|

市場調査レポート

商品コード

1521419

商用航空機解体:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Commercial Aircraft Disassembly - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 商用航空機解体:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

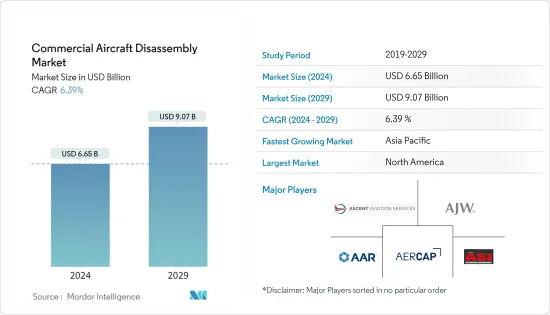

商用航空機解体の市場規模は2024年に66億5,000万米ドルと推定・予測され、2029年には90億7,000万米ドルに達し、予測期間中(2024-2029年)のCAGRは6.39%で成長すると予測されます。

主なハイライト

- オリバー・ワイマンのMROアウトルックによると、航空会社がより燃費の良いモデルに機材を更新するため、民間航空機の平均機齢は今後10年間で劇的に低下します。このため、年間平均退役率は過去10年と比較して20~25%増加します。

- 航空業界が持続可能な取り組みの活用を目指す中、使用済み航空機からの航空機部品のリサイクルがますます普及しています。エンジンのMROサービス・プロバイダーやリース会社は、ロールス・ロイスのトレント700やエアバスA330パワープラントなど、保有する旧式エンジンの需要が増加していることを目の当たりにしています。

- しかし、リサイクル工程で高価な合金を使用するため、工程全体のコストが上昇し、これが市場成長の課題となっています。

商用航空機解体市場の動向

予測期間中はナローボディセグメントが市場シェアを独占

- ナローボディセグメントが最大の市場シェアを占めると予想される主な理由は、航空会社が短距離路線と中距離路線の両方でナローボディ航空機を広く使用しているためです。ナローボディ航空機は、短距離路線における運航コストの低さや燃料効率の高さといった様々な利点と相まって、世界中の様々な格安航空会社で最も好まれて使用されている航空機のタイプとなっています。

- さらに、格安航空会社のビジネスモデルの成功は、その利点から、近年、新世代のナローボディ航空機に対する大規模な需要を生み出しています。新世代のナローボディ機の技術的進歩は、より長距離の飛行を可能にしています。ボーイングのB737とエアバスのA320は、最も多く販売されているナローボディ機の2つです。

- 例えば、2022年12月、エア・インディアは、エアバスと分割する歴史的な機材拡大の一環として、190機のナローボディ機ボーイングB737 MAXを含む200機以上のボーイング機を発注する契約を完了間近と発表しました。ボーイングB737 MAXが2020年後半に運航を再開することも、ナローボディ機セグメントの成長を後押しすると思われます。

アジア太平洋地域が予測期間中に最も高い成長を遂げる

- アジア太平洋地域の堅調な経済成長、良好な人口、発展途上国の人口動態が、同地域の航空旅客輸送を牽引しています。同地域では過去10年間に航空旅客輸送量が大幅に増加したが、その主な理由は同地域の観光地と航空旅行へのアクセスのしやすさにあり、これは予測期間中も続くと予想されます。

- 世界最大級の航空市場である中国とインドに加え、インドネシア、ベトナム、タイ、フィリピンなどの国々では、安価な休暇地を求める観光客による航空旅客輸送量がかつてないほど増加しています。

- この地域の航空会社が機材を近代化するにつれて、航空機の解体・リサイクル・サービスの需要が高まると予想されます。例えば、2022年9月、チャイナエアラインは、ボーイングB787ドリームライナーを最大24機発注することを決定したと発表しました。

- エアバスのアウトルックによると、中国では継続的な機材近代化の結果、2023年から2042年の間に2320機が退役します。従って、このような近代化努力は、古い航空機を再利用、修理、リサイクルする市場機会を拡大し、循環経済に貢献します。

商用航空機解体産業の概要

商用航空機解体市場は、一握りのプレーヤーが主要な市場シェアを占めることで統合されています。商用航空機解体・リサイクル市場で事業を展開している主要企業は、Ascent Aviation Services、A J Walter Aviation Ltd.、AAR、AerCap Holdings N.V.、Air Salvage International Ltd.です。

この市場で事業を展開するこれらの大手企業は、M&A、研究開発投資、提携、地域事業拡大、新製品発売など、さまざまな戦略を採用しています。航空機メーカー、航空会社、リサイクル企業、規制機関の間の協力的パートナーシップは、商用航空機解体・リサイクル市場拡大の原動力として浮上しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途別

- 解体・分解

- リサイクルと保管

- 使用済みサービス可能材料

- 回転可能部品

- 航空機タイプ別

- ナローボディ機

- ワイドボディ機

- リージョナルジェット機

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Ascent Aviation Services

- A J Walter Aviation Limited

- AAR

- AerCap Holdings N.V.

- AerSale, Inc.

- Air Salvage International Ltd

- Aircraft End-of-Life Solutions AELS

- Magellan Aerospace

- CAVU Aerospace Inc.

- China Aircraft Leasing Group Holdings Ltd

第7章 市場機会と今後の動向

The Commercial Aircraft Disassembly Market size is estimated at USD 6.65 billion in 2024, and is expected to reach USD 9.07 billion by 2029, growing at a CAGR of 6.39% during the forecast period (2024-2029).

Key Highlights

- According to Oliver Wyman's MRO outlook, the average age of commercial aircraft will decline dramatically over the next decade as airlines renew their fleets with more fuel-efficient models. This will drive average annual retirements to increase by 20-25% compared to the previous decade.

- With the aviation industry aiming at utilizing sustainable efforts, the recycling of aircraft parts from end-of-life aircraft is becoming increasingly popular. Engine MRO service providers and leasing companies are witnessing an increasing demand for some types of older engines in their portfolios, such as the Rolls-Royce Trent 700 and the Airbus A330 Powerplant, owing to lower fuel prices that have encouraged airlines to fly their aircraft for longer durations.

- However, the use of expensive alloys in the recycling process increases the overall cost of the process, which is a challenge to the market growth.

Commercial Aircraft Disassembly Market Trends

Narrow Body Segment to Dominate Market Share During the Forecast Period

- Narrow body segment is expected to hold the largest market share primarily due to the airlines' widespread use of narrow-body aircraft for both short and medium-haul routes. Advanced capabilities coupled with various other advantages such as low cost of operation and fuel efficiency in short-haul routes have led to narrow-body aircraft being the most preferred type of aircraft to be used by various low-cost carrier companies worldwide.

- Moreover, the success of the low-cost carrier business model has generated a massive demand for newer-generation narrow-body aircraft in recent years due to their advantages. Technological advancements in newer-generation narrow-body aircraft are making it possible to fly longer distances. Boeing's B737 and Airbus A320 are two of the most-sold aircraft narrow body aircraft.

- For instance, in December 2022, Air India announced that they are close to completing a deal to order more than 200 Boeing aircraft, which includes 190 narrowbody Boeing B737 MAX aircraft, as a part of a historic fleet expansion that will be split with Airbus. The return of the Boeing B737 MAX into service in late 2020 will also help the growth of the narrow-body segment.

Asia-Pacific to Witness Highest Growth During the Forecast Period

- The robust economic growth, favorable population, and demographic profiles of the populace in developing countries in the Asia-Pacific region are driving the air passenger traffic in the region. The region has seen a significant increase in air passenger traffic during the past decade, mostly due to the tourist destinations in the region and the ease of access to air travel, which is expected to continue during the forecast period.

- In addition to China and India, which are two of the largest aviation markets in the world, countries like Indonesia, Vietnam, Thailand, and the Philippines are experiencing an unprecedented increase in air passenger traffic from tourists exploring cheaper holiday locations.

- As airlines in this region modernize their fleets, demand for aircraft disassembly and recycling services is expected to rise. For instance, in September 2022, China Airlines announced that they had finalized an order for up to 24 Boeing B787 Dreamliners, as the carrier looks forward to continuing to upgrade its fleet with more modern and fuel-efficient airplanes.

- According to the Airbus Outlook, 2320 aircraft will retire between 2023 and 2042 in China as a result of continuous fleet modernization. Thus, such modernizing efforts will create growing market opportunities to reuse, repair, and recycle older aircraft and contribute to a circular economy.

Commercial Aircraft Disassembly Industry Overview

The commercial aircraft disassembly market is consolidated with a handful of players owing the major market share. The major players operating in the commercial aircraft disassembly, dismantling & recycling market are Ascent Aviation Services, A J Walter Aviation Ltd., AAR, AerCap Holdings N.V., and Air Salvage International Ltd.

These major players operating in this market have adopted various strategies comprising mergers and acquisitions, investment in R&D, collaborations, partnerships, regional business expansion, and new product launches. Collaborative partnerships between aircraft manufacturers, airlines, recycling companies, and regulatory bodies have emerged as a driving force behind the expansion of the commercial aircraft disassembly, dismantling, and recycling market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Disassembly and Dismantling

- 5.1.2 Recycling and Storage

- 5.1.3 Used Serviceable Material

- 5.1.4 Rotable Parts

- 5.2 By Aircraft Type

- 5.2.1 Narrow-body Aircraft

- 5.2.2 Wide-body Aircraft

- 5.2.3 Regional Jets

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Ascent Aviation Services

- 6.2.2 A J Walter Aviation Limited

- 6.2.3 AAR

- 6.2.4 AerCap Holdings N.V.

- 6.2.5 AerSale, Inc.

- 6.2.6 Air Salvage International Ltd

- 6.2.7 Aircraft End-of-Life Solutions AELS

- 6.2.8 Magellan Aerospace

- 6.2.9 CAVU Aerospace Inc.

- 6.2.10 China Aircraft Leasing Group Holdings Ltd