|

市場調査レポート

商品コード

1693965

二成分繊維- 市場シェア分析、産業動向・統計、成長予測(2025~2030年)Bicomponent Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 二成分繊維- 市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

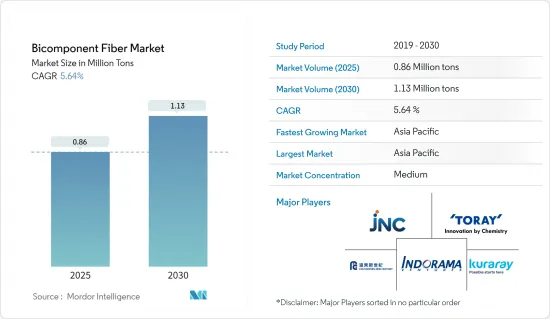

二成分繊維の市場規模は、2025年には86万トンと推定され、予測期間(2025~2030年)のCAGRは5.64%で、2030年には113万トンに達すると予測されています。

COVID-19のパンデミックは世界的規模で、自動車メーカー、衛生、医療、不織布繊維製品メーカーに操業停止を余儀なくさせ、2022年の二成分繊維の需要を低下させました。パンデミックは、製品需要から労働力の開発、パンデミック発生時にすでに進行していた動向の加速や減速に至るまで、これらの産業のほぼあらゆる側面に影響を与えました。顧客とその一時的な生産停止により生産レベルが低下し、需要の減少は生産プロセスに大きな影響を与えました。しかし、状況は回復し、予測期間の後半には調査した市場の成長軌道を回復すると予想されます。

主要ハイライト

- 長期的には、衛生産業における二成分繊維の採用拡大と不織布テキスタイル産業からの需要増加が市場需要を牽引すると予想されます。

- 消費者の認識不足と高い生産コストが市場成長の妨げになると予想されます。

- 再生二成分繊維の将来の用途は、市場に有利な機会を提供すると期待されています。

- アジア太平洋が最も高い市場シェアを占めており、予測期間中はこの地域が市場を独占する可能性が高いです。

二成分繊維市場の動向

衛生産業が市場を独占

- 二成分繊維は、紙おむつや衛生用品に不可欠とされる、ソフトな手触りやその他のユニークな物理的・審美的特性を備えた不織布の製造に利用されています。

- これらの繊維はまた、清潔で、リサイクル可能で、粘着剤が均一に分散しているという万能な特性のために使用されています。これらの繊維不織布は、幼児用トレーニングパンツ、乳児用おむつ、女性用ケア製品、成人用失禁製品、医療用アンダーパッド、創傷ケア、吸収性包帯などの製品に選ばれる材料です。

- さらに、乳幼児の衛生に対する意識の高まりから、親はベビー用おむつやベビー用ワイプの使用を強く推奨しています。おむつは乳幼児の日常ケアに欠かせない製品のひとつであり、ベビーワイプは細菌感染を防ぎ、快適さを提供するのに役立ちます。

- Parenting Modeによると、世界の紙おむつ市場は2022年までに年間約710億米ドルを占めます。赤ちゃんは生後2年間に約6,000枚の紙おむつを使用します。また、キンバリー・クラーク社のパーソナルケア・ブランドのうち、赤ちゃんの衛生用品を含むものは、2021年の1万270米ドルに対し、2022年には1万620米ドルの収益を上げました。

- 2023年4月、ミリームーンのベビー用紙おむつがカナダでの発売を発表しました。ミリー・ムーンは、清潔で高級な紙おむつブランドとして、高機能で美しく作られた紙おむつと敏感肌用ワイプを手頃な価格で提供するとしています。同社はまた、ラグジュアリー紙おむつの材料は赤ちゃんの肌に非常にやわらかく、クラウドタッチソフトネスで最適な快適さを実現するよう設計されているとしています。

- 2022年3月、ナイジェリアにおける事業拡大計画の一環として、キンバリー・クラークはラゴスのイコロドゥに新しい製造施設を開設し、ハギーズのベビー用紙おむつとコーテックスの女性用ケア製品を製造します。1億米ドルを投資した最新鋭の製造施設は、顧客により良いサービスを提供するための最新技術を備えています。

- EDANAによると、2022年には欧州全域で衛生・パーソナルケア用ワイプが不織布の全使用量の45%以上を占めるといいます。

- したがって、世界各地の衛生用品の成長動向と様々なプロジェクトを考慮すると、衛生産業が市場を独占する可能性が高く、その結果、予測期間中に二成分繊維の需要が高まると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋は、2022年にかなりの数量と収益シェアで二成分繊維市場を独占し、予測期間中もその優位性を維持すると予想されます。

- 世界の繊維・衣料品市場セグメントにおいて、中国は過去20年間常に主要な参入企業でした。世界貿易機関(WTO)に加盟して以来、中国の繊維・衣料品製造と販売は劇的に増加したが、これは主に欧米からのビジネス増加によるものです。

- 中国不織布工業繊維協会によると、2022年の中国の不織布生産量は前年比814万トンでした。加えて、中国はスポーツアパレル、アクセサリー、フットウェアを販売する魅力的な市場であり続けています。

- 中国での自動車生産台数の増加は、自動車用織物の消費を高める可能性が高く、これは研究市場の需要をさらにサポートすると予想されます。中国自動車工業協会(CAAM)によると、中国は2022年に2,702万1,000台の自動車を生産し、前年比3.4%の成長率を記録しました。2022年の自動車生産台数のうち、乗用車は2,383万6,000台、商用車は318万5,000台でした。

- 二成分繊維は建設産業の断熱材や床下地材に使用されています。建設セクタは中国の継続的な経済発展の主要鍵です。中国は建設メガブームに沸いています。中国国家統計局によると、建設生産額は2021年の29兆3,000億元(4兆2,000億米ドル)から2022年には31兆2,000億元(4兆5,000億米ドル)に達し、中国は2030年までに13兆米ドル近くを建築に費やすと予想されており、調査された市場には明るい展望が生まれている

- インドの紙おむつ製造企業数社は製品の革新と拡大に注力しており、これが二成分繊維の需要をさらに押し上げる可能性が高いです。例えば、2023年1月、Kimberly-Clarkは、同社の象徴的なおむつブランドであるHuggiesのリニューアルを発表し、インドで新しい「Huggies Complete Comfort」シリーズを発売しました。

- 2023年には、リライアンス・リテールのパフォーマックスアクティブウェアがインドサッカーチームの公式キットスポンサーになりました。この国産スポーツウェアブランドは、サッカーの全競技のキットを製造する独占権を持っています。また、男子、女子、ユースチームを含むAIFF(全インド・サッカー連盟)のすべての試合、遠征、トレーニングウェアの唯一のサプライヤーとなります。これに加えて、商品スポンサーとして、パフォーマックスはこれらの商品の製造・小売の権利も保有する見込みです。

- したがって、上記の理由は、予測期間にわたってアジア太平洋における二成分繊維市場の成長を促進すると考えられます。

二成分繊維産業概要

二成分繊維市場は部分的にセグメント化されており、複数の企業が世界レベルと地域レベルの両方で事業を展開しています。市場の主要企業(順不同)には、Indorama Ventures Public Company Limited、Far Eastern New Century Corporation、JNC Corporation、KURARAY、TORAY INDUSTRIES, INC.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 衛生産業における二成分繊維の採用拡大

- 不織布産業からの需要増加

- 抑制要因

- 消費者の認識不足と高い生産コスト

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 材料

- ポリエチレン(PE)/ポリプロピレン(PP)

- ポリプロピレン(PP)/ポリエチレンテレフタレート(PET)

- 高密度ポリエチレン/低密度ポリエチレン

- ポリエチレン/ポリエチレンテレフタレート(ペット)

- ポリエステル/PBT

- その他

- 構造タイプ

- シースコア

- サイド・バイ・サイド

- 海の中の島

- その他の構造タイプ

- エンドユーザー産業

- 不織布

- 自動車

- 衛生産業

- 建築

- 医療

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- CHA Technologies Group

- EMS-chemie Holding AG

- Far Eastern New Century Corporation

- Freudenberg Performance Materials

- Huvis Corp.

- Indorama Ventures Public Company Limited

- JNC Corporation

- Kolon Glotech

- Kuraray Co. Ltd.

- OC Oerlikon Management AG

- PTT Global Chemical Public Company Limited

- Shaoxing Yaolong Spunbonded Nonwoven Technology Co. Ltd

- TEIJIN Limited

- TORAY Industries Inc.

- WPT Nonwovens Corp.

第7章 市場機会と今後の動向

- 再生二成分繊維の今後の用途

The Bicomponent Fiber Market size is estimated at 0.86 million tons in 2025, and is expected to reach 1.13 million tons by 2030, at a CAGR of 5.64% during the forecast period (2025-2030).

The COVID-19 pandemic, on a global scale, forced automakers, hygiene, medical, and non-woven textile products manufacturers to shut down their operations, lowering the demand for bicomponent fiber in 2022. The pandemic impacted almost every aspect of these industries, from product demand to workforce development to accelerating or decelerating trends already underway when it struck. Customers and their temporary production stops reduced production levels, and demand reductions significantly impacted production processes. However, the condition is expected to recover, restoring the growth trajectory of the market studied during the latter half of the forecast period.

Key Highlights

- In the long term, the growing adoption of bicomponent fiber in the hygiene industry and rising demand from the non-woven textile industry are expected to drive market demand.

- Lack of consumer awareness and high production cost is expected to hinder the market's growth.

- Nevertheless, future applications of recycled bicomponent fibers is expected to offer lucrative opportunities to the market.

- Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Bicomponent Fiber Market Trends

Hygiene Industry to Dominate the Market

- Bicomponent fibers are utilized to produce nonwoven fabrics with a soft touch, along with other unique physical and aesthetic properties, which are deemed essential for diapers and hygiene products.

- These fibers are also used due to their versatile properties of being clean, recyclable, and have a uniform distribution of adhesive. These fiber nonwovens are the material of choice for products such as toddler training pants, infant diapers, feminine care products, adult incontinence products, medical underpads, wound care, and absorbent bandages, among others.

- Furthermore, owing to the increasing awareness about infant hygiene, parents are strongly adopting the usage of baby diapers and baby wipes. Diapers are among the essential infant daily care products, and baby wipes help prevent bacterial infection and provide comfort.

- According to the Parenting Mode company, the global disposable diaper market accounted for approximately USD 71 billion/year by 2022. Babies use about 6,000 diapers during their first two years of life. In addition, the personal care brands of Kimberly Clark, which include baby hygiene products, generated a revenue of USD 10.62 thousand in 2022 as compared to USD 10.27 Thousand in 2021.

- In April 2023, Millie Moon baby diapers announced their launch in Canada. Millie Moon claims to be a clean, luxury diaper brand offering high-performance and beautifully crafted diapers and sensitive wipes at affordable prices. The company also claims that the materials in its Luxury Diapers are extremely soft on babies' skin and engineered with CloudTouch Softness for optimum comfort.

- In March 2022, as part of its expansion plans in Nigeria, Kimberly-Clark opened a new manufacturing facility in Ikorodu, Lagos, which will manufacture Huggies baby diapers as well as Kotex feminine care products. With the investment of USD 100 million in its new state-of-the-art manufacturing facility, the company is equipped with the latest technology to serve its customers better.

- According to EDANA, in 2022, hygiene and personal care wipes accounted for more than 45% of all nonwoven use across Europe.

- Therefore, considering the growth trends and various projects of hygiene products in different regions worldwide, the hygiene industry is likely to dominate the market, which, in turn, is expected to enhance the demand for bicomponent fiber during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region dominated the bicomponent fiber market in 2022, with a considerable volume and revenue share, and is expected to maintain its dominance during the forecast period.

- In the global textile and clothing market segment, China has always been a major player for the last two decades. Since becoming a member of the World Trade Organization, China's textile and clothing manufacturing and sales have increased dramatically, largely due to increased business from the West.

- According to the China Nonwovens and Industrial Textiles Association, the output of nonwovens in China was 8.14 million tons Y-o-Y in 2022. In addition, China continues to be an attractive market for selling athletic apparel, accessories, and footwear.

- The rising production of automobiles in China is likely to enhance the consumption of automotive textiles, which is expected to further support the demand for the studied market. According to the China Association of Automobile Manufacturers (CAAM), China produced 27,021 thousand units of automobiles in 2022, registering a growth rate of 3.4% compared to the previous year. Out of the automobile production in 2022, passenger cars accounted for 23,836 thousand units, whereas commercial car production accounted for 3,185 thousand units.

- Bicomponent fiber is used for insulation and flooring underlayment in the construction industry. The construction sector is key to China's continued economic development. China is amid a construction mega-boom. According to the National Bureau of Statistics of China, The value of construction output accounted for 31.2 trillion yuan (USD 4.5 trillion) in 2022, up from 29.3 trillion yuan (USD 4.2 trillion) in 2021, China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive outlook for the studied market.

- Several diaper manufacturing companies in India are focusing on product innovation and expansion, which is further likely to drive the demand for bicomponent fibers. For instance, in January 2023, Kimberly-Clark announced the relaunch of its iconic diaper brand, Huggies, with the new 'Huggies Complete Comfort' range in India.

- In 2023, Reliance Retail's Performax activewear became the official kit sponsor for the Indian football team. The homegrown sportswear brand will have the exclusive rights to manufacture kits across all formats of the game. The firm will also be the sole supplier for all matches, travel, and training wear for the AIFF (All India Football Federation), including men's, women's, and youth teams. In addition to this, as the merchandise sponsor, Performax is also expected to hold the rights to manufacture and retail these products.

- Hence, the reasons mentioned above are likely to fuel the growth of the bicomponent fiber market in Asia-Pacific over the forecast period.

Bicomponent Fiber Industry Overview

The bicomponent fiber market is partially fragmented, with several companies operating on both global and regional levels. Some of the major players in the market (Not in any particular order) include Indorama Ventures Public Company Limited, Far Eastern New Century Corporation, JNC Corporation, KURARAY CO., LTD., and TORAY INDUSTRIES, INC., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Adoption of Bicomponent Fiber In the Hygiene Industry

- 4.1.2 Rising Demand From the Non-woven Textile Industry

- 4.2 Restraints

- 4.2.1 Lack of Consumer Awareness and High Production Cost

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume and Revenue)

- 5.1 Material

- 5.1.1 Polyethylene (PE)/Polypropylene (PP)

- 5.1.2 Polypropylene (PP)/polyethylene Terephthalate (PET)

- 5.1.3 High-density Polyethylene/Low-density Polyethylene

- 5.1.4 Polyethylene/polyethylene Terephthalate (pet)

- 5.1.5 Polyester/PBT

- 5.1.6 Other Materials

- 5.2 Structure Types

- 5.2.1 Sheath-core

- 5.2.2 Side-by-Side

- 5.2.3 Islands in the Sea

- 5.2.4 Other Structure Types

- 5.3 End-user Industry

- 5.3.1 Non-Woven Textiles

- 5.3.2 Automotive

- 5.3.3 Hygiene

- 5.3.4 Construction

- 5.3.5 Medical

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 CHA Technologies Group

- 6.4.2 EMS-chemie Holding AG

- 6.4.3 Far Eastern New Century Corporation

- 6.4.4 Freudenberg Performance Materials

- 6.4.5 Huvis Corp.

- 6.4.6 Indorama Ventures Public Company Limited

- 6.4.7 JNC Corporation

- 6.4.8 Kolon Glotech

- 6.4.9 Kuraray Co. Ltd.

- 6.4.10 OC Oerlikon Management AG

- 6.4.11 PTT Global Chemical Public Company Limited

- 6.4.12 Shaoxing Yaolong Spunbonded Nonwoven Technology Co. Ltd

- 6.4.13 TEIJIN Limited

- 6.4.14 TORAY Industries Inc.

- 6.4.15 WPT Nonwovens Corp.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Applications of Recycled Bicomponent Fibers