|

市場調査レポート

商品コード

1408767

加工用半導体デバイス-市場シェア分析、産業動向・統計、2024~2029年成長予測Semiconductor Device For Processing Applications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 加工用半導体デバイス-市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

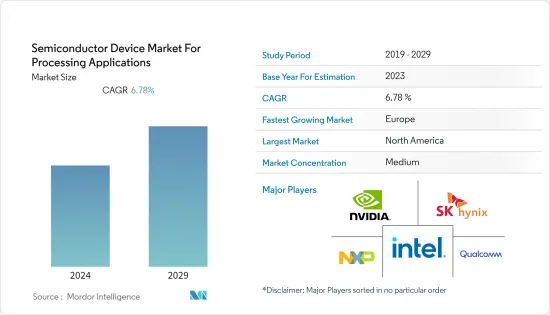

加工用半導体デバイス市場は、今年度2,011億米ドル、CAGR 6.78%を記録し、予測期間終了時には2,792億6,000万米ドルに達すると予測されます。

主なハイライト

- 半導体産業は急速な成長を遂げており、半導体はあらゆる現代技術の基本構成要素となっています。この分野の進歩や革新は、結果的にすべての川下技術に直接的な影響を及ぼしています。

- 半導体は、あらゆるコンピューティング・デバイスの構成要素を形成しています。例えば、多くのトランジスタが論理ゲートを構成し、コンピュータが使用する1と0のコードである2進情報を処理します。これらの半導体デバイスは、メモリブロックとしてバイナリコードを保持することもできます。

- スマートフォン、PC、ノートパソコンなどのコンピューティング・デバイスの普及に伴い、世界・ネットワーク上で生成され、しばしばリアルタイムで通信されるデータ量が急増しています。この成長に対応するため、ハイパフォーマンス・コンピューティング(HPC)が重要な役割を果たすようになり、大きな成長を遂げています。HPCとは、データを処理し、複雑な計算を高速で実行し、性能集約的な問題を解決することを指します。センサーやオプトエレクトロニクスのような多くの半導体デバイスは、HPCアプリケーションを実現するために必要です。

- ハイパフォーマンス・コンピューティング(HPC)は、半導体業界の重要な促進要因として浮上しています。

- さらに、COVID-19の流行はデジタル・プラットフォームとクラウド・サービスの利用を加速させ、データセンター開発の急増をもたらしました。データセンターとは、アプリケーションやデータを保管・共有する施設のことです。

- また、半導体はデータセンターの主要コンポーネントとして機能します。中央演算処理装置(CPU)、グラフィックス・プロセッシング・ユニット(GPU)、メモリー、ネットワーク・インフラ用チップ、電源管理など、さまざまなデバイスが使用されます。そのため、半導体メモリーチップは、データセンターでデータを保存・管理するための重要なデバイスであり、その性能はデータセンター運営の成功に欠かせないです。

半導体デバイス市場の動向

集積回路下のメモリが市場の需要を押し上げる見込み

- 半導体メモリは、集積回路上に半導体電子デバイスを実装したデジタル電子データ記憶装置です。DRAM、SRAM、NORフラッシュ、NANDフラッシュ、ROM、EPROMなど、さまざまな種類のメモリがあります。DRAM、SRAM、NANDフラッシュ、ROM、EPROMなどさまざまな種類のメモリがあり、パソコン、ノートパソコン、カメラ、携帯電話などのデジタル家電製品に広く使われています。

- データセンター需要の増加もメモリ部品の需要を後押ししています。現在、北米における大規模なデータセンター・プロジェクトが、DRAMをはじめとするメモリ需要の好調に寄与しています。しかし、ユーザー1人当たりのデータセンター面積を示す指標によると、中国のインターネット・データセンターは少なくとも米国の22倍、少なくとも現在の日本の10倍にまで成長する見込みです。したがって、DRAMには大きな成長機会があり、半導体デバイス産業に影響を与えています。

- さらに、ポータブル・システム市場の成長により、半導体業界は大容量記憶装置用途の不揮発性メモリー(NVM)技術に関心を寄せています。より高い効率性、より高速なメモリアクセス、低消費電力に対する需要の高まりは、NVM市場の成長を促す重要な要因のひとつです。データセンター・アプリケーションでは、突然の停電からデータ損失を保護するためにNVMの必要性が高まっています。データセンターの増加に伴い、次世代不揮発性メモリの採用も増加し、市場成長を牽引すると予想されます。

- さらに、WSTSによると、2022年のメモリ・コンポーネント販売による収益は1,344億1,000万米ドルに達すると予測され、2021年には1,548億4,000万米ドルを記録しました。しかし、メモリ部品販売収入は減少し、1,116億2,000万米ドルと推定されるが、近い将来に成長し、2023年末には、良好な成長を達成する可能性が高いです。このような要因が市場成長を後押しする可能性が高いです。

- サムスンはパートナーシップに参加しています。エンドユーザーは、様々なデバイス・サプライヤーや垂直統合型のハードウェアおよびソフトウェア企業が、今後のストレージ・ソリューションをサポートすることを確信できると思われます。例えば、2022年3月、サムスン電子とウェスタンデジタルは、次世代データ配置・処理・ファブリック(D2PF)ストレージ技術の標準化と普及のために協力することで合意しました。両社は、こうしたステップを踏むことで、業界が幅広いアプリケーションに集中できるようになり、最終的に顧客により多くの価値を提供できるようになることを期待しています。

- また、2022年7月、マイクロン・テクノロジー社は、ストレージ・ソリューションの前例のない性能を推進するために、業界をリードするイノベーションで構築された世界初の232層NANDの量産を開始したと発表しました。同社の232層 NANDは、3D NANDを200層以上に拡張できることを初めて実証したもので、ストレージ革新の分水嶺となります。

欧州地域が著しい成長を遂げる見込み

- 欧州地域は、世界中で最も重要な技術の中心地であり、現代技術の重要な推進者であり採用者です。先端技術の浸透が進み、半導体の採用が増加していることが、同地域の市場成長を牽引しています。

- モノのインターネット(IoT)の台頭により、半導体デバイスはあらゆるタイプのデバイスに組み込まれ、コンピューティングやデータストレージの応用範囲が広がっています。これらのデバイスに対する需要も着実に増加しています。最先端のメモリーやロジックデバイス、パワー半導体デバイス、各種センサーの性能を向上させるために、材料やアーキテクチャは着実に進化しています。

- さらに、5Gの展開はIoT接続、自動化、エッジ技術の実現につながると考えられています。このよりスマートな規格の新しいデバイスは、メモリやストレージの容量がさらに大きく、より高性能なウエハーを製造することを工場に要求します。

- 5Gネットワークと技術は、既存の市場分野や産業を変革することで、無線通信にさらなる革命をもたらそうとしています。同社によると、2021年から2025年にかけて、5Gは欧州経済におけるすべての主要産業で最大2兆億ユーロ(2兆1,700億米ドル)の新規売上高を創出します。そのため、5Gを実現する新しいデバイスには、メモリやストレージの容量がさらに大きく、より高性能なウエハーを製造するファブが必要になります。

- インテルは2022年3月、研究開発、製造、パッケージング技術を含む半導体バリューチェーン全体で今後10年間にEUに800億ユーロ(868億4,000万米ドル)を投資する計画の第1段階を発表しました。この投資ではさらに、ドイツでの半導体工場メガサイトの設立、フランスでの新しい研究開発・設計施設の開発、イタリア、ポーランド、アイルランド、スペインでの研究開発、製造、ファウンドリーサービスへの投資に約170億ユーロ(184億5,000万米ドル)を投資する計画です。

半導体デバイス産業の概要

加工用半導体デバイス市場は、統合の進展、技術の進歩、進化する地政学的シナリオの中で、複数の競合他社が変動を乗り越えており、適度な断片化を経験しています。イノベーションを通じて持続可能な競争優位性を確立することが最も重要な市場において、このような競争の激化はさらに深刻化するものと思われます。半導体製造セクターのエンドユーザーからの品質への期待を考えると、ブランド・アイデンティティはこの情勢において極めて重要な役割を果たしています。

主に、Intel Corporation、Nvidia Corporation、京セラ株式会社、Qualcomm Technologies Inc.など、業界をリードする重要な既存企業の存在により、市場浸透度は際立って高いです。

2022年4月、SKハイニックスは、サンノゼに拠点を置く子会社ソリディグムと共同で、データセンター向けに設計されたP5530として知られる最新のソリッド・ステート・ドライブ(SSD)を発表しました。SSDはフラッシュメモリーを活用してデータを保存するもので、この革新的なデバイスはSKハイニックスの主力製品である128層4D NANDとソリディグムのSSDコントローラーを組み合わせたものです。

2022年3月、サムスン電子とウエスタンデジタルは、次世代データ配置・処理・ファブリック(D2PF)ストレージ技術の標準化と普及で協力することで合意しました。両社の共同努力は、業界の慣行を合理化し、最終的に顧客により大きな価値を提供する幅広いアプリケーションを可能にすることを目的としています。

2022年1月、キオクシアはユニバーサル・フラッシュ・ストレージ(UFS)Ver.3.1内蔵フラッシュ・メモリ・デバイスの発売を発表しました。これらのデバイスは、単一パッケージで利用可能な最高密度を達成する能力を持つ、同社の先駆的なセルあたり4ビットのクアッドレベルセル(QLC)技術を活用しています。この技術は、特にハイエンド・スマートフォンなどの高密度アプリケーションに適しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 技術動向

- 業界のバリューチェーン/サプライチェーン分析

- 業界の魅力度ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済動向が市場に与える影響

第5章 市場力学

- 市場促進要因

- IoTやAIなどの技術の採用拡大

- 5Gの普及とデータセンター需要の増加

- 市場の課題

- 半導体チップ不足をもたらすサプライチェーンの混乱

第6章 市場セグメンテーション

- デバイスタイプ別

- ディスクリート半導体

- オプトエレクトロニクス

- センサー

- 集積回路

- アナログ

- ロジック

- メモリー

- マイクロ

- マイクロプロセッサ(MPU)

- マイクロコントローラー(MCU)

- デジタル・シグナル・プロセッサー

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第7章 競合情勢

- 企業プロファイル

- Intel Corporation

- Nvidia Corporation

- Qualcomm Incorporated

- NXP Semiconductors NV

- SK Hynix Inc.

- Kyocera Corporation

- Samsung Electronics Co., Ltd.

- Advanced Micro Devices, Inc

- ST microelectronics Nv

- Micron Technology Inc.

- Toshiba Electronic Devices And Storage Corporation

- Infineon Technologies AG

第8章 投資分析

第9章 市場の将来

The semiconductor device market for processing applications is estimated at USD 201.1 billion in the current year, registering a CAGR of 6.78%, to reach USD 279.26 billion by the end of the forecast period.

Key Highlights

- The semiconductor industry is witnessing rapid growth, with semiconductors emerging as the basic building blocks of all modern technology. The advancements and innovations in this field are resulting in a direct impact on all downstream technologies.

- Semiconductors form the building blocks of any computing device. For instance, many transistors make up a logic gate that processes binary information, the code of ones and zeros computers use. These semiconductor devices can also retain binary code as memory blocks.

- With the growing popularity of computing devices like smartphones, PCs, and laptops, the amount of data generated and communicated across a global network, often in real-time, has grown rapidly. To keep up with this growth, High-performance computing (HPC) has become crucial and is seeing significant growth. HPC refers to processing data and performing complex calculations at high speeds to solve performance-intensive problems. Many semiconductor devices like sensors and optoelectronics are required to enable HPC applications.

- High-performance computing (HPC) has emerged as an important growth driver for the semiconductor industry. For instance, Taiwan Semiconductor Manufacturing Co. (TSMC) expects the HPC platform to be the strongest-growing platform in 2022 and the largest contributor to the company's growth, fueled by the structural mega-trend, driving rising needs for higher computing power and energy-efficient computing.

- Further, the COVID-19 pandemic accelerated the use of digital platforms and cloud services, resulting in a surge in data center development. A data center is a facility that stores and shares applications and data.

- Also, semiconductors serve as a primary component for data centers. Different devices are used, like central processing units (CPUs), graphics processing units (GPUs), memory, chips for network infrastructure, and power management. Therefore, semiconductor memory chips are the key devices for storing and managing data in data centers, and their performance is crucial to the success of data center operations.

Semiconductor Device Market Trends

Memory Segment Under Integrated Circuits is Expected to Boost The Demand in The Market

- The semiconductor memory is a digital electronic data storage device implemented with semiconductor electronic devices on an integrated circuit. Different types of memory are available, such as DRAM, SRAM, Nor Flash, NAND Flash, ROM, and EPROM. They find widespread application in digital consumer products like PCs, laptops, cameras, and phones.

- The increasing demand for data centers is also bolstering the demand for memory components. Currently, large data center projects in North America have contributed to the strong demand for memory, such as DRAM. However, according to the measure of data center space per user, China's internet data centers are poised to grow to at least 22 times that of the United States or at least 10 times the current space of Japan. Hence, DRAM has a significant opportunity for growth and thus is impacting the semiconductor device industry.

- Further, the growth of the portable systems market attracted the semiconductor industry's interest in non-volatile memory (NVM) technologies for mass storage applications. The rise in demand for greater efficiency, faster memory access, and low power consumption are some of the significant factors driving the NVM market growth. There is an increasing need for NVM in data center applications to protect data losses from a sudden power outage. With the growth of data centers, the adoption of next-generation non-volatile memory is also expected to increase, driving market growth.

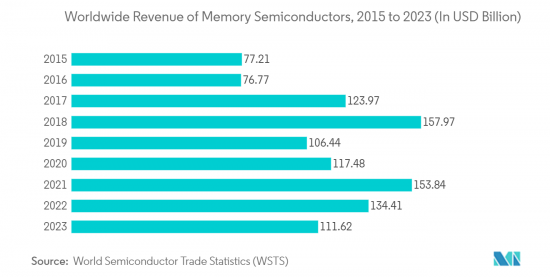

- Moreover, according to WSTS, In 2022, it is projected that revenue from memory component sales will amount to USD 134.41 billion, and in 2021 the recorded revenue of USD 154.84 billion. However, the revenue from memory component sales decreased, with an estimated amount of USD 111.62 billion, but it is likely to grow in the near future, and by the end of 2023, it will achieve good growth. Such factors are likely to boost the market growth.

- Samsung participates in partnerships; end users may be sure that various device suppliers and vertically integrated hardware and software firms will support its upcoming storage solutions. For instance, in March 2022, Samsung Electronics and Western Digital agreed to work together to standardize and promote next-generation data placement, processing, and fabrics (D2PF) storage technologies. They hope that by taking these steps, the industry will be able to concentrate on a wide range of applications that will ultimately provide customers with more value.

- Also, in July 2022, Micron Technology, Inc. announced that it had begun volume production of the world's first 232-layer NAND, built with industry-leading innovations to drive unprecedented performance for storage solutions. The company's 232-layer NAND is a watershed moment for storage innovation as the first proof of the capability to scale 3D NAND to more than 200 layers in production.

European Region Expected to Witness the Significant Growth

- The European region is home to some of the most crucial technology hubs across the globe and a critical driver and adopter of modern technology. The increasing penetration of advanced technologies and the increasing adoption of semiconductors drives market growth in the region.

- With the rise of the Internet of Things (IoT), semiconductor devices are being incorporated into all types of devices, with a wider range of computing and data storage applications. Demand for these devices is also steadily increasing. Materials and architecture are steadily evolving to improve the performance of cutting-edge memory and logic devices, power semiconductor devices, and various types of sensors.

- Furthermore, the rollout of 5G is perceived to be the enabler of IoT connectivity, automation, and edge technologies. New devices in this smarter standard will require fabs to produce higher-performing wafers with even greater capacity for memory and storage.

- 5G networks and technology are further revolutionizing wireless communications by transforming existing market sectors and industries. As per the company, between 2021 and 2025, 5G will drive up to EUR 2.0 trillion (USD 2.17 trillion) in total new sales across all major industries in the European economy. As such, new devices that enable 5G will require fabs to produce higher-performing wafers with even greater capacity for memory and storage.

- In March 2022, Intel issued the first phase of its EUR 80 billion (USD 86.84 billion) investment plan in the EU over the next decade across the semiconductor value chain, including R&D, manufacturing, and packaging technologies. Further in this investment, the company plans to invest approximately EUR 17 billion (USD 18.45 billion) in establishing a semiconductor fab mega-site in Germany, as well as the development of a new R&D and design facility in France, and to invest in R&D, manufacturing, and foundry services in Italy, Poland, Ireland, and Spain.

Semiconductor Device Industry Overview

The semiconductor device market for processing applications is experiencing moderate fragmentation, with several competitors navigating fluctuations amidst growing consolidation, technological advancements, and evolving geopolitical scenarios. This heightened competition is set to intensify in a market where establishing a sustainable competitive advantage through innovation is of paramount importance. Given the expectations of quality from end-users in the semiconductor manufacturing sector, brand identity plays a pivotal role in this landscape.

The market penetration levels are notably high, primarily due to the presence of significant market incumbents such as Intel Corporation, Nvidia Corporation, Kyocera Corporation, Qualcomm Technologies Inc., and other industry leaders.

In April 2022, SK Hynix Inc. introduced its latest solid-state drive (SSD), known as the P5530, designed for data centers in collaboration with its San-Jose-based subsidiary, Solidigm. SSDs leverage flash memory to store data, and this innovative device combines SK Hynix's 128-layer 4D NAND, a core product, with Solidigm's SSD controller.

In March 2022, Samsung Electronics and Western Digital reached an agreement to collaborate on standardizing and promoting next-generation data placement, processing, and fabrics (D2PF) storage technologies. Their joint efforts aim to streamline industry practices, allowing for a broader array of applications that ultimately deliver greater value to customers.

In January 2022, Kioxia Corporation announced the launch of Universal Flash Storage (UFS) Ver. 3.1 embedded flash memory devices. These devices harness the company's pioneering 4-bit per cell quad-level-cell (QLC) technology, which has the capability to achieve the highest densities available in a single package. This technology is particularly suited for high-density applications like high-end smartphones

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Trends

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Industry Attractiveness Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Impact of the Macroeconomics Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Technologies Like IoT And AI

- 5.1.2 Increased Deployment of 5G And Rising Demand For Data Centers

- 5.2 Market Challenges

- 5.2.1 Supply Chain Disruptions Resulting In Semiconductor Chip Shortage

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 Discrete Semiconductors

- 6.1.2 Optoelectronics

- 6.1.3 Sensors

- 6.1.4 Integrated Circuits

- 6.1.4.1 Analog

- 6.1.4.2 Logic

- 6.1.4.3 Memory

- 6.1.4.4 Micro

- 6.1.4.4.1 Microprocessors (MPU)

- 6.1.4.4.2 Microcontrollers (MCU)

- 6.1.4.4.3 Digital Signal Processors

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intel Corporation

- 7.1.2 Nvidia Corporation

- 7.1.3 Qualcomm Incorporated

- 7.1.4 NXP Semiconductors NV

- 7.1.5 SK Hynix Inc.

- 7.1.6 Kyocera Corporation

- 7.1.7 Samsung Electronics Co., Ltd.

- 7.1.8 Advanced Micro Devices, Inc

- 7.1.9 ST microelectronics Nv

- 7.1.10 Micron Technology Inc.

- 7.1.11 Toshiba Electronic Devices And Storage Corporation

- 7.1.12 Infineon Technologies AG