スペインのデータセンター物理セキュリティ:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

Spain Data Center Physical Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549877

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

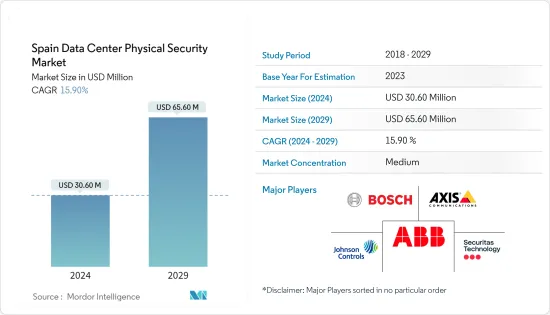

スペインのデータセンター物理セキュリティ市場規模は、2024年に3,060万米ドルと推定され、2029年には6,560万米ドルに達すると予測され、予測期間(2024~2029年)のCAGRは15.90%で成長すると予測されます。

中小企業におけるクラウドコンピューティング需要の増加、データセキュリティに関する政府規制、国内企業による投資の拡大などが、同国のデータセンター需要を促進する主要要因となっています。

主要ハイライト

- 建設中のIT負荷容量:スペインのデータセンター・ラック市場の今後のIT負荷容量は、2029年までに1,400MWに達する見込み。

- 建設中の高床スペース:2029年までにスペインの高床面積は600万平方フィートに増加すると予想されます。

- 計画中のラック:国内の設置予定ラック総数は、2029年までに33万個に達する見込みです。2029年までに最大数のラックが設置されるのはマドリードと予想されます。

- 計画されている海底ケーブル:スペインを結ぶ海底ケーブルシステムは32近くあり、その多くが建設中です。

- データセンターの攻撃対象や、物理的、人的、デジタル的にセキュリティが破られる可能性は拡大しています。このような市場の事例は、データセンターの物理的セキュリティの参入企業にとって、データセンターで重要な物理的セキュリティ製品の導入を支援する上で重要な役割を生み出しています。物理的セキュリティ製品を導入することで、複数の物理的セキュリティ層を設置した結果、割り込み、ソーシャル・エンジニアリング攻撃、内部脅威などの脅威を減らすことができるからです。

- また、国内のさまざまなエンドユーザーによるデータ消費の増加は、データセンター施設への需要を高め、その結果、ハイパースケール・プロバイダーやコロケーション・プロバイダーによる投資が増加しています。市場のこうした事例が物理セキュリティ製品の採用につながり、スペインのデータセンター物理セキュリティ市場の成長を後押ししています。

スペインのデータセンター物理セキュリティ市場動向

IT・通信セグメントが市場の主要シェアを占める

- ビッグデータと人工知能に牽引された大企業によるクラウド利用の増加がスペイン市場の主要促進要因となっています。クラウドベースのサービス導入の増加は、スペインにおける小売・卸売コロケーションサービスの拡大に拍車をかけ、需要増につながっています。このため、データセンターにはより多くのラックが必要となります。

- デジタル化に不可欠なクラウドサービス市場は急成長しています。スペインではデジタル経済の台頭とインターネット利用の増加に伴い、データ保存と処理のニーズが高まっている

- 政府は、中央政府プライベート・クラウド(SARAクラウド)構想の拡大と改善のために、8,400万ユーロ(9,081万米ドル)を割り当てています。クラウドの利用は新たなビジネスモデルの開発を促進し、あらゆる規模や業種の企業がイノベーションを起こし、競合を獲得することを可能にします。

- さらに、データセンター産業は通信部門に大きく依存しています。5Gとブロードバンド産業は、全国で急速にリンクを構築・展開しています。同国は、5Gの導入を推進するため、2025年までに43億2,000万ユーロ(45億5,110万米ドル)を拠出する「コネクティビティとデジタルインフラ計画」と「5G技術推進戦略」を策定しました。このような市場動向により、今後数年間はデータセンター向けセキュリティソリューションの需要が高まると予想されます。

ビデオモニタリングセグメントが最大の市場シェアを占める

- データセンターには機密性の高い重要なデータが保管されているため、セキュリティが最優先されます。データセンター事業者は、ビデオモニタリングシステムを通じてセキュリティ基準や規制の遵守を保証し、アクセスのモニタリング、不正侵入の検出、コンプライアンスの維持に役立てています。

- データセンターの運営者の多くは、遠隔ビデオモニタリングシステムを利用して、1日中施設をモニタリングしています。これにより、スタッフが現場にいなくても、あらゆるセキュリティ上の脅威に迅速に対処することができます。

- スペインを含む欧州連合(EU)では、一般データ保護規則(General Data Protection Regulation)などのデータ保護規制により、セキュリティとプライバシーに関する厳しい要件が課されています。これらの規制はビデオモニタリング装置によって遵守されなければならないため、データセンター事業者にとって極めて重要です。このような市場の事例が、調査対象市場の需要を後押ししています。

- さらに、インターネット・ユーザーやオンラインショッピングなどの要因も、データセンターと処理設備の世代増加に寄与すると考えられます。魅力的なキャンペーンを利用したオンラインショッピングを好むユーザーが増えるにつれ、デジタル決済サービスやウェブサイトのトラフィックが増加し、データ消費量が増加します。同国のデジタル決済ユーザー数は、2022年の3,235万人から2027年には4,060万人に達すると予測されています。これらすべての要因が消費の大幅な増加に寄与し、同地域におけるDC物理セキュリティソリューションの需要を押し上げると考えられます。

- 同市場の主要企業は、市場の需要に対応するため、データセンターの物理セキュリティソリューションの改善に注力しています。2023年4月、シュナイダーエレクトリックは、会員制のモジュール型データセンターサービスの新サービス「EcoCare」を開始しました。この革新的なサービスプランの会員は、24時間体制で継続的に状態をモニタリング・維持することによりモジュール型データセンターの効率を最大化する特別な専門知識を利用できます。

スペインのデータセンター物理セキュリティ産業概要

同国では今後DC建設プロジェクトが予定されており、スペインのデータセンター物理セキュリティ市場の需要は今後数年で増加すると考えられます。スペインのデータセンター物理セキュリティ市場は、Axis Communications AB、ABB Ltd、Securitas Technology、Bosch Sicherheitssysteme GmbH、Johnson Controlsなどの参入企業が市場に参入しており、適度に統合されています。圧倒的な市場シェアを誇るこれらの大手企業は、地域の顧客基盤の拡大に注力しています。

- 2023年4月、Securitasは、31カ国でマイクロソフトのデータセンターセキュリティを提供する5年間の拡大契約を締結。これには、リスク管理、システムインテグレーターとしての包括的なセキュリティ技術、安全セキュリティの専門リソース、警備サービス、デジタルインターフェースが含まれます。

- 2023年3月、Motorola Solutionsは、拡大性、安全性、柔軟性に優れたビデオセキュリティと入退室管理ソリューションを世界中の組織に提供する、新しいAvigilon物理セキュリティスイートを発表しました。Avigilonセキュリティスイートには、オンプレミスのAvigilon UnityソリューションとクラウドネイティブのAvigilon Altaが含まれ、それぞれ先進的分析機能を備え、ユーザーエクスペリエンスに優れた設計となっています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- クラウドコンピューティング機能に対する需要の高まりが市場の成長を促進

- セキュリティへの懸念の高まりが市場の成長を促進

- 市場抑制要因

- 物理的セキュリティインフラに関連する高コスト

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- ソリューションタイプ別

- ビデオモニタリング

- 入退室管理ソリューション

- その他(マントラップ、フェンス、モニタリングソリューション)

- サービスタイプ別

- コンサルティングサービス

- プロフェッショナルサービス

- その他(システムインテグレーションサービス)

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- 医療

- その他

第6章 競合情勢

- 企業プロファイル

- Axis Communications AB

- ABB Ltd

- Securitas Technology

- Bosch Sicherheitssysteme GmbH

- Johnson Controls

- Honeywell International Inc.

- Siemens AG

- Schneider Electric

- Cisco Systems Inc.

- Hikvision

- Genetec

- Pelco(Motorola Solutions Inc.)

- Milestone Systems AS

第7章 投資分析

第8章 市場機会と今後の動向

目次

The Spain Data Center Physical Security Market size is estimated at USD 30.60 million in 2024, and is expected to reach USD 65.60 million by 2029, growing at a CAGR of 15.90% during the forecast period (2024-2029).

The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country.

Key Highlights

- Under construction IT load capacity: The upcoming IT load capacity of the Spain data center rack market is expected to reach 1400 MW by 2029.

- Under construction raised floor space: The country's construction of raised floor area is expected to increase to 6 million sq. ft by 2029.

- Planned racks: The country's total number of racks to be installed is expected to reach 330,000 units by 2029. Madrid is expected to house the maximum number of racks by 2029.

- Planned submarine cables: There are close to 32 submarine cable systems connecting Spain, and many are under construction.

- The data center's attack surface and the physical, human, and digital ways security can be breached are expanding. Such instances in the market create a significant role for data center physical security players in helping to install physical security products that are important in data centers, as they reduce the threat of interruptions, social engineering attacks, insider threats, and others as a result of the installation of several layers of physical security.

- In addition, increasing data consumption among various end users in the country creates more demand for data center facilities, which results in increasing investments by hyperscale and colocation providers. Such instances in the market led to the adoption of physical security products and propelled the growth of the Spanish data center physical security market.

Spain Data Center Physical Security Market Trends

The IT and Telecommunication Segment Holds a Major Share in the Market

- Increasing use of the cloud by large companies, driven by big data and artificial intelligence, is the main driver of the Spanish market. Increased adoption of cloud-based services has fueled the expansion of retail and wholesale colocation services in Spain, leading to increased demand. This will require more racks in the data center.

- The cloud service market, which is indispensable for digitalization, is growing rapidly. With the rise of the digital economy and increased internet usage in Spain, the need for data storage and processing is increasing.

- The government has allocated EUR 84 million (USD 90.81 million) for the expansion and improvement of the Central Government Private Cloud (SARA Cloud) initiative. The use of the cloud facilitates the development of new business models, enabling companies of all sizes and industries to innovate and gain a competitive edge.

- Additionally, the data center industry heavily depends on the telecommunications sector. The 5G and broadband industries are rapidly building and deploying links across the nation. The nation has developed the Plan for Connectivity and Digital Infrastructures and the Strategy to Promote 5G Technology, which would be endowed with EUR 4,320 million (USD 4551.1 million) through 2025 to push the adoption of 5G. Such instances in the market are expected to create more demand for data center security solutions in the coming years.

The Video Surveillance Segment Holds the Largest Market Share

- Data centers are home to sensitive and vital data, which makes security their highest priority. Data center operators help ensure that security standards and regulations are respected through video surveillance systems, which provide them with monitoring of access, detection of unauthorized entry, and maintaining compliance.

- Many operators of data centers are using remote video surveillance to keep an eye on their facilities throughout the day. This ensures that all security threats can be quickly addressed, even where staff are not at the site.

- Data protection regulations such as the General Data Protection Regulation impose strict security and privacy requirements within the European Union, including Spain. These regulations must be complied with by video surveillance equipment, and, therefore, they are of vital importance for data center operators. Such instances in the market propel the demand of the studied market.

- Furthermore, factors such as internet users and online shopping would contribute to the increasing generation of data and processing facilities. As users grow more inclined to shop online with attractive deals offered, this would lead to a rise in digital payment services and traffic on websites, thus increasing data consumption. The number of digital payment users in the country is projected to reach 40.6 million by 2027, up from 32.35 million users in 2022. All these factors would contribute to a significant increase in consumption, boosting the demand for DC physical security solutions in the region.

- Key players in the market focus on improving the data center's physical security solutions to meet the market demand. In April 2023, Schneider Electric launched a new Service, EcoCare, for modular data center services included with membership. Special expertise in maximizing the efficiency of modular data centers by continuously monitoring and maintaining conditions 24 hours a day is available to members of this innovative service plan.

Spain Data Center Physical Security Industry Overview

The upcoming DC construction projects in the country would increase the demand for the Spanish data center physical security market in the coming years. The Spanish data center physical security market is moderately consolidated with some players in the market, including Axis Communications AB, ABB Ltd, Securitas Technology, Bosch Sicherheitssysteme GmbH, and Johnson Controls. These major players, with a prominent market share, focus on expanding their regional customer base.

- April 2023: Securitas signed an expanded 5-year agreement to provide data center security for Microsoft in 31 countries. It includes risk management, comprehensive security technology as a system integrator, specialized safety and security resources, guarding services, and digital interfaces.

- March 2023: Motorola Solutions announced the new Avigilon physical security suite, providing organizations worldwide with scalable, secure, and flexible video security and access control solutions. The Avigilon security suite includes the on-premise Avigilon Unity solutions and cloud-native Avigilon Alta, each with advanced analytics designed to provide an effortless user experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Cloud Computing Capabilities Drives the Market's Growth

- 4.2.2 Increasing Security Concerns Drives the Market's Growth

- 4.3 Market Restraints

- 4.3.1 High Costs Associated with Physical Security Infrastructure

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Solution Type

- 5.1.1 Video Surveillance

- 5.1.2 Access Control Solutions

- 5.1.3 Others (Mantraps, Fences, and Monitoring Solutions)

- 5.2 By Service Type

- 5.2.1 Consulting Services

- 5.2.2 Professional Services

- 5.2.3 Others (System Integration Services)

- 5.3 End User

- 5.3.1 IT and Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Healthcare

- 5.3.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Axis Communications AB

- 6.1.2 ABB Ltd

- 6.1.3 Securitas Technology

- 6.1.4 Bosch Sicherheitssysteme GmbH

- 6.1.5 Johnson Controls

- 6.1.6 Honeywell International Inc.

- 6.1.7 Siemens AG

- 6.1.8 Schneider Electric

- 6.1.9 Cisco Systems Inc.

- 6.1.10 Hikvision

- 6.1.11 Genetec

- 6.1.12 Pelco (Motorola Solutions Inc.)

- 6.1.13 Milestone Systems AS

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日