英国のB2B固定接続:市場シェア分析、産業動向、成長予測(2024年~2029年)

UK B2B Fixed Connectivity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549944

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

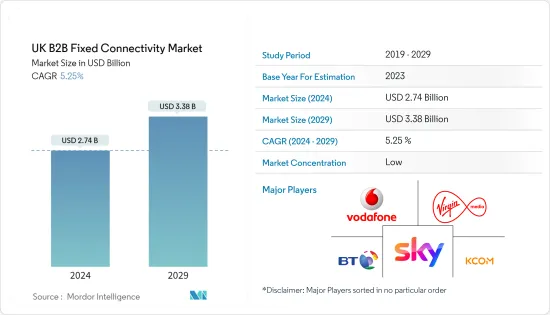

英国のB2B固定接続市場規模は2024年に27億4,000万米ドルと推定され、2029年には33億8,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは5.25%で成長する見込みです。

固定回線とは、顧客向けのケーブルベースの接続ソリューションを指します。固定回線接続には、光ファイバーであれ銅線であれ、物理的な回線に依存するすべてのインターネット接続が含まれます。英国のB2B固定接続市場は、通信産業の重要なセグメントであり、企業が効率的に業務を遂行し、デジタル化が進む世界で接続を維持するために不可欠なインフラとサービスを提供しています。

主要ハイライト

- 企業はデジタルトランスフォーメーションを活用し、ソフトウェア統合によって顧客維持率を高め、エクスペリエンスを向上させ、ブランドの評判を高めています。そのような企業は、技術の進歩を巧みに操り、産業の変化に応じて迅速にピボットします。特筆すべきは、COVID-19パンデミックの発生がデジタルトランスフォーメーション推進のきっかけとなり、英国政府機関が取り組みを急ぐようになったことです。

- 固定回線は高速インターネットを提供できます。光ファイバーによるイーサネットや銅線によるイーサネットのように、拡大性と柔軟性があります。そのため、あらゆる規模のビジネスに適しており、費用対効果の高い高速ネットワークソリューションを記載しています。

- 英国では、在宅勤務の傾向はまだ根強いが、現在は徐々に消え始めています。国家統計局の統計によると、2023年6月現在、英国の労働者の勤務形態は、常時在宅勤務が10%、一部在宅勤務が29%、在宅勤務不可が39%となっています。在宅勤務の動向の変化に伴い、英国の企業は、増加する現場労働者をサポートするために、高品質の固定接続ソリューションへの投資が必要になると予想されます。

- AIやML技術の採用が増加していることが、固定回線接続の需要を促進しています。英国政府は、量子、AI、工学生物学、半導体、未来の電気通信の5つを将来の主要技術として挙げています。注目すべきは、英国が9億英ポンド(約1,119.40米ドル)を投じて最先端のスーパーコンピューターを開発することで、これは国産のBritGPTを実現することを目的とした広範な人工知能戦略において極めて重要な動きとなっています。さらに、クラウドコンピューティング、AI/ML、データセンター技術の急増は、この市場に大きな利益をもたらすと見られています。

- 高いコストとサイバーセキュリティは、市場の成長軌道を大きく形成しています。例えば、インターネットサービスプロバイダのBeamingの調査によると、サイバー犯罪によって昨年英国経済は305億英ポンド(約37.94米ドル)の損害を受け、150万社の企業に影響が及んだことが明らかになりました。これは、企業にとって高速接続ソリューションの利用しやすさと手頃な価格を妨げるだけでなく、企業のサイバーセキュリティ予算を押し上げ、運営費を圧迫しています。

- さらに、ダウンタイムや接続障害も市場に悪影響を及ぼす可能性があります。例えば、ロンドンを拠点とする企業向け直接インターネット接続プロバイダーであるVorbossは、英国経済は昨年、接続障害により経済生産高が176億英ポンド(約218億9,000万米ドル)減少したと推定しています。その生産性分析を受けて、ヴォーボスは英国の通信規制当局であるOfcomに対し、接続のダウンタイムに直面した企業に対する自動補償制度の導入を検討するよう求めています。同社の調査によると、固定インターネット契約を結んでいる企業の半数以上(51%)が前年にサービスの中断に遭遇しており、ロンドンの企業ではその数が60%に上った。さらに、5分の1近く(19%)の企業が3回以上のサービス停止を経験しており、ロンドンではその数が28%に上った。潜在的な課題には直面しているもの、固定接続産業では市場は改善に向かっています。

英国のB2B固定接続市場の動向

固定データは急速な成長が見込まれる

- 固定データには、専用/私設回線、パケット、回線交換アクセスサービスのすべてが含まれ、標準的なブロードバンド接続の共有型とは対照的です。固定データでは、ユーザーは全帯域幅に自由にアクセスできるため、速度低下や不安定なパフォーマンスに対する懸念が解消されます。さらに、専用回線やプライベート回線には通常、サービス・レベル・アグリーメント(SLA)が付属しており、確約された品質とパフォーマンス基準が保証されています。

- 高速で信頼性の高い接続性へのニーズは高まっており、専用線サービスは極めて重要なソリューションとして注目されています。2023年には、固定専用線接続が英国のビジネスインターネット市場を席巻し、39%を超えるシェアを獲得した(ITインフラ企業Connect2の報告によると、この数字は一貫して上昇を続けている)。

- 固定データサービスの一部である専用線またはネットワークの典型的なエンドユーザーは、非公開会社、企業オフィス、企業です。GOV.UKと英国ビジネスエネルギー・産業戦略省によると、2023年、英国では約556万社の民間企業が営業しており、前年と比べ微増となっています。英国ビジネス貿易省によると、民間企業人口は0.8%(4万6,000社)増加しました。同国の民間企業やビジネスセクターの成長は、固定データネットワークの需要を促進すると予想されます。

- さらに、ITを含むハイテク産業はデータの重要な消費者であり、高速インターネットを必要としています。著名なオンライン教育・認証プラットフォームである商船三井によると、英国のハイテク部門は170万人以上の労働力を誇り、年間1,500億英ポンド(約1,900億米ドル)の実質的な国家経済に貢献しています。好条件が揃えば、英国のハイテク部門は2025年までにさらに415億ポンド(約520億米ドル)を経済に投入し、67万8,000人の新規雇用を生み出す可能性があります。こうした予測を踏まえると、急成長するハイテク・IT部門は、市場調査の主要な促進要因になると考えられます。

- さらに、クラウド導入の急増が英国の専用線産業を後押ししています。ハイブリッド・マルチクラウドコンピューティング企業の主要企業であるNutanixの報告によると、英国の回答者の84%が「クラウドスマート」アプローチを採用しています。これには、データセンター、複数のクラウド、ネットワークエッジにまたがるアプリケーションとワークロードの展開が含まれます。英国では、ハイブリッド・マルチクラウドモデルの採用率が現在の19%から今後3年間で26%に上昇すると予測されています。同時に、複数のパブリック・クラウドの利用率は、今後1~3年以内に11%から46%に急増すると予想されています。英国の企業は、ウェブベースのコンテンツ配信、クラウドアプリケーション、音声サービス、オンラインバックアップに専用線を活用するのが一般的です。

高速接続への大きな需要

- 英国では、高速接続に対する需要が急増しています。この急増の主要要因は、特にデバイスの急増、モノのインターネット(IIoT)の登場、スマートシティなどの野心的な取り組みにより、企業と個人のインターネットへの依存度が高まっていることです。モノのインターネット(IoT)が注目されるにつれ、企業はますますデバイスをウェブに統合するようになっています。この統合は、インテリジェント照明や防犯カメラから、空調制御、空気清浄機、IoTセンサーの数々まで、さまざまなシステムに及んでいます。このようなネットワークには高速インターネットが必要で、この地域の調査対象市場を後押ししています。

- 英国科学技術革新省は、地域の接続性を強化するために、町や都市でスマート技術を検査的に導入するために400万ポンド(約497万米ドル)を割り当てた。130万英ポンド(約161万米ドル)の大規模な政府パイロットの一環として、英国のさまざまな町や都市がスマート街灯を導入することになっています。次世代デジタル技術を搭載したこれらの街灯は、EV充電を提供し、ワイヤレス接続を強化します。具体的には、ケンブリッジシャー州議会、ティース・バレー複合自治体、キングストン・アポン・テムズ王立区、ウェストミンスター市議会、オックスフォードシャー州議会、ノース・エアシャー州議会を含む6つの主要な地域が、これらの革新的な街灯のテストの先頭に立っています。

- SCADAやIIoTのようなコネクテッドシステムに加え、スマート工場の採用が増加しているため、この地域では高速インターネット接続の需要が高まっています。これが、調査対象市場の成長を後押ししています。その一例として、2024年2月、英国研究革新省のMSI課題は、Innovate UK、工学・物理科学研究評議会、経済社会研究評議会と共同で、英国のスマート工場プロジェクトを強化するために370万英ポンド(約460万米ドル)の助成金を発表しました。GSMAによると、オートメーションやロボット工学のようなシステムでは、100Mbpsを超えるスピードと1ミリ秒以下の待ち時間が要求されます。その結果、これらのシステムには安定した堅牢な高速インターネット接続が必要となり、製造業におけるスマートコネクテッドシステムの採用がさらに促進され、その結果、同地域の固定コネクティビティ市場を牽引することになります。

- 2023年11月、英国政府は国内のデータセンターインフラの強化を目的とした9億6,000万英ポンド(11億米ドル)の投資を発表しました。このイニシアチブは、スケールアップ企業に対する同国の魅力を高めるという政府の広範な戦略の極めて重要な部分です。英国のデータセンター市場の拡大に伴い、高速インターネット接続の需要も並行して急増し、このセグメントの成長をさらに後押ししています。

- 例えば、Googleは2024年1月、英国ハートフォードシャー州ウォルサムクロスの新データセンターに10億米ドルを投資すると発表しました。この動きは、英国のユーザーのためだけでなく、世界中の聴衆のために、AIの革新とデジタルサービスの向上を推し進めるグーグルの姿勢を明確にし、同国の計算能力を強化するものです。データセンターの拡大は、固定接続市場を強化する構えです。

- さらに、2023年には、BTが、インターネットにアクセスできる英国の世帯の約25%にとって主要なインターネットサービス・プロバイダーとしてトップの座を占めました。Skyが僅差で続き、回答者の21%が主要プロバイダーとなっています。一方、Virgin Mediaを支持する世帯は17%でした。これらの調査結果は、英国の放送、通信、郵便サービスを監督する公的規制機関であるOfcomによって報告されました。

英国のB2B固定接続産業概要

英国のB2B接続市場はセグメント化されており、Vodafone Limited、BT Group、Virgin Media Business Ltd、XLN Telecom Ltdといった主要企業が存在します。同市場の参入企業は、サービス提供を強化し、サステイナブル競争優位性を獲得するために、提携、契約、イノベーション、買収などの戦略を採用しています。

- 2024年2月、英国のVirgin Media O2(VMO2)は、主要株主であるLiberty GlobalとTelefonicaと共同で、国内固定ネットワーク事業体NetCoを設立する意向を明らかにしました。この戦略的決定は、フルファイバー技術の採用を強化し、金融の道を広げ、他のネットワーク・プロバイダーとの合併に道を開く可能性があることを意図しています。NetCoは、Virgin Media O2の完全子会社として運営され、約1,620万世帯に及ぶ同社のケーブルとファイバーインフラを統合します。

- 2024年2月英国最大のアルトネットであるCityFibreは、同国の50億英ポンド(約62億1,000万米ドル)のブロードバンド補助金イニシアティブであるProject Gigabitの下で5つの新規契約を獲得。総額3億9,400万英ポンド(約4億9,004万米ドル)のこれらの契約は、20万2,000世帯の農村部へのフルファイバー配備を促進することを目的としています。対象となる地域は、バッキンガムシャー、ハートフォードシャー、バークシャー、レスターシャー、ウォリックシャー、サセックス、ケント、ベッドフォードシャー、ノーサンプトンシャー、ミルトンキーンズなどです。さらに、CityFibreの資金援助により、同社はこれらの地域における現在のインフラを拡大するだけでなく強化し、さらに45万箇所の施設に到達することを目標としています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 英国における通信関連サービスの規制状況

第5章 市場力学

- 市場促進要因

- 高速接続に対する莫大な需要

- 産産業におけるデジタル変革の高まり

- 市場抑制要因

- データの安全性とプライバシーに関する懸念

- 先進的通信インフラに伴う多額の設備投資

- 英国のビジネス固定接続に関連する主要市場指標に関する洞察

- 英国の企業向け光ファイバーと固定ブロードバンドの価格分析

- 英国の企業による固定専用線の導入に関する洞察

第6章 市場セグメンテーション

- タイプ別

- 固定データ

- 固定音声

- 企業規模別

- 中小企業(SME)

- 大企業

第7章 競合情勢

- 企業プロファイル

- TalkTalk Business Direct Limited

- Sky UK

- Vodafone Limited

- BT Group

- Virgin Media Business Ltd

- bOnline Limited

- KCOM Group Limited

- Hyperoptic Ltd

- Gigaclear Ltd

- XLN Telecom Ltd

- Chess Ltd

第8章 投資分析

第9章 市場機会と今後の動向

目次

The UK B2B Fixed Connectivity Market size is estimated at USD 2.74 billion in 2024, and is expected to reach USD 3.38 billion by 2029, growing at a CAGR of 5.25% during the forecast period (2024-2029).

A fixed line refers to a cable-based connectivity solution for customers. Fixed line connectivity encompasses all internet connections that rely on a physical line, be it fiber optic or copper. The UK B2B fixed connectivity market is a vital segment of the telecommunications industry, providing essential infrastructure and services that enable businesses to operate efficiently and stay connected in an increasingly digital world.

Key Highlights

- Organizations leverage digital transformation to boost customer retention, enhance experiences, and fortify brand reputation via software integration. Such businesses adeptly navigate tech advancements and pivot swiftly in response to industry changes. Notably, the onset of the COVID-19 pandemic catalyzed the digital transformation drive, prompting UK government bodies to hasten their initiatives, with the UK government forming a digital strategy to grow the digital economy - addressing tech sector skills, investment, and infrastructure.

- Fixed line connections are capable of providing high-speed internet. They are scalable and flexible, like ethernet over fiber and ethernet over copper. Therefore, they are suitable for businesses of all sizes and provide cost-effective and high-speed network solutions.

- The work-for-home trend is still strong in the United Kingdom but has now started to fade away slowly. According to the statistics by the Office for National Statistics, as of June 2023, working arrangements among UK workers were: work-from-home all the time at 10%, work-from-home some of the time at 29%, and unable to work-from-home at 39%. With the changes in the work-from-home trend, it is expected that companies in the United Kingdom will have to invest in high-quality fixed connectivity solutions to support increasing on-site workforces.

- The increasing adoption of AI and ML technologies is driving the demand for fixed-line connectivity. The UK government has pinpointed five key technologies for the future: quantum, AI, engineering biology, semiconductors, and future telecoms. Notably, the country is committing GBP 900 million (~USD 1119.40) to develop a state-of-the-art supercomputer, a pivotal move in its broader artificial intelligence strategy, which aims to enable the creation of a homegrown BritGPT. Additionally, the surge in cloud computing, AI/ML, and data center technologies is poised to significantly benefit the market studied.

- High costs and cybersecurity significantly shape the market's growth trajectory. For example, a study by internet service provider Beaming revealed that cybercrime cost the UK economy GBP 30.5 billion (~USD 37.94) last year, impacting 1.5 million businesses. This not only hampers the accessibility and affordability of high-speed connectivity solutions for businesses but also drives up a company's cybersecurity budget, adding pressure to its operational expenses.

- Additionally, downtime and connectivity outages can also have a negative impact on the market. For instance, London-based Vorboss, a provider of direct internet connectivity for businesses, estimates that the UK economy saw a GBP 17.6 billion (~USD 21.89 billion) dip in economic output in the last year due to connectivity disruptions. Following its productivity analysis, Vorboss has urged the UK's communications regulator, Ofcom, to consider implementing an automatic compensation system for businesses facing connectivity downtime. Its study revealed that over half (51%) of businesses with fixed internet contracts encountered service disruptions in the previous year, a number that surged to 60% for businesses in London. Furthermore, nearly one-fifth (19%) of businesses experienced three or more outages, with the number spiking to 28% in London. Although facing potential challenges, the market is poised for improvement in the fixed connectivity industry.

UK B2B Fixed Connectivity Market Trends

Fixed Data is Expected to Grow at a Rapid Pace

- Fixed data includes all dedicated/private line, packet, and circuit-switched access services, which contrasts strongly with the shared nature of standard broadband connections. With fixed data, the user enjoys unimpeded access to the entire bandwidth, eliminating concerns over sluggish speeds or erratic performance. Moreover, dedicated or private lines typically come with a Service Level Agreement (SLA), ensuring a committed quality and performance standard.

- The need for fast and reliable connectivity is rising, with leased line services standing out as a pivotal solution. In 2023, fixed leased line connections dominated the UK business internet market, capturing a share exceeding 39%, a figure that has been consistently climbing, as reported by Connect2, an IT infrastructure firm.

- Companies, corporate offices, and businesses are typical end users of private lines or networks that are part of fixed data services. According to GOV.UK and the UK Department for Business, Energy and Industrial Strategy, in 2023, approximately 5.56 million private businesses were operating in the United Kingdom, a slight increase compared to the previous year. According to the UK Department of Business and Trade, the private sector business population increased by 0.8% (46,000 businesses). The growth in the private business or business sector in the country is expected to drive the demand for fixed data networks.

- Further, the tech industry, including IT, stands as a significant consumer of data, necessitating high-speed internet. As per MOL, a prominent online education and certification platform, the UK tech sector boasts a workforce of more than 1.7 million, contributing a substantial GBP 150 billion(~USD 190 Billion) annually to the nation's economy. With favorable conditions, the UK tech sector has the potential to inject an additional GBP 41.5 billion(~USD 52 Billion) into the economy and generate 678,000 new jobs by 2025. Given these projections, the burgeoning tech and IT sector is poised to be a key driver of the market studied.

- Moreover, a surge in cloud adoption is bolstering the leased line industry in the United Kingdom. Nutanix, a leading name in hybrid multi-cloud computing companies, reports that 84% of UK respondents are embracing a 'cloud smart' approach. This involves deploying applications and workloads across data centers, multiple clouds, and the network edge. In the UK, the adoption of hybrid multi-cloud models is projected to rise from 19% today to 26% in the next three years. Simultaneously, the utilization of multiple public clouds is expected to jump from 11% to 46% within the next one to three years. Businesses in the United Kingdom commonly leverage leased lines for web-based content distribution, cloud applications, voice services, and online backups.

Huge Demand for High-speed Connectivity

- In the United Kingdom, the demand for enhanced connectivity is surging. This surge is primarily fueled by the escalating reliance of both businesses and individuals on the Internet, especially with the proliferation of devices, the advent of the Industrial Internet of Things (IIoT), and ambitious initiatives such as smart cities. As the Internet of Things (IoT) gains prominence, businesses increasingly integrate their devices into the web. This integration spans a variety of systems, from intelligent lighting and security cameras to climate controls, air purifiers, and an array of IoT sensors. Such a network demands high-speed internet, propelling the market under study in the region.

- The UK Department for Science, Innovation, and Technology has allocated GBP 4 million (~USD 4.97 million) to trial smart technology in towns and cities to enhance local connectivity. As part of a larger GBP 1.3 million (~USD 1.61 million) government pilot, various UK towns and cities are set to roll out smart street lamps. These lamps, equipped with next-gen digital technology, will provide EV charging and bolster wireless connectivity. Specifically, six key areas, including Cambridgeshire County Council, Tees Valley Combined Authority, Royal Borough of Kingston upon Thames, Westminster City Council, Oxfordshire County Council, and North Ayrshire Council, are spearheading the testing of these innovative street lamps, which are designed to accommodate EV charging hubs, thereby driving the need for faster internet connections.

- The rising adoption of smart factories, alongside connected systems like SCADA and IIoT, is spurring a heightened demand for high-speed internet connectivity in the region. This, in turn, is propelling the growth of the market under study. A case in point: in February 2024, the UK Research and Innovation's MSI Challenge, in collaboration with Innovate UK, the Engineering and Physical Sciences Research Council, and the Economic and Social Research Council, announced a grant of GBP 3.7 million (~USD 4.6 million) to bolster smart factory projects in the UK. Notably, as per GSMA, systems like automation and robotics mandate speeds exceeding 100 Mbps, with latency under 1 ms. Consequently, these systems necessitate a stable and robust high-speed internet connection, further bolstering the adoption of smart connected systems in manufacturing and, consequently, driving the Fixed Connectivity Market in the region.

- In November 2023, the UK government unveiled a GBP 960 million (USD 1.1 billion) investment aimed at bolstering the nation's data center infrastructure. This initiative is a pivotal part of the government's broader strategy to enhance the country's appeal to scale-up companies. With the UK data center market expanding, there is a parallel surge in the demand for high-speed internet connectivity, further propelling the sector's growth.

- For instance, in January 2024, Google announced a USD 1 billion investment in a new data center in Waltham Cross, Hertfordshire, United Kingdom. This move is set to bolster the country's computational capabilities, underlining Google's push for AI innovation and improved digital services, not only for its UK users but for a global audience. The expansion of data centers is poised to bolster the fixed connectivity market.

- Further, in 2023, BT held the top spot as the primary internet service provider for approximately 25% of UK households with internet access. Sky followed closely, serving as the main provider for 21% of respondents. Meanwhile, 17% of households favored Virgin Media. These insights were reported by Ofcom, the country's official regulatory body overseeing broadcasting, telecommunications, and postal services.

UK B2B Fixed Connectivity Industry Overview

The UK B2B connectivity market is fragmented, with major players like Vodafone Limited, BT Group, Virgin Media Business Ltd, and XLN Telecom Ltd. Players in the market are adopting strategies such as partnerships, agreements, innovations, and acquisitions to enhance their service offerings and gain sustainable competitive advantage.

- February 2024: Virgin Media O2 (VMO2) in the United Kingdom, in collaboration with its major shareholders Liberty Global and Telefonica, unveiled intentions to establish a distinct national fixed network entity, NetCo. This strategic decision is geared toward bolstering the adoption of full-fiber technology, broadening financial avenues, and potentially paving the way for mergers with other network providers. NetCo, a freshly minted entity, will operate as a wholly-owned subsidiary of Virgin Media O2, consolidating the company's cable and fiber infrastructure, which spans around 16.2 million UK premises.

- February 2024: CityFibre, the largest altnet in the United Kingdom, secured five new contracts under the country's GBP 5 billion (~USD 6.21 billion) broadband subsidy initiative, Project Gigabit. Valued at a cumulative GBP 394 million (~USD 490.04 million), these contracts aim to facilitate full-fiber deployment to 202,000 rural premises. The targeted regions include Buckinghamshire, Hertfordshire, Berkshire, Leicestershire, Warwickshire, Sussex, Kent, Bedfordshire, Northamptonshire, and Milton Keynes. Additionally, with the aid of CityFibre's funding, the company plans to not only expand but also enhance its current infrastructure in these areas, with a goal of reaching an additional 450,000 premises.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Regulatory Landscape in UK for Telecom-related Services

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Huge Demand for High-speed Connectivity

- 5.1.2 Rising Digital Transformation in the Industries

- 5.2 Market Restraints

- 5.2.1 Data Securities and Privacy Concerns

- 5.2.2 Heavy CAPEX Associated with Advanced Telecom Infrastructure

- 5.3 Insights on Key Market Indicators Related to Business Fixed Connectivity in UK

- 5.4 Analysis of Pricing for Fiber and Fixed Broadband for Businesses in UK

- 5.5 Insights on Adoption of Fixed Leased Lines by Businesses in UK

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Fixed Data

- 6.1.2 Fixed Voice

- 6.2 By Size of Enterprises

- 6.2.1 Small and Medium-sized Enterprises (SMEs)

- 6.2.2 Large Enterprises

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 TalkTalk Business Direct Limited

- 7.1.2 Sky UK

- 7.1.3 Vodafone Limited

- 7.1.4 BT Group

- 7.1.5 Virgin Media Business Ltd

- 7.1.6 bOnline Limited

- 7.1.7 KCOM Group Limited

- 7.1.8 Hyperoptic Ltd

- 7.1.9 Gigaclear Ltd

- 7.1.10 XLN Telecom Ltd

- 7.1.11 Chess Ltd

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日