|

市場調査レポート

商品コード

1549921

北米の医薬品ガラス包装:市場シェア分析、産業動向、成長予測(2024~2029年)North America Pharmaceutical Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の医薬品ガラス包装:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

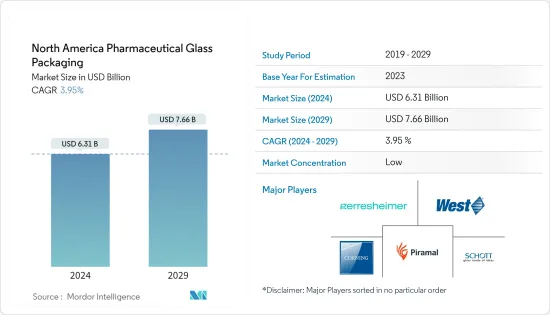

北米の医薬品ガラス包装市場規模は2024年に63億1,000万米ドルと推定・予測され、2029年には76億6,000万米ドルに達し、予測期間(2024~2029年)のCAGRは3.95%で成長すると予測されています。

米国は世界的に主要な包装市場の一つであり、多くの重要な企業が医薬品用ガラス容器を製造しています。経済が継続的に成長するにつれ、医療と医薬品に対する消費支出が増加し、ガラスパッケージングソリューションの需要を牽引しています。

主要ハイライト

- 医薬品包装用ガラスの使用量の増加は、国内で生産される医薬品の完全性と品質を向上させることを目的とした厳格な法規制の到来によるものです。製薬産業では無菌医療用包装製品に対するニーズが高まっており、予測期間中の市場拡大に拍車がかかると予想されます。

- 米国は、消費と開拓の両面で医薬品市場を独占しています。健康に特化したメディアであるSTATは、2023年までに同国の配合薬への支出は6,000億米ドルに達し、2019年の推定5,000億米ドルから大幅に増加すると予測しています。この支出の急増は、米国内の医薬品ガラス包装の需要を強化する態勢を整えています。

- 高価な医薬品の輸入に対する懸念が高まる中、米国政府は卸売業者や薬剤師がFDA認可の医薬品をカナダから輸入することを認める検査的プロジェクトを承認しました。この動きは、カナダにおけるガラス製医薬品包装の需要を間もなくエスカレートさせる構えです。

- さらに、無菌医療包装、特に製薬セクターからの急増するニーズは、予測期間中に市場の成長を強化するように設定されています。StatCanの予測によると、2024年にはカナダの医薬品・医療品製造業からの収益は99億4,000万米ドルに達する見込みです。

- しかし、医薬品のガラス包装は、輸送に役立ち、偶発的な破損の可能性を排除する低コストや軽量化などの利点により、ますますプラスチックに置き換えられています。製造コストを削減することで医薬品の三次包装を最小限に抑える必要性が、市場の成長に課題となっています。

北米医薬品ガラス包装市場の動向

予測期間中、米国が大きなシェアを占めると予測される

- 米国は世界の医薬品市場において重要な役割を担っており、医薬品用ガラス容器を専門に製造するメーカーが数多く存在します。経済の安定的な成長に伴い、消費者の医療支出が増加し、先進パッケージングソリューションへの需要が高まっている

- さらに、米国の製薬産業は最近の動向として、主に研究開発に注力することで大きな成長を遂げています。米国研究製薬工業協会(PhRMA)が強調しているように、製薬会社は収益の21%以上を研究開発に費やしています。しかし、このような取り組みにはリスクも伴う。医薬品の規制当局による承認が得られなければ、経済的に大きな打撃を受けることになりかねないからです。

- ユニセフが2023年5月に発表した報告書によると、ユニセフは麻疹、肺炎、ポリオなどの病気から子どもたちの安全を守るため、毎年20億本以上のワクチンを配布しています。これには、ユニセフが支援する国々が独自に達成できるような適切な商業条件をワクチン製造業者から得るために、その国々が必要とするワクチンを見積もり、プールすることも含まれます。このような継続的な取り組みにより、今後一定期間、市場全体でガラスバイアルとアンプルへの需要が高まると考えられます。

- 製薬産業では、がん治療、高力価医薬品(抗体結合体や速効性ステロイドなど)、注射剤の需要が急増しています。例えば、医薬品用ガラス包装の世界的大手企業であるBormioli Pharmaは、主に北米での堅調な売上に牽引され、トップラインの売上高が前年同期比40%増と著しい伸びを示しました。この成長には、特に注射剤用ガラス包装への大幅な投資と拡大が貢献しています。2023年に創業200周年を迎えるボルミオリファーマは、2025年までに医薬品包装にサステイナブル原材料を50%使用するという目標を発表しました。

- 米国国勢調査局によると、ガラスとガラス製品製造業はここ数年成長を続けています。2024年には、2014年の5億6,506万米ドルから増加し、7億583万米ドルになると予想されています。このようなガラス生産の増加は、予測期間中、国内の医薬品ガラス包装をさらに強化すると考えられます。

ガラス瓶セグメントが市場で大きなシェアを占めると予測される

- PharmaceuticalTechnologyの報告によると、米国で販売されている最も人気のある医薬品10品目のうち7品目がガラス瓶またはシリンジで包装されています。その他のガラス製医薬品には、アバスチン(20~50cc)、オプジーボ(20~50cc)、ハーセプチン(50cc)、キイトルーダ(50cc)、ヒュミラ(50cc)などがあります。シリンジもまた、大半の医薬品に一般的に使用されています。

- Corning Incorporatedは最近、ニュージャージー州で2,000 °Fの工業炉の建設を開始するため、2億400万米ドルの政府契約を獲得しました。この炉は、溶融ガラスを医療グレードの管に変え、それをワクチンの入ったバイアルに包装・梱包するものです。COVID-19のパンデミックの際、産業は8回から15回分のワクチンが入った10ミリリットルのバイアルを産業標準とすることに落ち着いた。

- さらに、消費者、立法者、顧客、メディアは包装の環境特性に絶えず注目しており、ガラスが主要な選択肢となっていることも、米国におけるガラス包装の成長を促進すると予想されます。IBMと全米小売業協会が実施した調査によると、米国とカナダの消費者の70%近くが、ブランドが持続可能か環境に優しいかどうかを重要視しています。

- さらに、医薬品包装市場では、ガラス瓶は、容器が利便性、安全性、セキュリティを提供するため、固体と液体の経口薬のアプリケーションの増加に牽引され、数量で大きなシェアを占めると予想されています。

- 製薬産業からの無菌医療用包装製品に対する需要の増加は、予測期間中の調査市場の成長をさらに促進すると考えられます。StatCan社によると、2024年には製薬・医薬品製造産業の収益は99億4,000万米ドルに達する見込みです。

北米医薬品ガラス包装産業概要

北米の医薬品ガラス包装市場は、以下のような様々な参入企業の存在によりセグメント化されています。Schott AG、Corning Incorporated、Gerresheimer AG、PGP Glass USA Inc.、West Pharmaceutical Services Inc.などの市場参入企業は、戦略的パートナーシップやコラボレーションといった新たな方法を見出し、この地域のガラス包装の開発に革新をもたらし、成長を促進しています。

- 2024年5月-米国を拠点とする注射薬管理で著名なWest Pharmaceuticals Services Inc.は、韓国のソウルに新施設を開設しました。この拡大により、倉庫の容量も増加しました。ソウルの商業の中心地に戦略的に位置するアップグレードされたオフィスは、Westが現在と将来の顧客とより密接な関係を築けるよう位置づけられています。この施設は、顧客トレーニングやセミナーから技術交流まで、さまざまなイベントを開催するための専門的なトレーニングエリアを誇っています。これらのセッションは、医薬品の安全性と包装に鋭い目を向けながら、日々進化する世界の規制状況など、極めて重要なトピックに焦点を当てます。

- 2024年3月-医薬品封じ込めソリューションの大手プロバイダーの1つであるショットAGは、米国に最初の施設を設立する予定です。この施設では、糖尿病や肥満などの疾病と闘うGLP-1療法などの治療に対応するガラス製プレフィラブルシリンジの製造が可能になります。さらに、この施設では、深冷条件を必要とするmRNA医薬品の保存と輸送に不可欠なプレフィラブルポリマーシリンジの製造にも注力します。投資額は3億7,100万米ドルで、着工は2024年後半、操業開始は2027年を予定しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 完全性と品質の向上を目的とした厳格な法規制の到来がガラス包装の需要を促進する見込み

- 無菌医療用包装の需要増加

- 市場抑制要因

- 代替製品の入手可能性

第6章 市場セグメンテーション

- 製品タイプ別

- ボトル

- バイアル

- アンプル

- カートリッジとシリンジ

- その他

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Schott AG

- Corning Incorporated

- PGP Glass USA Inc.

- West Pharmaceutical Services Inc.

- Gerresheimer AG

- Bormioli Pharma SpA

- Berlin Packaging

- Stoelzle Glass Group

第8章 投資分析

第9章 市場の将来展望

The North America Pharmaceutical Glass Packaging Market size is estimated at USD 6.31 billion in 2024, and is expected to reach USD 7.66 billion by 2029, growing at a CAGR of 3.95% during the forecast period (2024-2029).

The United States is one of the major packaging markets globally, and many vital players produce glass containers for pharmaceuticals. As the economy continuously grows, increasing consumer spending on healthcare and medicines drives the demand for glass packaging solutions.

Key Highlights

- The rise in the usage of glass for pharmaceutical packaging is attributed to the advent of strict legislation designed to improve the integrity and quality of pharmaceuticals produced domestically. The pharmaceutical industry's growing need for sterile medical packaging products is anticipated to fuel the market's expansion during the forecast period.

- The United States is a dominant force in the pharmaceutical market in both consumption and development. STAT, a health-focused media outlet, projected that by 2023, the nation's spending on prescription drugs would reach USD 600 billion, a significant increase from the estimated USD 500 billion in 2019. This surge in spending is poised to bolster the demand for pharmaceutical glass packaging within the United States.

- Amid rising concerns over costly pharmaceutical imports, the US government authorized a pilot project allowing wholesalers and pharmacists to import FDA-approved medicines from Canada. This move is poised to escalate the demand for glass pharmaceutical packaging in Canada shortly.

- Moreover, the surging need for sterile medical packaging, particularly from the pharmaceutical sector, is set to bolster the market's growth during the forecast period. According to the projections from StatCan, in 2024, the revenue from Canada's pharmaceutical and medicine manufacturing industry is expected to reach USD 9.94 billion.

- However, pharmaceutical glass packaging is increasingly substituted by plastic due to benefits like low cost and lightweight, which help in transportation and negate chances of accidental breakages. The need to minimize tertiary packaging of pharmaceutical products by reducing manufacturing costs is challenging the market's growth.

North America Pharmaceutical Glass Packaging Market Trends

The United States is Anticipated to have a Significant Share During the Forecast Period

- The United States is a critical player in the global pharmaceutical market, boasting a robust cadre of manufacturers specializing in glass containers for pharmaceuticals. With the economy's steady growth trajectory, heightened consumer healthcare spending propels the demand for advanced glass packaging solutions.

- Moreover, the US pharmaceutical sector has witnessed significant expansion in recent decades, primarily fueled by a heightened focus on research and development. Pharmaceutical firms channel over 21% of their revenues into R&D efforts, a figure the Pharmaceutical Research and Manufacturers of America (PhRMA) underscored. This commitment, however, comes with risks, as a failure to secure regulatory approval for a drug can result in substantial financial setbacks.

- According to a report published by UNICEF in May 2023, UNICEF distributes more than 2 billion vaccines every year to help keep children safe from diseases like measles, pneumonia, and poliomyelitis. This includes estimating and pooling vaccine needs from countries it supports to obtain adequate commercial terms from vaccine manufacturers that those countries could achieve independently. Such continued initiatives would bolster the demand for glass vials and ampules across the market in the upcoming period.

- The pharmaceutical industry is witnessing a surge in demand for oncology drugs, high-potency medications (like antibody conjugates and fast-acting steroids), and injectables. For instance, Bormioli Pharma, a leading global player in pharmaceutical glass packaging, saw a remarkable 40% Y-o-Y growth in its top-line revenue, primarily driven by solid sales in North America. This growth was further fueled by the company's significant investments and expansions in glass packaging, particularly for injectable drugs. In a notable move, marking its 200th anniversary in 2023, Bormioli Pharma unveiled its aim to incorporate 50% sustainable raw materials in its pharmaceutical packaging by 2025.

- According to the US Census Bureau, glass and glass product manufacturing has been witnessing growth over the last few years. In 2024, it is expected to be valued at USD 705.83 million, an increase from USD 565.06 million in 2014. Such an increase in glass production would further leverage the pharmaceutical glass packaging in the country during the forecast period.

The Glass Bottle Segment is Anticipated to Hold a Significant Share in the Market

- Glass packaging is widely utilized across the United States, with seven of the ten most popular drugs for sale in the country being packaged in glass bottles or syringes, as reported by PharmaceuticalTechnology. Other drugs packaged in glass include Avastin (20 to 50 cc), Opdivo (20 to 50 cc), Herceptin (50 cc), Keytruda (50 cc), and Humira (50 cc). Syringes are also commonly used for the majority of drugs.

- Corning Incorporated was recently awarded a government contract of USD 204 million to commence the construction of an industrial furnace at a temperature of 2,000 °F in New Jersey. The furnace will transform molten glass into a medical-grade tube, which will then be packaged and packaged into vials, each containing a vaccine. During the COVID-19 pandemic, the industry settled on a 10-milliliter vial containing between eight and fifteen vaccine doses as the industry standard.

- In addition, consumers, legislators, customers, and the media have been continuously focusing on the environmental characteristics of packaging, and glass is the primary choice, which is also expected to fuel the growth of glass packaging in the United States. According to a study conducted by IBM and the National Retail Federation, nearly 70% of consumers in the United States and Canada consider it important that a brand is sustainable or eco-friendly.

- Moreover, in the pharmaceutical packaging market, glass bottles are anticipated to occupy a significant share by volume, driven by the increasing number of applications in solid and liquid oral medications, as the containers provide convenience, safety, and security.

- The increasing demand for sterile medical packaging products from pharmaceutical industries would further drive the growth of the studied market during the forecast period. According to StatCan, in 2024, the pharmaceutical and medicine manufacturing industry revenue is expected to reach USD 9.94 billion.

North America Pharmaceutical Glass Packaging Industry Overview

The North American pharmaceutical glass packaging market is fragmented due to the presence of various players such as Schott AG, Corning Incorporated, Gerresheimer AG, PGP Glass USA Inc., and West Pharmaceutical Services Inc. Market players are finding new ways, such as strategic partnerships or collaborations, to innovate the development of glass packaging in the region, fostering growth.

- May 2024 - West Pharmaceuticals Services Inc., a prominent player in injectable drug administration based in the United States, inaugurated a new facility in Seoul, South Korea. This expansion also saw an increase in their warehouse capacity. The upgraded office, strategically located in Seoul's commercial hub, positions West to engage more closely with its current and prospective clients. The facility boasts a specialized training area to host various events, from customer training and seminars to technical exchanges. These sessions will focus on pivotal topics, including the ever-evolving global regulatory landscape, with a keen eye on drug safety and packaging.

- March 2024 - SCHOTT AG, one of the leading providers of pharmaceutical containment solutions, is set to establish its inaugural facility in the United States. The site will be able to manufacture glass pre-fillable syringes, catering to treatments like GLP-1 therapies, which combat ailments such as diabetes and obesity. Additionally, the facility will focus on producing pre-fillable polymer syringes, which are crucial for storing and transporting mRNA drugs that require deep-cold conditions. The venture commands a substantial investment of USD 371 million, with groundbreaking slated for late 2024 and operations expected to commence in 2027.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Advent of Strict Legislation Designed to Improve Integrity and Quality is Expected to Fuel the Demand for Glass Packaging

- 5.1.2 Increasing Demand for Sterile Medical Packaging

- 5.2 Market Restraints

- 5.2.1 Availability of Substitute Products

6 MARKET SEGMENTATION

- 6.1 By Product Types

- 6.1.1 Bottles

- 6.1.2 Vials

- 6.1.3 Ampoules

- 6.1.4 Cartridges and Syringes

- 6.1.5 Other Products

- 6.2 By Country

- 6.2.1 United States

- 6.2.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schott AG

- 7.1.2 Corning Incorporated

- 7.1.3 PGP Glass USA Inc.

- 7.1.4 West Pharmaceutical Services Inc.

- 7.1.5 Gerresheimer AG

- 7.1.6 Bormioli Pharma SpA

- 7.1.7 Berlin Packaging

- 7.1.8 Stoelzle Glass Group