北米の宇宙推進:市場シェア分析、産業動向、成長予測(2025~2030年)

North America Space Propulsion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 137 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693953

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

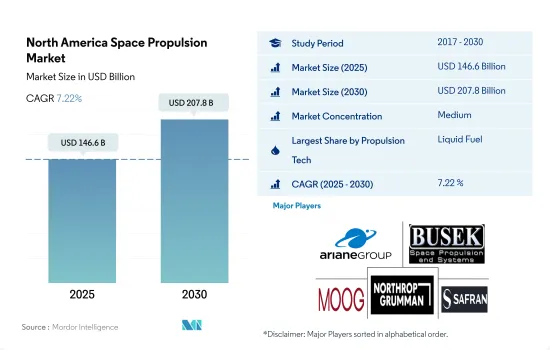

北米の宇宙推進市場規模は2025年に1,466億米ドルと推定・予測され、2030年には2,078億米ドルに達し、予測期間(2025~2030年)のCAGRは7.22%で成長すると予測されています。

高額の宇宙関連投資に関与する大手企業や宇宙機関が促進要因

- 衛星の推進システムは、宇宙船を軌道に推進し、その位置を調整するために一般的に使用されます。液体推進剤ロケットまたは液体ロケットは、液体推進剤を使用するロケットエンジンを利用します。気体推進剤を使用することもできるが、密度が低く、従来のポンピング方法を適用するのが難しいため、期待されていないです。液体は密度と比推力が適度に高いので望ましいです。

- ガスベースの推進システムは、効率と信頼性が証明されている動きを可能にします。これらのシステムには、ヒドラジンシステム、その他のシングルまたはツイン推進システム、ハイブリッドシステム、冷温風システム、固体燃料などがあります。これらのシステムは、強い推力や迅速な操縦が必要な場合に使用されます。したがって、ガス推進システムは、その総インパルス容量がミッション要件を満たすのに十分である場合に選択される宇宙推進技術であり続けます。

- 一方、電気推進は、商業通信衛星のステーション保持に一般的に使用されています。電気推進は、その高い比インパルスにより、一部の宇宙科学ミッションの主推進力となっています。Northrop Grumman Corporation、Moog Inc.、Sierra Nevada Corporation、SpaceX、Blue Originは、この地域における推進システムの主要プロバイダです。液体推進システムは固体推進に比べて比推力が高いため、衛星の効率が高く、運用寿命が長くなります。NASAのような大手開発企業や宇宙機関は、多額の宇宙関連投資を行っているため、研究開発に多くの費用を費やすことができ、継続的な技術革新と、より効率的で先進的技術の開発を可能にしています。同地域での新型衛星の打ち上げは、予測期間中に市場の成長を加速させると予想されます。

推進技術の製品革新が成長を後押しする見込み

- 北米の宇宙推進市場は、民間セクタの参入が著しく増加しています。SpaceX、Blue Origin、Rocket Labといった企業が主要企業として台頭し、革新的な推進技術を開発して打ち上げコストを削減しています。この動向は、競争の激化とこのセグメントの進歩の加速につながっています。

- 電気推進システム、特にイオン推進とホール効果スラスターが産業で脚光を浴びています。これらのシステムは、より高い効率、より長い運用寿命、深宇宙ミッションの能力を記載しています。これらのシステムは、人工衛星や惑星間探査機など、民間と政府の宇宙ミッションで使用されています。

- 北米は世界的に見ても主要市場のひとつであり、特に米国における強力な宇宙探査・開発活動がその理由です。NASAは、小型衛星用の先進推進システムを開発するために新興企業に投資しています。NASAはまた、太陽電気推進(SEP)プロジェクトにも取り組んでおり、野心的な発見・科学ミッションの期間と能力の延長を目指しています。

- この地域の様々な政府、商業、その他の参入企業により、衛星製造産業の需要は前向きに伸びています。2017~2022年の間に、この地域では4,300以上の衛星が打ち上げられ、宇宙推進市場を支援しています。このような投資と技術開拓の数に加え、北米は予測期間中、世界的に市場をリードすると予想されます。

