|

市場調査レポート

商品コード

1549910

欧州の金属包装:市場シェア分析、産業動向、成長予測(2024~2029年)Europe Metal Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の金属包装:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 124 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

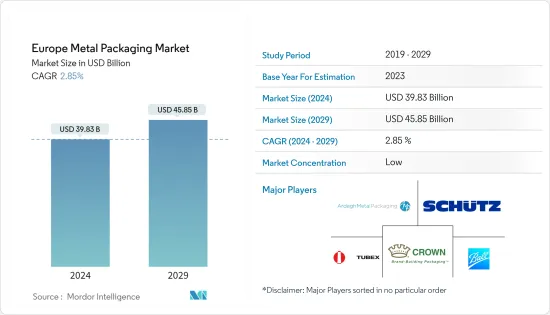

欧州の金属包装市場規模は2024年に398億3,000万米ドルと推定され、2029年には458億5,000万米ドルに達し、市場推定・予測期間(2024~2029年)のCAGRは2.85%で成長すると予測されています。

金属包装は、消費者だけでなく製品メーカーをも魅了する循環型経済に最も適していると考えられてきました。金属包装ソリューションは、小売、卸売、工業、商業を含むあらゆるセグメントで応用されています。持続可能性と安全性が実証された金属包装ソリューションは、ブランドオーナーや充填業者にとって賢明なソリューションと考えられています。

金属包装が提供するリサイクル性の利点は、何度リサイクルを試みても材料の特性が変化しないため、市場の成長に寄与します。これは金属包装に他の包装材料に対する競争優位性を与えています。金属包装は欧州で最もリサイクルされている包装です。金属・包装・欧州によると、欧州諸国で最もリサイクル率が高く、アルミ缶は約75%、スチール包装は約83%を占めています。

金属・包装・欧州によると、欧州の国民は毎週約4ユニットの金属包装ソリューションを消費しています。先進技術の利用は技術革新とともに新製品の発売をもたらし、この地域の市場成長をもたらしています。

塗料やワニスのようなバルク材料の取引の増加は、輸送用バレルやドラム、バルクコンテナを含む金属包装ソリューションの需要を牽引しています。化学品やその他の危険物を含むドラム缶や容器をトレースするためのQRコードなどの先進包装の利用は、金属包装メーカーが競合の一歩先を行くのに大いに役立っています。例えば、ドイツのヘッドタイトドラム専門メーカーであるDuttenhofer社は、ここ2、3年の間に統合技術に投資することで、化学品を含むドラム缶のトレーサビリティを導入しました。QRコードはドラム缶に貼られたラベルに印刷され、ドラム缶のメーカーやシリアル番号などの情報が記載されています。

金属包装はさまざまな技術に対応できるため、魅力的な包装製品を求めるブランドオーナーの間で人気があります。デジタル印刷、エンボス加工、デボス加工技術は、金属の視覚的なアピールを作成するために使用されます。人目を引く金属包装ソリューションは、ブランドが小売ディスプレイ包装で優位に立つのに役立ち、店頭で消費者の関心を集めています。

さらに、スチールやアルミニウムの価格変動は、最終製品の価格上昇につながるため、金属包装メーカーにとって障害となる可能性があります。金属包装ラインを設置するための高い投資コストは、中小規模の包装メーカーにとって成長の障壁となる可能性があります。

欧州金属包装市場の動向

欧州諸国におけるワイン消費の増加が金属製栓の売上を牽引すると予想される

- ワイン産業では風味と香りが重視されます。ワインの鮮度と品質をより長く保ちたいという願望が、ワインボトル用金属栓の売上を牽引する主要要因です。金属製キャップは非常に効果的なバリアを作り、内容物の汚染や湿気を防ぐのに役立ちます。また、金属・栓が提供する費用対効果とリサイクル性の利点により、ワイン・ボトルに理想的な選択肢となっています。Aluminium Closures Group(AMS Europe eVの一部)の調査によると、欧州で消費されるアルミ製キャップ10個のうち4個がリサイクルされています。

- ワインメーカーや包装業者は、ブドウ畑から使用後のリサイクル工程に至るまで、環境への影響を重視しており、金属製栓のメーカーに競争上の優位性を与えています。アルミ製栓の環境負荷は、他の栓に比べて低いです。ライフサイクルアセスメント(LCA)によると、アルミ製栓の方が環境性能が高く、コルク栓によるボトルワインの無駄を2~5%削減できます。また、アルミ製栓は大量に製造されるため、費用対効果も高いです。アルミ製キャップは世界中で製造されており、現地のバリューチェーンの一部となっています。経済的に輸送できるため、最終用途産業のニーズに即座に対応できます。

- 様々なタイプの金属製キャップが利用可能なため、様々な種類のワインの密封に関する懸念に対応できます。スクリューキャップは、使いやすさとワインの品質を保つ能力から、ワインボトルの密封に最もよく使われる金属製キャップです。スクリューキャップは、酸素の侵入を防ぐだけでなく、ボトルを気密に密閉するのに役立ちます。これに加えて、スクリュー・キャップは開栓も再封も簡単で、消費者にとって便利な選択となっています。クラウンキャップは、スパークリングワインに特別に使用され、製品に確実な密閉を記載しています。

- 金属・栓・メーカーによるイノベーションは、ワインメーカーやワイン包装業者の間で支持を集めています。例えば、Guala Closures Groupは、ワイン市場向けのコネクテッド栓、NeSTGATETMを提供しています。この栓はシングルチップNFCを搭載しており、製品の不正開封を検知するのに役立ちます。同社は、技術革新を適応させることで、スピリッツとワインの生産者を支援するというコミットメントを続けています。

- COVID-19の大流行中、バーやレストランの閉店によりワインの消費量は減少しました。しかし、ワインの小売販売は安定していたため、欧州におけるワイン用アルミ製栓のシェアは2%増加しました。これに加え、欧州連合(EU)はフランスで余剰ワインの破棄を開始したため、ワイン包装に使用される金属製栓の成長が妨げられる可能性があります。

- 欧州諸国におけるワインの消費量と生産量は他国に比べて高いです。国際ブドウ・ワイン機構(International Organization of Vine and Wine)が発表した報告書によると、2023年の世界のワイン生産量の約61%を欧州が占めています。ワインの生産量はフランスが多く、イタリア、スペイン、ドイツ、ポルトガル、その他の欧州諸国がそれに続きます。したがって、この地域でのワイン生産と消費の増加は、金属製栓の需要を急増させると予想されます。

英国における化粧品中小企業の増加が金属製包装の需要を押し上げる

- 英国の化粧品産業におけるエアロゾルディスペンサーの需要の高まりは、金属包装の需要の高まりを反映しています。化粧品・パーソナルケア産業で使用されるエアロゾル容器は、ほとんどがスチールやアルミニウム製です。消臭剤やスプレーは、簡単に吐出できるようにエアロゾル容器に詰められています。

- エアロゾル容器は密閉されているため、化粧品やパーソナルケア製品の主要消費者であるZ世代が懸念している液漏れの可能性を減らすことができます。エアロゾル・ディスペンサーを使用すれば、製品の大小を問わず、どんな場所にも簡単に塗布できるため、さまざまな化粧品やパーソナル・ケア製品に理想的な選択肢となります。また、日焼け止めの塗布など、エアロゾル・ディスペンサーの用途が産業で増えています。

- 英国は欧州諸国の中で4番目に大きな化粧品・パーソナルケア市場であり、ドイツ、フランス、イタリアがそれに続きます。このほか、英国では化粧品・パーソナルケアの中小企業の数が増加しています。コスメティック・トイレタリー・パフューマリー協会(CTPA)のデータによると、化粧品・パーソナルケアの中小企業数では英国が第1位で、フランス、ポーランド、イタリアがこれに続きます。このことは、化粧品・パーソナルケア産業向け金属包装市場の成長を助けると予想されます。

- 化粧品・パーソナルケア中小企業の増加に伴い、英国のエアロゾル生産量も高いです。最近、英国は欧州のエアロゾル生産量14億3,600万個の約27%を占めている(供給源-FEA)。化粧品とパーソナルケアはエアロゾル容器の主要最終用途であり、欧州のエアロゾル生産量の約55%を占める。国内で原料が入手可能なため、金属包装メーカーには輸入原料のコスト削減という利点があります。

- 英国におけるプラスチック包装税の採用は、リサイクル可能な金属包装ソリューションの成長機会を生み出す可能性があります。また、持続可能性目標の達成に重点を置く化粧品ブランドは、製品包装にリサイクル可能で無害な材料をより重視すると考えられます。これにより、英国の化粧品・パーソナルケア産業における金属包装の販売が促進される可能性があります。

欧州金属包装産業概要

欧州の金属包装市場は、Ardagh Metal Packaging SA(Ardagh Group)、Ball Corporation、Crown Holdings Inc.、TUBEX Packaging GmbH、Schutz GmbH &Co.KGaA、Silgan Holdings Inc.などです。市場の主要企業は、缶のような金属包装製品のための先進的な印刷とデザイン技術を使用して競争優位性を得ることに集中しようとしています。また、エンドユーザーブランドや環境意識の高い顧客の間で金属包装の需要が高まっていることから、各社は存在感と顧客基盤を拡大するために買収戦略を採用しています。

2024年2月、Ardagh Metal Packaging SAはBritvic Soft Drinksとの協業により、新製品Tango Mangoのハイエンドで革新的な缶デザインを発表しました。ハイエンドで人目を引くデザインの缶は、同ブランドが顧客の注目を集めるのに一役買う可能性があります。

2023年10月、Crown Holdings Inc.は、ドイツにあるHelvetia Packaging AGの飲料用缶・エンド製造施設の買収を発表しました。この買収は、同社の欧州飲料缶プラットフォームをドイツに拡大することを目的としたもので、年間約10億個の缶生産能力を持っています。この買収により、同社は、アルコール飲料やノンアルコール飲料のセグメントで、地元や地域の顧客の間で高まる飲料缶への嗜好に応えることができると期待されています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 地政学的シナリオが市場に与える影響

第5章 市場力学

- 市場促進要因

- 欧州諸国におけるワインの高い生産量と消費量が金属製栓の売上を牽引すると予想される

- 英国における化粧品中小企業の増加が金属製包装の需要を押し上げる

- 市場抑制要因

- 金属包装ライン設置のための高い投資コストが中小規模包装メーカーの障壁となる可能性

第6章 市場セグメンテーション

- 材料タイプ別

- アルミニウム

- スチール

- 製品タイプ別

- 缶

- 食品缶

- 飲料缶

- エアロゾル缶

- バルク容器

- 輸送用バレルとドラム

- キャップと栓

- その他の製品タイプ(チューブなど)

- 缶

- エンドユーザー産業別

- 飲料

- 食品

- 化粧品・パーソナルケア

- 家庭用

- 塗料・ワニス

- その他のエンドユーザー産業(自動車、工業)

- 国別

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

第7章 競合情勢

- 企業プロファイル

- Ardagh Metal Packaging SA(Ardagh Group)

- Ball Corporation

- Crown Holdings Inc.

- CANPACK SA(CANPACK Group)

- Silgan Holdings Inc.

- Greif Inc.

- TUBEX Packaging GmbH

- Mauser Packaging Solutions

- Colep Packaging(RAR Group Company)

- Schutz GmbH & Co. KGaA

第8章 投資分析

第9章 市場の将来

The Europe Metal Packaging Market size is estimated at USD 39.83 billion in 2024, and is expected to reach USD 45.85 billion by 2029, growing at a CAGR of 2.85% during the forecast period (2024-2029).

Metal packaging has been considered the best fit for a circular economy that attracts consumers as well as product manufacturers. Metal packaging solutions have applications in all fields, including retail, wholesale, industrial, and commercial. With a proven sustainability and safety record, metal packaging solutions are considered a smart solution for brand owners and fillers.

The recyclability benefit offered by metal packaging contributes to market growth as the properties of the material do not change even after multiple recycling attempts. This gives metal packaging a competitive advantage over other packaging materials. Metal packaging is the most recycled packaging in Europe. It has the highest recycling rate in European countries, according to Metal Packaging Europe, with aluminum cans accounting for around 75% and steel packaging around 83%.

According to Metal Packaging Europe, every European citizen consumes around 4 units of metal packaging solution weekly. The use of advanced technology, along with innovation, results in new product launches, providing market growth in the region.

The increase in the trade of bulk materials such as paints and varnishes drives the demand for metal packaging solutions, including shipping barrels and drums and bulk containers. The use of advanced technologies, such as QR codes, for tracing the drums or containers containing chemical and other hazardous products is significantly helping metal packaging manufacturers to stay ahead of the competition. For instance, Duttenhofer, a German head-tight drum specialist, introduced traceability for drums containing chemicals by investing in integrated technology over the past couple of years. The QR code is printed on a label applied to the drum, containing information about the drum manufacturer, serial number, and others.

The ability of metal packaging to adhere to different technologies makes it popular among brand owners who are looking for appealing packaging products. Digital printing, embossing, and debossing technologies are used to create a visual appeal of the metal. The eye-catching metal packaging solutions help the brand gain an advantage in retail display packaging, gaining consumer attraction in the store.

Moreover, the fluctuating prices of steel and aluminum may create an obstacle for metal packaging manufacturers as this results in the increased prices of the final product. The high investment cost of setting up the metal packaging line may create a growth barrier for small and medium-scale packaging manufacturers.

Europe Metal Packaging Market Trends

Increased Wine Consumption in European Countries is Expected to Drive the Sales of Metal Closures

- Flavor and aroma are the major aspects focused upon in the wine industry. The urge to preserve the freshness and quality of wine for a longer period is the major factor driving the sales of metal closures for wine bottles. Metal closures create a highly effective barrier that helps prevent the content from contamination and moisture. Also, the cost-effective and recyclability benefit offered by metal closures makes it an ideal choice for wine bottles. As per the study provided by Aluminium Closures Group (part of AMS Europe eV), four out of ten aluminum closures consumed in Europe are recycled.

- The winemakers and packers focus on the environmental impact, starting from the vineyard to the recycling process after use, giving the metal closure manufacturers a competitive advantage. Aluminum closures have a low environmental impact compared to other closure types. According to the Life Cycle Assessment (LCA), aluminum closures have better environmental performance and reduce the instances of bottled wine wastage due to corkage by 2% to 5%. Also, the aluminum closures are manufactured in bulk, which adds to the cost-benefit. The aluminum closures are made across the world and are a part of the local value chain. This helps in immediate reaction to the end-use industry needs as it can be transported economically.

- The availability of different types of metal closures helps to address the sealing concern for different types of wine. The screw caps are the most common metal closures used for sealing wine bottles due to the ease of use and the ability to preserve the quality of wine. Screw caps help in preventing the oxygen from entering the bottle as well as provide airtight sealing to it. In addition to this, it is also easy to open and reseal the bottle using a screw cap, which makes it a convenient choice for consumers. The crown caps are specially used for sparkling wines to provide a secure seal to the product.

- The innovations by metal closure manufacturers are gaining traction among winemakers and wine packers. For instance, Guala Closures Group offers NeSTGATETM, a range of connected closures for the wine market. The closure is equipped with a single-chip NFC, which will help detect unauthorized openings of the product. The company continues its commitment to supporting spirit and wine producers by adapting technological innovation.

- During the COVID-19 pandemic, wine consumption decreased due to the closure of bars and restaurants. However, the share of aluminum closures for wine in Europe increased by 2% as the retail sales of wine remained stable. Besides this, the European Union has initiated destroying the wine surplus in France, which may hamper the growth of metal closures used for wine packaging.

- Wine consumption and production in the European countries is high compared to other countries. Europe accounted for around 61% of the wine production in the world for the year 2023, according to the report presented by the International Organization of Vine and Wine. Wine production is high in France, followed by Italy, Spain, Germany, Portugal, and other European Countries. Therefore, the increased wine production and consumption in the region is expected to surge the demand for metal closures.

Increasing Cosmetic SMEs in the United Kingdom to Push the Demand for Metal Packaging

- The rising demand for aerosol dispensers in the cosmetic industry in the United Kingdom reflects the rise in demand for metal packaging. The aerosol containers used in the cosmetic and personal care industry are mostly made from steel and aluminum. The deodorants and sprays are packed in aerosol containers for ease of dispense.

- The aerosol containers are hermetically sealed, reducing the chances of leakage, which is a major concern for Gen Z, who are the major consumers of cosmetics and personal care products. The product can be easily applied to any large or small area using aerosol dispensers, which makes it an ideal choice for various cosmetics and personal care products. Also, the application of aerosol dispensers, such as sunscreen application, is increasing in the industry.

- The United Kingdom is the fourth-largest cosmetic and personal care market in the European countries, followed by Germany, France, and Italy. Besides this, the number of cosmetics and personal care SMEs is rising in the United Kingdom. The United Kingdom ranks first in terms of the number of cosmetics and personal care SMEs, followed by France, Poland, and Italy, according to data from the Cosmetic, Toiletry and Perfumery Association (CTPA). This is expected to aid the growth of the metal packaging market for the cosmetic and personal care industry.

- With the rising number of cosmetic and personal care SMEs, aerosol production in the United Kingdom is also high. Recently, the United Kingdom accounted for around 27% of the total aerosol production in Europe, which is 1,436 million units (Source - FEA). Cosmetics and personal care are the major end-use applications for aerosol containers, representing around 55% of European aerosol production. The availability of raw materials in the country provides added benefits to metal packaging manufacturers, resulting in reduced costs for imported materials.

- The introduction of the Plastic Packaging Tax in the United Kingdom may create growth opportunities for recyclable metal packaging solutions. Also, cosmetics brands that are focusing on achieving sustainability targets will focus more on recyclable and harmless materials for product packaging. This may push the sales of metal packaging in the cosmetic and personal care industry in the United Kingdom.

Europe Metal Packaging Industry Overview

The European metal packaging market is fragmented with the presence of various global and local players in the market, including Ardagh Metal Packaging SA (Ardagh Group), Ball Corporation, Crown Holdings Inc., TUBEX Packaging GmbH, Schutz GmbH & Co. KGaA, and Silgan Holdings Inc. The key players in the market are trying to focus on gaining a competitive advantage using advanced print and design technologies for metal packaging products such as cans. Also, the players are adopting an acquisition strategy to increase their presence and customer base with the rising demand for metal packaging among end-user brands and environmentally conscious customers.

In February 2024, Ardagh Metal Packaging SA announced its collaboration with Britvic Soft Drinks to launch the high-end innovative can design for the new Tango Mango product. The high-end, eye-catching design of the can may help the brand gain customers' attention.

In October 2023, Crown Holdings Inc. announced the acquisition of a beverage can and end manufacturing facility of Helvetia Packaging AG, located in Germany. The acquisition was aimed at expanding the company's European beverage can platform to Germany, with an annual can capacity of approximately one billion units. This acquisition was expected to help the company meet the increasing preference for beverage cans among local and regional customers for alcoholic and non-alcoholic drinks segments.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Geopolitical Scenario on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Wine Production and Consumption in European Countries is Expected to Drive the Sales of Metal Closures

- 5.1.2 Increasing Cosmetic SMEs in the United Kingdom to Push the Demand for Metal Packaging

- 5.2 Market Restraints

- 5.2.1 The High Investment Cost of Setting up the Metal Packaging Line May Create a Barrier for Small and Medium-scale Packaging Manufacturers

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminium

- 6.1.2 Steel

- 6.2 By Product Type

- 6.2.1 Cans

- 6.2.1.1 Food Cans

- 6.2.1.2 Beverage Cans

- 6.2.1.3 Aerosol Cans

- 6.2.2 Bulk Containers

- 6.2.3 Shipping Barrels and Drums

- 6.2.4 Caps and Closures

- 6.2.5 Other Product Type (Tubes, etc.)

- 6.2.1 Cans

- 6.3 By End-user Industry

- 6.3.1 Beverage

- 6.3.2 Food

- 6.3.3 Cosmetics and Personal Care

- 6.3.4 Household

- 6.3.5 Paints and Varnishes

- 6.3.6 Other End-user Industries (Automotive and Industrial)

- 6.4 By Country

- 6.4.1 United Kingdom

- 6.4.2 Germany

- 6.4.3 France

- 6.4.4 Spain

- 6.4.5 Italy

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Ardagh Metal Packaging SA (Ardagh Group)

- 7.1.2 Ball Corporation

- 7.1.3 Crown Holdings Inc.

- 7.1.4 CANPACK SA (CANPACK Group)

- 7.1.5 Silgan Holdings Inc.

- 7.1.6 Greif Inc.

- 7.1.7 TUBEX Packaging GmbH

- 7.1.8 Mauser Packaging Solutions

- 7.1.9 Colep Packaging (RAR Group Company)

- 7.1.10 Schutz GmbH & Co. KGaA