北米の金属製キャップおよびクロージャ:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

North America Metal Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549926

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

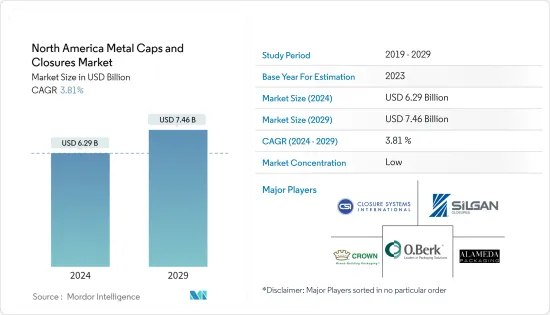

北米の金属製キャップおよびクロージャ市場規模は2024年に62億9,000万米ドルと推定され、2029年には74億6,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは3.81%で成長する見込みです。

主なハイライト

- この地域では環境に優しい製品への注目が高まっており、金属製キャップおよびクロージャの普及を後押ししています。プラスチック製キャップは金属製キャップにとって手ごわい課題であるが、プラスチックの不適切な廃棄に対する環境問題の高まりが、プラスチック製キャップに関連するリスクを増大させています。その結果、この力学が金属製キャップおよびクロージャの道を開いています。注目すべきは、こうした動向を受けてプラスチックから金属製キャップおよびクロージャへの移行を開始する企業が増えていることです。

- 金属製キャップおよびクロージャ市場で大きなシェアを占める食品業界は、必需品としての分類に後押しされ、需要が急増しています。この需要の高まりは、肉、野菜、果物の消費だけでなく、包装食品にも顕著に表れています。さらに、包装飲料や医薬品への需要も着実に高まっています。その結果、金属製キャップおよびクロージャの地域市場は、今後数年間で顕著な需要増加の態勢を整えています。

- 包装業界は、漏れ防止、簡単な閉鎖、強化されたバリア特性といった従来のニーズを超える需要の高まりに直面しています。イノベーションは業界の要として台頭し、消費者や社会の刻々と変化するニーズに適応しています。特に、金属キャップおよびクロージャの進歩は主に素材、重量、環境適合性、コスト効率をターゲットにしています。

- 医薬品業界は、耐小児性とコンタミネーションフリーのパッケージング機能が評価され、改ざん防止キャップおよびクロージャの需要を牽引する態勢を整えています。企業は賞味期限を延ばす製品を求めています。製品を出荷するメーカーが増えるにつれ、輸送や多様な環境条件に耐える堅牢な包装が不可欠となっています。

- さらに、化粧品やホームケア製品でキャップやクロージャの使用が拡大していることも、市場の成長を後押ししています。さらに、育児用製品の需要の増加が市場をさらに押し上げると予想されます。

北米の金属製キャップおよびクロージャ市場動向

飲料セグメントが大きな市場シェアを占める見込み

- アルコール飲料とノンアルコール飲料の消費量の増加と飲料パッケージング産業からの需要の増加により、金属製キャップおよびクロージャ市場は同地域で成長すると予測されます。

- 北米は、著しい成長と利益率を誇る消費者飲料パッケージング産業として継続すると予想されます。これは主に、同地域の消費者飲料に対する旺盛な需要と、飲料パッケージングにおける業界の自動化導入の増加によるものです。米国は、世界レベルで飲料パッケージングに大きく貢献している国のひとつです。

- さらに、消費者は、一人当たりの可処分所得の上昇を背景とした消費支出の増加により、安価なアルコールのまとめ買いから高級なプレミアムアルコール飲料の購入へと移行しています。カナダ統計局によると、2023年3月31日に終了する会計年度において、カナダでは1人当たり約94.5リットルのアルコール飲料が販売されました。

- さらに米国では、環境保護という持続可能な目標を達成するため、企業がリサイクル活動を開始するケースが増えています。例えば、米国を拠点とする金属製キャップ・キャップ製造会社のクラウン・ホールディングス社は、業界パートナーと協力して、世界規模での飲料用アルミ缶のリサイクル率に関する新たな野心的目標を達成しようとしています。米国における新たな目標は、現在の平均45%から、2030年までに70%、2040年までに80%、2050年までに90%に引き上げることです。

