|

市場調査レポート

商品コード

1408491

日本のデータセンター冷却:市場シェア分析、産業動向と統計、2024年~2030年の成長予測Japan Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のデータセンター冷却:市場シェア分析、産業動向と統計、2024年~2030年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

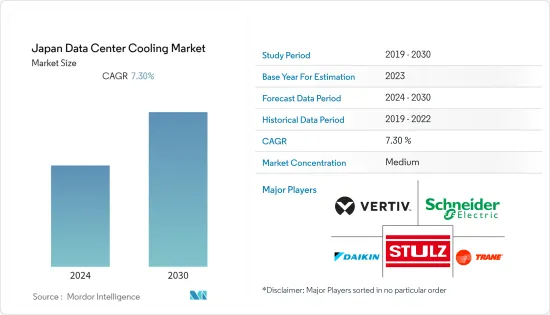

日本のデータセンター冷却市場は、前年度に6億7,020万米ドルの市場規模に達し、予測期間中のCAGRは7.3%になると予測されています。

主要ハイライト

- 中小企業におけるクラウドコンピューティング需要の増加、データセキュリティに関する政府規制、国内企業による投資拡大などが、同国・地域におけるデータセンター需要を促進する主要要因の1つです。

- 日本のデータセンター市場の今後のIT負荷容量は、2029年までに2,100MWに達すると予想されます。日本の床面積は2029年までに1万平方フィートに増加すると予想されます。

- 日本の総設置ラック数は2029年までに512Kユニットに達する見込みです。2029年には、大阪と東京に最大数のラックが設置される見込みです。年間を通じて、気温は通常2℃から30℃の間で変動し、-1℃を下回ったり0.5℃を上回ったりすることはほとんどないです。

- 日本を結ぶ海底ケーブルシステムは32近くあり、その多くが建設中です。

日本のデータセンター冷却市場動向

液体ベースの冷却が急成長中

- 技術の進歩により、液冷はメンテナンスが容易で、拡大性が高く、価格も手頃になり、データセンターの液冷消費量は熱帯気候では15%以上、環境に優しい地域では80%削減されています。液体冷却に使用されるエネルギーは、ビルや水の暖房に再利用でき、先進の人工冷媒はエアコンの二酸化炭素排出量を効果的に削減できます。

- 日本の企業の中には、1年のうち少なくとも数ヶ月は雪を冷媒として使用しているところもあります。日本の北海岸に位置する新潟県に本社を置く株式会社データドックは、長岡市にあるサーバーを融雪剤と冷たい外気で冷却しています。

- 日本のデータセンタープロバイダーであるKDDIとNTT DATAは、サーバー・ハードウェアの冷却におけるエネルギー浪費を大幅に削減するため、液浸技術を研究しています。KDDIの実地試験では、従来の空冷システムに比べ、温度制御時の消費電力を94%削減するという驚異的な結果を得た。KDDIによると、IT機器は最も電力を消費すると思われがちだが、データセンターの総消費電力の約半分は冷却に使われているといわれています。

- 直接液冷(DLC)ソリューションは、1.02~1.03の部分的な電力使用効率(PUE)値を達成することができ、最先端の空冷システムの効率さえも1桁台前半の差で上回る。しかし、PUEはDLCによるエネルギー効率向上の大部分を占めていないことに注意することが重要です。従来のサーバーセットアップでは、ファンがサーバーラック内の電力消費を担っており、この電力使用はPUE計算のIT電力セクションに考慮されています。これらのファンは、データセンター全体のエネルギー消費の不可欠な一部であると考えられています。

- 日本はeコマースの3大市場のひとつです。日本は、電子商取引の3大市場のひとつであり、英国を上回っているが、米国には遅れをとっています。日本のeコマース市場は、主にハイテク・ネットワーク・インフラに支えられたインターネットの高い普及率によって牽引されています。M-コマースは大幅な拡大を経験しています。モバイル販売は2022年までB2C eコマース市場全体を上回ると予測されています。日本におけるモバイルコマースの市場規模は、2021年時点で約4兆9,000億円です。過去10年間で2倍以上になっています。このような事例は、冷却サービスの向上に対する需要の高まりとともに、コロケーションの主要な需要に対応しています。

IT・通信が最大のセグメント

- 日本には、Sony、Panasonic、Fujitsu、NEC、Toshibaといった大手ICT企業があり、ICTの主要拠点としての日本の拡大に重要な役割を果たし続けています。加えて、国内における多数の近代化・拡大プロジェクトの整然とした開拓と、高品質かつ先進的なインフラの維持に向けた政府支出の増加も、市場の成長を後押ししています。

- 市民参加、自己評価、オンライン政府サービスへのフィードバックを含む地方電子政府プロジェクトの開拓に重点を置くE-Japan戦略の急成長は、日本のICT市場の今後の成長を牽引すると思われます。

- 日本政府は、民間部門のデジタルトランスフォーメーションを加速させ、新興中小企業を支援するための取り組みを進めています。2021年、経済産業省と総務省が主導する日本政府は、特に中小企業を対象とした、組織内のデジタルトランスフォーメーションを推進するためのガイドラインを発表しました。同様に、AI、サイバーセキュリティ、セキュアなクラウドサービスの導入に関するガイドラインも同年発表されました。

- 2022年11月、デジタル・インフラ・プロバイダーのEquinixは、新たなデータセンターに1億1,500万米ドルを投資し、日本におけるデジタル・インフラ拠点を拡大すると発表しました。この新しいデータセンターは、世界ネットワークやクラウドサービスプロバイダーとの企業接続を強化し、日本のデジタル経済の拡大と強化を可能にします。

- 日本政府は2022年6月、2030年末までに人口の99%に無線ネットワークを配備すると発表しました。デジタル化を推進するための基本方針と海底ケーブルは、2025年末までに日本全土で完成する予定です。

日本のデータセンター冷却産業概要

日本のデータセンター冷却市場は適度に競争しており、最近競合をつけてきました。現在、Stulz GmbH、Schneider Electric SE、Vertiv Group Corp.、Daikin Industries Ltd.、Trane Inc.など、少数の大手企業が市場で支配的な地位を占めています。

2023年3月、ハンブルクを拠点とする基幹空調会社STULZは、業界をリードするサイバーエアー3PRO DXシリーズに関して重要な発表を行った。同シリーズの一部のユニットが、地球温暖化係数(GWP)の低い冷媒R513Aに対応したことを明らかにしたのです。この画期的な開発は、データセンター向けに最も持続可能な空調システムを提供するという同社の継続的なコミットメントを強調するものです。さらにSTULZは、R513A冷媒の使用を取り入れた製品ポートフォリオを拡大しています。

2022年2月、GigabyteはAMD EPYCとNvidia A100技術に基づく先駆的なハイパフォーマンス・コンピューティング・サーバーを発表しました。これらのサーバーはCoolITの直接液体冷却システムを搭載しています。この新しいマシンは、最大128コアを誇るAMD EPYC 7003シリーズ「Milan」プロセッサー1基または2基と、Nvidia A100 80GB SXM4モジュール4基または8基を搭載しています。独自の直接液体冷却システムで知られるCoolITは、CPUとGPUを別々に冷却し、パフォーマンスを最適化します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 地域におけるITインフラの発展

- エコデータセンターの出現

- 市場抑制要因

- コスト、適応要件、停電

- バリューチェーン/サプライチェーン分析

- 業界の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- 冷却技術

- 空冷

- 液体式冷却

- 蒸発式冷却

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- メディア&エンターテイメント

- その他のエンドユーザー

第6章 競合情勢

- 企業プロファイル

- Vertiv Co.

- Schneider Electric SE

- STULZ GMBH

- Daikin Industries Ltd

- Trane Inc.

- Johnson Controls International PLC

- Mitsubishi Electric Corporation

- RITTAL Electro-Mechanical Technology Co. Ltd(RITTAL GMBH & CO. KG)

- Nortek Air Solutions

- Munters Air Treatment Equipment(Beijing)Co. Ltd

- CoolIT Systems Inc.

- Asetek AS

- Wakefield-Vette Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The Japan data center rack market reached a value of USD 670.2 million in the previous year, and it is further projected to register a CAGR of 7.3% during the forecast period.

Key Highlights

- The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country/region.

- The upcoming IT load capacity of the Japan data center market is expected to reach 2100 MW by 2029. The country's construction of raised floor area is expected to increase to 10K sq. ft by 2029.

- The country's total number of racks to be installed is expected to reach 512K units by 2029. Osaka and Tokyo are expected to house the maximum number of racks by 2029. Throughout the year, temperatures typically fluctuate between 2°C and 30°C, rarely dropping below -1°C or above 0.5°C.

- There are close to 32 submarine cable systems connecting Japan, and many are under construction.

Japan Data Center Cooling Market Trends

Liquid-based Cooling is The Fastest Growing Segment

- Technological advances have made liquid cooling easier to maintain, more scalable, and more affordable, reducing data center liquid consumption by more than 15% in tropical climates and by 80% in greener areas. The energy used for liquid cooling can be recycled to heat buildings and water, and advanced artificial refrigerants can effectively reduce the carbon footprint of air conditioners.

- Some Japanese companies already use snow as a coolant for at least several months of the year. Based in Niigata prefecture on Japan's north coast, DataDock Inc. cools its servers in Nagaoka City with snowmelt and cold outside air.

- Japanese data center providers KDDI and NTT DATA are researching immersion technology to significantly reduce energy waste in cooling server hardware. In KDDI's field test, we achieved an astounding result of reducing power consumption during temperature control by 94% compared to conventional air cooling systems. KDDI said IT equipment is often thought of as the biggest consumer of power, but about half of the total power consumption in data centers is used for cooling.

- Direct liquid cooling (DLC) solutions can achieve partial power usage effectiveness (PUE) values ranging from 1.02 to 1.03, surpassing the efficiency of even the most advanced air cooling systems by a low single-digit margin. It is important to note, however, that PUE does not account for a significant portion of the energy efficiency improvements attributed to DLC. In traditional server setups, fans are responsible for power consumption within the server rack, and this power usage is factored into the IT power section of the PUE calculation. These fans are considered an integral part of the data center's overall energy consumption.

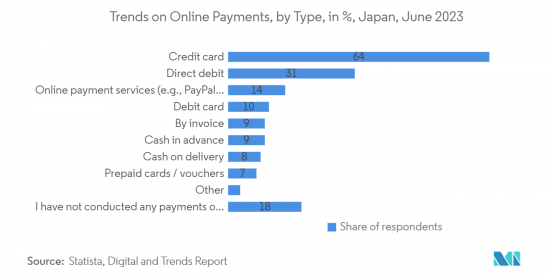

- Japan is one of the three largest markets for e-commerce. It is placed ahead of the United Kingdom but behind the United States. The e-commerce market in Japan is primarily driven by high internet penetration, secured by the Hi-tech network infrastructure. M-commerce is experiencing significant expansions. Mobile sales were projected to outpace the overall B2C e-commerce market until 2022. The mobile commerce market size in Japan stood at around JPY 4.9 trillion as of 2021. It has more than doubled over the last decade. Such instances cater to the major demand for colocation with the increasing demand for improved cooling services.

IT & Telecommunication is the Largest Segment

- Japan is home to major ICT organizations such as Sony, Panasonic, Fujitsu, NEC, and Toshiba, which continue to play a key role in the country's expansion as a major center for ICT. In addition, the orderly development of numerous modernization and expansion projects in the country, along with increasing government spending on maintaining high-quality and advanced infrastructure, are also driving the growth of the market.

- The rapid growth of the E-Japan strategy, which focuses on the development of local e-government projects involving citizen participation, self-evaluation, and feedback on online government services, will drive future growth of the Japanese ICT market.

- The Japanese government is making efforts to accelerate the digital transformation of the private sector and support emerging SMEs. In 2021, the Japanese government, led by the Ministry of Economy, Trade and Industry and the Ministry of Internal Affairs and Communications, published guidelines for promoting digital transformation within organizations, especially targeting small and medium-sized enterprises. Similarly, guidelines on implementing AI, cybersecurity, and secure cloud services were also published in the same year.

- In November 2022, digital infrastructure provider Equinix announced it would expand its digital infrastructure footprint in Japan with a USD 115 million investment in new data centers. The new data center will enhance corporate connectivity with global networks and cloud service providers, enabling them to scale and strengthen Japan's growing digital economy.

- In June 2022, the Japanese government announced that it would deploy wireless networks to 99% of the population by the end of 2030. Its basic policy to promote digitalization and submarine cables is scheduled to be completed throughout Japan by the end of 2025.

Japan Data Center Cooling Industry Overview

The Japan data center cooling market is moderately competitive and has recently gained a competitive edge. Currently, a few major players, including Stulz GmbH, Schneider Electric SE, Vertiv Group Corp., Daikin Industries Ltd, and Trane Inc., hold a dominant position in the market.

In March 2023, STULZ, a Hamburg-based mission-critical air conditioning company, made a significant announcement regarding its industry-leading CyberAir 3PRO DX series. They revealed that some units within this series are now compatible with the low global warming potential (GWP) refrigerant R513A. This groundbreaking development underscores the company's ongoing commitment to delivering the most sustainable air conditioning systems for data centers. Additionally, STULZ has expanded its product portfolio to incorporate the use of R513A refrigerant.

In February 2022, Gigabyte introduced pioneering high-performance computing servers based on AMD EPYC and Nvidia A100 technology. These servers are equipped with CoolIT's direct liquid cooling system. The new machines feature 1 or 2 AMD EPYC 7003 series 'Milan' processors, boasting up to 128 cores, as well as 4 or 8 Nvidia A100 80GB SXM4 modules. CoolIT, known for its unique direct liquid cooling system, ensures separate cooling for the CPU and GPU, optimizing performance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Development of IT Infrastructure in the Region

- 4.2.2 Emergence of Green Data Centers

- 4.3 Market Restraints

- 4.3.1 Costs, Adaptability Requirements, and Power Outages

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Cooling Technology

- 5.1.1 Air-based Cooling

- 5.1.2 Liquid-based Cooling

- 5.1.3 Evaporative Cooling

- 5.2 End-User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End-Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Vertiv Co.

- 6.1.2 Schneider Electric SE

- 6.1.3 STULZ GMBH

- 6.1.4 Daikin Industries Ltd

- 6.1.5 Trane Inc.

- 6.1.6 Johnson Controls International PLC

- 6.1.7 Mitsubishi Electric Corporation

- 6.1.8 RITTAL Electro-Mechanical Technology Co. Ltd (RITTAL GMBH & CO. KG)

- 6.1.9 Nortek Air Solutions

- 6.1.10 Munters Air Treatment Equipment (Beijing) Co. Ltd

- 6.1.11 CoolIT Systems Inc.

- 6.1.12 Asetek AS

- 6.1.13 Wakefield-Vette Inc.