|

市場調査レポート

商品コード

1408743

通信業界における半導体デバイス:市場シェア分析、産業動向と統計、2024~2029年の成長予測Semiconductor Device In Communication Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 通信業界における半導体デバイス:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

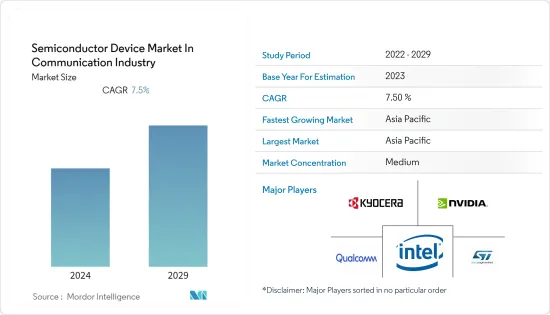

通信業界における半導体デバイス市場は、現在のところ2,079億米ドルと評価されており、予測期間中にCAGR 7.5%を記録し、今後5年間で2,995億米ドルになると予想されています。

主なハイライト

- 有線または無線半導体は、ネットワーク接続、基地局、ルーターから電話、ノートパソコン、その他の接続機器に至るまで、通信技術の重要な部分を形成しています。

- 近年、ワイヤレス技術は通信業界に革命をもたらし、世界中のモバイル加入者数は急速に伸びています。最も身近なワイヤレス・アプリケーションは携帯電話であり、スマートフォンは全世界のモバイル契約数の大きなシェアを占めています。現在の携帯電話は、ほとんどが4G無線通信システムを利用しています。4Gのデータ通信規格は非常に高速であり、現在開発中の5Gシステムはさらに高速になります。

- 地域政府は5Gの世界展開を支援するイニシアチブを取っており、通信業界における半導体デバイス市場の成長を牽引しています。例えば、欧州委員会は5G技術開発のための官民パートナーシップを設立しました。その結果、欧州委員会はHorizon 2020プログラムを通じて欧州全域での5G展開を支援するため、7億英ポンド(~8億8,950万米ドル)以上の公的資金を投入すると発表しました。

- さらに、デジタル技術の普及とインターネット利用者の増加を支えるため、ITインフラへの投資も拡大しています。例えば、インドでは2025年までに約45のデータセンターが新設され、2020年以降、約100億米ドルの投資が見込まれています。このような動向は、予測期間中の市場成長にとって好ましい見通しとなります。

- しかし、半導体業界では小型化が最重要動向の1つであるため、チップサイズの縮小は設計や製造の複雑さを著しく増大させるため、小型チップへの需要の増加は市場成長の妨げになると予想されます。

- さらに、パンデミックは5Gの展開、デジタルトランスフォーメーション、リモートワーク文化による高速ネットワーク接続の需要を増加させました。通信は医療、政府、民間などさまざまな産業の効率的な運営に欠かせないため、通信業界は大きな影響を受けています。

半導体デバイス市場の動向

5G技術の採用拡大

- 5Gの導入が進むことで、スマートフォンのような5G対応デバイスの需要が大きく伸びており、これが通信業界における半導体デバイス市場の需要を牽引しています。

- エリクソンは、2027年末までに世界中で44億の5G加入があり、全モバイル加入の48%を占めると予測しています。同社によると、5Gの契約数は2009年に開始された4Gよりも早く、4Gよりも2年早く10億契約に達しました。

- 主な要因としては、複数のベンダーから端末がタイムリーに提供され、価格が4Gよりも早く下落したこと、中国が大規模かつ早期に5Gを導入したことなどが挙げられます。エリクソンによると、5Gは2027年に契約数で支配的なモバイルアクセス技術になります。

- 改善された5Gネットワークと無制限のデータプランは、世界中でより多くの5G加入者を惹きつけると思われます。動画ベースのアプリ、仮想現実/拡張現実、ゲームは膨大なデータトラフィックを生み出します。GSMAによると、北米の5G加入率は90%を超え、全地域の中で最も高くなります。

- さらに、5Gネットワークの展開はデータセンターの需要を高めています。5Gネットワークは、エンドユーザーに高速で低遅延の接続を提供するため、大量のデータ処理とストレージ機能を必要とするからです。

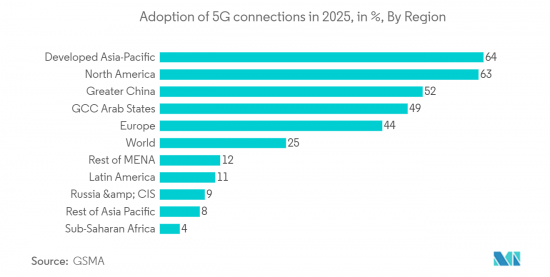

- さらに、2023年2月、GSMAは、5G接続は今後2年間で倍増すると予測していると報告しました。さらにGSMAは、最近5Gネットワークを開始したブラジルやインドなど、APACやLATAMの主要市場から成長がもたらされるとも報告しています。特にインドは重要で、2023年にJioとAirtelがサービスを拡大することが、同地域での継続的な普及の鍵になると予想されます。さらに、GSMAによれば、5Gは2025年末までにインドで1億4,500万台を占めると予想されています。

アジア太平洋が大きな市場シェアを占める

- スマートフォン、タブレット端末、クラウドベースの各種サービスのイントロダクションなど、さまざまな技術の出現により、より高速で広範な個人向けモバイル通信システムへの需要が着実に高まっています。その結果、携帯端末と主要な有線ネットワークとの接続ポイントを構築する無線基地局(BTS)のイントロダクションがますます多様化しています。

- IT部門の急成長と工業化も、アジア太平洋地域の通信産業における半導体デバイス市場の需要を牽引しています。これらの分野は外国からの投資を大いに促進し、この地域が先進国や新技術に触れる機会を増やすことになります。これらの分野の成長には高速で効率的な通信ネットワークの利用が不可欠であるため、民間部門と公的部門はこの地域の通信産業の発展に継続的に多額の投資を行っています。

- 日本の通信業界は、売上高では世界最大級です。市場全体が経済と人口動態の成長鈍化に後押しされているにもかかわらず、過去20年間、タワーやITインフラに多額の投資を行ってきた大手固定・モバイルネットワーク事業者はほとんどないです。インドでは5Gの普及も進んでおり、日本は2030年末までに5Gをほぼ完全にカバーすることを目指しています。

- さらに、インドの通信業界は、加入者基盤の拡大と、業界に対する政府の自由主義的・改革主義的なアプローチに牽引され、急成長を遂げています。例えば、IBEFによると、インドは世界第2位の通信市場のひとつであり、2022年4月までの加入者数は11億6,000万人に達します。さらに、2022年4月から6月にかけて、インドのインターネット加入者総数は8億3,686万人に達しました。さらに、2022年6月には、電話加入者総数の95.4%をワイヤレス分野が占めています。

- さらに、インド政府はデジタル化された堅実な経済諸国の開拓に大きく力を入れ始めており、デジタル技術の採用を促進するためにいくつかのイニシアチブをとっています。このことが、この地域の通信産業における半導体デバイス市場の成長を後押ししています。

- データセンター数の増加も、通信業界における半導体デバイス市場で事業を展開する企業に大きな機会を提供する可能性があります。例えば、2023年3月、OVHクラウドはアジア太平洋拡大計画の一環として、インドに初のデータセンターを開設すると発表しました。同社はまた、来年までにオーストラリアとシンガポールにさらに2つのデータセンターを展開する予定です。同様に、2022年6月、ST Telemedia Global Data Centers(STT GDC)は、韓国に新たなデータセンターサイトを建設する計画を発表しました。

半導体デバイス産業の概要

通信業界における半導体デバイス市場は、統合の進展、急速な技術進歩、地政学的ダイナミクスの変化などの要因により変動しています。持続可能な競争優位性がイノベーションによってもたらされる市場では、競争が激化しています。このような状況において、半導体製造に関するエンドユーザーの高品質な期待を考えると、ブランド・アイデンティティの重要性に取り組まなければならないです。

インテル・コーポレーション、エヌビディア・コーポレーション、京セラ・コーポレーション、クアルコム・テクノロジーズ・インク、STマイクロエレクトロニクスNVなど、複数の大手企業がこの市場を独占しており、高い市場浸透率につながっています。

2023年4月、京セラ株式会社は画期的な開発を発表しました。EIA 0201サイズの新型コンデンサ(MLCC)であり、10マイクロファラッドという業界最高の静電容量を誇る。京セラのKGM03シリーズは、ウェアラブル機器やスマートフォンなどに幅広く使用されています。この小型MLCCの大容量化により、設計者はより少ない部品と最小限のスペースでシステム要件を満たすことができます。

2022年6月、テキサス・インスツルメンツは、高品質のBluetooth Low Energy(LE)を他社製品に比べわずかなコストで提供する新しいワイヤレス・マイクロコントローラ(MCU)を発表し、コネクティビティ・ポートフォリオを拡充しました。SimpleLink Bluetooth LE CC2340シリーズは、同社の無線通信における豊富な経験を活用し、クラス最高の待機電流と無線周波数(RF)性能を実現します。

アナログ・デバイセズ社は2022年3月、必要な周波数帯域をカバーするように設計されたミリ波(mmW)5Gフロントエンド・チップセットを発表しました。この技術革新により、設計者は設計を簡素化し、より小型で汎用性の高い5G無線をより早く市場に投入することができます。このチップセットは4つの高集積ICで構成され、24~47GHzの5G無線に必要な部品点数を大幅に削減する包括的なソリューションを提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- マクロ動向が業界に与える影響

第5章 市場力学

- 市場促進要因

- 5G技術の採用拡大

- 市場の課題

- 半導体チップ不足

第6章 市場セグメンテーション

- デバイスタイプ別

- ディスクリート半導体

- オプトエレクトロニクス

- センサー

- 集積回路

- アナログ

- ロジック

- メモリー

- マイクロ

- マイクロプロセッサ(MPU)

- マイクロコントローラー(MCU)

- デジタル・シグナル・プロセッサー(DSP)

- 地域別

- 米国

- 欧州

- 日本

- 中国

- 韓国

- 台湾

- 世界のその他の地域

第7章 競合情勢

- 企業プロファイル

- Intel Corporation

- Nvidia Corporation

- Kyocera Corporation

- Qualcomm Incorporated

- STMicroelectronics

- Micron Technology Inc.

- Xilinx Inc.

- NXP Semiconductors NV

- Toshiba Corporation

- Texas Instruments Inc.

- Taiwan Semiconductor Manufacturing Company(TSMC)Limited

- SK Hynix Inc.

- Samsung electronics co. ltd

- Fujitsu Semiconductor Ltd

- Rohm Co. Ltd

- Infineon Technologies AG

- Renesas Electronics Corporation

- Advanced Semiconductor Engineering Inc.

- Broadcom Inc.

- ON Semiconductor Corporation

第8章 投資分析

第9章 市場の将来

The semiconductor device market in the communication industry is valued at USD 207.9 billion in the current year and is expected to register a CAGR of 7.5% during the forecast period to become USD 299.5 billion by the next five years.

Key Highlights

- Wired or wireless semiconductors form an important part of communications technology, from network connectivity, base stations, and routers to phones, laptops, and other connected devices.

- In recent years, wireless technology has revolutionized the communication industry, with mobile subscriptions across the world growing at a rapid rate. The most familiar wireless application is the mobile phone, where smartphones account for a major share of all mobile subscriptions globally. Today's cell phones mostly use 4G wireless communications systems. The data transmission standards for 4G are extremely fast, and 5G systems currently in development will be even faster.

- The regional governments are taking initiatives to support the global rollout of 5G and are driving the growth of the semiconductor device market in the communication industry. For instance, the European Commission has established a public-private partnership to develop 5G technology. As a result, the European Commission has announced over GBP 700 million (~USD 889.5 million) in public funding to support the rollout of 5G across Europe through its Horizon 2020 program.

- Furthermore, investments in supporting IT infrastructure have also been growing to support the growing penetration of digital technologies and a growing number of internet users. For instance, by 2025, about 45 new data centers will come up in India, attracting investment of nearly USD 10 billion since 2020. Such trends generate a favorable outlook for the studied market's growth during the projected timeline.

- However, as miniaturization is one of the high-priority trends in the semiconductor industry, the increasing demand for smaller chips is expected to hinder the market's growth, as shrinking chip size significantly increases design and manufacturing complexity.

- Moreover, the pandemic increased the 5G deployment, digital transformation, and demand for high-speed network connectivity due to the remote work culture. The communication industry has been greatly impacted because communications are crucial to the efficient running of various industries, including the medical, governmental, and private sectors.

Semiconductor Device Market Trends

Growing Adoption of 5G Technology

- The increasing implementation of 5G has resulted in a significant demand for 5G-enabled devices like smartphones, which, in turn, drives the demand for the semiconductor device market in the communication industry.

- Ericsson forecasts that there will be 4.4 billion 5G subscriptions across the globe by the end of 2027, accounting for 48% of all mobile subscriptions. As per the company, 5G subscription uptake is faster than that of 4G following its launch in 2009, reaching 1 billion subscriptions two years earlier than 4G did.

- Key factors include the timely availability of devices from several vendors, with prices falling faster than 4G, and China's large, early 5G deployments. According to Ericsson, 5G will become the dominant mobile access technology by subscriptions in 2027.

- The improved 5G network and unlimited data plans will attract more 5G subscribers across the globe. Video-based apps, virtual/augmented reality, and gaming generate huge data traffic. According to GSMA, 5G subscriptions in North America will be more than 90%, the highest among all regions.

- Moreover, the deployment of 5G networks is increasing the demand for data centers. This is because 5G networks require a significant amount of data processing and storage capabilities to provide high-speed, low-latency connections to end users.

- Furthermore, in February 2023, GSMA reported that 5G connections are anticipated to double over the upcoming two years. In addition, GSMA also reported that the growth would come from key markets within APAC and LATAM, like Brazil and India, which have recently launched 5G networks. India will be particularly significant, with the expansion of services from Jio and Airtel in 2023 expected to be key to continued adoption in the region. Moreover, as per GSMA, 5G is anticipated to account for 145 million in India by the end of 2025.

Asia-Pacific to Hold Significant Market Share

- The emergence of different technologies, including the introduction of smartphones, tablets, and a variety of cloud-based services, has driven a steady increase in demand for faster and more pervasive personal mobile communication systems. This, in turn, has resulted in the introduction of a growing variety of wireless base stations (BTS), creating the connection points between the mobile terminals and the main wired network.

- The rapid growth of the IT sector and industrialization are also driving the demand for the semiconductor device market in the communications industry in the Asia-Pacific region. These sectors will greatly facilitate foreign investment, increasing the region's exposure to developed countries and new technologies. The private and public sectors are continuously investing heavily in developing the region's telecommunications industry, as the availability of high-speed and efficient telecommunications networks is essential for the growth of these sectors.

- The Japanese telecommunications industry is among the largest in the world in terms of revenue. Few major fixed and mobile network operators have invested heavily in towers and IT infrastructure over the past two decades despite the overall market being fueled by slow economic and demographic growth. 5G adoption is also gaining traction in the country, and Japan aims to reach almost full 5G coverage by the end of 2030.

- Moreover, the Indian communication industry has been witnessing sharp growth driven by a growing subscriber base and the liberal and reformist government approach towards the industry. For instance, according to IBEF, India is among the world's second-largest telecommunications markets, with a subscriber base of 1.16 billion until April 2022. Furthermore, in April-June 2022, the total number of internet subscribers in India reached 836.86 million. Additionally, the wireless segment accounted for 95.4% of the total telephone subscriptions In June 2022.

- Additionally, the Indian government has started to focus significantly on developing a solid digitized economy and is taking several initiatives to promote the adoption of digital technologies; this, in turn, is aiding the growth of the semiconductor device market in the communication industry in the region.

- Increasing the number of data centers may also offer massive opportunities for companies operating in the semiconductor device market in the communication industry. For instance, in March 2023, OVH Cloud announced the launch of its first data center in India as a part of its Asia Pacific expansion plan. The company will also deploy two additional data centers in Australia and Singapore by next year. Similarly, in June 2022, ST Telemedia Global Data Centers (STT GDC) announced its plans for a new data center site in South Korea.

Semiconductor Device Industry Overview

The semiconductor device market in the Communication Industry is experiencing fluctuations due to factors such as increased consolidation, rapid technological advancements, and shifting geopolitical dynamics. In a market where sustainable competitive advantages are driven by innovation, competition is on the rise. In this context, the importance of brand identity must be addressed, given the high-quality expectations of end-users when it comes to semiconductor manufacturing.

Several major players dominate this market, including Intel Corporation, Nvidia Corporation, Kyocera Corporation, Qualcomm Technologies Inc., and STMicroelectronics NV, leading to high levels of market penetration.

In April 2023, Kyocera Corporation announced a groundbreaking development - a new capacitor (MLCC) in the EIA 0201 size category, boasting the industry's highest capacitance at 10 microfarads. The KGM03 series from Kyocera is widely used in wearable devices and smartphones. The increased capacity of these compact MLCCs empowers designers to meet system requirements with fewer components and minimal space utilization.

In June 2022, Texas Instruments extended its connectivity portfolio by introducing new wireless microcontrollers (MCUs) that offer high-quality Bluetooth Low Energy (LE) at a fraction of the cost of competitors. The SimpleLink Bluetooth LE CC2340 series leverages the company's extensive experience in wireless communication and delivers best-in-class standby current and radio-frequency (RF) performance.

March 2022 saw Analog Devices Inc. introduce a millimeter-wave (mmW) 5G front-end chipset designed to cover the necessary frequency bands. This innovation enables designers to simplify their designs and bring smaller and more versatile 5G radios to the market faster. The chipset consists of four highly integrated ICs, offering a comprehensive solution that significantly reduces the number of components required for 24 to 47GHz 5G radios.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Macro Trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of 5G Technology

- 5.2 Market Challenges

- 5.2.1 Semiconductor Chip Shortage

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 Discrete Semiconductors

- 6.1.2 Optoelectronics

- 6.1.3 Sensors

- 6.1.4 Integrated Circuits

- 6.1.4.1 Analog

- 6.1.4.2 Logic

- 6.1.4.3 Memory

- 6.1.4.4 Micro

- 6.1.4.4.1 Microprocessors (MPU)

- 6.1.4.4.2 Microcontrollers (MCU)

- 6.1.4.4.3 Digital Signal Processor

- 6.2 By Geography

- 6.2.1 United States

- 6.2.2 Europe

- 6.2.3 Japan

- 6.2.4 China

- 6.2.5 Korea

- 6.2.6 Taiwan

- 6.2.7 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intel Corporation

- 7.1.2 Nvidia Corporation

- 7.1.3 Kyocera Corporation

- 7.1.4 Qualcomm Incorporated

- 7.1.5 STMicroelectronics

- 7.1.6 Micron Technology Inc.

- 7.1.7 Xilinx Inc.

- 7.1.8 NXP Semiconductors NV

- 7.1.9 Toshiba Corporation

- 7.1.10 Texas Instruments Inc.

- 7.1.11 Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- 7.1.12 SK Hynix Inc.

- 7.1.13 Samsung electronics co. ltd

- 7.1.14 Fujitsu Semiconductor Ltd

- 7.1.15 Rohm Co. Ltd

- 7.1.16 Infineon Technologies AG

- 7.1.17 Renesas Electronics Corporation

- 7.1.18 Advanced Semiconductor Engineering Inc.

- 7.1.19 Broadcom Inc.

- 7.1.20 ON Semiconductor Corporation