|

市場調査レポート

商品コード

1550213

英国の固定接続:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)UK Fixed Connectivity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の固定接続:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

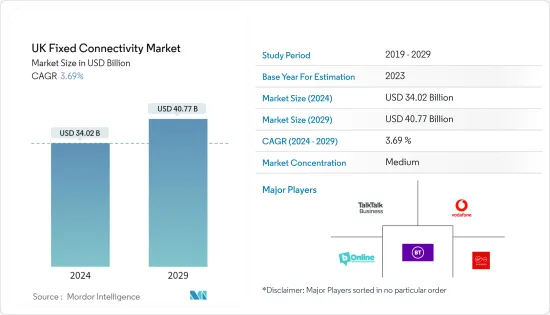

英国の固定接続市場規模は2024年に340億2,000万米ドルと推定され、2029年には407億7,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは3.69%で成長します。

主なハイライト

- 英国の固定接続市場は、デジタルトランスフォーメーション、インフラ投資、政府のイニシアチブの高まりに後押しされています。リモートワーク、オンライン教育、デジタルサービスなどの動向に後押しされ、信頼性の高い高速インターネットへのニーズが高まっており、堅牢な接続への需要が高まっています。

- 光ファイバーへの大規模な投資とギガビット対応ブロードバンドの展開は、インターネットサービスの可用性と質の両方を強化しています。プロジェクト・ギガビット」のような政府のイニシアチブは、サービスが行き届いていない地域に焦点を当て、ブロードバンドアクセスの拡大を特に目標としています。さらに、スムーズなストリーミングやスマートホーム技術の採用に対する消費者の需要が急増し、企業による安定した接続性への依存度が高まるにつれ、市場は顕著な上昇を目の当たりにしています。

- OfcomがISPの展開計画を分析したところ、市場の発展が著しく進んでいることが明らかになった。敷地内光ファイバー(FTTP)としても知られるフルファイバーカバレッジの物件数は、2023年5月の1,540万件から、2026年5月には推定2,700万件に急増し、全物件の91%を網羅することになります。物理的インフラ契約(PIA)は、ISPがオープンリーチのダクトや電柱にアクセスできるようにする、極めて重要な役割を果たします。

- このアクセス急増は、オープンリーチのインフラで運営するISPと、代替ネットワークを選択するISPとの間の選択肢を提供し、より多くの消費者に力を与えています。ハイパーオプティックのような代替ISPは、オープンリーチやヴァージン・メディアへの依存から脱却し、ファイバーネットワークを構築しつつあります。

- 市場の競合は激しく、既存プレーヤーと新興プレーヤーが混在しています。これらのプレーヤーは、競争力を強化し市場成長を促進するため、さまざまな戦略を採用しています。例えば、2024年2月、ヴァージン・メディアO2は、英国の大手プロバイダーとして住宅向け2Gbpsブロードバンド・サービスを公に導入し、顧客向けの代替アドオンとして、すべての速度層を通じて対称的なダウンロードとアップロード速度を提示しました。

- しかし、データ・セキュリティやプライバシー関連の問題に対する懸念の高まりや、高度な通信インフラに関連する多額の設備投資が、予測期間中の市場成長を抑制する要因となっています。

英国の固定接続市場の動向

デジタル変革が各業界で活発化

- 英国のデジタル変革の進展は、固定接続市場の成長を大きく後押ししています。国家がデジタル変革を受け入れるにつれ、高速で信頼性の高いインターネットへのニーズが急増。クラウドコンピューティング、リモートワーク、オンライン教育、デジタルサービスが企業や個人の定番となる中、堅牢な固定接続の重要性は最も高いです。

- ビデオ会議、ストリーミング、スマート・テクノロジーなどの高度なデジタル・アプリケーションの台頭により、安定した大容量ネットワークはますます不可欠になっています。このシフトは、光ファイバーやギガビット・ブロードバンドへの投資を加速させ、高度なデジタルサービスへの需要の高まりに対応するための接続性の強化を保証しています。その結果、固定接続インフラの全国的な強化・拡大が急がれています。

- 2024年3月、世界の共有通信インフラ・プロバイダーであるボルディン・ネットワークス(ボルディン)は、ロンドンのフルファイバー・プロバイダーであるG.Networkと戦略的提携を結びました。

- この提携は、世界のスマートシティを目指すロンドンの歩みを加速させることを目的としています。このパートナーシップは、より接続されたロンドンという統一ビジョンによって推進され、「Smarter London Together」イニシアチブを強化することを目的としています。このパートナーシップは、接続性を向上させ、都市サービスを最適化し、首都全体の持続可能な開発を促進することに重点を置いています。ボルディン・ネットワークスとのパートナーシップは、ロンドンのデジタル・トランスフォーメーションにおける極めて重要な分岐点であり、G.Networkの戦略的な動きを意味します。

- 英国ではソーシャルメディアの利用が増加しており、顧客エンゲージメントを増幅し、リアルタイムのフィードバックを可能にし、ブランド・ロイヤルティを育成することで、デジタル・トランスフォーメーションを推進しています。消費者の行動や嗜好を把握するためにデータ分析を活用し、的確なマーケティングを行うためにソーシャルメディアを活用する企業が増えています。この動向は、業務効率を高め、顧客体験を向上させることを目的とした、洗練されたデジタルツールやプラットフォームの採用を増加させています。

- ソーシャルメディアがeコマースの成長とインフルエンサーマーケティングに与える影響は、ビジネスモデルとデジタル戦略を再構築し、国のデジタル変革を加速させています。StatCounterによると、2024年5月現在、英国におけるフェイスブック全体の利用率は58.75%で、2023年12月には約56.44%だった。このようなソーシャルメディアの全体的な利用率の上昇は、国内のデジタルトランスフォーメーションの成長を促進し、市場の成長機会を大きく促進すると予想されます。

英国で高まる無線アクセスネットワーク需要

- 英国では、高速で信頼性の高いバックホールインフラに対する需要の高まりに後押しされ、無線アクセスネットワークの拡大が市場成長を後押ししています。このインフラは、無線サービスのリーチを拡大する上で極めて重要です。ワイヤレス化するデバイスの増加に伴い、頑丈な固定接続の必要性が最も重要になります。これらの接続は、無線アクセスポイントとコアネットワーク間のスムーズなデータフローを促進します。Ofcomの調査によると、2023年には英国人口の86%が固定ブロードバンド接続を利用し、91%が家庭でのインターネット接続を利用しています。

- 英国における5G技術の展開には、基地局用の堅牢な光ファイバーインフラが必要です。英国の無線アクセス・ネットワークは、モバイル機器の急速な普及、5G技術の急速な展開、リモートワークやオンライン教育ソリューションのニーズの高まりに後押しされ、力強い成長を遂げています。GSMA Intelligenceによると、2022年、英国ではモバイルデータ接続に4G技術が主に利用されていました。しかし、2030年までには5G技術が主流となり、全接続の93%を占めると予測されています。

- 同国では、モノのインターネット(IoT)やスマートシティの拡大に後押しされ、無線接続に対する需要が高まっています。政府のインフラ投資と有利な政策に支えられた電気通信事業者が、この成長を後押ししています。その結果、英国の都市部と農村部の両方で、無線ネットワークの容量、速度、信頼性が大幅に向上しています。

- 英国政府は、2030年までにすべての人口密集地域で5Gのカバレッジを確保するという目標を掲げたワイヤレスインフラ戦略を発表しました。同戦略は、将来の接続技術への投資を重視しています。同戦略は6Gに関する包括的な計画を概説しており、英国を来るべき無線技術時代の先駆者として位置づけています。最大1億英ポンド(1億3,000万米ドル)の初期資金を背景に、政府は「未来の通信」と6G技術における英国の地位を確固たるものにする国家ミッションも開始しました。

- 2024年1月、アクセス・グループの一部門であるアクセス・ホスピタリティは、英国のゲストWi-Fi、分析、マーケティング・ソリューションのプロバイダーであるワイヤレス・ソーシャルの買収を発表しました。この買収はAccess Hospitalityの広範な技術ポートフォリオを強化し、ホスピタリティ業界のあらゆる側面をカバーするITソリューションを提供します。これらのソリューションは、宿泊予約、EPoS、テーブル管理から、マーケティング、調達、施設管理、トレーニング、ホテルPMSまで多岐にわたる。

英国の固定接続業界の概要

英国の固定接続市場は、TalkTalk Business Direct Limited、Vodafone Limited、BT Groupなどの大手企業が存在するため、競争は中程度です。同市場のプレーヤーは、総合的な製品提供を強化し、持続可能な競争優位性を獲得するために、提携や製品発売などの戦略を広く採用しています。

- 2024年3月Virgin Media O2とLiberty Globalは、モバイルサービスを強化する斬新なアプローチを試みた。両社は、固定ネットワーク・インフラと先進的な4Gおよび5Gスマートポールを統合しました。このコラボレーションは、英国の様々な地域でのモバイルカバレッジの向上を目指します。

- 2024年2月ヴァージン・メディアO2は、主要株主であるリバティ・世界とテレフォニカと共同で、全国固定ネットワーク会社(NetCo)の設立を主導していました。この構想は、フルファイバーテクノロジーの導入と展開を強化し、革新的な資金調達手段を導入し、代替ネットワークプロバイダーとの合併の可能性に道を開くことを目的としています。その目的は、BTのオープンリーチに代わる強力なホールセール・プラットフォームを提供することで、同国の固定ネットワーク分野で重要な競争相手として位置づけることです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 英国の固定接続市場の洞察

- 市場概要

- 英国における通信関連サービスの規制状況

- マクロ経済シナリオの概要

- 光ファイバーインフラ開発に関する政府の取り組み

第5章 英国の固定接続市場力学

- 市場促進要因

- 高速接続に対する莫大な需要

- 産業界におけるデジタルトランスフォーメーションの高まり

- 市場抑制要因

- データの安全性とプライバシーに関する懸念

- 高度な通信インフラに伴う多額の設備投資

第6章 市場セグメンテーション

- タイプ別

- 固定データ

- 固定音声

- エンドユーザー別

- 消費者

- 企業

第7章 競合情勢

- 企業プロファイル

- TalkTalk Business Direct Limited

- Sky UK

- Vodafone Limited

- BT Group

- bOnline Limited

- Virgin Media Business Ltd

- TVNET Limited

- Eurocoms

- Full Fibre Limited

- ITS Technology Group Ltd

- RUCKUS(CommScope)

- Openreach Limited

第8章 投資分析

第9章 市場機会と今後の動向

The UK Fixed Connectivity Market size is estimated at USD 34.02 billion in 2024, and is expected to reach USD 40.77 billion by 2029, growing at a CAGR of 3.69% during the forecast period (2024-2029).

Key Highlights

- The UK's fixed connectivity market is propelled by rising digital transformation, infrastructure investments, and government initiatives. The increasing need for reliable, high-speed internet, fueled by trends like remote work, online education, and digital services, underscores the demand for robust connections.

- Substantial investments in fiber optics and the deployment of gigabit-capable broadband are bolstering both the availability and quality of internet services. Government initiatives, such as "Project Gigabit," are specifically targeting the expansion of broadband access, with a focus on underserved regions. Moreover, as consumer demands for smooth streaming and adoption of smart home technologies surge, and businesses increasingly rely on steadfast connectivity, the market is witnessing a notable upswing.

- Ofcom's analysis of ISPs' rollout plans reveals a significant surge in the market's development. The number of properties with full-fiber coverage, also known as fiber to the premises (FTTP), is set to jump from 15.4 million in May 2023 to an estimated 27.0 million by May 2026, encompassing a remarkable 91% of all the properties. Physical Infrastructure Agreements (PIAs) serve as a pivotal enabler, granting ISPs access to Openreach's ducts and poles.

- This access surge is empowering more consumers, offering them a choice between ISPs operating on Openreach's infrastructure and those opting for alternative networks. These alternatives, like Hyperoptic, are increasingly constructing their fiber networks, diverging from reliance on Openreach or Virgin Media.

- Competition in the market is intense, driven by a mix of established and emerging players. These players are adopting a range of strategies to enhance their competitive edge and fuel market growth. For instance, in February 2024, Virgin Media O2 became the major UK provider to publicly introduce a residential 2 Gbps broadband service and present symmetrical download as well as upload speeds throughout all of its speed tiers as an alternative add-on for customers.

- However, the growing concerns about data security and privacy-related issues and Heavy CAPEX associated with advanced telecom infrastructure are some factors that can restrain the market growth over the forecast period.

UK Fixed Connectivity Market Trends

Digital Transformation is Increasing Across the Industries

- The UK's escalating digital transformation significantly boosts the fixed connectivity market's growth. As the nation embraces digital change, the need for high-speed, reliable internet surges. With cloud computing, remote work, online education, and digital services becoming staples for businesses and individuals, the importance of robust fixed connections is paramount.

- Stable and high-capacity networks are becoming increasingly vital due to the rise of advanced digital applications such as video conferencing, streaming, and smart technologies. This shift is fuelling investments in fiber optics and gigabit broadband, guaranteeing enhanced connectivity to meet the rising demand for advanced digital services. Consequently, it is hastening the nationwide enhancement and expansion of fixed connectivity infrastructure.

- In March 2024, Boldyn Networks (Boldyn), a global shared communications infrastructure provider, forged a strategic partnership with G.Network, London's full-fiber provider.

- The collaboration aims to accelerate London's journey toward becoming a global smart city. The partnership, driven by a unified vision of a more connected London, aims to bolster the 'Smarter London Together' initiative. It focuses on improving connectivity, optimizing city services, and promoting sustainable development throughout the capital. The partnership with Boldyn Networks signifies a pivotal juncture in London's digital transformation and a strategic move for G.Network.

- Rising social media utilization in the United Kingdom is propelling digital transformation by amplifying customer engagement, enabling real-time feedback, and fostering brand loyalty. Businesses are increasingly utilizing social media for precise marketing, harnessing data analytics to grasp consumer behaviors and preferences. This trend is increasing the adoption of sophisticated digital tools and platforms aimed at enhancing operational efficiency and elevating customer experiences.

- Social media's impact on e-commerce growth and influencer marketing is reshaping business models and digital strategies, hastening the nation's digital transformation. According to StatCounter, as of May 2024, the overall usage of Facebook in the United Kingdom was 58.75%, whereas in December 2023, it was around 56.44%. This rise in the overall usage of social media is thus anticipated to fuel the growth of digital transformation within the country, driving market growth opportunities significantly.

The Demand for Wireless Access Networks is Rising in the United Kingdom

- The expansion of wireless access networks in the United Kingdom is propelling market growth, fueled by the rising demand for high-speed, reliable backhaul infrastructure. This infrastructure is crucial in bolstering the wireless services' reach. With an increasing number of devices going wireless, the necessity for sturdy fixed connections becomes paramount. These connections facilitate the smooth data flow between wireless access points and the core networks. According to a survey by Ofcom, in 2023, 86% of the UK population used fixed broadband connectivity, and 91% used home internet access.

- The deployment of 5G technology in the United Kingdom necessitates a robust fiber optic infrastructure for its base stations. The UK's wireless access networks are experiencing robust growth, propelled by the surge in mobile device adoption, the rapid deployment of 5G technology, and the escalating need for remote work and online education solutions. According to GSMA Intelligence, in 2022, the United Kingdom predominantly utilized 4G technology for its mobile data connections. However, by 2030, 5G technology is projected to dominate, constituting a substantial 93% of all connections.

- The country is witnessing a strong demand for wireless connectivity, propelled by the expansion of the Internet of Things (IoT) and smart cities. Telecom providers, backed by government infrastructure investments and favorable policies, propel this growth. Consequently, both urban and rural areas in the UK are witnessing a significant improvement in the capacity, speed, and reliability of wireless networks.

- The UK government unveiled its Wireless Infrastructure Strategy with a goal to ensure 5G coverage across all populated regions by 2030. The strategy emphasizes investments in future connectivity technologies. The strategy outlines a comprehensive plan for 6G, positioning the UK as a forerunner in the upcoming wireless technology era. The government, backed by an initial funding of up to GBP 100 million (USD 130 million), also initiated a national mission to solidify the UK's position in "future telecoms" and 6G technologies.

- In January 2024, Access Hospitality, a division of The Access Group, announced its acquisition of Wireless Social, the UK's provider of guest Wi-Fi, analytics, and marketing solutions. The acquisition bolstered Access Hospitality's extensive technology portfolio, offering IT solutions that cover every facet of the hospitality industry. These solutions range from guest booking, EPoS, and table management to marketing, procurement, facilities management, training, and hotel PMS.

UK Fixed Connectivity Industry Overview

The UK fixed connectivity market is moderately competitive due to the presence of significant players like TalkTalk Business Direct Limited, Vodafone Limited, and BT Group. Players in the market are widely adopting strategies such as partnerships and product launches to enhance their overall product offerings and gain sustainable competitive advantage.

- March 2024: Virgin Media O2 and Liberty Global trialed a novel approach to enhance mobile services. They integrated their fixed network infrastructure with advanced 4G and 5G smart poles. This collaboration aims to improve mobile coverage in various UK locales.

- February 2024: Virgin Media O2, in collaboration with its major shareholders, Liberty Global and Telefonica, was spearheading the formation of a national fixed network company (NetCo). This initiative aims to bolster the adoption and deployment of full-fiber technology, introduce innovative financing avenues, and pave the way for potential mergers with alternative network providers. The objective is to position it as a significant competitor in the country's fixed network sector, providing a robust wholesale platform that offers a compelling alternative to BT's Openreach.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 UK FIXED CONNECTIVITY MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Regulatory landscape in the UK for telecom-related services

- 4.3 Overview of macro-economic scenarios

- 4.4 Government initiatives related to fiber infrastructure developments

5 UK FIXED CONNECTIVITY MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Huge demand for high-speed connectivity

- 5.1.2 Rising digital transformation in the industries

- 5.2 Market Restraints

- 5.2.1 Data securities and privacy concerns

- 5.2.2 Heavy CAPEX associated with advanced telecom infrastructure

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Fixed Data

- 6.1.2 Fixed Voice

- 6.2 By End Users

- 6.2.1 Consumers

- 6.2.2 Enterprises

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 TalkTalk Business Direct Limited

- 7.1.2 Sky UK

- 7.1.3 Vodafone Limited

- 7.1.4 BT Group

- 7.1.5 bOnline Limited

- 7.1.6 Virgin Media Business Ltd

- 7.1.7 TVNET Limited

- 7.1.8 Eurocoms

- 7.1.9 Full Fibre Limited

- 7.1.10 ITS Technology Group Ltd

- 7.1.11 RUCKUS (CommScope)

- 7.1.12 Openreach Limited