|

市場調査レポート

商品コード

1687075

天然繊維強化複合材料:市場シェア分析、産業動向、成長予測(2025~2030年)Natural Fiber Reinforced Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 天然繊維強化複合材料:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

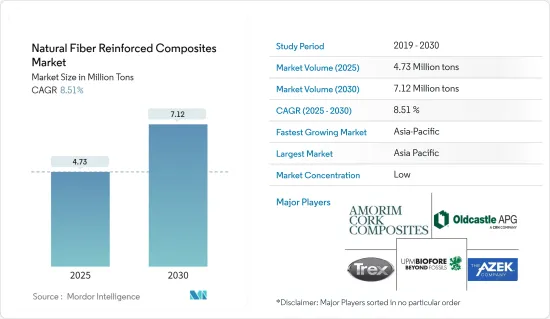

天然繊維強化複合材料の市場規模は、2025年に473万トンと推定され、予測期間(2025~2030年)のCAGRは8.51%で、2030年には712万トンに達すると予測されます。

中期的には、バイオベース複合材料の需要増加や世界の自動車産業の成長といった要因が、2024~2029年にかけて天然繊維強化複合材料市場を牽引するとみられます。

主要ハイライト

- しかし、水分の吸着、加工温度の制限、ほとんどのポリマーマトリックスとの非相溶性、外部環境にさらされることによる劣化の問題などが、市場抑制要因になりそうです。

- 建築・建設産業における人気の高まりは、市場に新たな機会をもたらすと予想されます。

- アジア太平洋が市場を独占し、2024~2029年のCAGRが最も高くなると予想されます。

天然繊維強化複合材料の市場動向

建設産業が市場を独占する見込み

- 建築材料産業では、エコフレンドリー材料が常に求められています。天然繊維強化ポリマーをベースとした複合材料は、その数多くの利点から、土木建築用途でますます使用されるようになっています。

- 建築・建設産業において、複合材料は極めて重要な役割を担っています。産業用支柱、タンク、ロングスパン屋根構造、高層ビル、軽量ドア、窓、家具、軽量ビル、橋梁部品、橋梁システム一式はすべて複合材料を採用しています。複合材料は、長期的な持続可能性を達成するために、建設産業においてますます不可欠になってきています。

- 建設部門では近年、大規模な投資が行われています。Oxford Economicsによると、世界の建設産業は2020~2030年の間に4兆5,000億米ドル(42%)成長し、15兆2,000億米ドルに達すると予想されています。また、中国、インド、米国、インドネシアは、2020~2030年にかけての建設における世界成長の58.3%を占めると予想されています。

- さらに、建設部門は中国の継続的な経済発展と天然繊維強化複合材料製品の需要に大きく貢献しています。中国は建設メガブームに沸いています。さらに、住宅・都市・農村開発省の予測によると、中国の建設部門は2025年までGDPの6%を維持すると予想されています。

- 建設部門は、中国の継続的な経済発展の主役です。中国国家統計局によると、建設生産額は2021年の29兆3,000億人民元(4兆2,000億米ドル)から2022年には31兆2,000億人民元(4兆5,000億米ドル)に増加します。中国は2030年までに建築物に13兆米ドル近くを投じると予想されており、天然繊維強化複合材料にとって明るい展望となっています。

- 北米では、米国が建設産業で大きなシェアを占めています。米国のほか、カナダとメキシコも建設部門への投資に大きく貢献しています。米国国勢調査局データによると、米国の公共住宅建設の年間金額は2022年に91億5,000万米ドルと評価され、2017年の67億4,000万米ドルと比較して35.7%増加しました。

- 同様に、ユーロ統計によれば、2023年の建設業の年間平均生産額は、2022年と比較して、ユーロ圏では0.2%増、欧州連合では0.1%増でした。建設業の年間生産高が最も増加したのは、ルーマニア(30.7%増)、ポーランド(18.9%増)、ベルギー(10.7%増)でした。

- したがって、前述の動向は2024~2029年にかけての建設セクターにおける天然繊維強化複合材料の成長に影響を与えると予測されます。

アジア太平洋が市場を独占する見込み

- アジア太平洋が世界市場を独占すると予想されます。中国、インド、日本などの国々で建設活動が活発化しているため、この地域では天然繊維強化複合材料の使用量が増加しています。

- 住宅・都市・農村開発省によると、中国の建設部門は2025年までGDPの6%を維持すると予想されています。この予測を受け、中国政府は2022年1月、建設部門をより持続可能で品質主導のものにするための5カ年計画を発表しました。

- 同様に、天然繊維強化複合材料のエレクトロニクス産業への応用が急増していることも、同国の産業成長を支えることになりそうです。India Brand Equity Foundation(IBEF)によると、インドの電子機器製造業は2025年までに5,200億米ドルに達すると予想されています。

- さらに、自動車は天然繊維強化複合材料の主要な消費者のひとつです。インドの自動車産業は、技術進歩とマクロ経済の拡大の両面で重要な役割を果たしているため、インド経済の業績を示す重要な指標となっています。

- さらに、インド政府は、2030年までに電気自動車(EV)普及率30%を目指す「(ハイブリッド車と)電気自動車の迅速な導入と製造(Faster Adoption and Manufacturing of(Hybrid and)Electric Vehicles)」計画を通じて、電気自動車(EV)の導入を奨励し、一部のセグメントでは義務化することで、勢いを生み出しています。この計画は、EVに対する需要インセンティブを創出し、都市中心部への充電技術とステーションの配備を支援するものです。政府は、2030年までにインドで販売される商用車の70%、自家用車の30%、バスの40%、二輪車と三輪車の80%を電気自動車にするという目標を掲げています。

- したがって、さまざまな政府による新しい施策と投資が、2024~2029年にかけて、その他のアジア太平洋の天然繊維強化複合材料市場の需要を押し上げると予想されます。

天然繊維強化複合材料産業概要

天然繊維強化複合材料市場は細分化されています。主要参入企業(順不同)には、Trex Company Inc.、The AZEK Company Inc.、Oldcastle APG Inc.、UPM、Amorim Cork Composites SAなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- バイオベース複合材料の需要増加

- 世界の自動車産業の成長

- 抑制要因

- 水分吸着、加工温度の制限、大半のポリマーマトリックスとの非相溶性

- 外部環境への暴露による劣化問題

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 繊維

- 木材繊維複合材料

- 非木材繊維複合材料

- 綿

- 亜麻

- ケナフ

- 麻

- その他の非木材繊維複合材料(ジュート、サイザル麻、アバカ、コアー、パイナップル、バナナ)

- ポリマー

- 熱硬化性樹脂

- 熱可塑性プラスチック

- ポリエチレン

- ポリプロピレン

- ポリ塩化ビニル

- その他の熱可塑性プラスチック(ポリカーボネート、ポリアミド、ポリブチレンテレフタレート(PBT))

- エンドユーザー産業

- 航空宇宙

- 自動車

- 海洋

- 建築・建設

- 電気・電子

- スポーツ

- その他のエンドユーザー産業(電力産業(風力タービン)、医療など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Amorim Cork Composites SA

- Beologic

- BPREG Composites

- Fiberon

- FKuR

- Flexform Technologies

- Green Dot Bioplastics

- GreenGran BN

- JELU-WERK J. Ehrler GmbH & Co. KG

- Oldcastle APG

- TECNARO GmbH

- The AZEK Company Inc.

- Trex Company Inc.

- UFP Technologies Inc.

- UPM

- Wuhu Haoxuan Wood Plastic Composite Co. Ltd

第7章 市場機会と今後の動向

- 建築・建設産業における人気の高まり

The Natural Fiber Reinforced Composites Market size is estimated at 4.73 million tons in 2025, and is expected to reach 7.12 million tons by 2030, at a CAGR of 8.51% during the forecast period (2025-2030).

In the medium term, factors such as the increasing demand for bio-based composites and the growth of the global automotive industry are likely to drive the natural fiber-reinforced composites market between 2024 and 2029.

Key Highlights

- However, moisture adsorption, restricted processing temperature, incompatibility with most polymer matrices, and degradation issues due to exposure to the external environment are likely to act as restraints for the market.

- Nevertheless, increasing popularity in the building and construction industry is expected to provide new opportunities for the market.

- Asia-Pacific is expected to dominate the market and is likely to witness the highest CAGR from 2024 to 2029.

Natural Fiber Reinforced Composites Market Trends

The Construction Industry is Expected to Dominate the Market

- There is always a continuous requirement for eco-friendly materials in the building materials industry. Natural fiber-reinforced polymer-based composites are increasingly used in civil engineering construction applications due to their numerous advantages.

- In the building and construction industry, composite materials are extremely significant. Industrial supports, tanks, long-span roof structures, high-rise buildings and lightweight doors, windows, furnishings, lightweight buildings, bridge components, and complete bridge systems have all employed composite materials. Composite materials are becoming increasingly essential in the construction industry to achieve long-term sustainability.

- The construction sector has witnessed major investments in recent years. According to Oxford Economics, the global construction industry is expected to grow by USD 4.5 trillion, or 42%, between 2020 and 2030 to reach USD 15.2 trillion. Also, China, India, the United States, and Indonesia are expected to account for 58.3% of global growth in construction between 2020 and 2030.

- Additionally, the construction sector is a key contributor to China's continued economic development and demand for natural fiber-reinforced composite products. China is amid a construction mega-boom. Moreover, as per the forecast given by the Ministry of Housing and Urban-Rural Development, the Chinese construction sector is expected to maintain a 6% share of the country's GDP going into 2025.

- The construction sector is a key player in China's continued economic development. According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.3 trillion (USD 4.2 trillion) in 2021. China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive outlook for natural fiber-reinforced composites.

- In North America, the United States has a major share in the construction industry. Besides the United States, Canada and Mexico contribute significantly to investments in the construction sector. According to the United States Census Bureau Data, the annual value of public residential construction in the United States was valued at USD 9.15 billion in 2022, an increase of 35.7% compared to USD 6.74 billion in 2017.

- Similarly, as per the Eurostat, the annual average production in construction for 2023, compared to 2022, increased by 0.2% in the euro area and by 0.1% in the European Union. The highest annual increases in construction production were recorded in Romania (+30.7%), Poland (+18.9%), and Belgium (+10.7%).

- Hence, the aforementioned trends are projected to influence the growth of natural fiber-reinforced composites in the construction sector between 2024 and 2029.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is expected to dominate the global market. With growing construction activities in countries such as China, India, and Japan, the usage of natural fiber-reinforced composites is increasing in the region.

- As per the Ministry of Housing and Urban-Rural Development, the Chinese construction sector is expected to maintain a 6% share of the country's GDP going into 2025. With the given forecasts, the Chinese government unveiled a five-year plan in January 2022 to make the construction sector more sustainable and quality-driven.

- Similarly, the surging application of natural fiber-reinforced composites in the electronics industry is likely to support the country's industry growth. According to the India Brand Equity Foundation (IBEF), the Indian electronics manufacturing industry is expected to reach USD 520 billion by 2025.

- Furthermore, automotive is among the major consumers of natural fiber-reinforced composites. The automotive industry in India is an important indicator of the Indian economic performance, as this sector plays a vital role in both technological advancements and macroeconomic expansion.

- Additionally, the Indian government has created momentum through its Faster Adoption and Manufacturing of (Hybrid and) Electric Vehicles schemes that encourage, and in some segments, mandate the adoption of electric vehicles (EV), intending to reach 30% EV penetration by 2030. The scheme creates demand incentives for EVs and supports the deployment of charging technologies and stations in urban centers. The government has set a target of 70% of all commercial cars, 30% of private cars, 40% of buses, and 80% of two-wheelers and three-wheelers sold in India by 2030 to be electric.

- Hence, the new policies and investments made by different governments are expected to boost the demand for the natural fiber-reinforced composites market in the rest of Asia-Pacific between 2024 and 2029.

Natural Fiber Reinforced Composites Industry Overview

The natural fiber reinforced composites market is fragmented in nature. Major players (not in any particular order) include Trex Company Inc., The AZEK Company Inc., Oldcastle APG Inc., UPM, and Amorim Cork Composites SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Bio-based Composites

- 4.1.2 Growth in the Automotive Industry Worldwide

- 4.2 Restraints

- 4.2.1 Moisture Adsorption, Restricted Processing Temperature, and Incompatibility with Most of the Polymer Matrices

- 4.2.2 Degradation Issue Due to Exposure to the External Environment

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Fiber

- 5.1.1 Wood Fiber Composites

- 5.1.2 Non-wood Fiber Composites

- 5.1.2.1 Cotton

- 5.1.2.2 Flax

- 5.1.2.3 Kenaf

- 5.1.2.4 Hemp

- 5.1.2.5 Other Non-wood Fiber Composites (Jute, Sisal, Abaca, Coir, Pineapple, and Banana)

- 5.2 Polymer

- 5.2.1 Thermosets

- 5.2.2 Thermoplastics

- 5.2.2.1 Polyethylene

- 5.2.2.2 Polypropylene

- 5.2.2.3 Poly Vinyl Chloride

- 5.2.2.4 Other Thermoplastics (Polycarbonate, Polyamide, and Polybutylene Terephthalate (PBT))

- 5.3 End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Automotive

- 5.3.3 Marine

- 5.3.4 Building and Construction

- 5.3.5 Electrical and Electronics

- 5.3.6 Sports

- 5.3.7 Other End-user Industries (Power Industry (Wind Turbines), Medical, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Amorim Cork Composites SA

- 6.4.2 Beologic

- 6.4.3 BPREG Composites

- 6.4.4 Fiberon

- 6.4.5 FKuR

- 6.4.6 Flexform Technologies

- 6.4.7 Green Dot Bioplastics

- 6.4.8 GreenGran BN

- 6.4.9 JELU-WERK J. Ehrler GmbH & Co. KG

- 6.4.10 Oldcastle APG

- 6.4.11 TECNARO GmbH

- 6.4.12 The AZEK Company Inc.

- 6.4.13 Trex Company Inc.

- 6.4.14 UFP Technologies Inc.

- 6.4.15 UPM

- 6.4.16 Wuhu Haoxuan Wood Plastic Composite Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Popularity in the Building and Construction Industry