|

市場調査レポート

商品コード

1683979

アジア太平洋の除草剤:市場シェア分析、産業動向、成長予測(2025年~2030年)Asia Pacific Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の除草剤:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 217 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

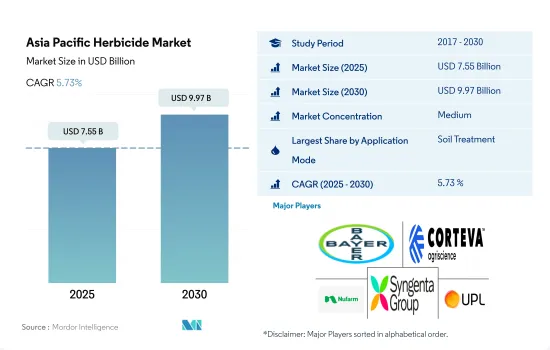

アジア太平洋の除草剤市場規模は2025年に75億5,000万米ドルと推定され、2030年には99億7,000万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは5.73%で成長すると予測されます。

雑草の蔓延とそれに伴う農作物の収量減少が市場を牽引

- アジア太平洋には、米、小麦、トウモロコシ、大豆などの主食作物や、綿花、サトウキビ、果物、野菜などの換金作物など、多様な作物が栽培されており、これらの作物は複数の雑草種による課題に直面しています。2022年には、土壌治療法がアジア太平洋の除草剤市場で最大のシェア46.8%を占め、その市場規模は30億米ドルに達しました。土壌治療は、除草剤を土壌に直接散布するもので、雑草防除の効果的な手段として機能します。この方法は、土壌に存在する雑草の種子、苗、または定着した雑草を対象として、作物の植え付け前または出穂後に利用することができます。

- 2022年には、除草剤の葉面散布は32.6%の市場シェアを占め、21億米ドルと評価されました。この方法は、広葉雑草、スゲ、イネ科植物、さらには水生雑草を標的にするのに非常に効果的です。これらの雑草の葉に除草剤を直接散布することで、最大限の吸収と防除を達成することができます。葉面散布の柔軟性により、農家は雑草が活発に生育している段階を狙い、最適な結果を得ることができます。

- 2022年には、化学的散布は除草剤散布方法の18.9%を占め、12億米ドルと評価されました。この成長は、マイクロ灌漑システムの採用が増加していることと、除草剤の散布が容易で、農地全体に均一に行き渡ることが要因です。

- 燻蒸は、特に他の方法では効果が低い閉鎖環境において、効果的で的を絞った雑草防除を行うことができます。他の方法では防除が困難な雑草の種子、根系、繁殖体にも到達することができます。

- 各手法の利点と特異性により、各手法の市場は予測期間中に成長すると予想されます。

稲のような主要作物への除草剤の使用が地域全体で拡大

- アジア太平洋の除草剤市場は、過去一定期間に着実な成長を遂げ、2022年には同地域が世界の除草剤市場で大きなシェアを占める。ブタクロール、プロパニル、プレチラクロール、2,4-D、ビスピリバック・ナトリウム、シハロホップ・ブチルなどが、この地域で一般的に使用されている除草剤です。

- アジアではコメが最も重要な作物であり、世界のコメ生産と消費の90%を占めています。アジア太平洋は米のような主食用穀物の最大の輸出国・生産国であるため、除草剤は主に穀物・穀類に使用されます。穀物・穀類セグメントは2022年に金額ベースで56.6%のシェアを占めました。

- この地域の多くの国々は、収量の損失を最小限に抑えるために、利用可能なすべての互換性のある防除戦術の使用を伴う統合雑草管理法を採用しています。新たに導入された雑草は、他の地域に広がる前に直ちに駆除する必要があるが、除草剤を使用することで防除できます。フィリピンのヌエバエシハ州とイロイロ州では、文化的管理と除草剤の適切な使用を組み合わせることで、収量がそれぞれ約10%から15%増加しました。

- しかし、雑草集団に除草剤耐性が発生すると、効果的な雑草管理のための除草剤の選択肢が制限されるため、大きな課題となっています。同時に、日本のような様々な国の政府は、新しい雑草とそれに対応する除草剤を発見するための研究イニシアチブに投資しています。このような政策は、農家が作物保護慣行を採用することを奨励しており、このセグメントの成長に貢献することを目指しています。このセグメントは予測期間(2023年~2029年)にCAGR 6.1%を記録すると予想されます。

アジア太平洋の除草剤市場の動向

稲のような主要作物で雑草の蔓延が増加し、効率的な雑草防除が必要となり、1ヘクタール当たりの除草剤消費量が増加

- アジア太平洋では、1ヘクタール当たりの除草剤使用量が過去の期間に比べ大幅に増加しています。これは農業における雑草の蔓延によるもので、雑草はさまざまな病気の媒介者として働き、その結果、この地域では真菌感染症が増加し、作物の損失が増加しています。日本は、歴史的期間に1ヘクタール当たりの除草剤消費量が大幅に増加し、その他アジア太平洋よりも約7%高いと推定されました。同国における1ヘクタール当たりの除草剤使用量の増加は、農家の高齢化、労働力不足、農地の増加など、さまざまな要因が重なったことに起因しています。その結果、コメや大豆などの主要作物の雑草管理は、手作業による除草から除草剤の使用へと移行しました。

- ミャンマーの1ヘクタール当たりの除草剤消費量は地域第2位で、2022年には1ヘクタール当たり2,200グラムが消費され、2017年の1,600グラムより増加しました。この増加は、雑草を防除し、コメなどの主要作物の農業生産を向上させるための適切な雑草管理技術の導入によるところが大きいです。雑草による稲作の平均収量損失は、乾期で約65%、雨期で約34%です。同国の農家は主要作物の雑草防除に除草剤製品に大きく依存しているため、1ヘクタール当たりの除草剤消費量が増加しています。

- アジア太平洋全体では、主要作物で雑草の発生が増加したため、中国を除くすべての国で1ヘクタール当たりの除草剤使用量が前年同期比で増加しました。しかし、中国は農薬のゼロ成長政策を実施しているため、他の雑草防除方法を使用しています。

気候変動が作物植物にストレスを与えるため、雑草の生育が増加し、市場を牽引しています。

- メトリブジンは、光合成を阻害することによってトウモロコシ、サトウキビ、ジャガイモ、トマトなどの主要作物の広葉雑草を防除するために使用される選択的浸透性除草剤です。2022年の価格は1トン当たり1万6,600米ドルでした。

- アトラジンは、トウモロコシや稲作におけるエキノクロア、エルシン属、アマランサスビリジスなどの広葉雑草やイネ科雑草の防除に広く使用される除草剤です。この除草剤は2022年に1万3,800米ドルで評価されました。

- パラコートはグラモキソンの有効成分で、雑草や草の防除に使用されます。また、収穫前の綿花などの作物の乾燥にも使用されます。パラコートは2022年に1トン当たり4,600米ドルと評価されました。中国はパラコート輸出大国で、パラコート生産量の80%以上が世界各国に輸出されています。

- ペンディメタリンは、2022年に1トン当たり3,300米ドルで評価される選択的出芽前除草剤です。ジャガイモ、タバコ、ソルガム、コメ、サトウキビ作物の一年生草や広葉雑草を幅広く防除します。同様に、2,4-ジクロロフェノキシ酢酸(2,4-D)は一般的な浸透性除草剤で、2022年の価格はトン当たり2,300米ドルと評価されました。芝、芝生、畑、果実、野菜作物の広葉雑草の防除に使用されます。

- グリホサートは、有機リン系広域スペクトラム浸透性除草剤および作物乾燥剤であり、2022年の価格は1トン当たり1,100米ドルです。グリホサートは主に、イネ科、スゲ科、広葉樹などの雑草を防除するために使用されます。

- 気候変動は植物にダメージやストレスを与え、極端なストレス条件下では生存できないため植物の健康に悪影響を及ぼし、雑草の生育を増加させる。これはさらに除草剤需要の増加につながり、有効成分の価格を押し上げます。

アジア太平洋の除草剤産業の概要

アジア太平洋の除草剤市場は適度に統合されており、上位5社で50.02%を占めています。この市場の主要企業は以下の通りです。 Bayer AG, Corteva Agriscience, Nufarm Ltd, Syngenta Group and UPL Limited.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 薬剤散布

- 葉面散布

- 燻蒸

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001681

The Asia Pacific Herbicide Market size is estimated at 7.55 billion USD in 2025, and is expected to reach 9.97 billion USD by 2030, growing at a CAGR of 5.73% during the forecast period (2025-2030).

The market is being driven by increasing weed infestation and associated yield losses in crops

- The Asia-Pacific region is home to a diverse range of crops, encompassing staple food crops like rice, wheat, corn, and soybeans, as well as cash crops such as cotton, sugarcane, fruits, and vegetables, which face challenges from several weed species. In 2022, the soil treatment method accounted for the largest share of 46.8% in the Asia-Pacific herbicide market, representing a value of USD 3.0 billion. Soil treatment involves the direct application of herbicides to the soil, serving as an effective means of weed control. This method can be utilized either before planting or after crop emergence, targeting weed seeds, seedlings, or established weeds present in the soil.

- In 2022, foliar application of herbicides held a market share of 32.6% and was valued at USD 2.1 billion. This method is highly effective in targeting broadleaf weeds, sedges, grasses, and even aquatic weeds. By directly applying herbicides to the foliage of these weeds, maximum absorption and control can be achieved. The flexibility of foliar application allows farmers to target weeds during their active growth stages for optimal results.

- In 2022, chemigation accounted for 18.9% of herbicide application methods, valued at USD 1.2 billion. This growth is attributed to the increasing adoption of micro-irrigation systems and the ease of herbicide application, ensuring uniform distribution throughout the cropland.

- Fumigation can provide effective and targeted weed control, especially in enclosed environments where other methods may be less effective. It can reach weed seeds, root systems, and weed propagules that are difficult to control through other means.

- Owing to the advantages and specificity of each method, the market for each method is anticipated to grow during the forecast period.

The use of herbicides for major crops like rice is growing across the region

- The herbicide market in Asia-Pacific witnessed steady growth during the historical period, with the region occupying a significant share of the global herbicide market in 2022. Butachlor, propanil, pretilachlor, 2,4-D, bispyribac-sodium, and cyhalofop-butyl are the commonly used herbicides in the region.

- Rice is by far the most important crop in Asia; the region accounts for 90% of the world's production and consumption of rice. Herbicides are mostly used for grains and cereals in the Asia-Pacific as the region is the largest exporter and producer of staple grains such as rice. The grains & cereals segment occupied a share of 56.6% by value in 2022.

- Many countries in the region have adopted the Integrated weed Management method that entails the use of all available compatible control tactics to minimize yield losses. Newly introduced weeds that would require immediate eradication before they spread to other areas can be controlled with the use of herbicides. It was observed that combining cultural management practices and judicious herbicide usage resulted in higher yields of about 10% to 15% in the Nueva Ecija and Iloilo provinces of the Philippines, respectively.

- However, the occurrence of herbicide resistance in weed populations presents a big challenge as it limits herbicide choices for effective weed management. At the same time, governments of various countries like Japan are investing in research initiatives to discover new weeds and their subsequent herbicides. Such policies are encouraging farmers to adopt crop protection practices that aim to contribute to the growth of the segment. The segment is expected to record a CAGR of 6.1% during the forecast period (2023-2029).

Asia Pacific Herbicide Market Trends

Increased weed infestations in major crops like rice need efficient weed control, boosting the per hectare herbicide consumption

- In the Asia-Pacific region, the use of herbicides per hectare significantly increased over the historical period. This is due to the prevalence of weeds in agriculture, which are acting as vectors for a variety of diseases, resulting in an increase in fungal infections and crop loss in the region. Japan experienced a significant rise in herbicide consumption per hectare over the historical period, which was estimated to be approximately 7% higher than the rest of the Asia-Pacific region. The increasing use of herbicides per hectare in the country is attributed to a combination of factors, including the aging of farmers, a lack of labor, and an increase in agricultural land. This resulted in a shift from manual weeding to the use of herbicides for weed management in major crops such as rice and soybeans.

- Myanmar ranks second in the region in terms of herbicide consumption per hectare, with 2,200 grams of herbicide per hectare consumed in 2022, an increase over the 1,600 grams consumed in 2017. This increase is largely attributed to the implementation of appropriate weed management techniques to control weeds and enhance agricultural production in key crops such as rice. The average yield losses in rice crops due to weeds are approximately 65% and 34% in the dry and wet seasons, respectively. Farmers in the country are majorly reliant on herbicide products to control weeds in major crops, which has led to increased consumption of herbicides per hectare.

- Overall, in the Asia-Pacific region, herbicide use per hectare increased Y-o-Y in all countries except China, as weed infestations increased in the major crops. However, China is using other weed control methods as it implements zero growth policies in pesticides.

Climate change causing stress to crop plants, thus leading to increased weed growth driving the market

- Metribuzin is a selective and systemic herbicide used to control broadleaf weeds in major crops like corn, sugarcane, potatoes, and tomatoes by inhibiting photosynthesis. In 2022, it was priced at USD 16.6 thousand per metric ton.

- Atrazine is an herbicide widely used for the control of broadleaf and grassy weeds like Echinocloa, Elusine spp., and Amaranthus viridis in maize and rice crops. The herbicide was valued at a price of USD 13.8 thousand in 2022.

- Paraquat is the active ingredient in Gramoxone, which is used to control weeds and grasses. It is also used for the desiccation of crops, like cotton, prior to harvest. Paraquat was valued at a price of USD 4.6 thousand per metric ton in 2022. China is a major paraquat export country, and over 80% of its paraquat output is exported to countries worldwide.

- Pendimethalin is a selective pre-emergence herbicide valued at USD 3.3 thousand per metric ton in 2022. It offers broad-spectrum control of annual grasses and broadleaf weeds in potato, tobacco, sorghum, rice, and sugarcane crops. Similarly, 2,4-dichlorophenoxyacetic acid (2,4-D) is a common systemic herbicide that was valued at a price of USD 2.3 thousand per metric ton in 2022. It is used in the control of broadleaf weeds in turf, lawn, field, fruit, and vegetable crops.

- Glyphosate is an organophosphorus broad-spectrum systemic herbicide and crop desiccant, priced at USD 1.1 thousand per metric ton in 2022. Glyphosate is mainly used to control weeds like grasses, sedges, and broadleaves.

- Climate change can cause damage and stress to plants and be detrimental to plant health as they cannot survive in extreme stress conditions, leading to increased weed growth. This further leads to an increase in herbicide demand, thereby boosting the prices of active ingredients.

Asia Pacific Herbicide Industry Overview

The Asia Pacific Herbicide Market is moderately consolidated, with the top five companies occupying 50.02%. The major players in this market are Bayer AG, Corteva Agriscience, Nufarm Ltd, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Myanmar

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Rainbow Agro

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms