|

市場調査レポート

商品コード

1549907

中東のデータセンターフィジカルセキュリティ:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Middle East Data Center Physical Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東のデータセンターフィジカルセキュリティ:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

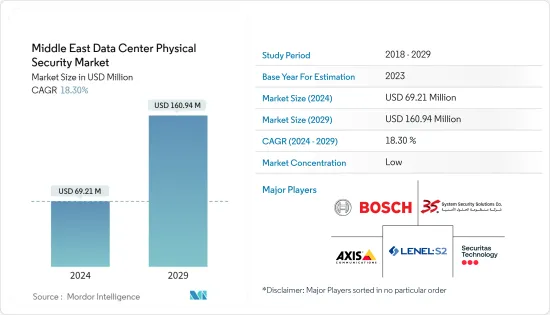

中東のデータセンターフィジカルセキュリティ市場規模は、2024年に6,921万米ドルと推定され、2029年には1億6,094万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは18.30%で成長すると予測されます。

データセンターのセキュリティは、境界セキュリティ、施設管理、コンピュータールーム管理、キャビネット管理の4層アプローチを採用しています。第1層である境界セキュリティは、不正侵入者の抑止と検知に重点を置き、潜在的な侵入を遅らせることを目的としています。万が一侵入された場合は、カード・スワイプや生体認証のようなアクセス・コントロール・システムを採用する第2層が、それ以上のアクセスを制限します。第3のレイヤーは、制限区域の監視、改札口、VCA、指紋、虹彩、血管パターンの生体認証アクセス・コントロール、無線周波数識別など、さまざまな検証方法で物理的セキュリティを強化します。これらのレイヤーは主に許可された人員に焦点を当てているが、追加のレイヤーであるキャビネット・ロック・メカニズムは、悪意のある従業員などの内部脅威の懸念に対応しています。

中東データセンター市場の今後のIT負荷容量は、2029年までに2,059.5MWに達すると予想されています。

同地域の増床面積は2029年までに970万平方フィート増加すると予想されます。

同地域で設置されるラックの総数は、2029年までに49万6,000ユニットに達すると予想されます。サウジアラビアが2029年までに最大数のラックを設置する見込みです。

中東を結ぶ海底ケーブルシステムは26近くあり、その多くが建設中です。2024年にサービス開始が見込まれる海底ケーブルのひとつがBlueで、テルアビブを陸揚げ点とする全長4,696kmに及ぶ。

中東のデータセンターフィジカルセキュリティ市場動向

IT・通信分野が大きなシェアを占める見込み

- IT業界では、オンプレミスからコロケーションやクラウドサービスへの移行が進む中、サードパーティ施設に移行する際のデータセンターの物理的セキュリティに対する懸念が高まっています。通常、Deutsche Telekom AG、Verizon、AT&Tなどの主要企業が所有・運営する通信データセンターは、コンテンツ配信やモバイルおよびクラウドサービスのサポートに不可欠であり、最高レベルの接続性とセキュリティが求められます。

- アラブ首長国連邦の著名なシステムインテグレーターであるFOSS LLCは、物理的セキュリティとCCTVソリューションに対する顧客の需要が大幅に増加していることを確認しています。この増加の主な原因は、安全性とセキュリティが重視されるようになったことです。特筆すべきは、IPベースのCCTVシステムとソフトウェア主導のアナリティクスの進歩により「インテリジェント」ソリューションが導入され、通信データセンターにおける常時人的監視の必要性が減少したことです。

- アラブ首長国連邦では、データ・トラフィックとネットワーク・ニーズの増加に伴い、通信データセンターが増加しています。5G技術の展開が進むにつれて、安全な通信データセンターへの需要が高まることが予想されます。

- 2023年7月、サウジテレコム(STC)の子会社Center3がリヤドのデータセンターを拡張しました。STCは既存のリヤドとジッダの施設の容量を増やし、ジッダ、リヤド、ダンマームなどの主要都市で新しいデータセンターを開発しており、王国のデータインフラが成長していることを強調しています。

著しい成長が期待されるアラブ首長国連邦

- アラブ首長国連邦(UAE)のデータセンターでは、4Gの普及が進み、5G革命が間近に迫っていることから、投資が増加しています。アラブ首長国連邦(UAE)の通信規制庁は、2022年3月時点でUAEのアクティブな携帯電話加入者は1,870万人と報告しています。

