|

市場調査レポート

商品コード

1549886

欧州のフィジカルセキュリティ:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Europe Physical Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のフィジカルセキュリティ:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

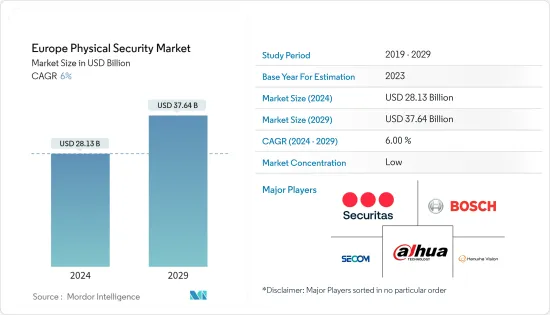

欧州のフィジカルセキュリティ市場規模は2024年に281億3,000万米ドルと推計され、2029年には376億4,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは6%で成長すると予測されます。

主なハイライト

- フィジカルセキュリティには、組織の安全を保証するために対処しなければならない多くの側面が含まれます。最も基本的なフィジカルセキュリティには、個人、資産、インフラの保護に直接関連するセキュリティ対策が含まれます。ビデオ監視カメラやクラウドベースの監視システムなどのフィジカルセキュリティシステムは、欧州市場の成長に大きく貢献しています。同市場では、防犯カメラの台数が増加しています。

- 人工知能(AI)や機械学習(ML)の急速な進歩により、新築や商業施設の改修におけるスマートビルディング技術に組み込まれ、フィジカルセキュリティ・システムを利用する機器が増加しています。これらの要因は、多くのアプリケーションでクラウドストレージが常に進化していることと相まって、フィジカルセキュリティシステムの成長を促進するアーキテクチャと技術の更新を必要としています。

- フィジカルセキュリティ市場の成長は、これらのシステムをモノのインターネット(IoT)デバイス、人工知能、クラウドサービスと統合することで拡張知能が高まる。例えば、2023年8月、英国・イングランドの主要道路沿いに、警察によって人工知能(AI)カメラシステムが設置されました。72時間以内に、このシステムは法律に違反した約300人の 促進要因を捉えました。5日後には、その数は合計1,000人にまで増えました。政府は事故を回避し、規則をよりよく執行するために、このようなセキュリティ対策を採用しています。AI搭載カメラは需要が急増しており、市場の成長を後押しする可能性が高いです。

- 高度なビデオ分析を導入することで、虹彩、指紋、顔、ナンバープレート認識、群衆認識、人の追跡とカウントなど幅広い機能が提供され、フィジカルセキュリティ・ソリューションのニーズを後押ししています。ドイツでは、小売業や接客業において、年齢推定や支払いプロセスなどを自動化するために生体認証の導入が進んでいます。このような採用により、ドイツ全土でフィジカルシステムに対する需要が高まると思われます。

- COVID-19の大流行後、欧州市場ではフィジカルセキュリティのビジネスチャンスが拡大し、より高度な製品やシステムを購入する可能性が出てきました。フィジカルセキュリティ市場は、着実に規模が拡大し、セキュリティ機器の導入が進んでいます。さらに、企業や公共エリアは、変化する衛生要件に対応しなければならなくなった。そのため、フィジカルセキュリティ・システムは現在、容量制限、マスク・コンプライアンス、衛生規制への準拠を可能にしています。

- しかし、欧州中の組織が監視・分析システムを導入する際には、運用上の問題があり、精度が導入の主な障壁の1つとなっているため、大きな課題に直面しています。さらに、ビデオ監視はプライバシーの侵害とみなされるため、市民的自由のコミュニティでは論争の的となっています。誰がビデオを見ているのか、悪用される可能性はないかという意識が高まっており、個人は自分のデータが合法的で特定された目的にのみ使用されることを期待しているため、市場の成長を妨げています。

欧州のフィジカルセキュリティ市場動向

バイオメトリクス・システム分野が大きな市場シェアを占める見込み

- バイオメトリクスは主に、盗難の影響を受けやすいセキュアな環境や、フィジカルセキュリティが不可欠な環境のセキュリティ・システムに採用されています。これらのシステムは、指紋、音声、網膜、顔、手信号などの不変データを収集します。バイオメトリクス・ソリューションは、パスワードやアクセス・カードといった他の認証方法よりも高いセキュリティを提供します。フィジカルセキュリティにおけるバイオメトリクス・システムの利用は、技術の進歩、手頃な価格と信頼性の向上により需要が高まっています。

- 例えば、2023年8月、フランス当局は、欧州連合(EU)のEES(出入国管理システム)システムが稼動すると、フランスに旅行する英国の乗客に行列が生じる可能性があるという懸念に対応するため、フェリー・カーの乗客から顔と指紋のバイオメトリクス・データを収集するための544台のキオスクと250台のタブレットを発注しました。また、同システムは、旅客が旅券を確認するためにデジタルキオスクでスキャンする必要があるため、国境審査にかかる時間が長くなる可能性があるとしています。

- 英国政府は、安全なバイオメトリクス出入国管理システムの導入を継続しています。2023年7月、英国政府はデジタルビザのバイオメトリクス要件に違反した場合、新たな罰則を導入しました。この改正は、顔バイオメトリクスを正確に照合できるように、書類に含まれる写真が高度すぎないことを保証するものです。このようなバイオメトリクス・システムの採用は、欧州全体のフィジカルセキュリティの需要を押し上げると思われます。

- バイオメトリクス技術の利用は増加傾向にあり、さまざまな分野で需要が高まっています。特に、顔認証はユーザーの身元確認にますます普及しています。例えば、2023年6月、フランス上院は、公共エリアにおける顔認証のテストに関する法律案を承認することを議決しました。この法律により、司法当局と情報機関は3年間、公共の場所で遠隔生体認証識別子を利用できるようになった。

- 指紋や虹彩認識などのバイオメトリクスは、乗客、職員、請負業者の身元を精密に確認することで、鉄道の安全性を高めることができます。英国の鉄道に対する公的支出は、前年の258億ポンド(315億2,000万米ドル)に対し、2022/23年度には約259億ポンド(316億4,000万米ドル)に達します。このような鉄道支出の増加は、英国の鉄道駅におけるバイオメトリクス・システム採用の需要を高めると思われます。また、欧州全域の公共スペースにおける他のフィジカルセキュリティ・システムの採用も促進されます。

- 2023年7月、ユーロスター・グループはロンドン・セント・パンクラスで、iProovが提供した生体認証非接触チェックインシステムSmartCheckを導入しました。このファスト・トラック・サービスにより、ユーロスターのビジネス・プレミアとキャラ・ブランシュの乗客は、英国と欧州大陸間の乗り継ぎ時に、発券と英国出国審査の列を回避できるようになった。

大幅な市場成長が期待されるドイツ

- ドイツでは、公共エリアにおけるテロ関連リスクの急増や、職場における従業員の安全と健康を強化する民間セクターの取り組みの増加により、監視カメラなどのフィジカルセキュリティ・システムの需要が急速に高まっています。ドイツ政府は国内のセキュリティを強化するためにいくつかの施策を採用しており、最新の監視技術の導入はこうした取り組みにおいて重要な役割を果たしています。

- 交通事故死者数の増加により、ビデオ監視カメラを設置する必要性が高まっています。ビデオ監視カメラは交通事故を監視し、記録することができるため、事故の原因や動向をより包括的に把握することができます。

- ドイツ連邦統計局(Statistische Bundesamt)によると、2022年のドイツの死亡事故件数は2776件で、前年より2562件増加しました。事故による安全リスクに対する意識の高まりは、より効果的な監視と予防対策の必要性を促しており、それが監視カメラの活用増加につながっています。

- 技術が進歩しコストが低下するにつれて、各国はAI監視カメラに投資してセキュリティと安全プロトコルを改善する価値を認識しています。例えば、2023年4月には、AIを搭載したビデオカメラ「Monocam」がラインラント・プファルツ州に配備される予定です。車内での異常な行動を検知することができ、録画は保存され、捜査のために関連する法執行当局に送信されます。このシステムは、ドイツのラインラント・プファルツ州の2つの高速道路橋でテストされる予定です。

- バイオメトリクスは、職員や乗客を正確に識別することで空港のセキュリティを向上させ、なりすましや不正アクセスのリスクを減らすことができます。例えば、2022年4月、ハンブルク空港の利用者は、搭乗券とスマートフォンなしで保安検査場と搭乗検査場にアクセスできるようになった。この措置は、スターアライアンスの生体認証顔認証システムのイントロダクションよるもので、試験期間の成功を受けて導入されました。この技術革新により、ハンブルク空港はバイオメトリックアクセスの恩恵を受ける4番目の空港となった。このシステムに登録した乗客は、参加空港すべてにアクセスできます。

欧州のフィジカルセキュリティ産業の概要

欧州のフィジカルセキュリティ市場は、複数の企業が存在するため、複雑化しています。各社は、製品革新、新製品発売、提携、共同開発、M&Aなどの戦略を採用しています。主要企業には、Siemens AG、Securitas AB、Secom、Dahua Technology、Hanwha Vision、G4S Limited、Vanderbilt Industries、Bosch Security Systems GmbH、Teledyne FLIR LLC、Genetec Inc.、Johnson Controls、Hangzhou Hikvision Digital Technology、Schneider Electric、Honeywell International Inc.などがあります。

- 2023年8月ハンファ・ビジョンは、スマートシティ・ソリューションを提供するA2 Technology社と提携し、革新的なビデオソリューションを提供します。A2は主に、人工知能(AI)とビデオ分析を通じて、コミュニティの保護とモビリティの向上を目指しています。同社のソリューションは世界100都市以上で導入されており、最も有名なソリューションは54のトンネルと300km以上の高速鉄道に設置されています。

- 2023年7月セキュリタスは、31カ国にあるマイクロソフトのデータセンター向けにセキュリティサービスを提供する5年間の延長契約を締結。この契約は、マイクロソフトの要件に合わせて設計された包括的な一連のサービスの概要を示すものです。セキュリタスは、必要なときに必要な場所で最高レベルのセキュリティを提供することに専念しています。セキュリタスは、セキュリティ対策と革新的なソリューションのバランスを取るために、イノベーションと技術統合を重要な優先事項としています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の影響とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 企業リスクとフィジカルセキュリティ脅威

- リモートワークやハイブリッドワークの普及による組織のアクセス制御要件の増大

- 加速する機械学習(ML)と人工知能(AI)の導入

- 市場の課題

- サイバー攻撃に対するフィジカルセキュリティシステムの脆弱性

- 急速な技術進歩による頻繁なシステム更新の必要性

第6章 市場セグメンテーション

- システムタイプ別

- ビデオ監視システム

- IP監視システム

- アナログ監視

- ハイブリッド監視

- フィジカルアクセスコントロールシステム(PACS)

- バイオメトリックシステム

- 境界セキュリティ

- 侵入検知

- ビデオ監視システム

- サービスタイプ別

- Access Control as a Service(ACaaS)

- Video Surveillance as a Service(VSaaS)

- 展開タイプ別

- オンプレミス

- クラウド

- 組織規模別

- 中小企業

- 大企業

- エンドユーザー産業別

- 政府サービス

- 銀行・金融サービス

- IT・通信

- 運輸・物流

- 小売

- ヘルスケア

- 住宅産業

- その他エンドユーザー産業

- 国別

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

第7章 競合情勢

- 企業プロファイル

- Securitas AB

- Bosch Security Systems GmbH

- Secom Co. Ltd

- Dahua Technology Co. Ltd

- Hanwha Vision Co. Ltd

- G4S Limited

- Vanderbilt Industries

- Siemens AG

- Teledyne FLIR LLC

- Genetec Inc.

- Johnson Controls

- Hangzhou Hikvision Digital Technology Co. Ltd

- Schneider Electric SE

- Honeywell International Inc.

- Axis Communications AB

- NEC Corporation

- HID Global Corporation

第8章 投資分析

第9章 市場の将来

The Europe Physical Security Market size is estimated at USD 28.13 billion in 2024, and is expected to reach USD 37.64 billion by 2029, growing at a CAGR of 6% during the forecast period (2024-2029).

Key Highlights

- Physical security encompasses many aspects that must be addressed to guarantee an organization's safety. At its most fundamental, physical security encompasses security measures directly related to safeguarding individuals, assets, and infrastructure. Physical security systems like video surveillance cameras and cloud-based surveillance have significantly contributed to the European market's growth. The market is witnessing an increasing number of security cameras.

- The rapid advancements of artificial intelligence (AI) and machine learning (ML), incorporated into smart building technology in new construction and commercial refurbishment, have resulted in an increasing number of devices utilizing physical security systems. These factors, combined with the ever-evolving nature of cloud storage for many applications, necessitate architecture and technology updates that drive the growth of physical security systems.

- The physical security market's growth is augmented by integrating these systems with Internet of Things (IoT) devices, artificial intelligence, and cloud services. For instance, in August 2023, an artificial intelligence (AI) camera system was installed along a major road in England, United Kingdom, by the police. Within 72 hours, the system had captured nearly 300 drivers in breach of the law. After five days, the number had increased to a total of 1,000. The government is adopting such security measures to avoid accidents and enforce the rules and regulations better. AI-powered cameras have seen a rapid increase in demand and will likely boost the market's growth.

- Implementing advanced video analytics offers a wide range of capabilities, such as iris, fingerprint, facial, license plate recognition, crowd recognition, and tracking and counting people, driving the need for physical security solutions. In Germany, biometrics are being increasingly used in retail and hospitality settings to automate age estimation, payment processes, and more. Such adoption will generate more demand for physical systems across Germany.

- After the COVID-19 pandemic, the European market increased physical security business opportunities, with the potential to purchase more advanced products and systems. The physical security market is experiencing a steady increase in size and the adoption of security devices. Additionally, businesses and public areas have had to keep up with changing health requirements. Therefore, physical security systems now enable compliance with capacity restrictions, mask compliance, and hygiene regulations.

- However, organizations across Europe face significant challenges when implementing surveillance and analytics systems, as they are subject to operational issues, and accuracy is one of the primary barriers to adoption. Furthermore, video surveillance has become a contentious issue in the civil liberties community, as it is seen as a breach of privacy. There is a growing awareness of who is watching the video and the potential for misuse, as individuals anticipate that their data will only be used for legitimate and specified purposes, thus hindering the market's growth.

Europe Physical Security Market Trends

The Biometric System Segment is Expected to Hold a Significant Market Share

- Biometrics are primarily employed in security systems for secure environments susceptible to theft or essential physical security needs. These systems collect immutable data, such as fingerprints, voice, retinal, facial, and hand signals. Biometric solutions provide more security than other authentication methods, such as passwords or access cards. The utilization of biometric systems in physical security is in demand due to technological advancements and their increasing affordability and dependability.

- For instance, in August 2023, the French authorities ordered 544 kiosks and 250 tablets for the collection of face and fingerprint biometric data from ferry car passengers in response to concerns that queues could arise for UK passengers traveling to France when the European Union's EES (Entry/Exit System) system becomes operational. It also stated that the system could increase the time taken to complete border checks, as passengers must be scanned at digital kiosks to verify their travel documents.

- The government of the United Kingdom is continuing to implement secure biometric immigration control systems. In July 2023, the United Kingdom government implemented new penalties for non-compliance with biometric requirements for digital visas. This amendment ensures that the photographs included in the documents are not too advanced so that face biometrics can be accurately matched. Such adoption of Biometrics Systems will boost the demand for physical security across Europe.

- The utilization of biometrics technology is on the rise, with growing demand across various sectors. In particular, facial recognition is becoming increasingly popular for verifying user identity. For instance, in June 2023, the French Senate voted to approve a proposal for a law on the testing of facial recognition in public areas. This law enabled judicial authorities and intelligence agencies to utilize remote biometric identifiers in public places for three years.

- Biometrics, such as fingerprints and iris recognition, can enhance railway safety by precision verifying the identity of passengers, staff, and contractors. Public expenditure on railways in the United Kingdom amounted to approximately GBP 25.9 billion (USD 31.64 billion) in FY 2022/23, compared to the previous year's GBP 25.8 billion (USD 31.52 billion). Such a rise in railway expenditure will increase the demand for biometrics systems adoption across railway stations in the United Kingdom. Also, it will boost the adoption of other physical security systems in public spaces across Europe.

- In July 2023, Eurostar Group implemented a biometric, contactless check-in system in London St Pancras, the SmartCheck system, which iProov provided. This fast-track service allows Eurostar's Business Premier and Cara Blanche passengers to bypass queues for ticketing and UK exit checks during connections between the United Kingdom and continental Europe.

Germany is Expected to Witness Significant Market Growth

- The demand for physical security systems like video surveillance cameras in Germany is increasing rapidly due to the proliferation of terrorism-related risks in public areas and increasing private sector initiatives to enhance the safety and health of personnel in the workplace. The German government has adopted several measures to strengthen security in the nation, and the implementation of modern surveillance technology has played a prominent role in these efforts.

- The increased number of road traffic fatalities has increased the need for installing video surveillance cameras. Video surveillance cameras can monitor and document traffic incidents, allowing for a more comprehensive understanding of the causes and trends of accidents.

- According to the Statistische Bundesamt, there were 2,776 fatalities in Germany in 2022, an increase of 2,562 cases from the previous year. The increasing awareness of safety risks caused by accidents is prompting the need for more effective monitoring and prevention measures, which is leading to an increase in the utilization of video surveillance cameras.

- As technology advances and costs decrease, countries recognize the value of investing in AI surveillance cameras to improve their security and safety protocols. For instance, in April 2023, the Monocam, a video camera equipped with AI, was expected to be deployed in the Rhineland-Palatinate region. It can detect any unusual activity in the car; the recording is stored and transmitted to the relevant law enforcement authorities for investigation. The system was expected to be tested on two highway bridges in the Land of Rhineland Palatinate, Germany.

- Biometrics can improve airport security by accurately identifying staff and passengers, thus reducing the risk of identity theft and unauthorized access. For instance, in April 2022, Hamburg Airport passengers could access security and boarding checkpoints without needing a boarding pass and smartphone. This measure was due to the introduction of the Star Alliance Biometric Face Field Recognition system, which was implemented following a successful trial period. This innovation made Hamburg Airport the fourth airport to benefit from biometric access. Passengers who register for the system can access all participating airports.

Europe Physical Security Industry Overview

The European physical security market is fragemented, owing to the presence of several companies. The players adopt strategies like product innovation, new product launches, partnerships, collaborations, and mergers and acquisitions. Some of the major players include Siemens AG, Securitas AB, Secom Co. Ltd, Dahua Technology Co. Ltd, Hanwha Vision Co. Ltd, G4S Limited, Vanderbilt Industries, Bosch Security Systems GmbH, Teledyne FLIR LLC, Genetec Inc., Johnson Controls, Hangzhou Hikvision Digital Technology Co. Ltd, Schneider Electric, and Honeywell International Inc.

- August 2023: Hanwha Vision partnered with A2 Technology, a company that offers smart city solutions, to provide innovative video solutions. A2 primarily aims to protect communities and improve mobility through artificial intelligence (AI) and video analytics. Its solutions are deployed in more than 100 cities worldwide, with its most renowned solution being installed in 54 Tunnels and 300+ km on high-speed railroads.

- July 2023: Securitas entered into an extended five-year contract to provide security services for Microsoft data centers in 31 countries. The agreement outlined a comprehensive suite of services designed according to Microsoft's requirements. Securitas is dedicated to providing the highest level of security when and where it is required. Innovation and technology integration are vital priorities for Securitas to strike a balance between security measures and innovative solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Corporate Risks and Physical Security Threats

- 5.1.2 Organizations' Access Control Requirements have Grown Due to the Prevalence of Remote and Hybrid Work

- 5.1.3 The Accelerated Incorporation of Machine Learning (ML) and Artificial Intelligence (AI)

- 5.2 Market Challenges

- 5.2.1 The Physical Security Systems Vulnerability to Cyber Attacks

- 5.2.2 Rapid Technological Progress Necessitates Frequent System Upgrades

6 MARKET SEGMENTATION

- 6.1 By System Type

- 6.1.1 Video Surveillance System

- 6.1.1.1 IP Surveillance

- 6.1.1.2 Analog Surveillance

- 6.1.1.3 Hybrid Surveillance

- 6.1.2 Physical Access Control System (PACS)

- 6.1.3 Biometric System

- 6.1.4 Perimeter Security

- 6.1.5 Intrusion Detection

- 6.1.1 Video Surveillance System

- 6.2 By Service Type

- 6.2.1 Access Control as a Service (ACaaS)

- 6.2.2 Video Surveillance as a Service (VSaaS)

- 6.3 By Type of Deployment

- 6.3.1 On-Premises

- 6.3.2 Cloud

- 6.4 By Organization Size

- 6.4.1 SMEs

- 6.4.2 Large Enterprises

- 6.5 By End-user Industry

- 6.5.1 Government Services

- 6.5.2 Banking and Financial Services

- 6.5.3 IT and Telecommunications

- 6.5.4 Transportation and Logistics

- 6.5.5 Retail

- 6.5.6 Healthcare

- 6.5.7 Residential

- 6.5.8 Other End-user Industries

- 6.6 By Country

- 6.6.1 United Kingdom

- 6.6.2 Germany

- 6.6.3 France

- 6.6.4 Spain

- 6.6.5 Italy

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Securitas AB

- 7.1.2 Bosch Security Systems GmbH

- 7.1.3 Secom Co. Ltd

- 7.1.4 Dahua Technology Co. Ltd

- 7.1.5 Hanwha Vision Co. Ltd

- 7.1.6 G4S Limited

- 7.1.7 Vanderbilt Industries

- 7.1.8 Siemens AG

- 7.1.9 Teledyne FLIR LLC

- 7.1.10 Genetec Inc.

- 7.1.11 Johnson Controls

- 7.1.12 Hangzhou Hikvision Digital Technology Co. Ltd

- 7.1.13 Schneider Electric SE

- 7.1.14 Honeywell International Inc.

- 7.1.15 Axis Communications AB

- 7.1.16 NEC Corporation

- 7.1.17 HID Global Corporation