アジア太平洋の金属製キャップ・クロージャー:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

Asia Pacific Metal Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549965

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

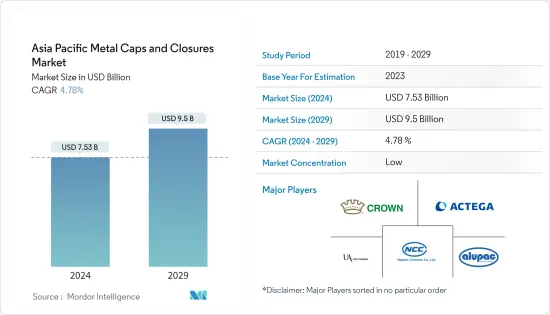

アジア太平洋の金属製キャップ・クロージャーの市場規模は、2024年に75億3,000万米ドルと推定され、2029年には95億米ドルに達すると予測され、予測期間中(2024年~2029年)のCAGRは4.78%で成長する見込みです。

主なハイライト

- インドや中国など人口密度の高い国々が需要を牽引しており、アジア太平洋市場は今後数年で成長する見込みです。人口増加と可処分所得の増加により、消費者はパッケージ製品やプレミアム製品へと舵を切り、同地域の多様な産業で金属製キャップ・クロージャーの需要が高まっています。

- 金属製キャップは、賞味期限を延ばし、味、風味、食感を保持することで、包装産業において極めて重要です。漏れにくく汚染に強い特性は、視覚的な魅力を高めるだけでなく、ブランドの差別化を助け、消費者の利便性を高めます。これらの汎用性の高いクロージャーは、飲食品、医薬品などの分野で広く利用されています。

- 包装食品と飲食品の需要が大幅に急増する中、これらの消耗品の鮮度を長期間保持する上でキャップ・クロージャーの役割は極めて重要であり、これらの地域における市場の推進力となっています。

- 同地域では医薬品生産が急増しており、規制の変化も相まって、小児用で付加価値が高く、高齢者にも優しいキャップがますます好まれるようになっています。この動向は、今後数年間で市場を牽引するものと思われます。さらに、小児用でいたずら防止の金属製キャップ・クロージャーの採用が急増しており、市場を大きく牽引しています。その結果、メーカーはより高品質の金属製キャップ・クロージャーの製造に軸足を移しています。

- 環境に優しい製品に対する需要の高まりが、金属製キャップ・クロージャーの普及を後押ししています。プラスチックキャップが手ごわい課題である一方で、プラスチックキャップ市場は環境への影響についてますます精査されるようになっており、金属製の代替品への道が開かれつつあります。これを受けて、多くの企業がプラスチック製から金属製キャップ・クロージャーへの移行を始めています。

アジア太平洋の金属製キャップ・クロージャー市場動向

市場のかなりの部分をアルミが占めると予測

- アルミ製キャップ・クロージャーは、代替材料に比べて耐久性と安定性に優れています。さまざまなサイズやスタイルがあり、製品の安全性、ブランディング、ユニークなデザインの魅力などを背景に、需要は急増する見通しです。さらに、より小さく、より便利な包装オプションへの嗜好の高まりに後押しされ、市場はさらに拡大するとみられます。

- リサイクル性の高さで知られるアルミニウムは、加工後もその核となる特性を維持するため、新鮮なアルミニウムを製造するよりもコスト効率が高く、環境に優しい代替品となります。さらに、アルミニウムのリサイクルは循環経済を促進し、金属の永続的な再利用性を保証します。

- プラスチック廃棄物による環境の悪化に対する意識が高まった結果、この地域のメーカーは、アルミニウムのような環境に優しい包装材に移行しています。例えば、UAパッケージングは、容器製造工程にアルミニウムを組み込むことで、持続可能性とネット・ゼロ・エミッションを採用しています。さらに、アルミニウムの自然な輝きは、高級感のあるパッケージを求める消費者を魅了します。同社はALUエアレスジャーで、持続可能性と高級感を両立させた独自のエコ・ラグジュアリー・パッケージング・ラインを構築しています。

- さらに、中国は昨年、電力不足の危機が解消した後に製錬所が生産量を増やし、アルミニウム生産量で過去最高を記録しました。同国の堅調な生産と消費の指標は、この商品を後押ししています。アルミニウムの消費量と生産量の両方で世界をリードする中国は、世界の総消費量の半分以上を占めています。

インドは市場で大きなシェアを占めると予想される

- アジア太平洋は、中国とインドの膨大な人口に牽引され、急速な成長を遂げようとしています。これらの国々における可処分所得の増加は、金属製キャップ・クロージャー市場の成長を後押しします。

- さらに、インドではアルコール飲料とノンアルコール飲料の消費が伸びており、金属製キャップ・クロージャー市場にプラスの影響を与えています。Banco do Nordesteの調査によると、2020年度のインドにおけるアルコール消費量は48億6,000万リットルでした。 2024年度の消費量は62億1,000万リットルに達すると予想されており、同国のアルコール飲料包装分野を後押ししています。

- 金属製クロージャーは、主にリサイクル性、耐久性、優れた漏れ防止性と耐汚染性により、飲料分野で最も高い採用率を示しています。特に飲料分野では、ビールが金属製クロージャー採用のトップランナーとなっています。

- さらに、国内の金属製キャップ・クロージャー市場の成長は、アルミニウム生産の増加によって後押しされます。例えば、2022年4月、Hindalco Industries Ltdは、世界の供給不足と旺盛な需要により、今後5年間でアルミニウム事業を拡大するために最大72億米ドルを投資する計画を発表し、前例のない価格となりました。ムンバイに本社を置く同社は、供給制約と旺盛な需要により価格が高止まりすることを見越して、数年間130万トンに抑えていたインドの1次アルミニウム生産能力を拡大します。インドのアルミニウム消費量は2032年3月までに約800万トンに達すると予測されています。

アジア太平洋の金属製キャップ・クロージャー産業の概要

アジア太平洋の金属製キャップ・クロージャー市場は、複数の国内メーカーとグローバルメーカーが存在するため、競争が激しくなっています。この市場の主要企業には、Crown Holdings Inc.、UA Packaging、ACTEGA、Nippon Closures、Alupac Indiaなどがあります。市場では、製品の差別化、ポートフォリオ、価格設定に関して激しい競争が繰り広げられています。付加価値の高いクロージャーと不正開封防止の需要の高まりは、様々なセグメントでの金属製キャップ・クロージャーの使用を増加させると思われます。

- 2023年4月UA Packagingは、異なるサイズの瓶やボトルに合うように調整できる新しい環境に優しいツールを発売しました。DOUBLE PCSアルミキャップは、軽すぎる、変形しやすい、ネジ山が見えるといったシングルピース・キャップの問題点を解決するために設計されています。アルミシェルの薄い金属板、粗い断面、鋭利なエッジは、肌に触れると不快感を与えますが、UAは高度なカーリングダイ技術でこの問題に取り組みました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度:ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 様々なエンドユーザーからの革新的ソリューションに対する需要の増加

- 他のクロージャー材料と比較した優れた特性

- 市場抑制要因

- 他のタイプのクロージャー材料の高い採用率

第6章 市場セグメンテーション

- 材料タイプ別

- アルミニウム

- スチール

- クロージャータイプ別

- クラウンキャップ

- スクリューキャップ

- ツイスト金属製キャップ

- その他のキャップ

- エンドユーザー産業別

- 食品

- 飲料

- アルコール

- ノンアルコール

- 医薬品

- パーソナルケア

- その他エンドユーザー産業

- 国別

- 中国

- 日本

- インド

- オーストラリア・ニュージーランド

- その他アジア太平洋

第7章 競合情勢

- 企業プロファイル

- Crown Holdings Inc.

- O.Berk Company

- Guala Closures SpA

- Berlin Packaging

- Silgan White Cap LLC

- Sonoco Products Company

- Alupac India

- Nippon Closures Co. Ltd

- ACTEGA(ALTANAのメンバー)

- UA Packaging

- 投資分析

- 市場の将来

目次

The Asia Pacific Metal Caps And Closures Market size is estimated at USD 7.53 billion in 2024, and is expected to reach USD 9.5 billion by 2029, growing at a CAGR of 4.78% during the forecast period (2024-2029).

Key Highlights

- With densely populated countries, such as India and China, driving demand, the Asia-Pacific market is poised for growth in the coming years. Rising populations and disposable incomes are steering consumers toward packaged and premium products, fueling a heightened demand for metal caps and closures across diverse industries in the region.

- Metal closures, by extending shelf-life and preserving taste, flavor, and texture, are pivotal in the packaging industry. Their leak-proof and contamination-resistant properties not only enhance visual appeal but also aid in brand differentiation and elevate consumer convenience. These versatile closures are widely utilized across sectors, including food, beverages, and pharmaceuticals.

- With a significant surge in demand for packaged foods and beverages, the pivotal role of caps and closures in preserving the freshness of these consumables for extended durations is poised to propel the market in these regions.

- The region's burgeoning pharmaceutical production, coupled with regulatory shifts, is increasingly favoring child-resistant, value-added, and senior-friendly closures. This trend is poised to propel the market in the coming years. Additionally, the surging adoption of child-resistant and tamper-evident metal caps and closures has garnered significant market traction. Consequently, manufacturers are pivoting toward crafting higher-quality metal caps and closures.

- The rising demand for eco-friendly products is driving the uptake of metal caps and closures. While plastic caps present a formidable challenge, the plastic caps market is increasingly under scrutiny for its environmental impact, paving the way for metal alternatives. In response, numerous companies have begun transitioning from plastic to metal caps and closures.

Asia Pacific Metal Caps And Closures Market Trends

A Considerable Portion of the Market is Anticipated to be Held by Aluminum

- Aluminum caps and closures offer superior durability and stability compared to alternative materials. Available in various sizes and styles, their demand is poised to surge, propelled by considerations like product safety, branding, and the appeal of their unique designs. Moreover, the market is set to expand further, buoyed by the rising preference for smaller, more convenient packaging options.

- Aluminum, known for its high recyclability, retains its core properties post-processing, rendering it a cost-effective and environmentally friendly alternative to manufacturing fresh aluminum. Moreover, aluminum recycling fosters a circular economy, ensuring the metal's perpetual reusability.

- As a result of increased consciousness regarding the environment's well-being caused by plastic waste, manufacturers in the region have transitioned to eco-friendly packaging alternatives like aluminum. For instance, UA Packaging has embraced sustainability and net-zero emissions by integrating aluminum into its container-making process. Moreover, aluminum's natural shine can attract consumers looking for luxurious packaging. With ALU Airless jar, the company is creating its own eco-luxe packaging line that balances sustainability and luxury.

- Furthermore, China hit a new high in aluminum production last year, with smelters ramping up output after the power shortage crisis resolution. The country's robust production and consumption metrics are bolstering the commodity. As the global leader in both aluminum consumption and production, China accounts for more than half of the world's total consumption.

India is Expected to Hold a Significant Share in the Market

- Asia-Pacific is poised for rapid growth, driven by the substantial populations of China and India. Rising disposable incomes in these nations are set to bolster the growth of the metal caps and closures market.

- Moreover, the growing consumption of alcoholic and non-alcoholic beverages in India has shown a significant rise, positively impacting the metal caps and closures market. According to a study performed by Banco do Nordeste, alcohol consumption in India was 4.86 billion liters in FY 2020. Consumption is expected to reach 6.21 billion liters in FY 2024, boosting the country's alcoholic beverage packaging segment.

- Metal closures see the highest adoption rates in the beverage sector, primarily due to their recyclability, durability, and superior leak-proof and contamination-resistant qualities. Notably, within the beverage landscape, beer emerges as the frontrunner for embracing metal closures.

- Furthermore, the growth of the country's metal caps and closures market is set to be boosted by an increase in aluminum production. For instance, in April 2022, Hindalco Industries Ltd announced its plan to invest up to USD 7.2 billion in expanding its aluminum business over the next five years due to global supply shortages and strong demand, resulting in unprecedented prices. The Mumbai-based company is expanding its primary aluminum capacity in India after holding it at 1.3 million tonnes for several years to anticipate that prices will remain high because of supply constraints and strong demand. India's aluminum consumption is predicted to reach approximately 8 million tonnes by March 2032.

Asia Pacific Metal Caps And Closures Industry Overview

The Asia-Pacific metal caps and closures market is highly competitive due to the presence of several domestic and global manufacturers. Some of the key players in this market are Crown Holdings Inc., UA Packaging, ACTEGA, Nippon Closures Co. Ltd, and Alupac India. Intense competition prevails in the market regarding product differentiation, portfolio, and pricing. The rising demand for value-added closures and tamper resistance properties will augment the usage of metal caps and closures in various segments.

- April 2023: UA Packaging launched a new eco-friendly tool that can be adjusted to fit jars or bottles of different sizes. The DOUBLE PCS Aluminum caps are designed to fix the issues with single-piece caps, such as being too lightweight, easily deformed, and having visible threads. The thin metal plate, rough cross-section, and sharp edges of the aluminum shell can cause discomfort when in contact with skin, but UA has tackled this problem with advanced curling die technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Innovative Solutions from Various End Users

- 5.1.2 Superior Properties Compared to Other Closure Materials

- 5.2 Market Restraints

- 5.2.1 High Adoption Rate of Other Types of Closure Materials

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By Closures Type

- 6.2.1 Crown Caps

- 6.2.2 Screw Caps

- 6.2.3 Twist Metal Caps

- 6.2.4 Other Closure Types

- 6.3 By End-user Industry

- 6.3.1 Food

- 6.3.2 Beverages

- 6.3.2.1 Alcoholic

- 6.3.2.2 Non-alcoholic

- 6.3.3 Pharmaceuticals

- 6.3.4 Personal Care

- 6.3.5 Other End-user Industries

- 6.4 By Country

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 India

- 6.4.4 Australia and New Zealand

- 6.4.5 Rest of Asia-Pacific

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 Crown Holdings Inc.

- 7.1.2 O.Berk Company

- 7.1.3 Guala Closures SpA

- 7.1.4 Berlin Packaging

- 7.1.5 Silgan White Cap LLC

- 7.1.6 Sonoco Products Company

- 7.1.7 Alupac India

- 7.1.8 Nippon Closures Co. Ltd

- 7.1.9 ACTEGA (A member of ALTANA)

- 7.1.10 UA Packaging

- 7.2 INVESTMENT ANALYSIS

- 7.3 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日