|

市場調査レポート

商品コード

1693438

穀物種子:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Grain Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 穀物種子:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 527 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

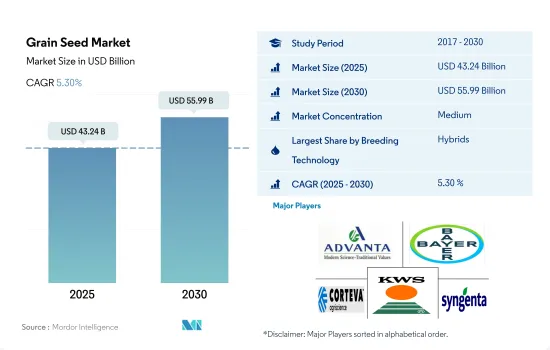

穀物種子市場規模は2025年に432億4,000万米ドルと推定され、2030年には559億9,000万米ドルに達し、予測期間中(2025~2030年)にCAGR 5.30%で成長すると予測されます。

主要成長国での高収量とGM作物の採用により、ハイブリッド種子が穀物種子市場を席巻

- 2022年の世界の穀物種子市場はハイブリッドが支配的で、64.1%という大きなシェアを獲得しました。この優位性は、高い収量、昆虫抵抗性、除草剤耐性、干ばつ耐性などの望ましい形質に起因しています。

- ハイブリッド作物のカテゴリーでは、トランスジェニック作物が市場金額の49.3%を占め、トランスジェニックハイブリッドは50.6%とわずかに高いシェアを主張しました。2022年には、アジア太平洋が非トランスジェニック穀物種子のリーダーとして台頭し、55.4%という大きな市場シェアを獲得しました。注目すべきは、遺伝子組み換え(GM)食用作物の栽培が制限されているインドのような国々が、農場の生産性を高めるために非トランスジェニック・ハイブリッド種子に大きく依存していることです。

- 遺伝子組換えハイブリッドセグメントでは、除草剤耐性ハイブリッドが大きなシェアを占め、2022年には51%に達します。除草剤耐性種子は、コメとトウモロコシの栽培にのみ認可されています。たとえば遺伝子組み換えトウモロコシは、細菌由来の遺伝子を組み込んで、さまざまな広範囲の除草剤に耐性を持たせています。

- 世界全体では、2022年の穀物・穀類種子市場の35.9%を開放受粉品種とハイブリッド派生品種が占めています。この中で、アジア太平洋は主要な消費者として台頭し、2022年の世界の穀物種子市場の32.5%を開放受粉品種が占めています。

- 企業は、先進的品種に対する需要の高まりに対応するため、新しい植物技術に多大な投資を行っています。これらの求められている品種は、多様な気候への適応性、高い収量ポテンシャル、耐病性、耐乾燥性を示します。新品種でこのような改良形質が利用できるようになったことで、今後数年間は種子需要の牽引役となることが予想されます。

加工産業からの高い需要と種子の商業利用によりトウモロコシが穀物・穀類種子市場を独占

- 穀物・穀類セグメントは最大のセグメントであり、2022年の世界種子市場の56.4%を占めました。市場金額は2023~2030年の間に43.7%成長すると推定されます。主要な穀物・穀類作物はトウモロコシです。2022年の市場規模は218億米ドルでした。これは主に、エタノール生産における加工産業からの需要増加と関連しています。

- 北米は穀物の主要生産国です。2022年には、穀物・穀類は北米の種子市場の57.6%を占めます。同地域における2022年の穀物・穀類栽培面積は8,270万ヘクタールで、2021年に比べ1.3%増加しました。これは、加工施設の増加や、穀物・穀類が食生活の主食であることから政府が自給自足の導入を推進しているためです。

- アジア太平洋では、中国が最大の穀物種子市場を有しており、2022年には金額ベースで62%を占め、市場規模は80億米ドルでした。2022年、アジア太平洋は世界のコメ種子市場の約74.3%を占めました。中国とインドは消費量が多いため(これらの国では人口の約65%が米を消費している)、2022年の世界の米種子市場の約37.6%を占めました。

- 欧州は世界最大の小麦生産国で、2022年の世界の小麦種子市場の45.3%を占めました。フランス、ドイツ、英国、ウクライナ、ロシアがこの地域で最大のシェアを占め、2022年の世界の小麦種子市場の30.1%を占めました。

- 加工産業からの穀物・穀類需要の増加、作物の輸出額の増加、人口の増加が、予測期間中の種子市場規模を押し上げる要因であると予測されます。

世界の穀物種子市場動向

消費用と食品・飼料産業からの穀物需要の増加により栽培面積が増加

- 穀物・穀類セグメントが世界の栽培面積を支配し、2022年には10億ヘクタールという広大な面積を占めます。小麦、トウモロコシ、米が主要穀物作物として台頭し、広範な栽培を確認しています。2017~2022年にかけて、栽培面積は1.9%増加したが、これは主に主食としての穀物に対する世界の需要の高まりによる。

- 小麦は主要な穀物作物であり、2022年には穀物作物総面積の約20.5%を占めます。小麦は温帯と亜熱帯地域で主食として繁栄しています。アジア太平洋は、恵まれた気候と消費者や加工産業からの旺盛な需要に支えられ、小麦の栽培面積が最大となっています。

- トウモロコシも主要穀物作物のひとつで、2022年には2億900万ヘクタールを占めます。その栽培面積は2017~2022年にかけて4.3%急増し、食品・飼料産業からの需要の高まりに後押しされました。トウモロコシは熱帯、亜熱帯、温帯の気候で栽培され、畑作トウモロコシ、スイートコーン、ポップコーン、ベビーコーンなどの品種があります。2022年には、アジア太平洋と北米が世界の作付面積の半分以上、すなわち51.9%を占め、トウモロコシ生産の強国に浮上します。

- 2022年に世界の穀物作付面積の15.3%を占めるコメの栽培面積は、2017年の1億6,260万ヘクタールから2022年には1億6,530万ヘクタールに増加します。アジア太平洋は、夏期とモンスーン期に豊富な降雨があるため、理想的な稲作環境が形成され、世界のコメ生産者として君臨しています。

- このような栽培面積の急増は、需要の増加に伴い、今後数年間の種子市場の成長を促進すると予測されます。

米は依然として主食であるため、耐病性米や、耐病性と適応性を強化したトウモロコシの需要が、農業従事者の拡大するニーズに応えるために高まっています。

- アジア太平洋における米の消費量は大きく、この地域の人々は通常、毎日の食事として米を食べています。中国とインドは世界の主要なコメ生産国として際立っています。気候の変化を踏まえ、種苗会社は生産者からの需要の急増に対応し、干ばつに強い品種の開発にますます力を入れるようになっています。2022年、中国は例年より乾燥した状況に直面し、干ばつに強い種子の需要がさらに高まりました。注目すべき動きとして、コルテバ・アグリスサイエンスは2020年にインド市場に自社ブランドのブレバントを導入しました。

- 米国、メキシコ、中国は世界規模で主要なトウモロコシ生産国であり、トウモロコシは収益性が高いため、生産者にとって有利な作物です。雑草防除、強化された穀物品質、早熟性、耐宿宿主性、多様な農業気候条件への適応性などの形質は、高い需要があります。Bayer AG、KWS SAAT SE & Co.KGaA、シンジェンタなどの産業大手は、特に効果的な散布やその他の防除方法がない場合に、収量を増やすために重要な、早腐れ病や葉の病気に対する抵抗性を備えた種子品種を提供しています。アジア太平洋では、生産者は穀粒の色、茎の高さ、穂軸あたりの粒数など、トウモロコシの物理的特性に影響する形質も好みます。

- 水不足、害虫の課題、病気の発生などの要因が、新しい種子品種の導入を促し、今後数年間の市場成長を促進すると予想されます。

穀物種子産業概要

穀物種子市場は適度に統合されており、上位5社で42.69%を占めています。この市場の主要企業は、Advanta Seeds-UPL、Bayer AG、Corteva Agriscience、KWS SAAT SE & Co. KGaA、Syngenta Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 最も人気のある品種

- コメとトウモロコシ

- 小麦とソルガム

- 育種技術

- 耕種作物

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非トランスジェニック・ハイブリッド

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- 昆虫抵抗性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 作物

- トウモロコシ

- 米

- ソルガム

- 小麦

- その他の穀物

- 地域

- アフリカ

- 育種技術別

- 作物別

- 国別

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他のアフリカ

- アジア太平洋

- 育種技術別

- 作物別

- 国別

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

- 欧州

- 育種技術別

- 作物別

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他の欧州

- 中東

- 育種技術別

- 作物別

- 国別

- イラン

- サウジアラビア

- その他の中東

- 北米

- 育種技術別

- 作物別

- 国別

- カナダ

- メキシコ

- 米国

- 北米その他

- 南米

- 育種技術別

- 作物別

- 国別

- アルゼンチン

- ブラジル

- その他の南米地域

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Bayer AG

- Corteva Agriscience

- Florimond Desprez

- Groupe Limagrain

- KWS SAAT SE & Co. KGaA

- RAGT Group

- S& W Seed Co.

- Syngenta Group

- Yuan Longping High-Tech Agriculture Co. Ltd

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92500

The Grain Seed Market size is estimated at 43.24 billion USD in 2025, and is expected to reach 55.99 billion USD by 2030, growing at a CAGR of 5.30% during the forecast period (2025-2030).

Hybrids dominated the grain seed market due to higher yield and adoption of GM crops in major growing countries

- Hybrids dominated the global grain seed market in 2022, capturing a significant 64.1% share. This dominance can be attributed to their desirable traits, including higher yields, insect resistance, herbicide tolerance, and drought tolerance.

- Within the hybrid category, transgenic crops accounted for 49.3% of the market's value, while transgenic hybrids claimed a slightly higher share of 50.6%. In 2022, Asia-Pacific emerged as the leader in non-transgenic grain seeds, commanding a sizable 55.4% market share. Notably, countries like India, with restrictions on genetically modified (GM) food crops, heavily rely on non-transgenic hybrids to bolster farm productivity.

- Within the transgenic hybrid segment, herbicide-tolerant hybrids took the lion's share, reaching 51% in 2022. Herbicide-tolerant seeds are exclusively authorized for rice and corn cultivation. GM corn, for instance, incorporates a gene from a bacterium, rendering it resistant to a range of broad-spectrum herbicides.

- Globally, open-pollinated varieties and hybrid derivatives accounted for 35.9% of the grains and cereals seed market in 2022. In this landscape, Asia-Pacific emerged as a key consumer, claiming 32.5% of the open-pollinated varieties of the global grain seed market in 2022.

- Companies are significantly investing in new plant technologies to meet the rising demand for advanced varieties. These sought-after varieties exhibit adaptability to diverse climates, high yield potential, disease resistance, and drought tolerance. The availability of such improved traits in new varieties is expected to drive seed demand in the coming years.

Corn dominates the grain and cereal seed market due to high demand from the processing industry and commercial usage of seeds

- The grains and cereals segment was the largest segment, and it accounted for 56.4% of the global seed market in 2022. The market value is estimated to grow by 43.7% between 2023 and 2030. Corn was the major grains and cereals crop. It accounted for a market value of USD 21.8 billion in 2022. It is mainly associated with higher demand from the processing industry in ethanol production.

- North America is the leading producer of grains. In 2022, grains and cereals accounted for 57.6% of the North American seed market. The total acreage under grains and cereals in the region in 2022 was 82.7 million hectares, which increased by 1.3% compared to 2021 due to an increase in the processing facilities and governments pushing the adoption of self-sufficiency as grains and cereals are the staple food in the diet.

- In Asia-Pacific, China has the largest grain seed market, and it accounted for 62% in terms of value in 2022, with a market value of USD 8.0 billion. In 2022, Asia-Pacific held about 74.3% of the global rice seed market. China and India accounted for about 37.6% of the global rice seed market in 2022 due to high consumption (about 65% of the population consumes rice in these countries).

- Europe was the largest wheat producer globally, accounting for 45.3% of the global wheat seed market in 2022. France, Germany, the United Kingdom, Ukraine, and Russia held the largest share in the region, accounting for 30.1% of the global wheat seed market in 2022.

- The increased demand for grains and cereals from processing industries, higher export value for the crops, and an increase in the population are the factors estimated to drive the seed market value during the forecast period.

Global Grain Seed Market Trends

Increased demand for grains for consumption and from food and feed industries led to increased area under cultivation

- The grains and cereals segment dominated global cultivation, covering an expansive 1 billion hectares in 2022. Wheat, corn, and rice emerged as the primary grain crops, witnessing widespread cultivation. Between 2017 and 2022, the cultivation area saw a 1.9% uptick, primarily driven by the rising global demand for grains as staple foods.

- Wheat is the leading grain crop, occupying approximately 20.5% of the total grain crop area in 2022. It thrives as a staple food in temperate and subtropical regions. Asia-Pacific, buoyed by favorable climates and robust demand from consumers and the processing industry, held the largest wheat cultivation area.

- Corn is also one of the major grain crops, accounting for 209.0 million hectares in 2022. Its cultivation area witnessed a 4.3% surge from 2017 to 2022, propelled by heightened demand from the food and feed industries. Corn finds its footing across tropical, sub-tropical, and temperate climates, with variants like field corn, sweet corn, popcorn, and baby corn. In 2022, Asia-Pacific and North America, commanding over half of the global acreage, i.e., 51.9%, emerged as the powerhouses of corn production.

- Rice, claiming 15.3% of the global grain crop area in 2022, saw its cultivation area inch up from 162.6 million hectares in 2017 to 165.3 million hectares in 2022. Asia-Pacific reigned supreme as the global rice producer due to abundant rainfall during the summer and monsoon seasons, thus creating an ideal rice-growing environment.

