日本のデータセンター物理セキュリティ:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

Japan Data Center Physical Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日

- 商品コード

- 1521844

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

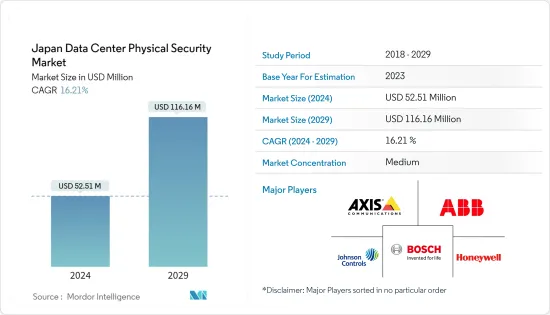

日本のデータセンター物理セキュリティ市場規模は、2024年に5,251万米ドルと推定され、2029年には1億1,616万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは16.21%で成長すると予測されます。

セキュリティ対策は、境界セキュリティ、施設管理、コンピュータルーム管理、キャビネット管理の4層に分類できます。データセンター・セキュリティの第一層は、境界における人員の不正侵入を阻止、検知、遅延させる。境界の監視に違反があった場合、第二の防御層はアクセスを拒否します。これは、カード・スワイプや生体認証を利用したアクセス・コントロール・システムです。

物理的セキュリティの第3層は、すべての制限区域の監視、回転式改札のような入場制限の配備、指や拇印、虹彩、血管パターンなどを確認する生体認証アクセス制御装置の提供、VCAの提供、無線周波数識別の使用など、さまざまな検証方法によってさらにアクセスを制限します。最初の3つのレイヤーは、許可された人のみの入場を保証します。入室を制限するためのさらなるセキュリティーには、キャビネットのロック機構が含まれます。この層は、悪意のある従業員のような「内部の脅威」の恐怖に対処します。

主なハイライト

- 建設中のIT負荷容量:日本のデータセンター物理セキュリティ市場の今後のIT負荷容量は、2029年までに2,000MWに達すると予想されます。

- 建設中の高床スペース:日本の床面積は2029年までに1,000万平方フィートに増加すると予想されます。

- 計画中のラック:国内に設置されるラックの総数は、2029年までに50万ユニットに達すると予想されます。2029年には、東京に最大数のラックが設置されると予想されます。

- 計画中の海底ケーブル:フィリピンを結ぶ海底ケーブルシステムは30近くあり、その多くが建設中です。2023年にサービス開始が予定されているそのような海底ケーブルのひとつは、東南アジア-日本ケーブル2(SJC2)で、千倉(日本)から志摩(日本)までの陸揚げ点を持つ10,500キロメートル以上に及ぶ。

日本のデータセンター物理セキュリティ市場動向

ビデオ監視セグメントが大きなシェアを占める

- データセンターには機密性の高い重要なデータが保管されているため、セキュリティは最優先事項です。データセンター事業者は、セキュリティ基準や規制を確実に満たすためにビデオ監視システムを利用しています。これにより、アクセスを監視し、不正アクセスを検出し、コンプライアンスを維持することができます。

- データ保護法は、データセンター事業者に厳しい要件を定めています。ビデオ監視は、物理的なセキュリティ対策を改善することで、コンプライアンスを維持するのに役立ちます。

- 2021年、日本の家庭におけるスマートフォンの普及率は89%近くに達しました。近年、人々がモバイルインターネットを利用する平均時間は増加しており、eコマースなどの関連産業にビジネスチャンスをもたらしています。オンラインショッピングプラットフォームの出現により、中小企業もオンライン決済方法に切り替え、eコマースの世界でデジタルな存在感を示しつつあります。老舗の大企業でさえ、eコマース・プラットフォームを従来のビジネス形態に統合しています。その結果、データ・トラフィックが増加し、データ・センターが増加し、ひいてはビデオ監視の需要が増加します。これは、ユーザーのデータセンターにおける悪意ある操作や誤操作を防止し、インシデント発生時には責任者を特定するための証拠となります。

- 日本のインターネット・ユーザーは2021年から2022年にかけて84万4,000人増加(0.7%増)。パンデミックによって家庭でのビデオ会議、遠隔学習、ビデオストリーミングが急増したため、2020年のインターネットトラフィックは2019年のCOVID-19以前のレベルと比較して1.6倍に増加しました。さらに、コネクテッドデバイスやスマートホームの利用が増加したことで、デジタルデータの需要が高まり、ネットワークトラフィックが改善しました。このため同国は、同地域におけるモバイルコマースのパイオニアのひとつとなっています。これは、データセンター全体でのデータ消費の増加を意味し、データセンター物理セキュリティ市場を押し上げます。

- 2021年の初めから、日本の携帯電話会社は5Gの展開を加速させてきました。国際通信省は、日本の5G体験をさらに進めたいと考えていました。その目標は、2024年3月末までに5G人口カバー率98%を達成することだった。全体として、日本は5Gサービスに利用可能な周波数の数を増やしたいと考えています。通信産業の成長はデータセンターの規模を拡大し、それによってビデオ監視の必要性を高めています。ビデオ監視には強力な抑止効果があり、物理的攻撃や重要データへの不正アクセスの可能性を低減します。

IT・通信セグメントが主要シェアを占める

- 日本には、ソニー、パナソニック、富士通、NEC、東芝といった大手ICT企業があり、ICTの主要拠点としての日本の拡大に重要な役割を果たし続けています。加えて、国内における多数の近代化・拡張プロジェクトの整然とした開拓と、高品質かつ先進的なインフラの維持に向けた政府支出の増加も、市場の成長を後押ししています。

- 日本政府は、民間部門のデジタルトランスフォーメーションを加速させ、新興中小企業を支援するための取り組みを行っています。2021年、経済産業省と総務省が主導する日本政府は、特に中小企業をターゲットとした組織内のデジタルトランスフォーメーション推進のためのガイドラインを発表しました。同様に、AI、サイバーセキュリティ、安全なクラウドサービスの導入に関するガイドラインも同年発表されました。

- 政府は、5Gや、現在のLTE(Long Term Evolution)よりもさらに高速なデータ転送が可能なその他の最先端技術の普及を引き続き推進しています。NTTドコモ、KDDI、ソフトバンク、楽天モバイルは2019年4月、総務省からそれぞれ5Gの周波数帯を割り当てられました。これらモバイルサービスプロバイダー4社は2020年に5G通信サービスを開始しました。このシナリオは、データの消費とデータセンターの利用を増加させ、調査対象市場の成長を促進する可能性があります。

- 日本政府のデジタル庁は、中央官庁と地方官庁の両方でクラウドサービスの利用を推進しています。例えば、デジタル庁は2022年10月、政府機関が年度内に「政府クラウド」サービスを採用すると発表しました。

- 経済産業省は2017年度から、クラウドサービスを含むIT投資を行う組織に対して「IT導入補助金」を支給しました。厚生労働省は2021年、COVID-19パンデミックの影響を受けた組織に対し、リモートワークへの移行を支援する「働き方改革推進」助成金を支給しました。厚生労働省は、中小企業がクラウドサービスやその他のIT機器と契約する際の契約料や機器費用を支援します。

日本のデータセンター物理セキュリティ産業の概要

市場は、Axis Communications AB、ABB Ltd、Bosch Sicherheitssysteme GmbHのようなプレーヤーが企業の能力向上に重要な役割を果たしているため、非常に断片化されています。市場志向は高度な競合環境につながります。小売・卸売データセンター市場の最大手企業は、システムを盗難から守り、安全なものにしようとしています。中小企業は競争に勝つために生産規模を拡大しようとし、大手企業は市場での地位を維持するために製品の革新と発売を重視しているため、市場には統合の波が押し寄せています。例えば

2023年4月、シュナイダーエレクトリックは新しいサービス「EcoCare for Modular Data Centers」を開始しました。この革新的なサービスプランの会員は、24時間365日のプロアクティブな遠隔監視と状態ベースのメンテナンスにより、モジュラー型データセンターの稼働時間を最大化するための専門知識を利用できます。会員専用のサポートには、専任のカスタマー・サクセス・マネジメント・チームが含まれ、リモート・サービスチームとオンサイト・サービス・チームの指揮を執り、問題が発生した場合にのみ各資産に対する断片的なアプローチではなく、システム・レベルでインフラとメンテナンスのニーズに対応します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- データトラフィックの増加と安全な接続性へのニーズがデータセンター物理セキュリティ市場の成長を促進

- サイバー脅威の増加がデータセンター物理セキュリティ市場の成長を促進

- 市場抑制要因

- 限られたIT予算、低コストの代替品の入手可能性、海賊版がデータセンター物理セキュリティ市場の潜在的成長を阻害しています。

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- ソリューションタイプ別

- ビデオ監視

- 入退室管理ソリューション

- その他(マントラップ、フェンス、モニタリングソリューション)

- サービスタイプ別

- コンサルティングサービス

- プロフェッショナルサービス

- その他(システムインテグレーションサービス)

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- ヘルスケア

- その他のエンドユーザー

第6章 競合情勢

- 企業プロファイル

- Axis Communications AB

- ABB Ltd

- Bosch Sicherheitssysteme GmbH

- Honeywell International Inc.

- Johnson Controls

- Schneider Electric

- ASSA ABLOY

- Cisco Systems Inc.

- Boon Edam

- Dahua Technology

第7章 投資分析

第8章 市場機会と今後の動向

目次

The Japan Data Center Physical Security Market size is estimated at USD 52.51 million in 2024, and is expected to reach USD 116.16 million by 2029, growing at a CAGR of 16.21% during the forecast period (2024-2029).

Security measures can be categorized into four layers, i.e., perimeter security, facility controls, computer room controls, and cabinet controls. The first layer of data center security discourages, detects, and delays any unauthorized entry of personnel at the perimeter. In case of any infringement in the perimeter monitoring, the second layer of defense denies access. It is an access control system utilizing card swipes or biometrics.

The third layer of physical security further restricts access through various verification methods, including monitoring all restricted areas, deploying entry restrictions such as turnstiles, providing biometric access control devices to verify finger and thumbprints, irises, or vascular patterns, providing VCA, and using radio frequency identification. The first three layers ensure the entry of only authorized people. Further security to restrict admission includes cabinet locking mechanisms. This layer addresses the fear of an 'insider threat,' such as a malicious employee.

Key Highlights

- Under Construction IT Load Capacity: The upcoming IT load capacity of the Japanese data center physical security market is expected to reach 2,000 MW by 2029.

- Under Construction Raised Floor Space: The country's construction of raised floor area is expected to increase to 10 million sq. ft by 2029.

- Planned Racks: The country's total number of racks to be installed is expected to reach 500 K units by 2029. Tokyo is expected to house the maximum number of racks by 2029.

- Planned Submarine Cables: There are close to 30 submarine cable systems connecting the Philippines, and many are under construction. One such submarine cable that is estimated to start service in 2023 was the Southeast Asia-Japan Cable 2 (SJC2), which stretches over 10,500 kilometers with landing points from Chikura, Japan, to Shima, Japan.

Japan Data Center Physical Security Market Trends

The Video Surveillance Segment Holds Significant Share

- Sensitive and important data are stored in data centers, so security is a top priority. Data center operators use video surveillance systems to ensure that security standards and regulations are met. This allows one to monitor access, detect unauthorized access, and maintain compliance.

- Data protection laws set strict requirements for data center operators. Video surveillance can help maintain compliance by improving physical security measures.

- In 2021, the smartphone penetration rate in Japanese households was nearly 89%. In recent years, the average amount of time people spend using mobile internet has increased, creating business opportunities for related industries such as e-commerce. With the advent of online shopping platforms, small and medium-sized businesses are also switching to online payment methods and a digital presence in the world of e-commerce. Even large, well-established companies are integrating e-commerce platforms with traditional forms of business. This leads to an increase in data traffic and, thus, an increase in data centers and, in turn, an increase in the demand for video surveillance. This helps prevent malicious or erroneous operations in the user's data center and provides evidence to identify those responsible in the event of an incident.

- Internet users in Japan increased by 844 thousand (+0.7%) between 2021 and 2022. Internet traffic increased 1.6x in 2020 compared to pre-COVID-19 levels in 2019 as the pandemic led to a surge in home video conferencing, distance learning, and video streaming. In addition, the increased use of connected devices and smart homes increased the demand for digital data and improved network traffic. This makes the country one of the pioneers of mobile commerce in the region. This means an increase in data consumption across data centers, thereby boosting the data center physical security market.

- Since the beginning of 2021, Japanese mobile phone companies have been accelerating the rollout of 5G. The Ministry of International Communications wanted to advance Japan's 5G experience further. The goal was to achieve 98% 5G population coverage by the end of March 2024. Overall, Japan wants to increase the number of frequencies available for its 5G services. The growth of the telecommunications industry is increasing the size of data centers, thereby increasing the need for video surveillance. Video surveillance has a powerful deterrent effect, reducing the likelihood of physical attacks and unauthorized access to critical data.

The IT and Telecommunication Segment Holds the Major Share

- Japan is home to major ICT organizations such as Sony, Panasonic, Fujitsu, NEC, and Toshiba, which continue to play a key role in the country's expansion as a major center for ICT. In addition, the orderly development of numerous modernization and expansion projects in the country, along with increasing government spending on maintaining high-quality and advanced infrastructure, are also driving the growth of the market.

- The Japanese government is making efforts to accelerate the digital transformation of the private sector and support emerging SMEs. In 2021, the Japanese government, led by the Ministry of Economy, Trade and Industry and the Ministry of Internal Affairs and Communications, published guidelines for promoting digital transformation within organizations, especially targeting small and medium-sized enterprises. Similarly, guidelines on implementing AI, cybersecurity, and secure cloud services were also published in the same year.

- The government is continuing to push the rollout of 5G and other cutting-edge technologies capable of transferring data at even higher rates than currently possible with long-term evolution (LTE). NTT DOCOMO, KDDI, Softbank, and Rakuten Mobile were each allocated a 5G spectrum by the Ministry of Internal Affairs and Communication (MIC) in April 2019. These four mobile service providers launched 5G telecommunication services in 2020. This scenario may increase the consumption of data and use of data centers, thereby driving the growth of the market studied.

- The Government of Japan's Digital Agency promotes the utilization of cloud services for both central and local government offices. For instance, the Digital Agency announced in October 2022 that the government agencies would adopt "Government Cloud" services for the fiscal year.

- The Ministry of Economics, Trade and Industry (METI) provided an IT Adoption Subsidy to organizations investing in IT, including cloud services, from FY 2017. In 2021, the Ministry of Health, Labour and Welfare (MHLW) provided organizations affected by the COVID-19 pandemic with a "Workstyle Reform Promotion" subsidy to help them transition to remote work. MHLW supports SMEs to cover the contracting fees and equipment costs of cloud services and other IT devices.

Japan Data Center Physical Security Industry Overview

The market is highly fragmented due to players like Axis Communications AB, ABB Ltd, and Bosch Sicherheitssysteme GmbH, which play a vital role in upscaling the capabilities of enterprises. Market orientation leads to a highly competitive environment. The biggest retail and wholesale data center market companies are trying to make their system secure and safe from thefts. There has been a wave of consolidation in the market as smaller players seek to scale up their production to compete, and big companies are focusing on product innovation and launches to maintain their market position. For instance,

In April 2023, Schneider Electric launched a new service offer, EcoCare for Modular Data Centers. Members of this innovative service plan benefit from specialized expertise to maximize modular data centers' uptime with 24/7 proactive remote monitoring and condition-based maintenance. Members benefit from exclusive support, which includes a dedicated customer success management team, who become their go-to coach, orchestrating remote and on-site services teams and addressing infrastructure and maintenance needs at a system level, rather than a fragmented approach for each asset only when problems arise.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Data Traffic and Need for Secured Connectivity is Promoting the Growth of the Data Center Physical Security Market

- 4.2.2 Rise in Cyber Threats is Causing the Data Center Physical Security Market to Grow

- 4.3 Market Restraints

- 4.3.1 Limited IT Budgets, Availability of Low-Cost Substitutes, and Piracy is Discouraging the Potential Growth of Data Center Physical Security Market

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Solution Type

- 5.1.1 Video Surveillance

- 5.1.2 Access Control Solutions

- 5.1.3 Others (Mantraps and Fences and Monitoring Solutions)

- 5.2 By Service Type

- 5.2.1 Consulting Services

- 5.2.2 Professional Services

- 5.2.3 Others (System Integration Services)

- 5.3 End-User

- 5.3.1 IT and Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Healthcare

- 5.3.5 Other End User

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Axis Communications AB

- 6.1.2 ABB Ltd

- 6.1.3 Bosch Sicherheitssysteme GmbH

- 6.1.4 Honeywell International Inc.

- 6.1.5 Johnson Controls

- 6.1.6 Schneider Electric

- 6.1.7 ASSA ABLOY

- 6.1.8 Cisco Systems Inc.

- 6.1.9 Boon Edam

- 6.1.10 Dahua Technology

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日