|

市場調査レポート

商品コード

1549863

南米のデータセンター電力:市場シェア分析、産業動向・統計、成長予測(2024~2029年)South America Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米のデータセンター電力:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

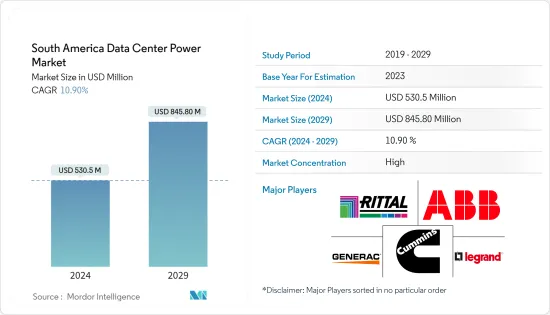

南米のデータセンター電力市場規模は2024年に5億3,050万米ドルと推定され、2029年には8億4,580万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは10.90%で成長する見込みです。

ブラジルのような国では、大規模な太陽光発電と風力発電をハイブリッド発電所として結合させ、地域の持続可能なデータセンターを支える将来性が高いです。2021年、ブラジルのエネルギー規制当局であるANEELは、ハイブリッド発電所の運用に関する新たな規制を承認しました。これにより、ブラジルのデータセンター電力市場には、今後数年間、十分なビジネスチャンスがもたらされると期待されています。同市場では、リチウムイオンUPSやニッケル亜鉛システムの調達も大きく伸びています。プロイセン・ナトリウム・プロバイダーも、データセンターにこれらのバッテリー技術を採用することに強い関心を示しています。

南米のデータセンター建設市場における今後のIT負荷容量は、2029年までに1,800MWに達すると予想されています。

同地域の延床面積は2029年までに780万平方フィート増加すると予想されます。

同地域の総設置ラック数は2029年までに39万2,000ユニットに達すると予想されます。2029年までに最大数のラックが設置されるのはブラジルと予想されます。

南米を結ぶ海底ケーブルは60近くあり、その多くが建設中です。海底ケーブルのひとつであるCarnival Submarine Network-1(CSN-1)は、2025年にサービスを開始する予定です。CSN-1は全長4,500キロで、コロンビアのバランキヤに陸揚げされます。

南米のデータセンター電力市場動向

IT・通信分野が大きなシェアを占める見込み

- 過去10年間、南米はインフラ整備で大きく前進したが、デジタル・エコシステムの状況はさまざまです。固定ブロードバンドの一般的な普及率は低いが、現在では光ファイバー網の導入に向け、地域内のさまざまな国で大きな取り組みが行われています。

- チリ政府は光ファイバー・ネットワークに大規模な投資を行っており、接続は人口の90%以上に達しています。その結果、チリのほとんどの家庭が高速インターネット・サービスを利用できるようになり、利用可能なデジタル・サービスの幅が広がっています。

- 5G接続に関しては、2026年7月31日までに、人口20万人以上のブラジルのすべての自治体が、少なくとも1つのアンテナを備えた5Gネットワークを導入する予定です。2021年10月に行われたブラジルの5G周波数オークションでは、約85億米ドルが調達されました。2035年までにブラジルに5Gを導入すれば、1兆2,000億米ドルの経済効果と3兆米ドルの生産性向上が見込める。ネットワークトラフィックの増加に伴い、データセンターの建設が増加しており、大規模な電源バックアップソリューションの需要が高まっています。

- 伝統的なデータセンターの多くは交流(AC)配電システムを使用しているが、通信データセンターは主に直流(DC)電源で稼働しており、UPSやPDUなどがこれにあたる。テレコム・データセンターは、電力会社から交流で電力を得て、整流器を使って直流に変換し、バッテリーの充電も行っています。

- 南米のデータセンターの平均電力使用効率は1.48 PUEで、効率的なレベルを示しています。このため、電力のバックアップを維持するためには、バックアップ発電機やUPSといった主要な電源が必要となります。

著しい成長を遂げるブラジル

- ブラジルのデジタル経済は、中長期的に成長し続ける可能性を示しています。ブラジル政府は、現地のデータセンター・インフラ整備に大きな役割を果たしています。同政府によると、同国の一般データ保護法(LGPD)は2020年8月に施行されました。これにより、多くの企業がクラウドアクセスをプライベートネットワークに移行し、ユーザーデータ保護を拡張するために暗号化サービスを更新せざるを得なくなると予想されます。

- データのおよそ10~15%は、集中データセンターやクラウドの外で作成・処理されています。しかし、その数は2025年までに60~70%を超えると予想されており、これは世界の動向としてブラジルでも予想されています。このような要因により、発電機、PDU、UPSの電力バックアップ需要が大幅に増加します。

- マイクロソフト、アマゾンウェブサービス、グーグルは、ブラジルの主要なクラウドサービスプロバイダーです。これらのクラウド・サービス・プロバイダーは、既存のコロケーション事業者とワークロードをコロケーションし、新規参入事業者と協力してクラウドベースのサービスを提供します。

- ブラジルでは、サンパウロは最も交通の便が良い都市のひとつであり、デジタル・ビジネスや金融の中心地として利用可能性が高いため、施設開発には有利な立地となっています。また、ブラジルのデータローカライゼーション法Lei Geral de Protecao de Dados Pessoais(LGPD)により、国内で生成されたデータの保存に関するいくつかの規制が可決されたため、同地域では市場への投資が活発化しています。

- 2021年3月、マイクロソフトは"More Brazil "計画の一環として、サンパウロに新たなアベイラビリティゾーンを設けることを発表しました。さらに、同社は2021年末までにゾーンのカバレッジを拡大する計画だった。

- データセンター建設に関しては、2021年12月にScala Data Centersがブラジルに2つのハイパースケールデータセンター施設を建設する計画を発表しました。SP4とSP5の施設は18MWと9MWの電力容量を持ち、それぞれ2022年4月と2022年9月までに稼動する予定です。全体として、上記の要因は電力ソリューションの需要に有利に関係しています。

南米のデータセンター電力業界の概要

南米のデータセンター電力市場は、各プレイヤーの間でやや統合が進んでおり、近年は競合優位性を獲得しています。主なプレーヤーとしては、ABB社、Generac Power Systems社、Cummins社などが挙げられます。圧倒的な市場シェアを持つこれらの大手企業は、地域顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために、戦略的協業イニシアティブを活用しています。

2023年6月、ルグランは業界の次世代インテリジェントラック配電ユニット(PDU)を発表しました。サーバーテクノロジーPRO4XとラリタンPX4ラックPDUは、卓越した可視性、最先端のハードウェア、強化されたセキュリティにより、データセンター電力管理を再定義する態勢を整えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- メガデータセンターとクラウドコンピューティングの導入拡大

- 運用コスト削減需要の高まり

- 市場抑制要因

- 導入・保守コストの高さ

- バリューチェーン/サプライチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- 電力インフラ

- 電気ソリューション

- UPSシステム

- 発電機

- 配電ソリューション

- PDU

- スイッチギア

- クリティカル配電

- 転送スイッチ

- リモートパワーパネル

- その他のソリューション

- サービス

- 電気ソリューション

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- メディア&エンターテイメント

- その他のエンドユーザー

- 国名

- ブラジル

- チリ

第6章 競合情勢

- 企業プロファイル

- ABB Ltd

- Caterpillar Inc.

- Cummins Inc.

- Eaton Corporation

- Legrand Group

- Rolls-Royce PLC

- Vertiv Group Corp.

- Schneider Electric SE

- Rittal GmbH & Co. KG

- Fujitsu Limited

- Cisco Systems Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The South America Data Center Power Market size is estimated at USD 530.5 million in 2024, and is expected to reach USD 845.80 million by 2029, growing at a CAGR of 10.90% during the forecast period (2024-2029).

A country such as Brazil has a strong future for coupling large-scale solar and wind power as hybrid power plants, supporting sustainable data centers in the region. In 2021, the Brazilian energy regulator, ANEEL, approved a new regulation for the operation of hybrid power plants. This, in turn, is expected to provide ample opportunity for Brazil's data center power market in the coming years. The market is also witnessing significant growth in procuring lithium-ion UPS and nickel-zinc systems. Prussian sodium providers also witness strong interest in adopting these battery technologies in data centers.

The upcoming IT load capacity of the South American data center construction market is expected to reach 1,800 MW by 2029.

The region's construction of raised floor area is expected to increase 7.8 million sq. ft by 2029.

The region's total number of racks to be installed is expected to reach 392K units by 2029. Brazil is expected to house the maximum number of racks by 2029.

Close to 60 submarine cable systems are connecting South America, and many are under construction. One submarine cable, Carnival Submarine Network-1 (CSN-1), is estimated to start service in 2025. It stretches over 4500 kilometers and has a landing point in Barranquilla, Colombia.

South America Data Center Power Market Trends

The IT & Telecom Segment is Expected to Hold Significant Share

- Over the past decade, South America has made considerable strides in developing infrastructures, although the status of its digital ecosystem varies. Although general penetration of fixed broadband is low, significant efforts are now being made in the different countries across the region to deploy fiber optic networks.

- The Chilean government has substantially invested in fiber-optic networks, with connections reaching more than 90% of the population. As a result, most Chilean families now have access to high-speed internet services, enabling them to benefit from the expanding range of available digital services.

- Regarding 5G connectivity, all Brazilian municipalities with at least 200,000 residents will have a 5G network by July 31, 2026, with at least one antenna. Brazil's 5G spectrum auction held in October 2021 raised about USD 8.5 billion. By 2035, introducing 5G in Brazil may have a USD 1.2 trillion economic impact and a USD 3 trillion productivity boost. With increasing network traffic, the data center construction is increasing, leading to demand for major power backup solutions.

- While most traditional data centers use alternating current (AC) power distribution systems, telecom data centers run mainly on direct current (DC) power, such as UPS and PDU. Telecom data centers get power from the utility in the AC and convert it to DC using rectifiers, which also charge their batteries.

- South American data centers' average power usage efficiency is 1.48 PUE, indicating an efficient efficiency level. This requires major power sources such as backup generators and UPS to maintain the electricity backup.

Brazil to Hold Significant Growth

- Brazil's digital economy demonstrates the potential for continued growth over the medium and long term. The Brazilian government plays a significant role in developing local data center infrastructure. According to the government, the country's General Data Protection Act (LGPD) was implemented in August 2020. It is expected to force many enterprises to migrate their cloud access to private networks and update their encryption services to extend user data protection.

- Around 10-15% of data is created and processed outside centralized data centers or the cloud. However, the number is expected to surpass 60-70% by 2025, a global trend also expected in Brazil. Such factors will lead to significant power backup demand for generators, PDUs, and UPS.

- Microsoft, Amazon Web Services, and Google are major cloud service providers in Brazil. These cloud service providers will collocate their workloads with existing colocation operators and collaborate with the new market entrants to provide cloud-based services.

- In Brazil, Sao Paulo is one of the most connected cities, with a high availability of digital business and financial centers, making the city a favorable location for facility development. The region is also witnessing a boost in investments in the market due to the Brazilian data localization law, Lei Geral de Protecao de Dados Pessoais (LGPD), which passed some regulations for storing the data generated within the country.

- In March 2021, Microsoft announced new availability zones in Sao Paulo as part of its "More Brazil" plan. In addition, the company planned to expand its zone coverage by the end of 2021.

- Regarding data center construction, in December 2021, Scala Data Centers announced its plan to build two hyperscale data center facilities in Brazil. The SP4 and SP5 facilities will have 18 MW and 9 MW power capacity and are expected to work by April 2022 and September 2022, respectively. Overall, the above factor relates favorably to the demand for power solutions.

South America Data Center Power Industry Overview

The South American data center power market is slightly consolidated among the players and has gained a competitive edge in recent years. A few major players are ABB Ltd, Generac Power Systems Inc., Cummins Inc., etc. These major players, with a prominent market share, focus on expanding their regional customer base. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

In June 2023, Legrand introduced the industry's next generation of intelligent rack power distribution units (PDUs). The Server Technology PRO4X and Raritan PX4 rack PDUs are poised to redefine power management in data centers with exceptional visibility, cutting-edge hardware, and enhanced security.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Mega Data Centers and Cloud Computing

- 4.2.2 Increasing Demand to Reduce Operational Costs

- 4.3 Market Restraints

- 4.3.1 High Cost of Installation and Maintenance

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of the COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Power Infrastructure

- 5.1.1 Electrical Solution

- 5.1.1.1 UPS Systems

- 5.1.1.2 Generators

- 5.1.1.3 Power Distribution Solutions

- 5.1.1.3.1 PDU

- 5.1.1.3.2 Switchgear

- 5.1.1.3.3 Critical Power Distribution

- 5.1.1.3.4 Transfer Switches

- 5.1.1.3.5 Remote Power Panels

- 5.1.1.3.6 Other Solutions

- 5.1.2 Service

- 5.1.1 Electrical Solution

- 5.2 End User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End Users

- 5.3 Country

- 5.3.1 Brazil

- 5.3.2 Chile

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 ABB Ltd

- 6.1.2 Caterpillar Inc.

- 6.1.3 Cummins Inc.

- 6.1.4 Eaton Corporation

- 6.1.5 Legrand Group

- 6.1.6 Rolls-Royce PLC

- 6.1.7 Vertiv Group Corp.

- 6.1.8 Schneider Electric SE

- 6.1.9 Rittal GmbH & Co. KG

- 6.1.10 Fujitsu Limited

- 6.1.11 Cisco Systems Inc.