- This surge in cultivation areas is projected to fuel the growth of the seed market in the coming years, aligning with the rising demand.

The demand for disease-resistant rice, as it remains a staple food, and for corn with disease resistance and enhanced adaptability is rising to cater to the expanding needs of farmers

- Rice consumption in Asia-Pacific is significant, with people in the region typically having it as a daily meal. China and India stand out as major global rice producers. Given the changing climate, seed companies are increasingly focusing on developing drought-tolerant varieties, responding to a surge in demand from growers. In 2022, China faced drier conditions than usual, further fueling the demand for drought-tolerant seeds. In a notable move, Corteva Agriscience introduced its brand, Brevant, to the Indian market in 2020, featuring traits like wider adaptability and drought tolerance.

- The United States, Mexico, and China are key corn producers on a global scale, with corn being a lucrative crop for growers due to its high profitability. Traits such as weed control, enhanced grain quality, early maturity, lodging resistance, and adaptability to diverse agro-climatic conditions are in high demand. Industry leaders like Bayer AG, KWS SAAT SE & Co. KGaA, and Syngenta are delivering seed varieties that offer resistance to diseases like early rots and leaf diseases, which are critical for increasing yield, especially in the absence of effective sprays or other control methods. In Asia-Pacific, growers also prefer traits that influence corn's physical attributes, such as kernel color, stalk height, and grain count per cob.

- Factors like water scarcity, pest challenges, and disease outbreaks are expected to drive the introduction of new seed varieties and fuel market growth in the coming years.

Grain Seed Industry Overview

The Grain Seed Market is moderately consolidated, with the top five companies occupying 42.69%. The major players in this market are Advanta Seeds - UPL, Bayer AG, Corteva Agriscience, KWS SAAT SE & Co. KGaA and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Rice & Corn

- 4.2.2 Wheat & Sorghum

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Corn

- 5.2.2 Rice

- 5.2.3 Sorghum

- 5.2.4 Wheat

- 5.2.5 Other Grains & Cereals

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Breeding Technology

- 5.3.1.2 By Crop

- 5.3.1.3 By Country

- 5.3.1.3.1 Egypt

- 5.3.1.3.2 Ethiopia

- 5.3.1.3.3 Ghana

- 5.3.1.3.4 Kenya

- 5.3.1.3.5 Nigeria

- 5.3.1.3.6 South Africa

- 5.3.1.3.7 Tanzania

- 5.3.1.3.8 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Breeding Technology

- 5.3.2.2 By Crop

- 5.3.2.3 By Country

- 5.3.2.3.1 Australia

- 5.3.2.3.2 Bangladesh

- 5.3.2.3.3 China

- 5.3.2.3.4 India

- 5.3.2.3.5 Indonesia

- 5.3.2.3.6 Japan

- 5.3.2.3.7 Myanmar

- 5.3.2.3.8 Pakistan

- 5.3.2.3.9 Philippines

- 5.3.2.3.10 Thailand

- 5.3.2.3.11 Vietnam

- 5.3.2.3.12 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Breeding Technology

- 5.3.3.2 By Crop

- 5.3.3.3 By Country

- 5.3.3.3.1 France

- 5.3.3.3.2 Germany

- 5.3.3.3.3 Italy

- 5.3.3.3.4 Netherlands

- 5.3.3.3.5 Poland

- 5.3.3.3.6 Romania

- 5.3.3.3.7 Russia

- 5.3.3.3.8 Spain

- 5.3.3.3.9 Turkey

- 5.3.3.3.10 Ukraine

- 5.3.3.3.11 United Kingdom

- 5.3.3.3.12 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Breeding Technology

- 5.3.4.2 By Crop

- 5.3.4.3 By Country

- 5.3.4.3.1 Iran

- 5.3.4.3.2 Saudi Arabia

- 5.3.4.3.3 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Breeding Technology

- 5.3.5.2 By Crop

- 5.3.5.3 By Country

- 5.3.5.3.1 Canada

- 5.3.5.3.2 Mexico

- 5.3.5.3.3 United States

- 5.3.5.3.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 By Breeding Technology

- 5.3.6.2 By Crop

- 5.3.6.3 By Country

- 5.3.6.3.1 Argentina

- 5.3.6.3.2 Brazil

- 5.3.6.3.3 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 Florimond Desprez

- 6.4.5 Groupe Limagrain

- 6.4.6 KWS SAAT SE & Co. KGaA

- 6.4.7 RAGT Group

- 6.4.8 S&W Seed Co.

- 6.4.9 Syngenta Group

- 6.4.10 Yuan Longping High-Tech Agriculture Co. Ltd

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms