欧州の金属製キャップ・クロージャー:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

Europe Metal Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549953

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

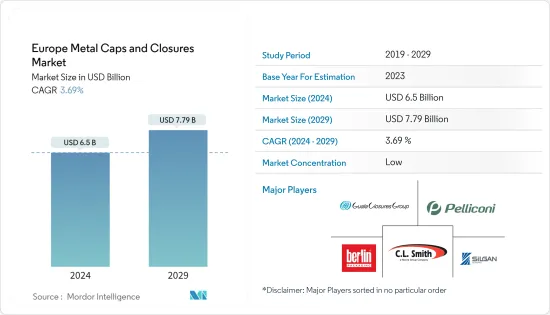

欧州の金属製キャップ・クロージャーの市場規模は、2024年に65億米ドルと推定され、2029年には77億9,000万米ドルに達すると予測され、予測期間中(2024年~2029年)のCAGRは3.69%で成長する見込みです。

主なハイライト

- 金属製クロージャーは、主に金属製包装の高いリサイクル性により、プラスチック製クロージャーよりも支持を集めています。金属製包装の主要材料であるアルミニウムとスチールは、キャップ・クロージャーの最重要選択肢として際立っており、確立されたリサイクルシステムの恩恵を受けています。

- 金属製キャップは賞味期限を延ばし、味、風味、食感を保持します。漏れにくく、汚染に強いという特性は、視覚的なアピールを高め、ブランドの差別化と消費者の利便性を助けます。飲食品、医薬品などの分野で広く利用されている金属製クロージャーは、包装ソリューションの要となっています。

- 欧州は、ジャム、ゼリー、ピューレ、マーマレードといった食品の世界市場を独占しており、世界輸入量の約50%を占めています。さらに、この地域のジャムやピクルスを含むパック詰め食品への嗜好が、金属製クロージャー市場の成長を後押ししています。

- さらに、金属製クロージャーは製薬業界で広く使用されており、その強固なバリア性と断熱性が珍重されています。これらのクロージャーはしっかりと密封され、開封が容易で効果的な再密封が可能です。OTC医薬品、特にシロップボトルの人気が高まるにつれ、この地域では金属製クロージャーの需要が増加しています。EFPIA 2023報告書によると、2022年の欧州の医薬品生産額は3,400億ユーロ(約3,583億米ドル)と推定され、同地域の輸出額は約6,700億ユーロ(約7,060億米ドル)に達します。

- 欧州の1次アルミニウム産業は、需要の高まり、天然ガスコストの高騰、再生可能エネルギー(風力、太陽光、水力)や原子力エネルギー源の不足といった要因が重なり、エネルギー価格の高騰に悩まされています。

- こうした課題をさらに深刻にしているのが、ウクライナの紛争で、特に天然ガスのサプライチェーンが大きく寸断され、エネルギー危機を悪化させています。その結果、アルミニウムのようなエネルギー多消費型部門は、欧州での操業を停止または休止しています。欧州の主要なアルミニウム製錬所がエネルギー費の高騰に対応して生産を縮小しているため、この地域の金属製キャップ・クロージャー市場は、迫り来る景気後退に直面しています。

欧州の金属製キャップ・クロージャー市場の動向

飲料産業が金属製キャップ・クロージャーを大幅に採用する見込み

- 飲料産業が金属製キャップ市場を大きく牽引しています。クラウンキャップ、アルミスクリューキャップ、ツイスト/ラグクロージャーを含む金属製キャップは飲料包装において極めて重要です。これらのキャップは、炭酸清涼飲料やエネルギー飲料からアルコール飲料まで、さまざまな飲料に応用されています。

- 欧州では、アルコール飲料とノンアルコール飲料の両方が広く消費されているため、飲料用キャップ・クロージャーの需要が増加しています。Brewers of Europe 2023報告書によると、2022年の欧州のビール生産量は4億194万5,000ヘクトリットルという驚異的な数字で、この地域の飲料産業が堅調であることを裏付けています。このような飲料生産の急増は、欧州市場における金属製キャップ・クロージャーの必要性を直接煽っています。

- 金属製キャップ・クロージャーは、ワインの品質と鮮度を維持する能力が高く評価され、ワインボトルの包装で人気を集めています。現代的な選択肢であるアルミスクリュークロージャーは、ワインの独特の味と香りを守るのに優れています。酸化を防ぐことで、ワインの熟成に理想的な環境を作り出し、永続的な品質を保証します。

- 欧州の拡大は、世界的な包装メーカーにとって重要な戦略であり、急成長する同地域の市場に参入するために、M&Aを行う企業が増えています。例えば、ワインとオリーブオイル業界向けにガラスと金属の包装を提供する家族経営のPanvetriは、大手ハイブリッド包装サプライヤーであるBerlin Packagingに買収されました。パンヴェトリは、ビール、スピリッツ、スパークリングワインのボトル、オリーブオイルの缶、食品の瓶、クロージャーも提供しています。Berlin Packagingの広範なローカルプレゼンスと経験豊富な販売チームは、Panvetriの製品ラインナップを拡大する上でサポートすることができます。

英国が市場で大きなシェアを占める見込み

- 英国は、Guala Closures SpA、Pelliconi &Co.SpA、Silgan Closuresなどが牽引しています。金属製キャップ・クロージャーは、リサイクル性、耐久性、漏れ防止・汚染防止シールが優れていることから、飲料分野で主に好まれています。特に、ビールは飲料業界で金属製クロージャーを採用するトップランナーとして浮上しています。

- さらに、英国ではアルコール飲料とノンアルコール飲料の消費量の増加が顕著で、金属製キャップ・クロージャーの市場を直接強化しています。英国国家統計局のデータによると、近年、飲食品やノンアルコール飲料に対する消費支出が大幅に増加しています。

- リサイクルと持続可能性への関心も、英国の金属製キャップ・クロージャー市場の成長を後押ししています。金属の持続可能性は主にリサイクルによって推進され、原材料を作るのに必要な原材料とエネルギーを最大95%節約できます。

- 2023年、英国はアルミニウム包装のリサイクル率が68%に達したという注目すべきマイルストーンを達成しました。年間を通じて、英国は16万2,357トンのアルミ包装材をリサイクルし、特に飲料缶のリサイクル率は81%という驚異的な数字を記録しました。さらに、この年次データは、アルミニウム包装に対する英国の国内需要の大幅な増加を強調しています。

- さらに、アルコール部門の多くの企業が飲料を導入し、成長市場を掴んでいます。例えば、Lockdown Liquor & Co.は、Easy Liquorという新シリーズでプレミアム缶カクテルを発売しました。ラインナップはマルガリータ、ラムパンチ、ジンジャーコスモ、エスプレッソマティーニなどです。新しい缶飲料の導入の増加は、金属製キャップ・クロージャーの需要を生み出しています。

欧州の金属製キャップ・クロージャー産業の概要

欧州の金属製キャップ・クロージャー市場は、複数の国内メーカーとグローバルメーカーの存在により競争が激しくなっています。この市場の主要企業には、Guala Closures SpA、Berlin Packaging、Pelliconi &C. SpA、C.L. Smith Co.(Novvia Group)、Silgan Closures(Silgan Holdings Inc.)などがあります。市場では製品の差別化、ポートフォリオ、価格に関して激しい競争が繰り広げられています。付加価値の高いクロージャーと不正開封防止の需要の高まりは、様々なセグメントでの金属製キャップ・クロージャーの使用を増加させると思われます。

- 2023年6月欧州のアルミニウムサプライヤーであるAludiumは、ワイン・蒸留酒用クロージャーのメーカーであるAmcor Capsulesと提携し、スクリューキャップ用の低カーボンフットプリントのアルミニウム製品を開発しました。この製品は、独自に認証・検証され、欧州で販売・使用されている平均的な1次アルミニウム材料よりも、カーボンフットプリントが最低50%低くなると予測されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度:ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 化粧品・パーソナルケア産業の成長

- 他のクロージャー材料に比べ優れた特性

- 市場抑制要因

- 代替キャップ・クロージャーソリューションとの競合

- 高い初期投資と製造上の制約

第6章 市場セグメンテーション

- 材料タイプ別

- アルミニウム

- スチール

- クロージャータイプ別

- クラウンキャップ

- スクリューキャップ

- ツイスト金属製キャップ

- その他のキャップ

- エンドユーザー産業別

- 食品

- 飲料

- アルコール

- ノンアルコール

- 医薬品

- パーソナルケア

- その他エンドユーザー産業

- 国別

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

第7章 競合情勢

- 企業プロファイル

- O.Berk Company

- Guala Closures SpA

- Pelliconi & C. SpA

- C.L. Smith Co.(Novvia Group)

- Technocap SpA

- Can-Pack SA

- Amcor PLC

- P. Wilkinson Containers Ltd

- Silgan Closures(Silgan Holdings Inc.)

- ACTEGA(ALTANAのメンバー)

- Berlin Packaging

第8章 投資分析

第9章 市場の将来

第10章 出版社について

目次

The Europe Metal Caps And Closures Market size is estimated at USD 6.5 billion in 2024, and is expected to reach USD 7.79 billion by 2029, growing at a CAGR of 3.69% during the forecast period (2024-2029).

Key Highlights

- Metal closures are gaining traction over their plastic counterparts, primarily due to the higher recyclability of metal packaging. Aluminum and steel, the primary materials in metal packaging, stand out as top choices for caps and closures, benefiting from well-established recycling systems.

- Metal closures extend shelf-life and preserve taste, flavor, and texture, which are pivotal in packaging. Their leak-proof and contamination-resistant nature enhances visual appeal and aids in brand distinction and consumer convenience. Widely utilized in sectors spanning food, beverages, and pharmaceuticals, metal closures stand as a cornerstone of packaging solutions.

- Europe dominates the global market for food items like jams, jellies, purees, and marmalades, accounting for approximately 50% of the global imports. Additionally, the region's penchant for packed food, including jams and pickles, fuels the growth of the metal closures market.

- Furthermore, metal closures are widely used in the pharmaceutical industry and are prized for their robust barrier and insulating properties. These closures seal securely and allow for easy opening and effective resealing. With the increasing popularity of OTC drugs, particularly in syrup bottles, the demand for metal closures is on the rise in the region. As per the EFPIA 2023 report, Europe's pharmaceutical production value in 2022 was estimated at EUR 340 billion (approximately USD 358.3 billion), with the region's export value pegged at around EUR 670 billion (approximately USD 706 billion).

- The European primary aluminum industry is reeling from surging energy prices, driven by a confluence of factors: heightened demand, steep natural gas costs, and a dearth of affordable renewable (wind, solar, and hydro) or nuclear energy sources.

- Compounding these challenges, the conflict in Ukraine has severely disrupted supply chains, especially for natural gas, exacerbating the energy crisis. Consequently, energy-intensive sectors, such as aluminum, are either shuttering or halting operations in Europe. As leading aluminum smelters in Europe scale back production in response to escalating energy expenses, the regional market for metal caps and closures faces a looming downturn.

Europe Metal Caps and Closures Market Trends

The Beverage Industry is Expected to Adopt Metal Closures Significantly

- The beverage industry significantly drives the metal closures market. Metal closures, including crown caps, aluminum screw caps, and twist/lug closures, are pivotal in beverage packaging. These closures find applications in a range of beverages, from carbonated soft drinks and energy drinks to alcoholic beverages.

- In Europe, the demand for beverage caps and closures is on the rise, propelled by the continent's extensive consumption of both alcoholic and non-alcoholic beverages. According to the Brewers of Europe 2023 report, in 2022, Europe produced a staggering 401,945 thousand hectoliters of beer, underscoring the region's robust beverage industry. This surge in beverage production is directly fueling the need for metal closures in the European market.

- Metal caps and closures are gaining traction in wine bottle packaging, lauded for their prowess in maintaining wine quality and freshness. Aluminum screw closures, a contemporary choice, excel in safeguarding the distinct taste and aroma of wines. By staving off oxidation, these closures create an ideal environment for wine maturation, guaranteeing its enduring quality.

- European expansion is a key strategy for global packaging manufacturers, who are increasingly turning to mergers and acquisitions to tap into the region's burgeoning market. For instance, Panvetri, a family-owned business that offers glass and metal packaging for the wine and olive oil industries, was acquired by Berlin Packaging, a leading hybrid packaging supplier. Panvetri also provides beer, spirits, and sparkling wine bottles, olive oil cans, food jars, and closures. Berlin Packaging's extensive local presence and experienced sales team can support Panvetri in broadening its range of products.

The United Kingdom is Expected to Hold a Significant Share in the Market

- The United Kingdom is poised to claim a substantial share in the metal caps and closures market, driven by key players like Guala Closures SpA, Pelliconi & Co. SpA, and Silgan Closures. Metal closures are predominantly favored in the beverage sector, prized for their recyclability, durability, and adeptness at providing leak-proof and contamination-resistant seals. Notably, beer emerges as the frontrunner for embracing metal closures in the beverage industry.

- Furthermore, the rising consumption of both alcoholic and non-alcoholic beverages in the United Kingdom has notably surged, directly bolstering the market for metal caps and closures. Data from the Office for National Statistics in the United Kingdom highlights a substantial uptick in consumer spending on food and non-alcoholic beverages in recent years.

- Recycling and sustainability concerns are also driving the growth of the UK metal caps and closures market. Metal sustainability is primarily driven by recycling, saving up to 95% of the raw material and energy needed to make raw materials.

- In 2023, the United Kingdom achieved a notable milestone, with its aluminum packaging recycling rate hitting 68%, as reported by the Environment Agency through the National Packaging Waste Database. Throughout the year, the nation recycled 162,357 tonnes of aluminum packaging, notably led by beverage cans, with an impressive 81% recycling rate. Furthermore, the annual data highlights a significant uptick in the UK's domestic demand for aluminum packaging.

- Furthermore, many companies in the alcohol sector are introducing drinks and seizing the growing market. For instance, Lockdown Liquor & Co. introduced its premium canned cocktails with a new range called Easy Liquor. The line-up includes a Margarita, a Rum Punch, a Ginger Cosmo, and an Espresso Martini. The growing introduction of new canned beverages creates demand for metal caps and closures.

Europe Metal Caps and Closures Industry Overview

The European metal caps and closures market is highly competitive due to the presence of several domestic and global manufacturers. Some of the key players in this market are Guala Closures SpA, Berlin Packaging, Pelliconi & C. SpA, C.L. Smith Co. (Novvia Group), and Silgan Closures (Silgan Holdings Inc.). Intense competition prevails in the market regarding product differentiation, portfolio, and pricing. The rising demand for value-added closures and tamper resistance properties will augment the usage of metal caps and closures in various segments.

- June 2023: Aludium, a European supplier of aluminum, collaborated with Amcor Capsules, a manufacturer of wine and spirits closures, to create an aluminum product with a low carbon footprint for screw caps. This product has been certified and verified independently and is predicted to have a minimum of 50% less carbon footprint than the average primary aluminum materials sold and used in Europe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Cosmetics and Personal Care Industry

- 5.1.2 Superior Properties Compared to Other Closure Materials

- 5.2 Market Restraints

- 5.2.1 Competition from Alternative Caps and Closures Solution

- 5.2.2 High Initial Setup Cost and Manufacturing Constraints

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By Closures Type

- 6.2.1 Crown Caps

- 6.2.2 Screw Caps

- 6.2.3 Twist Metal Caps

- 6.2.4 Other Closure Type

- 6.3 By End-user Industry

- 6.3.1 Food

- 6.3.2 Beverages

- 6.3.2.1 Alcoholic

- 6.3.2.2 Non-alcoholic

- 6.3.3 Pharmaceuticals

- 6.3.4 Personal Care

- 6.3.5 Other End-user Industries

- 6.4 By Country

- 6.4.1 United Kingdom

- 6.4.2 Germany

- 6.4.3 France

- 6.4.4 Italy

- 6.4.5 Spain

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 O.Berk Company

- 7.1.2 Guala Closures SpA

- 7.1.3 Pelliconi & C. SpA

- 7.1.4 C.L. Smith Co. (Novvia Group)

- 7.1.5 Technocap SpA

- 7.1.6 Can-Pack SA

- 7.1.7 Amcor PLC

- 7.1.8 P. Wilkinson Containers Ltd

- 7.1.9 Silgan Closures (Silgan Holdings Inc.)

- 7.1.10 ACTEGA (A member of ALTANA)

- 7.1.11 Berlin Packaging

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

10 ABOUT US

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日