ロジック

- メモリー

- アナログIC

- マイクロ

- 大型商用車

- ディスクリート

- オプトエレクトロニクス

- センサとアクチュエータ

- ロジック

- メモリ

- アナログIC

- マイクロ

- 乗用車

- アプリケーション

- シャーシ

- パワーエレクトロニクス

- セーフティ

- ボディエレクトロニクス

- コンフォート/エンターテイメントユニット

- その他

- 国名

- 英国

- ドイツ

- フランス

- イタリア

第7章 競合情勢

- 企業プロファイル

- NXP Semiconductor NV

- Infineon Technologies AG

- Renesas Electronics Corporation

- STMicroelectronics NV

- Toshiba Electronic Devices & Storage Corporation(Toshiba Corporation)

- Texas Instrument Inc.

- Robert Bosch GmbH

- Micron Technology Inc.

- Onsemi(Semiconductor Components Industries LLC)

- Analog Devices Inc.

- ROHM Co. Ltd

第8章 投資分析

第9章 市場の将来

The Europe Automotive Semiconductor Market size is estimated at USD 15.46 billion in 2025, and is expected to reach USD 24.01 billion by 2030, at a CAGR of 9.2% during the forecast period (2025-2030).

Key Highlights

- An automotive semiconductor is a type of semiconductor chip specifically designed and used in the automotive industry. These chips play a crucial role in the functioning of various electronic components and systems in vehicles. They are responsible for powering and controlling many features and functions, including safety systems, infotainment systems, engine control units, sensors, etc.

- Automotive semiconductors have become increasingly important as vehicles have become more technologically advanced. They are essential for integrating advanced technologies such as autonomous driving, electric powertrains, and connected car systems. These semiconductors are designed to meet the specific requirements of the automotive industry, including durability, reliability, and the ability to operate in harsh environments.

- One of the primary applications of automotive semiconductors is in Advanced Driver Assistance Systems (ADAS). These systems use sensors, cameras, and processors to enhance vehicle safety and assist drivers in real-time. Semiconductors enable features like adaptive cruise control, lane-keeping assist, automatic emergency braking, blind-spot detection, and pedestrian detection, making driving safer and reducing the risk of accidents.

- Semiconductors play a crucial role in developing advanced infotainment systems in vehicles. These systems provide a seamless integration of entertainment, navigation, and communication features. Automotive semiconductors enable touchscreens, voice recognition, connectivity options, and multimedia playback, transforming the driving experience into a personalized and connected one.

- The increasing investments in the automotive semiconductor industry in Europe are likely to aid the development of the market studied. For instance, in August 2023, Robert Bosch GmbH, TSMC, NXP Semiconductors NV, and Infineon Technologies AG announced a plan to jointly invest in ESMC (European Semiconductor Manufacturing Company GmbH) in Dresden, Germany, to offer advanced semiconductor manufacturing services. ESMC is claimed to mark a substantial step toward constructing a 300 mm fab to support the future capacity requirements of the fast-growing automotive and industrial sectors.

- The project is designed under the framework of the European Chips Act. The planned fab is anticipated to have a monthly production capacity of 40,000 wafers (12-inch) on TSMC's 28/22 nanometer planar CMOS and 16/12 nanometer FinFET process technology, bolstering Europe's semiconductor manufacturing ecosystem with advanced FinFET transistor technology and creating approximately 2,000 direct high-tech professional jobs. ESMC seeks to begin construction of the fab in the second half of 2024, with production targeted to commence by the end of 2027.

- Semiconductors enable vehicle connectivity, forming the foundation for connected car technology. They power wireless communication systems, allowing vehicles to connect with other vehicles (V2V), infrastructure (V2I), and the internet (V2X). This connectivity facilitates real-time data exchange, enabling features like traffic updates, remote vehicle diagnostics, over-the-air updates, and even autonomous driving capabilities.

- With the increasing concern for environmental sustainability and the necessity to reduce carbon emissions, electric vehicles (EVs) have gained immense popularity in Europe. EVs rely heavily on semiconductor technology for power management, battery management, and motor control systems. As the demand for EVs continues to rise, so does the demand for automotive semiconductors.

- According to the European Automobile Manufacturers Association (ACEA), the sales volume of battery electric (BEV) and plug-in hybrid electric vehicles (PHEV) in Europe increased from 559.81 thousand in Q2 2022 to 757.83 thousand in Q3 2023. Such an increase in the demand for EVs would offer lucrative opportunities for the growth of the studied market.

- However, the high cost of development and production is a significant barrier to the growth of the market studied. The complex manufacturing processes and testing requirements make these semiconductors expensive, limiting their affordability for both manufacturers and consumers.

- Furthermore, the conflict between Russia and Ukraine is expected to significantly impact the semiconductor industry. The conflict has already exacerbated the electronics & semiconductor supply chain issues and the chip shortage that have affected the industry for some time. The disruption may result in volatile pricing for critical raw materials such as nickel, palladium, copper, titanium, and aluminum, resulting in material shortages. This, in turn, could impact the manufacturing of automotive semiconductors.

Europe Automotive Semiconductor Market Trends

The Passenger Vehicles Segment is Expected to Drive the Market's Growth

- Automotive semiconductors find applications in various safety systems within passenger vehicles. These semiconductors are used in power electronics modules that control the anti-lock braking system (ABS), electronic stability control (ESC), and advanced driver-assistance systems (ADAS). By accurately monitoring and adjusting power flow, these systems enhance vehicle stability, traction, and overall safety.

- Moreover, automotive semiconductors play a crucial role in power management within passenger vehicles. These semiconductors are used in DC-DC converters, voltage regulators, and other power control modules, ensuring efficient power distribution and optimal utilization of electrical energy.

- These tiny electronic components are integrated into different systems within the vehicle, enabling advanced safety features and ensuring a safer driving experience. One of the primary applications of automotive semiconductors in passenger vehicle safety is the anti-lock braking system (ABS). ABS relies on sensors and microcontrollers to monitor wheel speed and prevent wheel lock-up during sudden braking. By rapidly modulating brake pressure, automotive semiconductors help maintain vehicle stability, prevent skidding, and reduce the risk of accidents.

- They are also employed in electronic stability control (ESC) systems. ESC uses sensors, accelerometers, and microcontrollers to monitor vehicle dynamics and apply selective braking to individual wheels. Automotive semiconductors enable real-time data processing and precise control, enhancing vehicle stability and preventing loss of control in hazardous situations.

- The increasing automotive production in Europe is likely to increase the demand for automotive semiconductors. For instance, according to OICA, around 1.5 million motor vehicles were produced in France in 2023, 68.2% of which were passenger cars. In 2022, approximately 1.3 million cars were produced in France.

- Furthermore, the proliferation of connected car technologies has transformed the way users interact with vehicles. From infotainment systems to advanced driver assistance systems (ADAS), connected car technologies rely on semiconductor chips to enable seamless communication and data processing. With the increasing integration of internet connectivity, cloud services, and data analytics in vehicles, the demand for automotive semiconductors is expected to grow exponentially.

Germany is Expected to Witness High Market Growth Rate

- Germany, known for its strong automotive industry, has established itself as one of the leading players in the global automotive semiconductor market. With a robust ecosystem of automotive manufacturers, suppliers, and technology companies, Germany has become a hub for semiconductor development and production. Semiconductor companies like Infineon Technologies, Bosch, and Continental AG have a significant presence in Germany. These companies specialize in producing a diverse range of automotive semiconductors, including microcontrollers, sensors, power management ICs, and connectivity solutions.

- German semiconductor companies often collaborate with automotive manufacturers, research institutions, and start-ups to foster innovation, drive technological advancements, and enhance their market capitalization.

- For instance, in January 2024, Infineon Technologies AG and GlobalFoundries announced a new multi-year agreement on the supply of Infineon's AURIX TC3x 40 nanometer automotive microcontrollers and power management and connectivity solutions. The additional capacity is anticipated to contribute to secure Infineon's business growth from 2024 through 2030. At the center of this collaboration is claimed to be a highly reliable embedded non-volatile memory technology solution that is designed to enable mission-critical automotive applications while satisfying the stringent safety and security requirements for next-generation vehicle systems.

- The increasing automobile production in Europe is likely to augment the demand for the market studied. For instance, according to the International Organization of Motor Vehicle Manufacturers (OICA), in 2023, Germany was the largest automobile manufacturing country in Europe, with approximately 4.1 million vehicles produced.

- The increasing demand for electric vehicles (EVs) and autonomous driving systems has driven the development of specialized semiconductors to meet the unique requirements of these applications. For instance, according to the Kraftfahrt-Bundesamt (Federal Motor Transport Authority - KBA), the number of new electric cars registered in Germany has grown significantly in recent years, increasing from 470,559 in 2022 to 524,219 in 2023.

- Automotive manufacturers in Germany are constantly striving to improve the energy efficiency of vehicles. Semiconductor technology enables more efficient power management and control systems, resulting in decreased energy consumption and increased overall efficiency. With stricter regulations on fuel economy and emissions, the demand for automotive semiconductors that contribute to energy-efficient solutions will continue to rise.

- Autonomous driving is the future of transportation, and semiconductors are at the heart of this technological revolution. These components power the advanced sensors, cameras, LiDAR, radar, and AI processors that enable autonomous vehicles to perceive, interpret, and respond to their surroundings. Semiconductors facilitate complex decision-making algorithms, ensuring the safety and reliability of autonomous driving systems. German semiconductor companies are at the forefront of developing sensors, vision systems, and AI chips that enable vehicles to perceive their surroundings and make intelligent decisions in real time.

Europe Automotive Semiconductor Industry Overview

The European automotive semiconductor market is a semiconsolidated market with the presence of several prominent market players like NXP Semiconductors NV, Infineon Technologies AG, STMicroelectronics NV, Texas Instruments Inc., Robert Bosch GMBH, Micron Technology Inc., etc. The market players are striving to innovate new products by way of extensive investments in R&D, collaborations, and mergers to cater to the evolving demands of consumers.

- January 2024: Texas Instruments introduced new semiconductors designed to enhance automotive safety and intelligence. The AWR2544 77 GHz millimeter-wave radar sensor chip is designed for satellite radar architectures, enabling higher levels of autonomy by improving sensor fusion and decision-making in ADAS.

- August 2023: STMicroelectronics NV, one of the largest European semiconductor contract manufacturing and design companies, and BorgWarner, an American automotive supplier, joined forces to integrate SiC technology into BorgWarner's VIPER power modules. This integration strives to support Volvo Cars' transition to full vehicle electrification by 2030.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19, Aftereffects, and Other Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Vehicle Production and Adoption of EVS

- 5.1.2 Growing Demand For Advanced Safety and Comfort Systems Augmented by Government Regulations

- 5.2 Market Restraint

- 5.2.1 Increasing Costs Associated With Growing Advance Features

6 MARKET SEGMENTATION

- 6.1 Vehicle Type

- 6.1.1 Passenger Vehicle

- 6.1.1.1 Discrete

- 6.1.1.2 Optoelectronics

- 6.1.1.3 Sensors and Actuators

- 6.1.1.4 Logic

- 6.1.1.5 Memory

- 6.1.1.6 Analog IC

- 6.1.1.7 Micro

- 6.1.2 Light Commercial Vehicle

- 6.1.2.1 Discrete

- 6.1.2.2 Optoelectronics

- 6.1.2.3 Sensors and Actuators

- 6.1.2.4 Logic

- 6.1.2.5 Memory

- 6.1.2.6 Analog IC

- 6.1.2.7 Micro

- 6.1.3 Heavy Commercial Vehicle

- 6.1.3.1 Discrete

- 6.1.3.2 Optoelectronics

- 6.1.3.3 Sensors and Actuators

- 6.1.3.4 Logic

- 6.1.3.5 Memory

- 6.1.3.6 Analog IC

- 6.1.3.7 Micro

- 6.1.1 Passenger Vehicle

- 6.2 Application

- 6.2.1 Chassis

- 6.2.2 Power Electronics

- 6.2.3 Safety

- 6.2.4 Body Electronics

- 6.2.5 Comfort/Entertainment Unit

- 6.2.6 Other Applications

- 6.3 Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 NXP Semiconductor NV

- 7.1.2 Infineon Technologies AG

- 7.1.3 Renesas Electronics Corporation

- 7.1.4 STMicroelectronics NV

- 7.1.5 Toshiba Electronic Devices & Storage Corporation (Toshiba Corporation)

- 7.1.6 Texas Instrument Inc.

- 7.1.7 Robert Bosch GmbH

- 7.1.8 Micron Technology Inc.

- 7.1.9 Onsemi (Semiconductor Components Industries LLC)

- 7.1.10 Analog Devices Inc.

- 7.1.11 ROHM Co. Ltd