- 金属製のキャップおよびクロージャは、ワインの品質と鮮度を保つことができるため、ワインボトルの包装にますます普及しています。アルミニウム製のスクリュー・クロージャは、ワイン独特の味と香りを保つための現代的なソリューションです。このクロージャは酸化を防ぎ、ワインが熟成するための純粋な環境を提供するため、時間が経っても品質が変わらないことを保証します。使い勝手がよく、さまざまなデザインオプションでカスタマイズの機会も豊富です。さらに、このアルミキャップは環境に優しく、リサイクルも可能なため、循環型経済モデルにも最適です。

市場のかなりの部分をアルミが占めると予想される

- アルミ製キャップおよびクロージャは、他の素材に比べて頑丈で、パッケージングが安定しています。これらのキャップには様々なスタイルやサイズがあり、その市場需要は製品の安全性、独自性、ブランディングといった要因によって牽引される可能性が高いです。さらに、包装サイズの小型化や利便性に対する需要の高まりにより、市場の拡大が見込まれています。

- さらに、アルミ製クロージャは製品の味や匂いに影響を与えることなく、非常に効果的なバリアを形成します。アルミ製クロージャはニュートラルなプロファイルを誇り、味や色の変化を回避して医薬品の完全性を維持するために極めて重要です。世界の糖尿病人口の急増に伴い、インスリン注射、注射器、注射ペンの需要も増加しています。その結果、アルミキャップは注射器のノズル、バイアル、カートリッジで有用性が高まっています。

- さらに、FDA、CPSC、ISOによる厳しい規制が、医薬品、飲食品、化粧品業界全体の製品革新と高度化を後押ししています。メーカーは、アルミキャップやクロージャだけでなく、規制を満たすために、利便性、小児への耐性、高齢者への配慮といった製品機能をますます利用するようになっています。

- 近年、米国のアルミニウム協会は、アルミニウム・リサイクルの改善に向けて大きな一歩を踏み出しています。同協会は環境保護庁(EPA)と協力して自主的なプログラムを作成し、製造業におけるリサイクル材料の使用を奨励するキャップ・アンド・トレード炭素政策を支持しています。アルミニウムのリサイクルイニシアチブは、この地域のメタルキャップおよびクロージャのメーカーに潜在的な成長の見込みを提供しています。

北米の金属製キャップおよびクロージャ産業の概要

北米の金属製キャップおよびクロージャ市場は、複数の国内メーカーと世界メーカーが存在するため競争が激しいです。この市場の主要企業には、Crown Holdings、O.Berk Company、Closure Systems International Inc.(CSI)、Alameda Packaging LLCなどがあります。市場では、製品の差別化、ポートフォリオ、価格設定に関して激しい競争が繰り広げられています。付加価値の高いクロージャと耐タンパー性の需要の高まりは、医薬品と飲料を中心とする様々な分野でのメタルキャップおよびクロージャの使用を増大させると思われます。

- 2024年1月持続可能なアルミニウムソリューションの著名なプロバイダーであり、アルミニウム圧延とリサイクルの世界的リーダーであるNovelis Inc.は、持続可能なアルミニウム飲料包装の主要企業であるArdagh Metal Packaging USA Corp.との新たな合意を明らかにしました。この契約により、ノベリスは飲料用アルミニウム包装シートをアーダグの北米金属包装生産拠点に供給することになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 様々なエンドユーザーからの革新的ソリューションに対する需要の増加

- 他のクロージャ材料と比較した優れた特性

- 市場抑制要因

- 他のタイプのクロージャ材料の高い採用率

第6章 市場セグメンテーション

- 材料タイプ別

- アルミニウム

- スチール

- クロージャタイプ別

- クラウンキャップ

- スクリューキャップ

- ツイストメタルキャップ

- その他のクロージャタイプ(イージーオープンエンドとROPPメタルキャップ)

- エンドユーザー産業別

- 食品

- 飲料

- アルコール飲料

- ノンアルコール

- 医薬品

- パーソナルケア

- その他のエンドユーザー産業

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Crown Holdings Inc.

- O.Berk Company

- Guala Closures SpA

- Pelliconi & C. SpA

- Closure Systems International Inc(CSI)

- Silgan Closures(Silgan Holdings Inc.)

- SKS Bottle & Packaging Inc.

- Amcor Group GmbH

- Qorpak(Berlin Packaging)

- Alameda Packaging LLC

- Massilly North America(Massilly Group)

第8章 投資分析

第9章 市場の将来

目次

The North America Metal Caps And Closures Market size is estimated at USD 6.29 billion in 2024, and is expected to reach USD 7.46 billion by 2029, growing at a CAGR of 3.81% during the forecast period (2024-2029).

Key Highlights

- The region's increasing focus on eco-friendly products has propelled the uptake of metal caps and closures. While plastic caps present a formidable challenge to their metal counterparts, heightened environmental worries over improper plastic disposal are amplifying the risks associated with plastic caps. Consequently, this dynamic is opening up avenues for metal caps and closures. Notably, a growing number of companies have begun the transition from plastic to metal caps and closures in response to these trends.

- The food industry, commanding a significant share in the metal caps and closures market, is experiencing surging demand, bolstered by its classification as an essential commodity. This heightened demand is notably evident in packaged food items, as well as in the consumption of meat, vegetables, and fruits. Additionally, the appetite for packaged beverages and pharmaceuticals is steadily rising. Consequently, the regional market for metal caps and closures is poised for a notable uptick in demand in the coming years.

- The packaging industry faces heightened demands beyond the traditional need for leak prevention, easy closure, and enhanced barrier properties. Innovation has emerged as the industry's cornerstone, adapting to the ever-changing needs of consumers and society-notably, advancements in metal caps and closures primarily target material, weight, eco-friendliness, and cost-efficiency.

- The pharmaceuticals industry is poised to drive the demand for tamper-evident caps and closures, valued for their child-resistant and contamination-free packaging features. Companies seek products that extend shelf life. As more manufacturers ship products, robust packaging is essential to withstand transportation and diverse environmental conditions.

- Moreover, the expanding use of caps and closures in cosmetics and home care products is set to bolster market growth. Additionally, the increasing demand for childcare products is expected to boost the market further.

North America Metal Caps And Closures Market Trends

The Beverage Segment is Expected to Account for a Significant Market Share

- The metal caps and closures market is expected to grow in the region due to the rise in alcoholic and non-alcoholic beverage consumption and the increasing demand from the beverage packaging industry.

- North America is anticipated to continue as the consumer beverage packaging industry with significant growth and profit margins. This is primarily due to the region's strong demand for consumer drinks and the industry's increasing adoption of automation in beverage packaging. The United States is one of the significant contributors to beverage packaging on a global level.

- Furthermore, consumers have transitioned from buying cheap alcohol in bulk to purchasing high-end, premium alcoholic drinks due to rising consumer expenditure, backed by rising per capita disposable income. According to Statistics Canada, approximately 94.5 liters of alcoholic drinks were sold per person in Canada for the fiscal year ending on March 31, 2023.

- Moreover, companies in the United States are increasingly initiating recycling activities in order to achieve sustainable goals to protect the environment. For instance, Crown Holdings Inc., a US-based metal caps and closures manufacturing company, is working with industry partners to meet new, ambitious targets for the rate of recycling of aluminum beverage cans on a worldwide scale. The new goals in the United States aim to increase the average from the current 45% to objectives of 70% by 2030, 80% by 2040, and 90% by 2050.

- Metal caps and closures are becoming increasingly popular in wine bottle packaging due to their ability to preserve the quality and freshness of the wine. Screw closures made from aluminum are a modern solution for preserving the unique taste and aroma of wine. These closures prevent oxidation and provide a pure environment for wine to mature, ensuring its quality remains unchanged over time. They are user-friendly and offer ample opportunities for customization with various design options. Moreover, these aluminum caps are eco-friendly and can be recycled, making them an excellent addition to circular economy models.

A Considerable Portion of the Market is Anticipated to be Held by Aluminum

- Aluminum caps and closures are sturdier and more stable for packaging compared to other materials. These caps come in various styles and sizes, and their market demand is likely to be driven by factors such as product safety, uniqueness, and branding. Additionally, the market is expected to grow due to increased demand for smaller packaging sizes and convenience.

- Moreover, aluminum closures create a highly effective barrier without affecting the product's taste and smell. Aluminum closures boast a neutral profile, which is crucial for preserving the integrity of drugs by averting taste and color alterations. As the global diabetic population surges, so does the demand for insulin shots, syringes, and injection pens. Consequently, aluminum caps have heightened utility in syringe nozzles, vials, and cartridges.

- Additionally, stringent regulations by the FDA, CPSC, and ISO have driven product innovation and sophistication across the pharmaceutical, food and beverage, and cosmetic industries. Manufacturers increasingly use product features such as convenience, child resistance, and senior friendliness to meet the regulations, as well as aluminum caps and closures.

- In recent years, the Aluminum Association in the United States has taken significant steps toward improving aluminum recycling. The Association has worked in partnership with the Environmental Protection Agency (EPA) to create voluntary programs and endorsed cap and trade carbon policy to encourage the use of recycled materials in manufacturing. The aluminum recycling initiative offers potential growth prospects for manufacturers of metal caps and closures in the region.

North America Metal Caps And Closures Industry Overview

The North American metal caps and closures market is highly competitive due to the presence of several domestic and global manufacturers. Some of the key players in this market are Crown Holdings, O.Berk Company, Closure Systems International Inc. (CSI), and Alameda Packaging LLC. Intense competition prevails in the market regarding product differentiation, portfolio, and pricing. The rising demand for value-added closures and tamper resistance properties will augment the usage of metal caps and closures in various segments, primarily pharmaceuticals and beverages.

- January 2024: Novelis Inc., a prominent provider of sustainable aluminum solutions and the global leader in aluminum rolling and recycling, revealed a fresh agreement with Ardagh Metal Packaging USA Corp., a key player in sustainable aluminum beverage packaging. As per the deal, Novelis is set to provide aluminum beverage packaging sheets to Ardagh's North American metal packaging production sites.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyer

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Innovative Solutions from Various End Users

- 5.1.2 Superior Properties Compared to Other Closure Materials

- 5.2 Market Restraints

- 5.2.1 High Adoption Rate of Other Types of Closure Materials

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By Closure Type

- 6.2.1 Crown Caps

- 6.2.2 Screw Caps

- 6.2.3 Twist Metal Caps

- 6.2.4 Other Closure Type (Easy Open Ends and ROPP Metal Caps)

- 6.3 By End-user Industry

- 6.3.1 Food

- 6.3.2 Beverages

- 6.3.2.1 Alcoholic

- 6.3.2.2 Non-Alcoholic

- 6.3.3 Pharmaceuticals

- 6.3.4 Personal Care

- 6.3.5 Other End-user Industries

- 6.4 By Country

- 6.4.1 United States

- 6.4.2 Canada

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 Crown Holdings Inc.

- 7.1.2 O.Berk Company

- 7.1.3 Guala Closures SpA

- 7.1.4 Pelliconi & C. SpA

- 7.1.5 Closure Systems International Inc (CSI)

- 7.1.6 Silgan Closures (Silgan Holdings Inc.)

- 7.1.7 SKS Bottle & Packaging Inc.

- 7.1.8 Amcor Group GmbH

- 7.1.9 Qorpak (Berlin Packaging)

- 7.1.10 Alameda Packaging LLC

- 7.1.11 Massilly North America (Massilly Group)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日