- BIOS中東グループは、UAEのデータセンターにアクセスセキュリティソリューションを提供しています。BIOS中東グループは、UAEのデータセンター向けにアクセスセキュリティソリューションを提供しています。これらのシステムは、バイオメトリクス、カードキー、コードによる入館管理を利用しています。アクセス・ログを定期的にレビューすることで、継続的なセキュリティを確保しています。

- クラウドの新興企業がデータセンター建設ブームを牽引する中、UAEでは入退室管理ソリューションの需要が高まると予想されています。同国には、TruKKer、G42、Alaanなど、約1,171社のSaaS新興企業があります。

- UAEの通信当局は、2025年までに5Gの普及率を100%にするという目標を掲げており、通信プロバイダーにとってデータセンターが大幅に拡大することを示しています。特に、内部犯行などのセキュリティ脅威は物理的なネットワークアクセスに起因することが多く、堅牢なデータセンターフィジカルセキュリティ対策の必要性が高まっていることが浮き彫りになっています。

中東のデータセンターフィジカルセキュリティ産業の概要

中東のデータセンターフィジカルセキュリティ市場は、プレーヤー間で細分化されており、近年は競合優位性を獲得しています。主なプレーヤーとしては、Securitas Technology、Bosch Sicherheitssysteme GmbHなどが挙げられます。圧倒的な市場シェアを誇るこれらの大手企業は、地域顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために戦略的協業イニシアティブを活用しています。

2023年4月シュナイダーエレクトリックは、新しいサービス「EcoCare for Modular Data Centers」のメンバーシップサービスを開始しました。この革新的なサービスプランの会員は、24時間365日のプロアクティブなリモート監視と状態ベースのメンテナンスにより、モジュラー型データセンターの稼働時間を最大化するための専門知識を利用できます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 犯罪率と脅威の増加による入退室管理システムの採用拡大

- クラウドシステムに接続されたビデオ監視システムの進歩

- 市場抑制要因

- 運用と投資収益率に関する懸念

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- ソリューションタイプ別

- ビデオ監視

- 入退室管理ソリューション

- その他のソリューションタイプ(マントラップ、フェンス、モニタリングソリューション)

- サービスタイプ別

- コンサルティングサービス

- プロフェッショナルサービス

- その他のサービスタイプ(システム・インテグレーション・サービス)

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- ヘルスケア

- その他のエンドユーザー

- 国名

- イスラエル

- サウジアラビア

- アラブ首長国連邦

第6章 競合情勢

- 企業プロファイル

- Axis Communications AB

- LenelS2

- Securitas Technology

- 3S System Security Solutions Co.

- Bosch Sicherheitssysteme GmbH

- Johnson Controls International

- Honeywell International Inc.

- Siemens AG

- Schneider Electric

- Ctelecoms

- BIOS Middle East Group

- Pacific Control Systems

- Fiber Optics Supplies and Services LLC

- Convergint Technologies LLC

第7章 投資分析

第8章 市場機会と今後の動向

The Middle East Data Center Physical Security Market size is estimated at USD 69.21 million in 2024, and is expected to reach USD 160.94 million by 2029, growing at a CAGR of 18.30% during the forecast period (2024-2029).

Data center security employs a four-layered approach: perimeter security, facility controls, computer room controls, and cabinet controls. The first layer, perimeter security, focuses on deterring and detecting unauthorized personnel, aiming to delay potential breaches. Should a breach occur, the second layer, which employs access control systems like card swipes or biometrics, restricts further access. The third layer enhances physical security with various verification methods, including monitoring restricted areas, turnstiles, VCA, biometric access controls for fingerprints, irises, or vascular patterns, and radio frequency identification. While these layers primarily focus on authorized personnel, an additional layer, cabinet locking mechanisms, addresses concerns of insider threats, such as malicious employees.

The upcoming IT load capacity of the Middle Eastern data center market is expected to reach 2,059.5 MW by 2029.

The region's construction of raised floor area is expected to increase 9.7 million sq. ft by 2029.

The region's total number of racks to be installed is expected to reach 496K units by 2029. Saudi Arabia is expected to house the maximum number of racks by 2029.

Close to 26 submarine cable systems are connecting the Middle East, and many are under construction. One such submarine cable estimated to start service in 2024 is Blue, which stretches over 4,696 km with a landing point in Tel Aviv.

Middle East Data Center Physical Security Market Trends

The IT and Telecom Segment is expected to Hold a Significant Share

- IT players are increasingly concerned about the physical security of data centers when transitioning to third-party facilities, even as the industry moves away from on-premise setups towards colocation and cloud services. Telecom data centers typically owned and operated by major players like Deutsche Telekom AG, Verizon, or AT&T, are essential in content delivery and supporting mobile and cloud services, necessitating top-tier connectivity and security.

- FOSS LLC, a prominent systems integrator in the UAE, has observed a significant rise in customer demands for physical security and CCTV solutions. This increase is largely attributed to a growing emphasis on safety and security. Notably, advancements in IP-based CCTV systems and software-driven analytics have introduced "intelligent" solutions, reducing the need for constant human monitoring in telecom data centers.

- With rising data traffic and networking needs, the United Arab Emirates is experiencing a rise in telecommunication data centers. As the deployment of 5G technology progresses, the demand for secure telecom data centers is expected to increase.

- In July 2023, Saudi Telecom's (STC) subsidiary, Center3, expanded its data center in Riyadh. STC is increasing capacities in its existing Riyadh and Jeddah facilities and developing new data centers across key cities like Jeddah, Riyadh, and Dammam, highlighting the Kingdom's growing data infrastructure.

The United Arab Emirates is Expected to Hold Significant Growth

- The UAE's data center landscape is experiencing increased investments, driven by the rising adoption of 4G and the imminent 5G revolution. The Telecommunications Regulatory Authority (UAE) reported 18.7 million active mobile subscribers in the UAE as of March 2022.

- BIOS Middle East Group provides access security solutions for UAE data centers. Their measures include limiting physical access to authorized personnel, supported by on-premise security systems. These systems utilize biometric, card key, and coded entry controls. Regular reviews of access logs ensure ongoing security.

- As cloud startups drive a boom in data center construction, the UAE's demand for access control solutions is expected to rise. The country has approximately 1,171 SaaS startups, including TruKKer, G42, and Alaan.

- The UAE's telecoms authority has set a target of achieving 100% 5G penetration by 2025, indicating a significant data center expansion for telecom providers. Notably, security threats like insider breaches often stem from physical network access, highlighting the growing need for robust data center physical security measures.

Middle East Data Center Physical Security Industry Overview

The Middle Eastern data center physical security market is fragmented among the players and has gained a competitive edge in recent years. A few major players are Securitas Technology, Bosch Sicherheitssysteme GmbH, etc. These major players, with a prominent market share, focus on expanding their regional customer base. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

April 2023: Schneider Electric launched a new service offer, EcoCare for Modular Data Centers services membership. Members of this innovative service plan benefit from specialized expertise to maximize modular data centers' uptime with 24/7 proactive remote monitoring and condition-based maintenance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Access Control Systems Owing to Rising Crime Rates and Threats

- 4.2.2 Advancements in Video Surveillance Systems Connected to Cloud Systems

- 4.3 Market Restraints

- 4.3.1 Operational and Return On Investment Concerns

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of the COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Solution Type

- 5.1.1 Video Surveillance

- 5.1.2 Access Control Solutions

- 5.1.3 Other Solution Types (Mantraps and Fences and Monitoring Solutions)

- 5.2 By Service Type

- 5.2.1 Consulting Services

- 5.2.2 Professional Services

- 5.2.3 Other Service Types (System Integration Services)

- 5.3 End User

- 5.3.1 IT and Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Healthcare

- 5.3.5 Other End Users

- 5.4 Country

- 5.4.1 Israel

- 5.4.2 Saudi Arabia

- 5.4.3 United Arab Emirates

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Axis Communications AB

- 6.1.2 LenelS2

- 6.1.3 Securitas Technology

- 6.1.4 3S System Security Solutions Co.

- 6.1.5 Bosch Sicherheitssysteme GmbH

- 6.1.6 Johnson Controls International

- 6.1.7 Honeywell International Inc.

- 6.1.8 Siemens AG

- 6.1.9 Schneider Electric

- 6.1.10 Ctelecoms

- 6.1.11 BIOS Middle East Group

- 6.1.12 Pacific Control Systems

- 6.1.13 Fiber Optics Supplies and Services LLC

- 6.1.14 Convergint Technologies LLC