|

市場調査レポート

商品コード

1693940

欧州の宇宙推進:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Space Propulsion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の宇宙推進:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 139 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

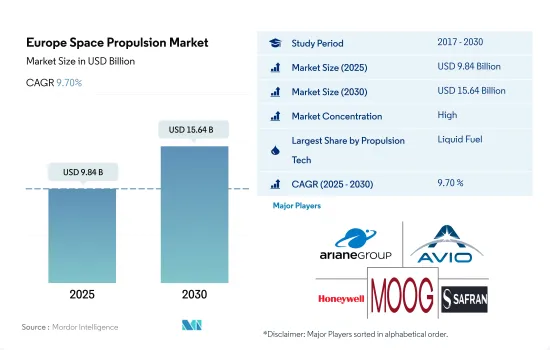

欧州の宇宙推進市場規模は2025年に98億4,000万米ドルと推定・予測され、2030年には156億4,000万米ドルに達し、予測期間(2025~2030年)のCAGRは9.70%で成長すると予測されています。

予測期間中にガスベースの推進力の利用が急増する見込み

- 欧州の宇宙推進市場では、ガスベースの推進システムが、簡便性、信頼性、迅速な応答時間が重要な小型~中型衛星に引き続き広く使用されています。ガス推進システムは、通信、地球観測、科学研究など、さまざまな衛星ミッションで広く利用されています。

- 電気推進システムは、その燃料効率と運用寿命の延長により、欧州の衛星市場で脚光を浴びています。この技術はより高い比インパルスを提供するため、衛星はより少ない推進剤でより多くのペイロードを運ぶことができます。さらに、電気推進システムは、長時間のミッションや精密な軌道制御が可能です。静止衛星、深宇宙ミッション、全地球をカバーする衛星コンステレーションに適しています。

- 液体推進システムは、主にヒドラジンや四酸化窒素のような二液性燃料をベースとしており、欧州の衛星で主推進や大規模な軌道制御に広く採用されています。液体推進システムは、複雑な軌道移動やランデブー・マヌーバを柔軟に行うことができます。しかし、有毒で腐食性のある推進剤を注意深く取り扱う必要があり、電気やガスを利用したシステムと比べて推進剤の質量が大きくなります。2023~2029年の間に、市場は81%急増すると予想され、ガスベースの推進力が市場を独占すると予想されます。

推進技術の製品革新が成長を後押しする見込み

- 宇宙推進とは、宇宙船や人工衛星を加速させるために用いられる方法です。現在の宇宙推進システムには、主に2つのソリューションがあります。電気モーター(EP)を使用してイオン化した推進剤を加速する方法と、化学反発(CP)を使用してプロペラ自体を推進力の動力源とする方法です。

- 宇宙製造産業はニッチなセクタであり、最終的な収益は72億5,000万ユーロを占め、3万8,000人の先進的資格を持つ雇用を生み出しています。その規模の小ささにもかかわらず、宇宙産業は幅広いサービスと応用を可能にし、この地域の政府や企業にとって極めて戦略的な産業です。

- ESAの将来宇宙輸送プログラムは、推進システムの技術的な成熟度を通じて、課題に対処し、解決策を提供するための主要な打ち上げシステム技術を特定します。主要技術は、推進実証エンジンに組み込まれ、適切な環境でテストされる前に、コンポーネントとサブシステムの両方のレベルで設計されます。この地域には多くの政府系、商業系、その他の参入企業が存在するため、衛星製造産業の需要はプラス成長を示しました。これに基づき、2017~2022年の間に、この地域では570以上の衛星が打ち上げられました。製造・打ち上げられた570機以上の衛星のうち、90%近くが業務用です。

欧州の宇宙推進市場の動向

欧州の宇宙推進市場の投資機会が需要を牽引

- 欧州諸国は、宇宙セグメントにおける様々な投資の重要性を認識しています。世界の宇宙産業で競合と革新性を維持するために、宇宙プログラムや技術革新への支出を増やしています。2022年11月、ESAは、地球観測における欧州のリードを維持し、航法サービスを拡大し、米国との探査におけるパートナーであり続けるために、今後3年間で宇宙資金を25%増額することを提案したと発表しました。ESAは22カ国に対し、2023~2025年にかけて185億ユーロの予算を支援するよう要請しました。同様に、フランス政府は2022年9月、過去3年間で約25%増となる90億米ドル以上を宇宙活動に充てる計画を発表しました。

- 2022年11月、ドイツは様々な宇宙関連活動に約23億7,000万ユーロを割り当てると発表しました。2023年4月、ドーン・エアロスペース社は、DLR(ドイツ航空宇宙センター)と共同で、人工衛星や深宇宙ミッション用の亜酸化窒素ベースのグリーン推進剤の性能を高めるための実現可能性調査を行う契約を締結しました。2022年12月、英国宇宙庁は13の初期段階技術プロジェクトに270万ユーロを拠出すると発表しました。European Astrotechは、キセノンまたはクリプトンを使用する電気推進システムを搭載した衛星を整備するための推進薬充填カート(GSE)に対して5万4,000ユーロを受け取りました。スモールスパーク・スペースシステムズは、スモールスパークのデュアル発射モード推進システムS4-NEWT-A2の開発と成熟のために7万6,000ユーロを受け取りました。

欧州の宇宙推進産業概要

欧州の宇宙推進市場はかなり統合されており、上位5社で77.76%を占めています。この市場の主要企業は、Ariane Group、Avio、Honeywell International Inc.、Moog Inc.、Safran SAです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 宇宙開発への支出

- 規制の枠組み

- フランス

- ドイツ

- ロシア

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 推進技術

- 電気式

- ガスベース

- 液体燃料

- 国名

- フランス

- ドイツ

- ロシア

- 英国

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ariane Group

- Avio

- Honeywell International Inc.

