音センサー:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Sound Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

- 発行日

- ページ情報

- 英文 179 Pages

- 納期

- 2~3営業日

- 商品コード

- 2066469

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

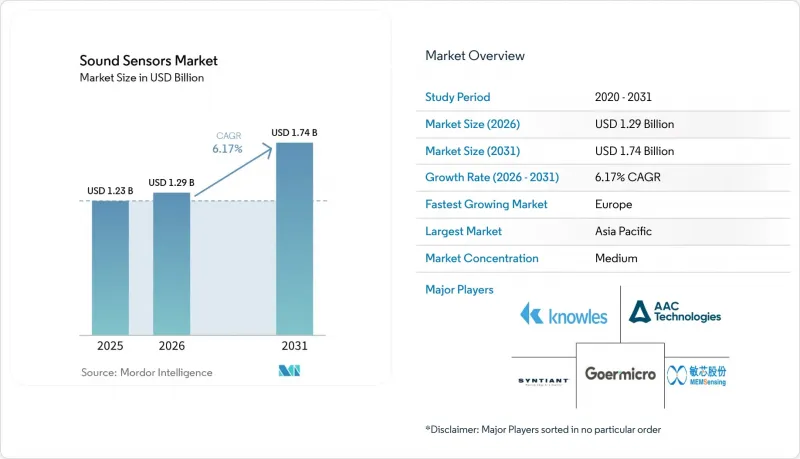

Mordor Intelligenceによると、音センサー市場の規模は2025年に12億3,000万米ドルと評価され、2026年の12億9,000万米ドルから2031年までに17億4,000万米ドルに達すると予測されており、予測期間(2026年~2031年)におけるCAGRは6.17%となる見込みです。

本レポートは、センサータイプ(マイクロエレクトロメカニカル(MEMS)システムマイクなど)、周波数(低周波音、可聴音など)、用途(音声認識および音声処理など)、エンドユーザー産業(家庭用電子機器、スマートフォンおよびタブレット、完全ワイヤレスステレオイヤホンおよびヘッドセット、スマートスピーカーなど)、および地域別に分類されています。市場規模および予測は、金額(米ドル)ベースで示されています。

世界の音センサー市場の動向と洞察

「ボイスファースト」型コンシューマーデバイスの拡大

音センサー市場において、短期的には、スマートフォン、TWSイヤホン、スマートスピーカー、AI搭載ウェアラブルデバイスに搭載された常時稼働型の音声インターフェースが、最も強力な牽引力となっています。デバイスのアップグレードはもはやウェイクワード検出のみに焦点を当てたものではなく、ローカル推論ワークロードにおいて、音響フロントエンドに対してより低い自己ノイズとより広い周波数応答が求められるようになったためです。Syntiant社は2025年12月、eWLBおよび超薄型パッケージを採用したNDP115ポートフォリオを拡充し、コンパクトなデバイス向けに推論用シリコンとフロントエンドの音響技術がいかに緊密に共同設計されているかを実証しました。この設計動向により、OEM各社がベンダー数の削減と、より統合されたオーディオ・AIスタックを求めるようになるにつれ、音センサー市場における認定プロセスの絞り込みが進んでいます。また、これにより、依然として主にパッケージングや組立の規模に依存している企業に比べ、MEMSプロセス制御や信号処理IPを有するサプライヤーの優位性が高まっています。

産業用予知保全の導入

音センサー市場は、回転機器や往復運動機器における音響モニタリングを、定期点検から連続センシングへと移行させている産業オペレーターから、持続的な支持を得つつあります。2025年6月の調査によると、MEMS音響エミッションセンサーは、ネットワークエッジにおける遊星歯車箱において90%を超える故障分類精度を達成しており、クラウドへの依存が課題となる過酷な環境での迅速な導入を後押ししています。こうしたシステムが企業アーキテクチャに組み込まれるにつれ、価値の多くは、トランスデューサー単体ではなく、センサー、ASIC、および分析技術の組み合わせへとシフトしつつあります。これにより、音センサー市場において、共同統合された処理機能を備えていないスタンドアロンの部品ベンダーには圧力がかかっています。ノウルズ社が民生用MEMSマイクロフォン事業を売却した後の事業再編も、サプライヤーが産業用音響分野において、より安定した利益率とより長い設備サイクルを見込んでいることを示唆しています。

騒音環境における精度の低下

音センサー市場は依然として、残響の多い空間、騒音の激しい産業現場、および屋外の密集した環境において、生音響性能が急速に低下するという明確な技術的限界に直面しています。2025年5月に発表された調査によると、ディープラーニングを活用したノイズ対策型摩擦発電式音響センサーは、-10 dBという低い信号対雑音比(SNR)でも性能を維持できることが示されましたが、その利得はセンサー上に追加されたニューラル処理に依存しており、これによりシリコン面積とシステムコストが増加します。これにより、調達方針も変化しています。購入者は、マイク単体ではなく、音響ノードの総コストを評価する傾向が強まっているからです。実際の導入においては、音センサー市場における一部の音声およびモニタリング使用事例において、実際の運用条件下で必要な精度基準を満たすのに依然として苦労していることを意味します。商用化されたノイズ対策アーキテクチャは、根底にある需要のパイプラインに比べて成熟度がまだ低いため、この制約は短期的には特に顕著に現れています。

セグメント分析

2025年、MEMSマイクロフォンは音センサー市場シェアの41.35%を占め、他のすべてのセンサーカテゴリーを確実にリードし続けています。このリードは、小型パッケージ、低消費電力、安定した音響性能が標準的な要件とされるスマートフォン、TWSイヤホン、スマートスピーカーにおける度重なる設計採用を反映したものです。エレクトレット・コンデンサー型マイクロフォンは、コスト重視のインターコムや基本的な産業用音声アプリケーションにおいて依然として一定の地位を占めていますが、OEMの仕様が高度化するにつれて、そのシェアは縮小し続けています。ダイナミック型(ムービングコイル)マイクロフォンは、ライブオーディオや放送の現場で依然として定着していますが、液体結合型および空気結合型の超音波デバイスは、より限定的な検査や測定の使用事例に焦点を当て続けています。音センサー市場の中で最も高い成長を見せているのは、音響エミッションセンサーであり、2031年までCAGR7.77%を記録すると予測されています。

この成長は、施設における設備の健全性管理方法の構造的変化と密接に関連しています。運用担当者は、定期的な手動点検に頼るのではなく、継続的なIIoTデータストリームを構築するようになっているためです。そのため、音響センサー業界では、ネットワーク化された診断、長い稼働寿命、およびプラント分析システムとの統合をサポートする音響エミッションプラットフォームが、より重視されるようになっています。2025年6月に実施された遊星歯車系の故障診断に関する研究では、MEMS音響エミッションセンシングが産業環境において高精度なエッジ分類をサポートできることが示され、この方向性を裏付ける結果となりました。XARIONや類似の光学式アプローチも、従来の接触式センシングでは効果が低下しがちな高温・高圧環境において競合しており、差別化された技術に活躍の場が広がっています。市場規模の面では、AAC Technologies社によると、同社のMEMSマイクロフォンの売上高は2025年に50%以上増加し、2025会計年度の総売上高は318億2,000万人民元(44億3,000万米ドル)に達しました。これは、音センサー市場のトップ層における膨大な販売数量を裏付けるものです。

2025年には可聴帯域が売上高の69.24%を占め、音センサー市場において圧倒的なシェアを誇る周波数帯となりました。この地位は、20 Hz~20 kHzの範囲で動作するスマートフォン、イヤホン、スマートスピーカー、ウェアラブル端末の大量出荷に根ざしています。超低周波帯は、地震観測、構造物の健全性監視、軍事監視の用途において依然として重要ですが、その需要基盤は、はるかに小さく販売数量も少ない状況です。超音波帯は最も急成長している周波数セグメントであり、超音波センサー市場は2031年までCAGR6.58%で拡大すると予測されています。その需要は可聴帯よりも多様で、医療用画像診断、ソナー、EVバッテリーの試験、ロボティクス、産業レベルの計測などに及んでいます。

超音波分野の成長は、単一のエンドマーケットではなく、複数の調達サイクルによって牽引されています。サンライズ・ウィンド・プロジェクトに関する米国海洋大気庁(NOAA)の文書によると、受動型音響モニタリングが洋上開発およびコンプライアンスプログラムの一部となりつつあり、これが海底および水中音響システムに対する長期的な需要を支えています。2025年5月に『Scientific Data』誌に掲載された調査では、光ファイバーに沿った可聴スペクトル内の音声を捉えた分散型音響センシングデータセットも紹介されており、インフラセンシングが音響技術の活用範囲をいかに拡大しているかが示されています。したがって、音センサー市場では、収益の中心は依然として可聴帯域にありますが、最高周波数帯域におけるビジネスチャンスは超音波分野にあります。これは、価格のコモディティ化が進んでおらず、応用範囲が広いからです。低周波音は、規模は小さいもの安定した役割を維持しており、公共部門や防衛分野の調達が需要の下支えとなっています。

地域別分析

2025年、北米は音センサー市場シェアの29.91%を占め、地域別では最大の貢献度を示しました。米国は、ハイパースケーラーの音声プラットフォーム、自動車関連プログラム、産業用モニタリング、防衛音響分野を通じて需要を牽引しています。カナダは、2026年3月にOcean Sonics社が410万米ドル規模の「カナダ・オーシャン・スーパークラスター」プロジェクトに参加したことを受け、海洋および海底音響分野に貢献しています。メキシコは、自動車関連の音響サプライチェーンにおける沿岸組立拠点として台頭しつつあります。FCCパート15やOSHAの騒音関連要件を含む規制された調達経路が、北米市場をさらに支えています。

アジア太平洋地域は最も急成長している地域であり、音センサー市場は2031年までCAGR7.17%で拡大すると予測されています。中国は、新エネルギー車(NEV)の生産、MEMSの生産能力、および都市騒音管理の実施において主導的な役割を果たしています。上海市が策定した騒音対策計画は、環境騒音に対するガバナンスの強化を強調しています。Goertek Microelectronics社は、2025年7月の香港上場目論見書において、2024年度時点で音響センサーの世界市場シェアが43%に達したと報告しており、これは同地域における製造の集中を反映しています。日本と韓国は、精密部品や高級ウェアラブルオーディオ製品を通じて世界の標準に影響を与えている一方、インドや東南アジアは、展開および組立の拠点として拡大しています。

欧州も依然として重要な市場であり、ドイツ、英国、フランスが、産業オートメーション、医療診断、高級自動車セクターにおける需要を牽引しています。EUの環境騒音指令は、自治体や交通回廊における騒音モニタリングプログラムを支援しており、それによって安定した公共調達基盤が確保されています。洋上風力発電や受動的音響監視は、特に北海での活動において、海底モニタリングへの需要をさらに後押ししています。南米、中東・アフリカは依然として小規模な市場ですが、鉱業、石油・ガス、スマートシティのデジタル化、環境規制への対応が、これらの地域において選択的な成長を牽引しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストによるサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 音声優先型コンシューマーデバイスの普及

- 産業用予知保全の導入

- 自動車車内センシング市場の成長

- 遠隔およびウェアラブル音響診断の台頭

- スマートシティにおける騒音モニタリングの義務化

- 洋上風力および海底モニタリングの需要

- 市場抑制要因

- ノイズの多い環境における精度の低下

- レーダー、LiDAR、および光学センシングによる競合

- MEMS用特定用途向け集積回路(ASIC)の知的財産の分散化

- 特殊圧電材料の供給変動

- マクロ経済要因が市場に与える影響

- 業界バリューチェーン分析

- 規制情勢

- 技術展望

- ポーターのファイブフォース分析

第5章 市場規模と成長予測

- センサータイプ別

- マイクロエレクトロメカニカル(MEMS)システム・マイクロフォン

- エレクトレット・コンデンサー・マイクロフォン

- ダイナミック・ムービングコイル型マイクロフォン

- 超音波センサー

- 空気伝搬型超音波センサー

- 音響エミッションセンサー

- 液体結合型超音波センサー

- その他のセンサータイプ

- 周波数別

- 低周波音

- 可聴音

- 超音波

- 用途別

- 音声認識および音声処理

- ノイズキャンセリングおよびオーディオエンハンスメント

- 環境・騒音モニタリング

- セキュリティ・監視

- 医療診断およびヘルスケア

- 水中センシングおよびソナー

- 通信インフラ

- その他の用途

- エンドユーザー産業別

- 家庭用電子機器

- スマートフォンおよびタブレット

- 完全ワイヤレスステレオイヤホンおよびヘッドセット

- スマートスピーカーおよびホームハブ

- ウェアラブルおよびヒアラブル

- 産業

- 自動車・輸送産業

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他の南米諸国

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他の欧州諸国

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他のアジア太平洋諸国

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他の中東諸国

- アフリカ

- 南アフリカ

- エジプト

- その他のアフリカ諸国

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Knowles Corporation

- AAC Technologies Holdings Inc.

- Goertek Microelectronics Co., Ltd.

- Syntiant Corp.

- Sonion A/S

- Suzhou MEMSensing Microelectronics Technology Co., Ltd.

- Shandong Gettop Acoustic Co., Ltd.

- BSE Co., Ltd.

- ZillTek Technology Corp.

- SensiBel AS

- Bosch Sensortec GmbH

- Wuxi Silicon Source Technology Co., Ltd.

- Microsonic GmbH

- Massa Products Corporation

- XARION Laser Acoustics GmbH

- Ocean Sonics Ltd.

- Sonardyne International Ltd.

- Precision Acoustics Ltd.

- Audiowell Electronics(Guangdong)Co., Ltd.

- Fuzhou Feiying Ultrasonic Technology Co., Ltd.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 179 Pages

- 納期

- 2~3営業日