北米の宇宙推進市場の動向

北米の宇宙推進市場における投資機会

- 宇宙プログラムへの投資が技術革新を促進し、衛星推進市場の繁栄を促進しています。宇宙プログラムに関連する研究開発イニシアティブは、効率向上と運用寿命の延長を提供する新しい推進システムの創造につながります。これらの推進システムは、宇宙船の操縦、軌道維持、ミッションの長寿命化において重要な役割を果たしています。この地域の政府と民間部門は、助成金という形で宇宙セグメントの研究と技術革新に資金を充てています。北米では、宇宙プログラムのための政府支出が2022年に約248億米ドルと過去最高を記録しました。例えば、2023年2月、NASAは研究助成金として3億3,300万米ドルを分配しました。さらに、米国政府は2022年に約620億米ドルを宇宙プログラムに費やしており、宇宙セグメントで世界一の支出国となっています。米国以外では、カナダ宇宙庁の予算は控えめで、2022~23年の予算支出見込み額は3億2,900万米ドルです。2022~2027年度の大統領予算要求概要でNASAに割り当てられた資金を見ると、NASAは宇宙電力と原子力推進の開発に4,500万米ドルを受け取ると予想されています。

- NASAは、太陽電気推進(SEP)の開発に9,800万米ドルを受け取る見込みです。2021年3月、NASA、Maxar Technologies、Busek Co.は、PPEに搭載される6キロワット(kW)の太陽電気推進サブシステムの検査を成功裏に完了しました。太陽電気推進プロジェクトは、2023年度第1四半期の初めにエアロジェットロケットダイン社から最初の適格スラスタを受領する予定でした。政府は、核熱推進システムの開発に1億1,000万米ドルの資金を割り当てました。

北米の宇宙推進産業概要

北米の宇宙推進市場は適度に統合されており、上位5社で52.89%を占めています。この市場の主要企業は、Ariane Group、Busek Co. Inc.、Moog Inc.、Northrop Grumman Corporation、Safran SAです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 宇宙開発への支出

- 規制の枠組み

- カナダ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 推進技術

- 電気式

- ガスベース

- 液体燃料

- 国名

- カナダ

- 米国

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ariane Group

- Blue Origin

- Busek Co. Inc.

- Moog Inc.

- Northrop Grumman Corporation

- OHB SE

- Safran SA

- Sierra Nevada Corporation

- Space Exploration Technologies Corp.

- Thales

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50001267

The North America Space Propulsion Market size is estimated at 146.6 billion USD in 2025, and is expected to reach 207.8 billion USD by 2030, growing at a CAGR of 7.22% during the forecast period (2025-2030).

Major players and space agencies, involved in high space-related investment is the driving factor

- A satellite's propulsion system is commonly used to propel a spacecraft into orbit and coordinate its position. A liquid propellant rocket or liquid rocket utilizes a rocket engine that uses liquid propellants. Gas propellants may also be used but are not expected due to their low density and difficulty in applying conventional pumping methods. Liquids are desirable as they have a reasonably high density and specific impulse.

- Gas-based propulsion systems enable movements that have been proven efficient and reliable. These systems include hydrazine systems, other single or twin propulsion systems, hybrid systems, cold/hot air systems, and solid fuels. These systems are used when strong thrust or rapid manoeuvring is required. Therefore, gas-based propulsion systems remain the space propulsion technology of choice when their total impulse capacity is sufficient to meet the mission requirements.

- On the other hand, electric propulsion is commonly used to hold stations for commercial communication satellites. It is the main propulsion of some space science missions due to its high specific impulses. Northrop Grumman Corporation, Moog Inc., Sierra Nevada Corporation, SpaceX, and Blue Origin are some of the major providers of propulsion systems in the region. Liquid propulsion systems offer higher specific impulses compared to solid propulsion, resulting in greater efficiency and longer operational life for satellites. Major players and space agencies, like NASA, are involved in high space-related investments, enabling them to spend more on R&D and allowing them to innovate continuously and develop more efficient and advanced technologies. Launching new satellites in the region is expected to accelerate the market's growth during the forecast period.

Product innovation in propulsion technology is expected to boost growth

- The North American space propulsion market has witnessed a significant rise in private sector participation. Companies like SpaceX, Blue Origin, and Rocket Lab have emerged as key players, developing innovative propulsion technologies and reducing launch costs. This trend has led to increased competition and accelerated advancements in the field.

- Electric propulsion systems, particularly ion propulsion and Hall-effect thrusters, have gained prominence in the industry. These systems offer higher efficiency, longer operational lifetimes, and the capability for deep space missions. They are used in commercial and government space missions, including satellites and interplanetary probes.

- North America is one of the major markets globally, especially due to strong space exploration and development activity in the United States. NASA invests in start-ups to develop advanced propulsion systems for small satellites. NASA is also working on the Solar Electric Propulsion (SEP) project, which aims to extend the duration and capabilities of ambitious discoveries and science missions.

- Due to various government, commercial, and other players in the region, the demand in the satellite manufacturing industry is growing positively. During 2017-2022, 4,300+ satellites were launched in the region, aiding the space propulsion market. In addition to the number of such investments and technological developments, North America is expected to lead the market globally during the forecast period.

North America Space Propulsion Market Trends

Investment opportunities in the North American space propulsion market

- Investments in space programs are driving technological innovations and fostering the thriving satellite propulsion market. R&D initiatives associated with space programs lead to the creation of new propulsion systems, which offer increased efficiency and longer operational lifetime. These propulsion systems play a crucial role in spacecraft maneuvering, orbit maintenance, and mission longevity. The region's government and the private sector have dedicated funds for research and innovation in the space sector in terms of grants. In North America, government expenditure for space programs hit a record of approximately USD 24.8 billion in 2022. For instance, in February 2023, NASA distributed USD 333 million as research grants. Additionally, in 2022, the US government spent nearly USD 62 billion on its space programs, making it the world's highest spender in the space sector. Apart from the United States, the Canadian Space Agency budget is modest, and the estimated budgetary spending for 2022-23 is USD 329 million. In terms of funds allocated for NASA under the president's budget request summary for FY 2022-2027, NASA is expected to receive USD 45 million for the development of space power and nuclear propulsion.

- NASA is expected to receive USD 98 million to develop solar electric propulsion (SEP). In March 2021, NASA, Maxar Technologies, and Busek Co. completed a test of the 6-kilowatt (kW) solar electric propulsion subsystem successfully destined for the PPE. The Solar Electric Propulsion project was anticipated to receive the first qualification thruster from Aerojet Rocketdyne at the beginning of the first quarter of FY 2023. The government allocated funding of USD 110 million for developing nuclear thermal propulsion systems.

North America Space Propulsion Industry Overview

The North America Space Propulsion Market is moderately consolidated, with the top five companies occupying 52.89%. The major players in this market are Ariane Group, Busek Co. Inc., Moog Inc., Northrop Grumman Corporation and Safran SA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Spending On Space Programs

- 4.2 Regulatory Framework

- 4.2.1 Canada

- 4.2.2 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Propulsion Tech

- 5.1.1 Electric

- 5.1.2 Gas based

- 5.1.3 Liquid Fuel

- 5.2 Country

- 5.2.1 Canada

- 5.2.2 United States

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Ariane Group

- 6.4.2 Blue Origin

- 6.4.3 Busek Co. Inc.

- 6.4.4 Moog Inc.

- 6.4.5 Northrop Grumman Corporation

- 6.4.6 OHB SE

- 6.4.7 Safran SA

- 6.4.8 Sierra Nevada Corporation

- 6.4.9 Space Exploration Technologies Corp.

- 6.4.10 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

北米の宇宙推進:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 137 Pages

- 納期

- 2~3営業日