|

|

市場調査レポート

商品コード

1687908

宇宙における推進:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Space Propulsion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 宇宙における推進:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 213 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

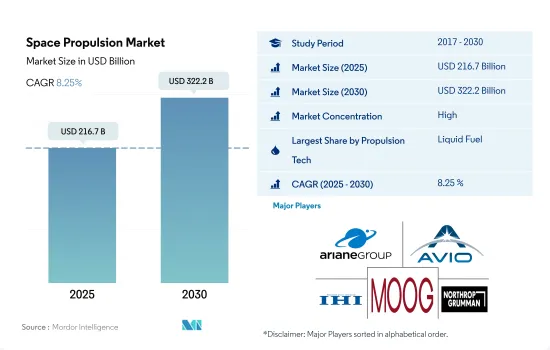

宇宙における推進の市場規模は2025年に2,167億米ドルと推定され、2030年には3,222億米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは8.25%で成長します。

ガスベース推進ドライブの一貫した採用がセグメントをリード

- 速度と方向を変えるために、衛星の推進システムは重要な役割を果たします。また、軌道上で宇宙船の位置を調整するためにも使用されます。軌道に入った後、宇宙船は地球と太陽に対して正しく方向を合わせるための姿勢制御を必要とします。場合によっては、ある軌道から衛星を移動させる必要があり、軌道を調整する能力がなければ、衛星の寿命は尽きると考えられています。そのため、推進システムの重要性が市場成長の原動力になると予想されます。

- 様々な種類の推進剤が目的に応じて使用されています。液体推進剤は、液体燃料を使用するロケットエンジンを使用します。ガス推進剤も使用できるが、密度が低く、従来のポンプ方式を適用するのが難しいため、一般的ではないです。移動を可能にした化学推進システムは、効率的で信頼性が高いことが証明されました。これらには、ヒドラジンシステム、シングルまたはツイン推進システム、ハイブリッドシステム、コールド/ホットエアシステム、固体推進剤が含まれます。これらは、強い推力や迅速な操縦が必要な場合に使用されます。したがって、化学推進システムは、その総インパルス容量がミッション要件を満たすのに十分である場合に選択される宇宙における推進技術であり続ける。

- 電気推進は、商業通信衛星のステーションを保持するために一般的に使用されており、比推力が高いため、一部の宇宙科学ミッションの主推進となっています。ノースロップ・グラマン社、ムーグ社、シエラネバダ社、スペースX社、ブルーオリジン社は、推進システムの主要なプロバイダーです。人工衛星の新たな打ち上げは、予測期間中の市場成長を加速させると予想されます。

宇宙探査に対する政府や民間企業の関心の高まりが、この市場の拡大に拍車をかけています。

- 衛星推進システムの世界市場は、様々な分野での衛星配備需要の増加に牽引され、近年力強い成長を遂げています。北米は、NASAなどの確立された宇宙機関やSpaceX、Blue Origin、Boeingなどの非公開会社の存在などにより、世界の宇宙における推進市場の支配的なプレーヤーとして台頭してきました。これらの企業は野心的な宇宙ミッションや衛星配備に取り組んでおり、先進推進システムの需要を牽引しています。NASAも太陽電気推進プロジェクトに取り組んでおり、野心的な発見や科学ミッションの期間と能力の延長を目指しています。

- アジア太平洋は近年、宇宙能力の急速な拡大を目の当たりにしてきました。中国、インド、日本のような国々は、宇宙技術や衛星製造において大きな進歩を遂げ、世界市場における強力なプレーヤーとしての地位を確立しています。2022年5月、中国の衛星電気推進会社であるKongtian Dongliは、中国の衛星打ち上げ計画が急増する中、数百万元のエンジェルラウンド資金を確保しました。

- 欧州には、ESAのような組織を通じた宇宙探査における協力の強い伝統があります。ESAと複数の加盟国とのパートナーシップは、宇宙技術、衛星製造、打上げ能力において大きな進歩をもたらしました。2023年2月、スペインを拠点とする宇宙モビリティ・プロバイダーであるIENAI SPACE社は、ATHENA(NAnotechnologyを動力源とするエレクトロスプレーに基づく適応可能なTHruster)推進システムの成熟と更なる開発のため、一般支援技術プログラム内で2つのESA契約を獲得しました。

世界の宇宙における推進市場動向

世界の宇宙における推進市場における投資機会の増加

- 研究と投資のための助成金は、北米の衛星打ち上げロケット市場の革新と成長の主な原動力となっています。これは、衛星打ち上げコストを大幅に削減する可能性のある再使用型ロケットなどの新技術開発に資金を提供するのに役立っています。2023年度、2022年度から2027年度までの大統領予算要求サマリーによると、NASAは太陽電気推進の開発に9,800万米ドルを受け取る見込みです。2021年3月、NASAはMaxar TechnologiesおよびBusek Co.とともに、6キロワット(kW)の太陽電気推進サブシステムの試験に成功しました。

