|

市場調査レポート

商品コード

1693700

インドのソフトウェアサービス輸出-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Software Services Export - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのソフトウェアサービス輸出-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 143 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

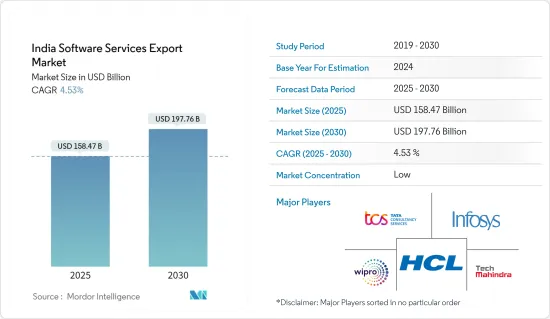

インドのソフトウェアサービス輸出市場規模は、2025年に1,584億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.53%で、2030年には1,977億6,000万米ドルに達すると予測されます。

北米や欧州諸国におけるクラウド変革は高コストを伴い、適切なリソースが不足しているため、オフショアリングやアウトソーシングの最前線にあり、新たな動向、技術、技術を更新しているインドが選ばれています。このような要因が、予測期間中の市場拡大に寄与するとみられます。

主要ハイライト

- 産業全体でデジタルトランスフォーメーションが急速に進み、IoT、AI、ブロックチェーンなどの新技術が採用され、非中核業務をアウトソーシングすることでコアコンピタンスを活用することが重視されるようになっていることが、市場の主要促進要因となっています。

- インド企業がデジタル変革のためにクラウド、人工知能(AI)、自動化、ネットワークインフラ、モノのインターネット(IoT)、その他の先進技術に傾倒する中、デジタルトランスフォーメーション(DX)とITの近代化への支出はインド企業の最優先課題となっています。

- クラウドサービスへの移行が進んでいることは、調査対象市場の重要な促進要因であり、その結果、そこから収益を生み出す重要な協力関係が生まれています。クラウドへの移行により、大企業も中小企業もソフトウェアアプリケーション、データベース、その他のITリソースをクラウドサーバーに移行し、シームレスで安全かつ透明性の高いシステムを実現できます。これにより、企業のソフトウェア開発ライフサイクルプロセス管理がより効率的になります。企業は一般的に、より優れたスケーラビリティ、可用性、ソフトウェアサービスの迅速な展開のために、クラウド移行戦略に投資します。

- ソフトウェア製品に関するインドの国家施策は、ソフトウェア製品のエコシステムをサポートするために承認された次世代インキュベーション・スキーム(NGIS)によって部分的に対処されています。強力なITセクタの持続的拡大、新たな雇用創出、競合向上を支援するため、盛んなソフトウェア製品エコシステムを構築することが計画されています。NASSCOMの試算によると、インドのソフトウェア製品産業は2023年度の売上高で歴史的な成果を上げ、142億米ドルに達しました。

- しかし、規制やコンプライアンス・ニーズの管理といった要因が、予測期間中の市場成長を抑制する可能性があります。これは、運用コストの増加、厳格なデータ保護法によるサービス提供の制限、変化し進化する規制への絶え間ない適応の必要性によるイノベーションと拡大努力からのリソースの流用を伴うからです。

- さらに、COVID-19の大流行後、いくつかの企業では従業員が在宅勤務をするようになり、効率的なITシステムを導入する必要性が大幅に高まっています。アプリケーションやソフトウェアをクラウドやクラウドベースのプラットフォームに移行する組織も増えています。このような状況は、調査対象市場の成長機会を大幅に増大させています。

インドのソフトウェアサービス輸出市場動向

インフラ近代化、デジタルサポート、クラウドサービスに対する需要の増加

- インフラの近代化には、パフォーマンス、拡大性、セキュリティの向上を目的とした組織のITセットアップの強化が含まれます。これには、古いシステムからクラウドベースのプラットフォームへの移行、コンテナ化の採用、自動化とDevOps手法の統合などが含まれます。主要目的は、俊敏性を高め、運用コストを削減し、デジタルトランスフォーメーションを促進し、企業が技術動向や顧客ニーズを先取りできるようにすることです。

- サイバーセキュリティ、運用効率、コスト効率を重視する傾向が強まっていることが、インフラの近代化を後押ししています。このような強化により、インドのソフトウェアサービスプロバイダは、世界の顧客の進化する要求に応えるだけでなく、高品質で革新的かつ安全なソリューションを提供することで、国際市場での競合を維持することができます。

- インドは先進市場経済諸国への移行を進めており、先進技術の導入はこのプロセスにおいて重要な役割を果たすと期待されています。さらに、インドの財務大臣は、同国の中間予算において、現代における経済の正式化を推進する上でのインドのデジタルインフラを強調しています。Vi Business(Vodafone Ideaの傘下)の最近の調査によると、約1,000社のMSMEは、さまざまな業種にわたってデジタル化を受け入れている企業は60%以下であると回答しています。

- 電子情報技術省(Ministry of Electronics and Information Technology)によると、インドのIT/ITeS産業は世界的に重要な地位を占めており、輸出と雇用創出を大幅に促進しています。国内のIT-BPM部門(eコマースを除く)の評価額は2,540億米ドルに達し、2023~24会計年度の輸出額は約2,000億米ドルに達する見込みです(推定)。また、IT-ITeS産業は雇用を大幅に強化し、約543万人の専門家を雇用すると予想されています。これは前年度(2022~2023年度)から6万人の増加を意味します。特筆すべきは、女性がこの産業の労働人口の36%を占めていることです。

- 市場関係者は、企業のデジタルトランスフォーメーションIT戦略の構築を支援しています。例えば、2024年3月、タタコンサルタンシー・サービシズは、デンマークに本社を置くアーキテクチャー、エンジニアリング、コンサルタント会社であるランボル社のエンド・ツー・エンドのIT変革を支援するため、数百万米ドルの戦略的パートナーシップを締結することを宣言しました。同社は、ランボルのITオペレーティングモデルを近代化・合理化し、今後7年間でITの事業成長を目指します。

ITサービスが大きな市場シェアを獲得する見込み

- 多くの国々は、人件費を節約するために、IT業務をインドのような新興経済諸国に輸出してきました。インドにはITサービス輸出の大手企業が多数進出しており、ITサービス輸出の需要は今後数年で大きく勢いを増すと予想されます。世界のデジタルトランスフォーメーションに伴い、企業はレガシーITインフラを急速にアップグレードしているため、インドではITコンサルティングやインプリメンテーションサービスの需要が生じています。デジタルトランスフォーメーションは、ITサービスとその重要性を決定し、ITサービスを計画・構築・実行のフレームワークの活動としてさらに組織化し、組織のITサービス戦略を定義するという点で、企業に戦略的・競争的優位性を記載しています。

- インドにおけるITサービスの状況は急速に変化しています。様々なエンドユーザー産業におけるビッグデータや機械学習のような先端技術の普及は、ITインフラの更新の必要性を煽っています。また、このような新技術の採用により、企業は時代遅れのインフラやハードウェアを置き換えることが可能となり、インドにおけるITサービスセグメントの成長を牽引しています。さらに、クラウドベースのプラットフォームにおけるIT運用の進歩により、ITサービスはよりデータ主導でリアルタイムなものとなり、特に業務効率化、ビジネス機会の発見、リモートアクセスの最適化など、ビジネスに大きな価値を生み出しています。NASSCOMのデータによると、先進的で近代的なデジタルインフラへの投資により、インドの技術部門は2,450億米ドルの成長を遂げました。

- さらに、クラウドコンピューティングは、企業、政府、消費者を変革する技術として想定されています。クラウドコンピューティングはデジタルトランスフォーメーションをサポートするだけでなく、ITエコシステムの参入企業間のイノベーションとコラボレーションを可能にします。国際貿易局によると、ICTセクタとデジタル経済は合わせてインドのGDPの13%以上を占め、極めて重要な経済の柱となっています。インドは野心的な目標を掲げており、2025年までにICTセクタの評価額を1兆米ドルに引き上げることを目指しています。

- また、ITサービスプロバイダは、さまざまなエンドユーザー企業とパートナーシップを結び、先進技術の導入を支援しています。2024年2月、Wiproはアグネの大株主になることを発表しました。この動きにより、Wiproはアグネの先進的技術と専門知識を利用できるようになり、損害保険産業における地位が強化されました。Wiproとアグネの統合された能力は、技術を活用し、損害保険産業の顧客により迅速な市場投入と競合サービスを提供するのに役立つと考えられます。

- さらに、加入者数の増加により、CRM、課金、ネットワーク管理システムなど、電気通信に特化したソフトウェアソリューションの需要が高まり、市場の成長を大きく後押ししています。接続性と通信機能の強化により、リモートコラボレーションやアウトソーシングの機会が増加し、ソフトウェアサービスプロバイダは世界にサービスを提供できるようになります。さらに、通信の進歩は革新的なアプリケーションやデジタルサービスの開発を促進し、ソフトウェア輸出企業の市場機会を拡大します。このような電気通信の拡大とソフトウェア需要の相乗効果が、市場の成長を大きく促進しています。TRAIによると、2023年12月現在、インドのデリーにおける都市部の電気通信加入者は5,800万人を超えており、測定期間中のインド全土の都市部電気通信加入者総数は6億6,200万人を超えています。

インドのソフトウェアサービス輸出産業概要

インドのソフトウェアサービス輸出産業市場はセグメント化されています。Tata Consultancy Services Limited、Infosys Limited、Wipro Limited、HCL Technologies、Tech Mahindra Ltdなどが主要企業です。各社は市場シェアを維持するため、技術革新と戦略的提携を続けています。

- 2024年4月:HCL TechはGoogle Cloudとの提携を発表し、産業ソリューションを確立し、マルチモーダル大規模言語AIモデルのGeminiを展開します。HCLは、エンジニアが効率的にコーディングし、問題を解決し、納期を短縮し、顧客のソフトウェアプロジェクトの品質を高めることを可能にするGeminiの先進的コード補完と要約機能で、HCL Tech AI Forceプラットフォームを強化することを計画しました。

- 2024年2月:技術サービスとコンサルティング会社であるWipro・リミテッドは、Wipro・エンタープライズ人工知能(AI)-Ready Platformを立ち上げ、顧客が企業レベルの完全に統合され、カスタマイズ型AI環境を構築できるようにしました。このプラットフォームは、自動化のためのAIと生成AIワークロードの消費、予測分析を用いて変化するワークロードを動的に調整する動的リソース管理、企業におけるインシデント削減と業務効率の改善への投資に必要なインフラとコアソフトウェアを記載しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- マクロ経済動向が市場に与える影響

第5章 市場力学

- 市場の促進要因

- パンデミック課題によるインフラ近代化、デジタルサポート、クラウドサービスに対する需要の増加

- コンプライアンス削減、生産性向上、国際競合強化を実現したIT産業を支援する政府改革

- 市場抑制要因

- 世界各地の規制とコンプライアンス・ニーズの管理

- ソフトウェアサービスの動向と技術開発

- 地域分析

- カルナータカ州

- タミルナドゥ州

- テランガナ州

- マハラシュトラ州

- ウッタル・プラデシュ州

- ハリヤナ州

第6章 市場セグメンテーション

- 活動別

- ITサービス

- ソフトウェア製品開発

- BPOサービス

- エンジニアリングサービス

- サービスタイプ別

- オンサイト

- オフサイト

- 輸出先別

- 北米

- 欧州

- アジア太平洋

- その他

第7章 競合情勢

- 企業プロファイル

- Tata Consultancy Services Limited

- Infosys Limited

- Wipro Limited

- HCL Technologies

- Tech Mahindra Ltd

- Mphasis Limited

- Oracle Corporation

- LTIMindtree Limited

- Microsoft Corporation

- Capgemini Technology Services India Ltd

- IBM Corporation

- Accenture PLC

- Deloitte Touche Tohmatsu Limited

- PWC LLP

第8章 キャプチャー企業リスト

第9章 アドバイザリー会社リスト

第10章 投資分析

第11章 市場の将来

The India Software Services Export Market size is estimated at USD 158.47 billion in 2025, and is expected to reach USD 197.76 billion by 2030, at a CAGR of 4.53% during the forecast period (2025-2030).

As the cloud transformation in the North American and European nations involves high costs and lacks proper resources, India is preferred as it is at the forefront of offshoring and outsourcing and is updated with emerging trends, techniques, and technology. This factor is expected to contribute to the market's expansion during the forecast period.

Key Highlights

- Rapidly increasing digital transformation across industries, adoption of new technologies such as IoT, AI, and blockchain, and a growing emphasis on leveraging the core competencies by outsourcing non-core operations are the major driving factors of the market.

- As Indian organizations gravitate toward the cloud, artificial intelligence (AI), automation, network infrastructure, Internet of Things (IoT), and other developed technologies to transform them digitally, spending on digital transformation (DX) and IT modernization are the top priorities of Indian companies.

- The growing migration to cloud services is a crucial driving factor in the market studied, resulting in significant collaborations generating revenue from it. Cloud migration facilitates both large and small businesses to move their software applications, databases, and other IT resources to cloud servers for seamless, secure, and transparent systems. This allows the company's software development lifecycle process management to be more efficient. Businesses generally invest in cloud migration strategies for better scalability, availability, and quicker deployment of software services.

- The Indian National Policy on Software Products has been addressed partly by the Next Generation Incubation Scheme (NGIS), which has been approved to support the software product ecosystem. It is planned to build a thriving software product ecosystem to support the strong IT sector's sustained expansion, new job creation, and competitiveness improvement. As per NASSCOM estimate, the Indian Software Product industry has made historic achievements in revenue in FY 2023, reaching USD 14.2 billion.

- However, factors like managing regulatory and compliance needs can restrain the market's growth during the forecast period. It is because this involves increasing operational costs, limiting service offerings due to stringent data protection laws, and diverting resources from innovation and expansion efforts due to the constant need to adapt to varying and evolving regulations.

- Furthermore, after the COVID-19 pandemic, several businesses have employees working from home, and the need to adopt efficient IT systems has increased substantially. Organizations have increasingly migrated to the cloud or cloud-based platforms for their applications and software. This situation has significantly augmented the growth opportunities for the market studied.

India Software Services Export Market Trends

Increasing Demand for Infrastructure Modernization, Digital Support, and Cloud Services

- Infrastructure modernization involves enhancing an organization's IT setup for better performance, scalability, and security. This encompasses transitioning from older systems to cloud-based platforms, embracing containerization, and integrating automation and DevOps methodologies. The primary goal is to boost agility, cut operational expenses, and facilitate digital transformation, empowering businesses to stay ahead of tech trends and customer needs.

- The increasing emphasis on cybersecurity, operational efficiency, and cost-effectiveness is driving the push for infrastructure modernization. These enhancements empower Indian software service providers to not only meet the evolving demands of global clients but also to stay competitive in the international market by delivering high-quality, innovative, and secure solutions.

- India is on a journey to transition into a developed market economy and advanced technology deployment, which is expected to play a significant part in this process. Moreover, India's Finance Minister has emphasized India's digital infrastructure in driving economic formalization in the modern era in the country's interim budget. According to a recent survey by Vi Business (the Arm of Vodafone Idea), nearly one lakh MSMEs said that less than 60% of businesses had embraced digitalization across various verticals.

- As per the Ministry of Electronics and Information Technology, India's IT/ITeS industry holds a significant global position, significantly bolstering exports and job creation. The nation's IT-BPM sector (excluding e-commerce) is poised to hit a valuation of USD 254 billion, with exports making up approximately USD 200 billion in the fiscal year 2023-24 (estimated). The IT-ITeS industry has also significantly bolstered employment and is anticipated to employ a total workforce of around 5.43 million professionals. This marks an increase of 60,000 individuals from the previous fiscal year (FY 2022-2023). Notably, women constitute 36% of the industry's workforce.

- The market players are helping companies build their digital transformation IT strategies. For instance, in March 2024, Tata Consultancy Services declared the multimillion-dollar strategic partnership to support the end-to-end IT transformation of Ramboll, an architecture, engineering, and consultancy company headquartered in Denmark. The company would modernize and streamline Ramboll's IT operating model to strive for business growth in IT over the next seven years.

IT Services Expected to Capture Significant Market Share

- Many countries have long exported IT work to developing economies like India to save on labor costs. With the country housing many major IT service export players, the demand for IT services export is expected to gain significant momentum in India in the coming years. In the wake of digital transformation worldwide, companies are rapidly upgrading their legacy IT infrastructure, thus creating demand for IT consulting and implementation services in India. Digital transformation provides companies with a strategic and competitive advantage in terms of determining IT services and their importance, further organizes the IT services as an activity of a plan-build-run framework, and defines the IT service strategy for the organization.

- The landscape of IT services in India is changing rapidly. The proliferation of advanced technologies, like big data and machine learning in various end-user industries, fuels the need for updated IT infrastructure. In addition, this adoption of emerging technologies enables businesses to replace outdated infrastructure and hardware, driving the IT services segment's growth in India. Moreover, due to advancements in IT operation across the cloud-based platform, IT services have become more data-driven and real-time, creating greater value for the business, especially in operational efficiency, business opportunity discovery, and remote access optimization. As per data by NASSCOM, the technology sector grew by USD 245 billion in India due to investments in advanced and modern digital infrastructure.

- Furthermore, cloud computing is envisioned as a transformative technology for enterprises, governments, and consumers. It not only supports digital transformation but also enables innovation and collaboration among the IT ecosystem players. According to the International Trade Administration, the ICT sector and the digital economy collectively account for over 13% of India's GDP, making them pivotal economic pillars. India has set an ambitious target, aiming to elevate the ICT sector to a USD 1 trillion valuation by 2025, representing a significant 20% of the projected GDP.

- In addition, IT service providers are indulging in partnerships with various end-user companies to assist them with advanced technology implementation. In February 2024, Wipro announced becoming a majority shareholder in Aggne. This move strengthens Wipro's position in the property and casualty (P&C) insurance industry by giving them access to Aggne's advanced technology and expertise. The integrated capabilities of Wipro and Aggne will help leverage technologies to deliver faster speed-to-market and more competitive services to clients in the P&C sector.

- Furthermore, the rising number of telecom subscribers is driving the market's growth significantly, as it increases the demand for telecom-specific software solutions, such as CRM, billing, and network management systems. Enhanced connectivity and communication capabilities boost remote collaboration and outsourcing opportunities, enabling software service providers to deliver their services globally. In addition, telecom advancements promote the development of innovative applications and digital services, expanding market opportunities for software exporters. This synergy between telecom expansion and software demand fuels the growth of the market significantly. According to TRAI, as of December 2023, there were over 58 million urban telecom subscribers in Delhi, India, and the total number of urban telecom subscribers across India during the measured time period was more than 662 million.

India Software Services Export Industry Overview

The Indian software services export industry market is fragmented. Tata Consultancy Services Limited, Infosys Limited, Wipro Limited, HCL Technologies, and Tech Mahindra Ltd are among the major companies. The corporations continue to innovate and form strategic partnerships to maintain their market share.

- April 2024: HCL Tech announced an alliance with Google Cloud to establish industry solutions and deploy Gemini for its multimodal large-language AI model. HCL planned to boost the HCL Tech AI Force platform with Gemini's advanced code completion and summarization capabilities, which allow engineers to code efficiently, solve issues, reduce delivery time, and enhance the quality of software projects for clients.

- February 2024: Wipro Limited, a technology services and consulting company, launched the Wipro Enterprise Artificial Intelligence (AI)-Ready Platform to help clients create enterprise-level, fully integrated, and customized AI environments. This platform provides the necessary infrastructure and core software for the consumption of AI and generative AI workloads for automation, dynamic resource management to adjust to varying workloads using predictive analytics dynamically, and investment in improvements in incident reduction and operational efficiency in the enterprise.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Infrastructure Modernization, Digital Support, and Cloud Services Owing to Pandemic Challenges

- 5.1.2 Government Reforms Aiding IT Industry that has Reduced Compliance, Increased Productivity, and Increased Global Competitiveness

- 5.2 Market Restraints

- 5.2.1 Managing Regulatory and Compliance Needs Across the World

- 5.3 Trends and Technology Developments in Software Services

- 5.4 Regional Analysis

- 5.4.1 Karnataka

- 5.4.2 Tamil Nadu

- 5.4.3 Telangana

- 5.4.4 Maharashtra

- 5.4.5 Uttar Pradesh

- 5.4.6 Haryana

6 MARKET SEGMENTATION

- 6.1 By Activity

- 6.1.1 IT Services

- 6.1.2 Software Product Development

- 6.1.3 BPO Services

- 6.1.4 Engineering Services

- 6.2 By Services Type

- 6.2.1 On-site

- 6.2.2 Off-site

- 6.3 By Export Destination

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tata Consultancy Services Limited

- 7.1.2 Infosys Limited

- 7.1.3 Wipro Limited

- 7.1.4 HCL Technologies

- 7.1.5 Tech Mahindra Ltd

- 7.1.6 Mphasis Limited

- 7.1.7 Oracle Corporation

- 7.1.8 LTIMindtree Limited

- 7.1.9 Microsoft Corporation

- 7.1.10 Capgemini Technology Services India Ltd

- 7.1.11 IBM Corporation

- 7.1.12 Accenture PLC

- 7.1.13 Deloitte Touche Tohmatsu Limited

- 7.1.14 PWC LLP