|

市場調査レポート

商品コード

1549807

南米のデータセンター建設:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)South America Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米のデータセンター建設:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

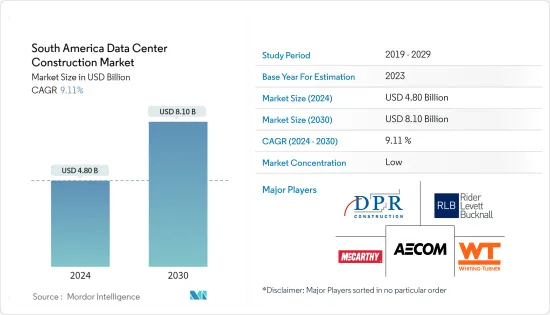

南米のデータセンター建設市場規模は2024年に48億米ドルと推定され、2030年には81億米ドルに達すると予測され、予測期間中(2024~2030年)のCAGRは9.11%で成長すると予測されます。

主要ハイライト

- 南米では、2030年までに建設中のIT負荷容量が1,800MW以上に達すると予想されます。

- 同地域のデータセンター用床面積は、2030年までに700万平方フィートを超えると予測されます。

- この地域で設置されるラックの総数は、2030年までに25万個を超えると予想され、計画中のラック数ではブラジルが最大となります。

- 同地域では、海底ケーブル・プロジェクトが増加しています。そのひとつがカリビアンエクスプレス(CX)で、コロンビアのカルタヘナを陸揚げ点とする全長3,472キロメートルの海底ケーブルです。

- ラテンアメリカは、データセンター市場にとって新興国市場のひとつです。同地域では、政府機関、通信サービス・プロバイダー、公益事業者の努力により、海底ネットワーク接続の設置が増え、データセンター開発の活発化につながっています。ラテンアメリカは68本の海底ケーブルで結ばれており、過去20年間で同地域の容量は5倍に増加しました。ブラジルとチリは、大規模、大規模、中規模施設のデータセンター数が最も多いです。

南米データセンター建設市場の動向

クラウドセグメントが予測期間中に最も急成長する見込み

- クラウドサービスの需要は、ブラジル、チリ、アルゼンチンなどで有望です。アルゼンチンでは、クラウドコンピューティングに関する法規制環境の整備が他の地域諸国と比較して早く、最近の技術動向に沿ったものとなっています。最近、アマゾン・ウェブサービスは、アルゼンチンの新しいデータセンターに10年間で約8億米ドルを投資する計画を発表しました。

- ラテンアメリカデータセンター・ストレージ市場では、クラウドサービス・プロバイダーが主要貢献者となっています。ブラジル、チリ、コロンビア、アルゼンチンなどの国々に複数のクラウド地域を設立してクラウドのプレゼンスを拡大することで、同市場における高性能ストレージの採用が促進されると期待されています。ブラジルの新興企業では、SaaS(Software-as-a-Service)が主要なビジネスモデルとなっており、同国の新興企業の41%以上を占めています。SaaSは、PaaS(Platform-as-a-Service)とIaaS(Infrastructure-as-a-Service)とともに、ブラジルのクラウドコンピューティングの3大カテゴリーの1つです。

- メキシコでは、2018年に企業の48%がクラウド関連の商品やサービスに投資しました。マイクロソフトは2020年、メキシコの発展を支援するため「Innovate for Mexico」を発表しました。この戦略の主要目標は、技術へのアクセスを民主化することで、メキシコのデジタルトランスフォーメーションを早めることです。5年間で11億米ドルの投資計画を実施し、メキシコ国内にクラウドデータセンターを建設します。

- ITセクターは2021年にチリのGDPに2.7%貢献しました。Google、Century Link、Huawei、HPなどの有名企業や、地域の通信事業者であるEntelやGtdが運営する多くのデータセンターがすでにチリにあります。さらに多くの企業が参入する中、コロンビアは次のラテンアメリカ主要市場として浮上しています。Huaweiは、クラウドインフラ専用の物理的な拠点を対象としており、コロンビアで新たなクラウドポイント・オブ・プレゼンス(PoP)を稼動させる予定です。アルゼンチン政府は、ARSATの堅牢な国立データセンターに投資し開発することで、「クラウドファースト」ポリシーを実施しています。全体として、ラテンアメリカクラウドデータセンター市場は大幅な成長が見込まれています。

データセンター建設はブラジルが主流と予測

- ブラジルとチリが南米最大のデータセンター市場シェアを占めています。ブラジル政府は、Regime Especial de Tributacao do Programa Nacional de Banda Larga(REPNBL)プログラムを通じてインセンティブを提供しており、これには国内のコロケーションサービスの向上に役立つインフラ購入に対するインセンティブが含まれています。

- リオデジャネイロは、2023年にブラジルの公共データ処理とIT事業体への投資を主導する見込みで、同州のProderjは当初、ICTサービスと拡大のために5億9,200万BRL近くを予定していました。2023年1月、ブラジルの通信サービス会社Telecallは、リオデジャネイロの主要データセンターを相互接続する光ファイバー網の拡大計画を発表しました。Telecallは、リオデジャネイロに設置される少なくとも4つの新しいデータセンターを接続するため、新たに3つの冗長化された合計80kmの地下光ファイバールートを展開します。全体として、ブラジルはデータセンター立地の主要拠点となっています。

- チリは、今後数年間で再生可能エネルギー発電の可能性を活用する計画により、競合エネルギー価格を実現しています。エネルギーコストは5年前の3分の1にまで下がりましたが、これは主に、現在総発電量の46%を占める再生可能エネルギーによるものです。

- チリは伝統的にこの地域で最も優れた通信インフラを有しており、完全に冗長化されたファイバー・バックボーンを確保するため、2つの大規模なファイバー・プロジェクトが進行中です。これには、深南部とGtdの南北3,500kmの海底ケーブルを結ぶ国営のFibra Optica Austral(FOA)海底ケーブルが含まれます。2022年には、Scala Data Centers、ODATA、Ascenty(Digital Realty)、EdgeConneXなどのコロケーション事業者が、チリのデータセンター市場への主要な投資家となりました。

- チリは競合エネルギー価格を持っていますが、これは主に、今後数年間で自然再生可能エネルギー発電の可能性を活用する計画によって後押しされたものです。エネルギーコストは5年前の3分の1にまで下がり、その主要要因は、現在総発電量の46%を占める再生可能エネルギーです。チリは伝統的にこの地域で最も優れた通信インフラを有しており、完全に冗長化されたファイバー・バックボーンを確保するため、2つの大規模なファイバー・プロジェクトが進行中です。これには、深南部とGtdの南北3,500kmの海底ケーブルを結ぶ国営のFibra Optica Austral(FOA)海底ケーブルが含まれます。2022年には、Scala Data Centers、ODATA、Ascenty(Digital Realty)、EdgeConneXなどのコロケーション事業者が、チリのデータセンター市場への主要投資家となっていました。

南米データセンター建設産業概要

南米のデータセンター建設市場はかなり細分化されており、 AECOM、DRP Construction、Fortis Construction、Rider Levett Bucknall、Mercury Engineeringのような主要企業が存在します。市場参入企業は、買収や提携など、さまざまな戦略を採用して、商品ラインナップを充実させ、市場での競合を維持しようとしています。

2024年2月、ラテンアメリカで著名なデータセンター運営会社ODataは、メキシコでの存在感を大幅に高めています。アラインド傘下の同社は、ケレタロにある既存のQR01データセンターの拡大計画を明らかにしました。さらに、ODataはメキシコで2つの新しいハイパースケールデータセンターキャンパスの建設を開始しました。1つ目はグアナファトに位置し、QR02キャンパスとして知られ、30MWの容量を提供する予定です。2つ目のQR03キャンパスはエル・マルケスに位置し、150MWの容量を提供する予定です。

2024年5月、Equinixは、ブラジルのリオデジャネイロにある3番目のデータセンターに9,400万米ドルを投資します。リオデジャネイロのボタフォゴ地区から約30キロメートル離れたサン・ジョアン・デ・メリティ自治体に位置するRJ3は、2025年の開設を予定しています。広さ1467平方メートル(15,800平方フィート)の同センターには、コロケーションサービス用に560のラックが設置される予定で、さらなる仕様はまだ明らかにされていないです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

- 調査の枠組み

- 2次調査

- 1次調査

- データの三角測量と洞察の生成

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 市場力学

- 市場促進要因

- クラウドアプリケーション、AI、ビッグデータの成長

- ハイパースケールデータセンターの採用増加

- 市場抑制要因

- 電力コストと不動産コストの増加

- 市場促進要因

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 主要データセンター建設統計

- 南米のデータセンター数(2022年と2023年)

- 南米におけるデータセンター建設中容量(MW)(2024~2029年)

- 南米データセンター建設市場の平均CAPEXとOPEX

- データセンターの電力吸収量(MW)(特定国):南米、2022年と2023年

- 南米におけるデータセンターインフラへのCAPEX支出上位国

第5章 市場セグメンテーション

- 市場セグメンテーション-インフラ別

- 市場セグメンテーション:電気インフラ別

- 配電ソリューション

- PDU-ベーシック &スマート-メータード &スイッチドソリューション

- 転送スイッチ

- 静的

- 自動(ATS)

- 開閉装置

- 低圧

- 高圧

- パワーパネルとコンポーネント

- その他の配電ソリューション

- 電源バックアップソリューション

- UPS

- 発電機

- サービス-デザイン&コンサルティング、インテグレーション、サポート&メンテナンス

- 市場セグメンテーション:機械インフラ別

- 冷却システム

- 液浸冷却

- ダイレクト・ツー・チップ冷却

- リアドア熱交換器

- インローとインラック冷却

- ラック

- その他の機械インフラ

- 一般構造

- 市場セグメンテーション:電気インフラ別

- 市場セグメンテーション:ティアタイプ別

- ティアIとII

- ティアIII

- ティアIV

- 市場セグメンテーション:エンドユーザー別

- 銀行、金融サービス、保険

- IT・通信

- 政府・防衛

- 医療

- その他

- 市場セグメンテーション-地域別

- ブラジル

- チリ

- その他の南米

第6章 競合情勢

- 企業プロファイル

- AECOM

- Whiting-turner Contracting Company

- Turner Construction Co.

- Jacobs Solutions Inc.

- DPR Construction

- Rider Levett Bucknall

- Balfour Beatty US

- Hensel Phelps

- McCarthy Building Companies

- Gilbane Building Company

- Fonseca Mercadante Constructor

- Mercury Engineering

第7章 投資分析

第8章 市場機会と今後の動向

第9章 出版社について

The South America Data Center Construction Market size is estimated at USD 4.80 billion in 2024, and is expected to reach USD 8.10 billion by 2030, growing at a CAGR of 9.11% during the forecast period (2024-2030).

Key Highlights

- The upcoming IT load capacity in South America is expected to reach more than 1,800 MW by 2030 for under construction IT load capacity.

- The construction of raised floor area for data centers in the region is expected to reach more than 7 million sq. ft by 2030 for under construction raised floor space.

- The region's total number of racks to be installed is expected to reach above 250,000 units by 2030, with Brazil expected to house the maximum number of racks by that time for planned racks.

- The region is witnessing rising submarine cable projects. One such submarine cable, estimated to start service in 2025, is Caribbean Express (CX), stretching over 3,472 kilometers with landing points from Cartagena, Colombia, for planned submarine cables.

- Latin America is one of the developing regions for the data center market. The region is seeing more installations of submarine network connectivity, leading to higher data center development driven by efforts from government agencies, telecommunication service providers, and utility providers. Latin America is connected by 68 submarine cables, which has increased the region's capacity five-fold in the last 20 years. Brazil and Chile have the highest number of data centers in terms of massive, large, and medium-sized facilities.

South America Data Center Construction Market Trends

Cloud Segment Expected to Grow Fastest During the Forecasted Period

- The demand for cloud services is promising in Brazil, Chile, Argentina, and other countries. In Argentina, the evolution of the legal and regulatory environment for cloud computing has been faster and more in line with recent technological developments compared to other regional countries. Recently, Amazon Web Services announced plans to invest approximately USD 800 million over a decade in a new data center in Argentina.

- Cloud service providers are the main contributors to Latin America's data center storage market. Expanding cloud presence through establishing multiple cloud regions across countries like Brazil, Chile, Colombia, and Argentina is expected to drive high-performance storage adoption in the market. Software-as-a-service (SaaS) was the leading business model of Brazilian startups, accounting for more than 41% of emerging companies in the country. With platform-as-a-service (PaaS) and infrastructure-as-a-service (IaaS), SaaS is one of Brazil's three principal categories of cloud computing.

- In Mexico, 48% of businesses made investments in cloud-related goods and services in 2018. Microsoft announced "Innovate for Mexico" in 2020 to aid in the development of the country. The primary goal of the strategy is to hasten Mexico's digital transformation through democratizing access to technology. The corporation's five-year USD 1.1 billion investment plan would be implemented to build an area for cloud data centers in the country.

- The IT sector contributed 2.7% to Chile's GDP in 2021. Many data centers run by well-known companies, like Google, Century Link, Huawei, and HP, as well as regional telcos Entel and Gtd, are already located in Chile. As more players enter, Colombia is emerging as the next major Latin American market. Huawei targets a dedicated physical location for its cloud infrastructure and is expecting to activate a new cloud point-of-presence (PoP) in Colombia. The Argentine government is implementing a 'cloud first' policy by investing in and developing a robust national data center at ARSAT. Overall, the Latin American market for cloud data centers is expected to grow significantly.

Brazil is Projected to Witness Majority Data Center Construction Activities

- Brazil and Chile hold the largest South American data center market shares. The Brazilian government provides incentives through the Regime Especial de Tributacao do Programa Nacional de Banda Larga (REPNBL) program, which includes incentives for purchasing infrastructure that help improve colocation services in the country.

- Rio de Janeiro is expected to lead investments in public data processing and IT entities in Brazil in 2023, with close to BRL 592 million initially earmarked by the state's Proderj company for ICT services and expansions. In January 2023, Brazilian telecom services company Telecall announced plans to expand its fiber optics network to interconnect the main data centers in Rio de Janeiro. The three new redundant and underground fiber routes, totaling 80 km, will be deployed by Telecall to connect at least four new data centers that are being installed in Rio de Janeiro. Overall, Brazil is a major hub for data center locations.

- Chile has competitive energy prices, primarily fueled by plans to take advantage of its natural renewable energy generation potential over the coming years. Energy costs have dropped to one-third of what they were five years ago, mainly based on renewable energy that now makes up 46% of the total produced.

- Chile traditionally has some of the region's best telecommunications infrastructure, and two major fiber projects are underway to ensure it will have a fully redundant fiber backbone. These include the state-funded Fibra Optica Austral (FOA) submarine cable connecting the deep south and Gtd's 3,500 km north-south submarine cable. In 2022, colocation operators, such as Scala Data Centers, ODATA, Ascenty (Digital Realty), and EdgeConneX, were the major investors in the Chilean data center market.

- Chile has competitive energy prices, primarily fueled by plans to take advantage of its natural renewable energy generation potential over the coming years. Energy costs have dropped to one-third of what they were five years ago, mainly based on renewable energy that now makes up 46% of the total produced. Chile traditionally has some of the region's best telecommunications infrastructure, and two major fiber projects are underway to ensure it will have a fully redundant fiber backbone. These include the state-funded Fibra Optica Austral (FOA) submarine cable connecting the deep south and Gtd's 3,500 km north-south submarine cable. In 2022, colocation operators, such as Scala Data Centers, ODATA, Ascenty (Digital Realty), and EdgeConneX, were the major investors in the Chilean data center market.

South America Data Center Construction Industry Overview

The South American data center construction market is fairly fragmented, with significant players such as AECOM, DRP Construction, Fortis Construction, Rider Levett Bucknall, and Mercury Engineering. The market players are adopting various strategies, including acquisitions and partnerships, to enhance their product offerings and remain competitive in the market.

February 2024: OData, a prominent data center operator in Latin America, was seen significantly increasing its presence in Mexico. The company, owned by Aligned, revealed plans to expand its existing QR01 data center in Queretaro. Moreover, OData commenced the construction of two new hyperscale data center campuses in Mexico. The first, located in Guanajuato, will be known as the QR02 campus and is set to provide a capacity of 30 MW. The second campus, QR03, situated in El Marques, is slated to offer an impressive 150 MW.

May 2024: Equinix is injecting USD 94 million into its third data center in Rio de Janeiro, Brazil. Situated in the Sao Joao de Meriti municipality, approximately 30 km from the Botafogo neighborhood in the capital, the RJ3 facility is slated for a 2025 debut. Spanning 1467 sq. m (15,800 sq. ft), the center will house 560 racks for colocation services, with further specifications yet to be revealed.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Growing Cloud Applications, AI, and Big Data

- 4.2.1.2 Rising Adoption of Hyperscale Data Centers

- 4.2.2 Market Restraints

- 4.2.2.1 Increase in Power and Real Estate Costs

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Key Data Center Construction Statistics

- 4.4.1 Number of Data Centers in South America, 2022 and 2023

- 4.4.2 Data Center Under Construction in South America, in MW, 2024-2029

- 4.4.3 Average CAPEX and OPEX For South America Data Center Construction Market

- 4.4.4 Data Center Power Capacity Absorption in MW, Selected Countries, South America, 2022 and 2023

- 4.4.5 Top CAPEX Spenders on Data Center Infrastructure in South America

5 MARKET SEGMENTATION

- 5.1 Market Segmentation - By Infrastructure

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.1.1.1 Power Distribution Solution

- 5.1.1.1.1 PDU - Basic & Smart - Metered & Switched solutions

- 5.1.1.1.2 Transfer Switches

- 5.1.1.1.2.1 Static

- 5.1.1.1.2.2 Automatic (ATS)

- 5.1.1.1.3 Switchgear

- 5.1.1.1.3.1 Low-Voltage

- 5.1.1.1.3.2 Medium-Voltage

- 5.1.1.1.4 Power Panels and Components

- 5.1.1.1.5 Other Power Distribution Solutions

- 5.1.1.2 Power Back-up Solutions

- 5.1.1.2.1 UPS

- 5.1.1.2.2 Generators

- 5.1.1.3 Service - Design & Consulting, Integration, Support & Maintenance

- 5.1.2 Market Segmentation - By Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.1.1 Immersion Cooling

- 5.1.2.1.2 Direct-To-Chip Cooling

- 5.1.2.1.3 Rear Door Heat Exchanger

- 5.1.2.1.4 In-Row and In-Rack Cooling

- 5.1.2.2 Racks

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.3 General Construction

- 5.1.1 Market Segmentation - By Electrical Infrastructure

- 5.2 Market Segmentation - By Tier Type

- 5.2.1 Tier-I and II

- 5.2.2 Tier-III

- 5.2.3 Tier-IV

- 5.3 Market Segmentation - By End User

- 5.3.1 Banking, Financial Services, and Insurance

- 5.3.2 IT and Telecommunications

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Other End Users

- 5.4 Market Segmentation - By Geography

- 5.4.1 Brazil

- 5.4.2 Chile

- 5.4.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AECOM

- 6.1.2 Whiting-turner Contracting Company

- 6.1.3 Turner Construction Co.

- 6.1.4 Jacobs Solutions Inc.

- 6.1.5 DPR Construction

- 6.1.6 Rider Levett Bucknall

- 6.1.7 Balfour Beatty US

- 6.1.8 Hensel Phelps

- 6.1.9 McCarthy Building Companies

- 6.1.10 Gilbane Building Company

- 6.1.11 Fonseca Mercadante Constructor

- 6.1.12 Mercury Engineering