- さらに2022年11月、ESAは、宇宙プロジェクトにおける欧州のリードを維持するため、今後3年間で宇宙資金を25%増額することを提案したと発表しました。ESAは22カ国に対し、2023年から2025年にかけて185億ユーロの予算を支持するよう求めています。2023年4月、ドーン・エアロスペース社は、DLR(ドイツ航空宇宙センター)と共同で、人工衛星や深宇宙ミッション用の亜酸化窒素ベースのグリーン推進剤の性能を高めるための実現可能性調査を行う契約を締結しました。

- アジア太平洋では、宇宙計画の増加により宇宙における推進剤の需要が高まっています。2022年5月、中国の衛星電気推進会社であるKongtian Dongli社は、中国のコンステレーション計画が急増する中、数百万元のエンジェルラウンド資金を確保したと発表しました。同社の主な製品はホールスラスターとマイクロ波電気推進システムです。同様に2023年2月、インド政府は、ISROが液体推進システムセンター(LPSC)やISRO推進複合施設の開発を含む様々な宇宙関連活動のために20億米ドルを受け取る見込みであると発表しました。

宇宙における推進産業の概要

宇宙における推進市場はかなり統合されており、上位5社で68%を占めています。この市場の主要企業は以下の通りです。 Ariane Group, Avio, IHI Corporation, Moog Inc. and Northrop Grumman Corporation(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 宇宙開発への支出

- 規制の枠組み

- 世界

- オーストラリア

- ブラジル

- カナダ

- 中国

- フランス

- ドイツ

- インド

- イラン

- 日本

- ニュージーランド

- ロシア

- シンガポール

- 韓国

- アラブ首長国連邦

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 推進技術

- 電気式

- ガスベース

- 液体燃料

- 地域

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- 日本

- ニュージーランド

- シンガポール

- 韓国

- 欧州

- 国別

- フランス

- ドイツ

- ロシア

- 英国

- 北米

- 国別

- カナダ

- 米国

- 世界のその他の地域

- 国別

- ブラジル

- イラン

- サウジアラビア

- アラブ首長国連邦

- 世界のその他の地域

- アジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Ariane Group

- Avio

- Blue Origin

- Honeywell International Inc.

- IHI Corporation

- Moog Inc.

- Northrop Grumman Corporation

- OHB SE

- Sierra Nevada Corporation

- Sitael S.p.A.

- Space Exploration Technologies Corp.

- Thales

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 66785

The Space Propulsion Market size is estimated at 216.7 billion USD in 2025, and is expected to reach 322.2 billion USD by 2030, growing at a CAGR of 8.25% during the forecast period (2025-2030).

Consistent adoption of gas-based propulsion drives to lead the segment

- To change the velocity and direction, the satellite's propulsion system plays an important role. It is also used to coordinate the position of the spacecraft in orbit. After entering into orbit, the spacecraft needs attitude control which helps to correctly align its direction with respect to the Earth and the Sun. In some cases, satellites need to be moved from one orbit, and without their ability to adjust to their orbit, the life of satellites is considered to be over. Therefore, the importance of propulsion systems is expected to drive the market growth.

- Various types of propellants are used for different purposes. Liquid propellants use rocket engines that use liquid fuel. Gas propellants can also be used but are not common due to their low density and difficulty in applying conventional pumping methods. The chemical propulsion systems that enabled movements proved to be efficient and reliable. These include hydrazine systems, single or twin propulsion systems, hybrid systems, cold/hot air systems, and solid propellants. They are used when strong thrust or rapid maneuvering is required. Therefore, chemical systems remain the space propulsion technology of choice when their total impulse capacity is sufficient to meet the mission requirements.

- Electric propulsion is commonly used to hold stations for commercial communication satellites, and it is the main propulsion of some space science missions due to their high specific impulses. Northrop Grumman Corporation, Moog Inc., Sierra Nevada Corporation, SpaceX, and Blue Origin are some of the major providers of propulsion systems. The new launch of satellites is expected to accelerate market growth during the forecast period.

The growing interest of governments and private players in space exploration have fueled the expansion of this market

- The global market for satellite propulsion systems witnessed robust growth in recent years, driven by the increasing demand for satellite deployments across various sectors. North America has emerged as a dominant player in the global space propulsion market, mainly due to the presence of established space agencies such as NASA and private companies like SpaceX, Blue Origin, and Boeing. These entities have undertaken ambitious space missions and satellite deployments, driving the demand for advanced propulsion systems. NASA is also working on the Solar Electric Propulsion project, which aims to extend the duration and capabilities of ambitious discoveries and science missions.

- Asia-Pacific has witnessed a rapid expansion of its space capabilities in recent years. Countries like China, India, and Japan have made significant strides in space technology and satellite manufacturing, positioning themselves as formidable players in the global market. In May 2022, Kongtian Dongli, a Chinese satellite electric propulsion company, secured multi-million yuan angel round financing amid a proliferation of Chinese constellation plans.

- Europe has a strong tradition of collaboration in space exploration through organizations like the ESA. ESA's partnerships with multiple member states have resulted in significant advancements in space technology, satellite manufacturing, and launch capabilities. In February 2023, IENAI SPACE, an in-space mobility provider based in Spain, received two ESA contracts within the General Support Technology Program to mature and further develop ATHENA (Adaptable THruster based on Electrospray powered by NAnotechnology) propulsion systems.

Global Space Propulsion Market Trends

Rising investment opportunities in the global space propulsion market

- The grant for research and investment has been a major driver of innovation and growth in the North American satellite launch vehicle market. It has helped to fund the development of new technologies, such as reusable launch vehicles, which have the potential to significantly reduce the cost of satellite launches. In FY2023, according to the President's budget request summary from FY2022 to FY2027, NASA is expected to receive USD 98 million for the development of Solar Electric Propulsion. In March 2021, NASA, along with Maxar Technologies and Busek Co., successfully completed a test of the 6-kilowatt (kW) solar electric propulsion subsystem.

- Additionally, in November 2022, ESA announced that it had proposed a 25% boost in space funding over the next three years to maintain Europe's lead in space projects. The ESA is asking its 22 nations to back a budget of EUR 18.5 billion for 2023-2025. In April 2023, Dawn Aerospace was awarded a contract to conduct a feasibility study with DLR (German Aerospace Center) to increase the performance of a nitrous-oxide-based green propellant for satellites and deep-space missions.

- In Asia-Pacific, the demand for space propulsion is driven by increasing space programs. In May 2022, Kongtian Dongli, a Chinese satellite electric propulsion company, announced that it had secured multi-million yuan angel round financing amid a proliferation of Chinese constellation plans. The company's main products are hall thrusters and microwave electric propulsion systems. Likewise, in February 2023, the Indian government announced that ISRO is expected to receive USD 2 billion for various space-related activities, including the development of the Liquid Propulsion Systems Centre (LPSC) and ISRO Propulsion Complex.

Space Propulsion Industry Overview

The Space Propulsion Market is fairly consolidated, with the top five companies occupying 68%. The major players in this market are Ariane Group, Avio, IHI Corporation, Moog Inc. and Northrop Grumman Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Spending On Space Programs

- 4.2 Regulatory Framework

- 4.2.1 Global

- 4.2.2 Australia

- 4.2.3 Brazil

- 4.2.4 Canada

- 4.2.5 China

- 4.2.6 France

- 4.2.7 Germany

- 4.2.8 India

- 4.2.9 Iran

- 4.2.10 Japan

- 4.2.11 New Zealand

- 4.2.12 Russia

- 4.2.13 Singapore

- 4.2.14 South Korea

- 4.2.15 United Arab Emirates

- 4.2.16 United Kingdom

- 4.2.17 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Propulsion Tech

- 5.1.1 Electric

- 5.1.2 Gas based

- 5.1.3 Liquid Fuel

- 5.2 Region

- 5.2.1 Asia-Pacific

- 5.2.1.1 By Country

- 5.2.1.1.1 Australia

- 5.2.1.1.2 China

- 5.2.1.1.3 India

- 5.2.1.1.4 Japan

- 5.2.1.1.5 New Zealand

- 5.2.1.1.6 Singapore

- 5.2.1.1.7 South Korea

- 5.2.2 Europe

- 5.2.2.1 By Country

- 5.2.2.1.1 France

- 5.2.2.1.2 Germany

- 5.2.2.1.3 Russia

- 5.2.2.1.4 United Kingdom

- 5.2.3 North America

- 5.2.3.1 By Country

- 5.2.3.1.1 Canada

- 5.2.3.1.2 United States

- 5.2.4 Rest of World

- 5.2.4.1 By Country

- 5.2.4.1.1 Brazil

- 5.2.4.1.2 Iran

- 5.2.4.1.3 Saudi Arabia

- 5.2.4.1.4 United Arab Emirates

- 5.2.4.1.5 Rest of World

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Ariane Group

- 6.4.2 Avio

- 6.4.3 Blue Origin

- 6.4.4 Honeywell International Inc.

- 6.4.5 IHI Corporation

- 6.4.6 Moog Inc.

- 6.4.7 Northrop Grumman Corporation

- 6.4.8 OHB SE

- 6.4.9 Sierra Nevada Corporation

- 6.4.10 Sitael S.p.A.

- 6.4.11 Space Exploration Technologies Corp.

- 6.4.12 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms