アジア太平洋地域のデータセンターフィジカルセキュリティ:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

Asia-Pacific Data Center Physical Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549908

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

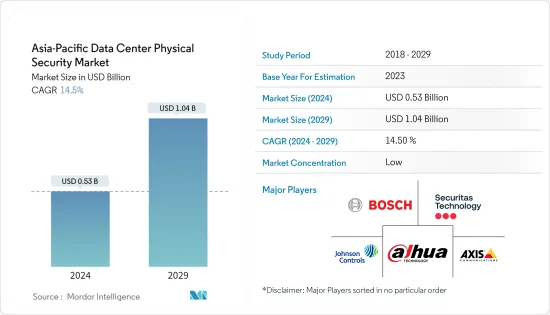

アジア太平洋地域のデータセンターフィジカルセキュリティ市場規模は、2024年に5億3,000万米ドルと推定され、2029年には10億4,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは14.5%で成長すると予測されます。

データセンターのセキュリティは、境界セキュリティ、施設管理、コンピュータルーム管理、キャビネット管理の4層アプローチを採用しています。第1層の境界セキュリティは、不正侵入者の抑止と検知に重点を置き、潜在的な侵入を遅らせることを目的としています。万が一侵入された場合は、カード・スワイプや生体認証のようなアクセス・コントロール・システムを採用する第2層が、それ以上のアクセスを制限します。第3のレイヤーは、制限区域の監視、改札口、VCA、指紋、虹彩、血管パターンの生体認証アクセス・コントロール、無線周波数識別など、さまざまな検証方法で物理的セキュリティを強化します。これらの層は主に許可された人員に焦点を当てていますが、追加の層であるキャビネットロック機構は、悪意のある従業員などの内部脅威の懸念に対応しています。

主なハイライト

- アジア太平洋地域のデータセンター建設市場における今後のIT負荷容量は、2029年までに2万3,000万kWに達すると予想されます。

- 同地域の床面積は、2029年までに7,450万平方フィート増加すると予想されます。

- 同地域で設置されるラックの総数は、2029年までに420万ユニットに達する見込みです。2029年までに最大数のラックが設置されると予想されるのはインドです。

- アジア太平洋地域を結ぶ海底ケーブルシステムは160近くあり、その多くが建設中です。2024年にサービス開始が予定されているそのような海底ケーブルの1つが、東南アジア-日本ケーブル2(SJC2)で、中国、台湾、日本、韓国、タイ、ベトナムを陸揚げ点とする10,500km以上に及ぶ。

アジア太平洋地域のデータセンターフィジカルセキュリティ市場動向

IT・通信分野が大きなシェアを占める見込み

- アジア太平洋地域では、ハイパーコネクティビティ環境が、消費者や企業のコネクティビティやコラボレーションのニーズをサポートする上で基礎的な役割を果たす通信事業者の重要性を高めています。アジア太平洋地域全体では、通信事業者の75%がプラスの収益成長を記録しました。韓国は、通信市場成熟度の世界ランキングで香港に次いで2位です。

- 韓国は6Gを含む最新の通信技術開発の最先端にあります。投資の面では、2022年11月、マレーシアの通信会社CelcomとDiGiが合併契約を承認しました。両社が完全に合併すれば、新会社は2,000万人以上の加入者を抱えるマレーシア最大級の通信事業者となります。

- オーストラリアは主要都市に5Gを配備し、より多くのサービスを提供するために周波数帯のオークションを進めています。2021年4月、政府はハイバンド5G周波数帯(26GHz帯)を割り当て、超高速・大容量サービスが可能になります。2021年後半には、政府は低帯域の5G周波数帯(850/900 MHz帯)を割り当てた。これにより、企業市場における5Gの新たな応用が可能になり、データトラフィックとデータセンター需要の大幅な増加につながります。これにより、物理的なセキュリティ需要が大幅に増加します。

- アジア太平洋地域における5Gの登場は、高速ネットワーク接続のためのスモールセル展開を加速させています。多くの国が、新しいスモールセルを展開する際に適用できる免責基準を策定しています。例えばシンガポールでは、情報通信メディア開発庁(IMDA)がビル開発者や所有者に対し、通信プロバイダーが通信機器用に屋上スペースを無償で提供するよう指示しています。

- 中国政府は市場の需要に応えるため、データセンターの物理的セキュリティ・ソリューションの改善に注力しています。中国政府は2025年までに8つのコンピューティング・ハブと10のデータセンター・クラスターを建設し、統一データセンター・システムを構築する計画です。このプロジェクトは、東部から増加する需要を西部地域のデータセンターに振り向けることを目的としています。

著しい成長が期待される中国

- 中国政府は市場の需要に応えるため、データセンターフィジカルセキュリティ・ソリューションの改善に注力しています。中国政府は、2025年までに8つのコンピューティング・ハブと10のデータセンター・クラスターを建設し、統一データセンター・システムを構築する計画です。このプロジェクトは、東部からの増大する需要を西部地域のデータセンターに振り向けることを目的としています。

- 多くの企業がデータセンターの拡張に絶えず投資しており、データセンター・アプリケーションの市場機会を生み出すことになります。例えばGLP Pteは、デジタルインフラ資産に対する投資家の需要が高まる中、中国におけるデータセンター・プラットフォームの拡大を支援するため、2022年2月に5億米ドルの新規資金を調達しました。同社によると、この取引によって中国のデータセンターの価値は40億米ドルから50億米ドルに達する可能性があるといいます。このような投資は市場を前進させると思われます。

- クラウド・コンピューティングはウェブベースのインフラを提供し、追加コンピューティングや情報ストレージなどのサービスをクライアントに提供します。クラウド・インフラストラクチャは、データセンター内に大規模なサーバー・ファームやストレージ・システムを配置する従来のシステムよりも比較的安価です。このような要因は、クラウド・データセンターの大規模な建設と関連しており、物理的なセキュリティ・ソリューションの需要に対応しています。

- 中国政府は、第5世代モバイル通信技術とインターネット・データセンターの可能性を活用したeコマース部門の繁栄に力を入れており、その結果、IDCは業界の利害関係者にとって実行可能な投資を可能にしています。さらに、この動向はTencent HoldingsやHuawei Technologiesのような強豪企業の台頭によって支えられており、その成長がこの地域におけるIDC施設の建設を後押しし、ビデオ監視や入退室管理ソリューションの大きな需要につながっています。

アジア太平洋地域のデータセンターフィジカルセキュリティ産業の概要

アジア太平洋地域のデータセンターフィジカルセキュリティ市場は、Axis Communications AB、ABB Ltd、Bosch Sicherheitssysteme GmbHのようなプレーヤーが、企業の能力向上に重要な役割を果たしているため、非常に断片化されています。市場志向は高度な競合環境につながります。圧倒的な市場シェアを持つこれらの大手企業は、地域全体の顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために、戦略的協業イニシアティブを活用しています。

2023年4月:シュナイダーエレクトリックは、新しいサービス「EcoCare for Modular Data Centers」の会員サービスを開始しました。この革新的なサービスプランの会員は、24時間365日のプロアクティブな遠隔監視と状態ベースのメンテナンスにより、モジュラー型データセンターの稼働時間を最大化するための専門知識を利用できます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ハイパースケールおよびコロケーション事業者によるデータセンター活動と投資の増加

- クラウドシステムに接続されたビデオ監視システムの進歩

- 市場抑制要因

- 運用と投資収益率に関する懸念

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- ソリューションタイプ別

- ビデオ監視

- 入退室管理ソリューション

- その他のソリューションタイプ(マントラップ、フェンス、モニタリングソリューション)

- サービスタイプ別

- コンサルティング・サービス

- プロフェッショナルサービス

- その他のサービスタイプ(システム・インテグレーション・サービス)

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- ヘルスケア

- その他のエンドユーザー

- 国名

- インドネシア

- インド

- 中国

- オーストラリア

- 韓国

- フィリピン

- タイ

- シンガポール

- ニュージーランド

- 日本

- マレーシア

- ベトナム

- 香港

- 台湾

第6章 競合情勢

- 企業プロファイル

- Axis Communications AB

- Zhejiang Dahua Technology Co. Ltd

- Securitas Technology

- Bosch Sicherheitssysteme GmbH

- Johnson Controls International

- Honeywell International Inc.

- Schneider Electric

- Convergint Technologies LLC

- ASSA ABLOY

- Cisco Systems Inc.

- ABB Ltd

第7章 投資分析

第8章 市場機会と今後の動向

目次

The Asia-Pacific Data Center Physical Security Market size is estimated at USD 0.53 billion in 2024, and is expected to reach USD 1.04 billion by 2029, growing at a CAGR of 14.5% during the forecast period (2024-2029).

Data center security employs a four-layered approach: perimeter security, facility controls, computer room controls, and cabinet controls. The first layer, perimeter security, focuses on deterring and detecting unauthorized personnel, aiming to delay potential breaches. Should a breach occur, the second layer, which employs access control systems like card swipes or biometrics, restricts further access. The third layer enhances physical security with various verification methods, including monitoring restricted areas, turnstiles, VCA, biometric access controls for fingerprints, irises, or vascular patterns, and radio frequency identification. While these layers primarily focus on authorized personnel, an additional layer, cabinet locking mechanisms, addresses concerns of insider threats, such as malicious employees.

Key Highlights

- The upcoming IT load capacity of the Asia-Pacific data center construction market is expected to reach 23K MW by 2029.

- The region's construction of raised floor area is expected to increase 74.5 million sq. ft by 2029.

- The region's total number of racks to be installed is expected to reach 4.2 million units by 2029. India is expected to house the maximum number of racks by 2029.

- There are close to 160 submarine cable systems connecting Asia-Pacific, and many are under construction. One such submarine cable estimated to start service in 2024 is Southeast Asia-Japan Cable 2 (SJC2), which stretches over 10,500 kilometers with a landing point in China, Taiwan, Japan, South Korea, Thailand, and Vietnam.

Asia-Pacific Data Center Physical Security Market Trends

The IT & Telecom Segment is Expected to Hold Significant Share

- In Asia-Pacific, the hyper-connectivity environment has reinforced the importance of telcos, which play a foundational role in supporting consumers' and enterprises' connectivity and collaboration needs. Across Asia-Pacific, 75% of the operators registered positive revenue growth. South Korea is second only to Hong Kong in the world rankings of telecom market maturity.

- South Korea is on the leading edge of the latest telecom technology developments, including around 6G. In terms of investment, in November 2022, Malaysian telcos Celcom and DiGi approved the merger agreement. Once the two companies are fully merged, the new entity will be one of the largest carriers in Malaysia, with over 20 million subscribers.

- Australia has deployed 5G in major cities and is in the process of auctioning off the spectrum to provide more services. In April 2021, the government allocated a high band 5G spectrum (in the 26 GHz band), which will enable extremely fast, high-capacity services. In the second half of 2021, the government allocated a low band 5G spectrum (in the 850/900 MHz band), which will be crucial for ensuring broader geographic coverage of 5G services. This will enable new applications for 5G in the enterprise market leading to major increase in data traffic and data center demand. This will lead to major physical security demand.

- The advent of 5G in Asia-Pacific has accelerated small-cell deployment for high-speed network connectivity. Many nations have created exemption standards that can be applied when deploying new small cells. For instance, in Singapore, The Infocomm Media Development Authority (IMDA) has directed the building developers and owners to provide rooftop spaces free of charge for telecommunication equipment the telecom providers.

- The Chinese government is focusing on improving the data center physical security solutions to meet the market demand. The Chinese government plans to build eight computing hubs and 10 data center clusters to build a unified data center system by 2025. The project aims to channel the growing demand from the east to the data centers in the western region of the country.

China is Expected to Hold Significant Growth

- The Chinese government is focusing on improving the data center physical security solutions to meet the market demand. The Chinese government plans to build eight computing hubs and 10 data center clusters to build a unified data center system by 2025. The project aims to channel the growing demand from the east to the data centers in the western region of the country.

- Many businesses are constantly investing in data center expansion, which will create market opportunities in data center applications. GLP Pte, for example, raised USD 500 million in new funds in February 2022 to help expand its data center platform in China amid rising investor demand for digital infrastructure assets. According to the company, the transaction could value China data centers between USD 4 billion and USD 5 billion. Such investments will propel the market forward.

- Cloud computing provides web-based infrastructure, wherein services such as additional computing and information storage are delivered to the clients. The cloud infrastructure is comparatively cheaper than the traditional system, wherein sizeable server farms and storage systems are allocated in a data center. Such factor relates with major construction in cloud data center catering to major physical security solutions demand.

- Chinese government is stridden into fifth-generation mobile telecommunications technology and the thriving e-commerce sector leveraging the potential of internet data centers, thereby enabling IDCs viable investments for the industry stakeholders. Further, the trend is supported by the emergence of powerhouses such as Tencent Holdings and Huawei Technologies, whose growth drives the construction of IDC facilities in the region leading to major demand for video surveillance and access control solutions.

Asia-Pacific Data Center Physical Security Industry Overview

The Asia-Pacific data center physical security market is highly fragmented due to players like Axis Communications AB, ABB Ltd, and Bosch Sicherheitssysteme GmbH, which play a vital role in upscaling the capabilities of enterprises. Market orientation leads to a highly competitive environment. These major players with a prominent market share focus on expanding their customer base across the region. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

April 2023: Schneider Electric launched of new services offer, EcoCare for Modular Data Centers services membership. Members of this innovative service plan benefit from specialized expertise to maximize modular data centers' uptime with 24/7 proactive remote monitoring and condition-based maintenance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Data Center Activities and Investment by the Hyperscale and Colocation Operators

- 4.2.2 Advancements in Video Surveillance Systems Connected to Cloud Systems

- 4.3 Market Restraints

- 4.3.1 Operational and Return On Investment Concerns

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Solution Type

- 5.1.1 Video Surveillance

- 5.1.2 Access Control Solutions

- 5.1.3 Other Solution Types (Mantraps, Fences, and Monitoring Solutions)

- 5.2 By Service Type

- 5.2.1 Consulting Services

- 5.2.2 Professional Services

- 5.2.3 Other Service Types (System Integration Services)

- 5.3 End User

- 5.3.1 IT & Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Healthcare

- 5.3.5 Other End Users

- 5.4 Country

- 5.4.1 Indonesia

- 5.4.2 India

- 5.4.3 China

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 Philippines

- 5.4.7 Thailand

- 5.4.8 Singapore

- 5.4.9 New Zealand

- 5.4.10 Japan

- 5.4.11 Malaysia

- 5.4.12 Vietnam

- 5.4.13 Hong Kong

- 5.4.14 Taiwan

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Axis Communications AB

- 6.1.2 Zhejiang Dahua Technology Co. Ltd

- 6.1.3 Securitas Technology

- 6.1.4 Bosch Sicherheitssysteme GmbH

- 6.1.5 Johnson Controls International

- 6.1.6 Honeywell International Inc.

- 6.1.7 Schneider Electric

- 6.1.8 Convergint Technologies LLC

- 6.1.9 ASSA ABLOY

- 6.1.10 Cisco Systems Inc.

- 6.1.11 ABB Ltd

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日