- Moog Inc.

- OHB SE

- Safran SA

- Sitael S.p.A.

- Space Exploration Technologies Corp.

- Thales

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50001252

The Europe Space Propulsion Market size is estimated at 9.84 billion USD in 2025, and is expected to reach 15.64 billion USD by 2030, growing at a CAGR of 9.70% during the forecast period (2025-2030).

The utilization of gas-based propulsion is expected to surge during the forecast period

- In the European space propulsion market, gas-based propulsion systems continue to be widely used for small to medium-sized satellites, where simplicity, reliability, and quick response times are crucial. They are widely utilized in various satellite missions, including telecommunications, Earth observation, and scientific research.

- Electric propulsion systems have gained prominence in the European satellite market due to their fuel efficiency and extended operational lifespan. This technology provides higher specific impulses, enabling satellites to carry more payload while utilizing less propellant. In addition, electric propulsion systems offer the capability for long-duration missions and precise orbital maneuvers. They are well-suited for geostationary satellites, deep space missions, and satellite constellations for global coverage.

- Liquid propulsion systems, predominantly based on bipropellants like hydrazine and nitrogen tetroxide, have been widely employed in European satellites for primary propulsion and large orbital maneuvers. Liquid propulsion systems offer the flexibility to perform complex orbital transfers and rendezvous maneuvers. However, they require careful handling of toxic and corrosive propellants and necessitate a higher propellant mass compared to electric or gas-based systems. Between 2023 and 2029, the market is expected to surge by 81%, and gas-based propulsion is expected to dominate the market.

The product innovation in propulsion technology is expected to boost the growth

- Space propulsion is a method used to accelerate spacecraft or artificial satellites. The current space propulsion system includes two main solutions. Uses of an electric motor (EP) accelerates the ionized propellant, and chemical repulsion (CP) uses the propeller itself as the power source for thrust force.

- The space manufacturing industry is a niche sector, accounting for EUR 7.25 billion in final revenue and creating 38,000 highly qualified jobs. Despite its small size, the space sector enables a wide range of services and applications and is highly strategic for governments and businesses in the region.

- ESA's Future Space Transport Program identifies key launch system technologies to address the challenges and deliver solutions through technology-ready maturity for propulsion systems. Key technologies are designed at both the component and subsystem levels before being integrated into the propulsion demonstration engine and tested in the right environment. Due to the presence of many governmental, commercial, and other players in the region, demand in the satellite manufacturing industry witnessed positive growth. Based on this, during 2017-2022, more than 570 satellites were launched in the area. Of the more than 570 satellites produced and launched, nearly 90% are for commercial use.

Europe Space Propulsion Market Trends

Investment opportunities in the European space propulsion market is driving the demand

- European countries are recognizing the importance of various investments in the space domain. They are increasing their spending on space programs and innovation to stay competitive and innovative in the global space industry. In November 2022, ESA announced that it had proposed a 25% boost in space funding over the next three years designed to maintain Europe's lead in Earth observation, expand navigation services and remain a partner in exploration with the United States. The ESA has asked its 22 nations to support a budget of EUR 18.5 billion from 2023 to 2025. Likewise, in September 2022, the French government announced that it plans to allocate more than USD 9 billion to space activities, an increase of about 25% over the past three years.

- In November 2022, Germany announced that about EUR 2.37 billion were allocated for various space-related activities. In April 2023, Dawn Aerospace was awarded a contract to conduct a feasibility study with DLR (German Aerospace Center) to increase the performance of a nitrous-oxide-based green propellant for satellites and deep-space missions. In December 2022, the UK Space Agency announced EUR 2.7 million for 13 early-stage technology projects. European Astrotech received EUR 54,000 for a propellant loading cart (GSE) to service satellites with electric propulsion systems using xenon or krypton. SmallSpark Space Systems received EUR 76,000 for the development and maturation of SmallSpark's dual-firing mode propulsion system, the S4-NEWT-A2, which will form part of the architecture of its S4-SLV in-space logistics vehicle and as a candidate system for upper-stage launch vehicles.

Europe Space Propulsion Industry Overview

The Europe Space Propulsion Market is fairly consolidated, with the top five companies occupying 77.76%. The major players in this market are Ariane Group, Avio, Honeywell International Inc., Moog Inc. and Safran SA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Spending On Space Programs

- 4.2 Regulatory Framework

- 4.2.1 France

- 4.2.2 Germany

- 4.2.3 Russia

- 4.2.4 United Kingdom

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Propulsion Tech

- 5.1.1 Electric

- 5.1.2 Gas based

- 5.1.3 Liquid Fuel

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 Russia

- 5.2.4 United Kingdom

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Ariane Group

- 6.4.2 Avio

- 6.4.3 Honeywell International Inc.

- 6.4.4 Moog Inc.

- 6.4.5 OHB SE

- 6.4.6 Safran SA

- 6.4.7 Sitael S.p.A.

- 6.4.8 Space Exploration Technologies Corp.

- 6.4.9 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms