全エクソームシーケンシング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Whole Exome Sequencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 160 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687710

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

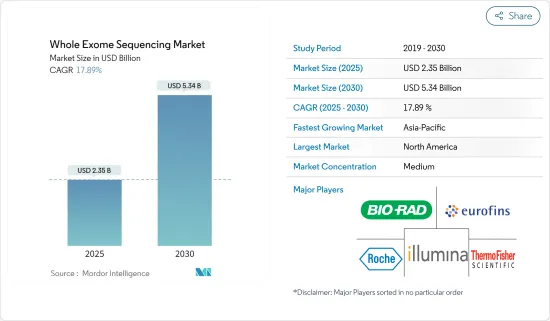

全エクソームシーケンシング市場規模は2025年に23億5,000万米ドルと推定・予測され、予測期間中(2025~2030年)のCAGRは17.89%で、2030年には53億4,000万米ドルに達すると予測されます。

世界の全エクソームシーケンシング市場を推進する主な要因としては、臨床診断における用途の拡大、希少疾患の診断需要の高まり、ゲノミクスと次世代シーケンシングにおける研究開発努力の強化、個別化医療への意欲の高まりなどが挙げられます。例えば、2022年3月にBritish Medical Journalに掲載された論文では、全エクソームシーケンシングは小児期の希少遺伝病と診断された一部の患者グループに対して日常的に利用可能であることが強調されています。同記事はさらに、次世代シーケンサーは数百から数千の遺伝子の配列を迅速に、しかも大幅に削減したコストで決定できることを強調しています。このような利点を考えると、全エクソームシーケンシング市場は今後数年で成長する見込みです。

さらに、全エクソームシーケンシングは、HIV、がん、COVID-19などの疾患に関連するウイルスのゲノムを検査する上で極めて重要な役割を果たしています。これらの疾患の有病率が上昇するにつれて、全エクソームシーケンシングの需要も増加しています。例えば、世界保健機関(WHO)のHIV Statisticsによると、2023年には世界で約3,990万人がHIVとともに生活しています。このようなゲノムシーケンス法は、病気につながる可能性のある遺伝子変異に光を当て、RNAシーケンスの需要をさらに増幅させる。

さらに、ゲノミクスと次世代シーケンサーにおける研究開発の急増が市場の成長を促進しています。例えば、2022年5月、NanoString Technologies Inc.は、Illumina NextSeq 1000、NextSeq 2000シーケンスシステム、GeoMx Digital Spatial Profilerのユーザー向けに空間データ解析を強化するように設計されたクラウドベースのワークフローを発表しました。この技術革新は、統合されたユーザーフレンドリーなランプランニングツールにより、プロテオーム分析と同時に全トランスクリプトームの空間解析を合理化します。このような進歩は市場をさらに強化すると予想されます。

結論として、前述の要因は市場の堅調な成長軌道を示しています。この技術の複雑な性質、熟練した専門家の差し迫ったニーズ、全エクソームシーケンシングを取り巻く法的・倫理的ジレンマが、市場の拡大を抑制する可能性があります。

全エクソームシーケンシング市場の動向

個別化医療セグメントは予測期間中に大幅な成長が見込まれる

個別化医療は、疾患の分子的基盤に基づいて個々の患者に合わせた治療法を提供します。このアプローチは近年人気を集めています。しばしば「個別化医療」と呼ばれる精密医療は、各患者の明確な遺伝子プロファイルを重視することで、従来の方法とは一線を画しています。遺伝学が進歩し、人間の遺伝的体質、特にそれが健康、発育、薬物反応にどのような影響を及ぼすかについての理解が深まったことで、医療専門家は無数の健康状態に対して、より安全で効果的な治療法を作り出そうとしています。精密医療の利点は多岐にわたり、健康とヘルスケアの両方を向上させる。

個別化医療分野を推進する要因としては、様々ながんの有病率の上昇、がんやその他の疾患に対する個別化治療の手頃な価格、個別化治療による副作用の軽減、先進国市場での広範な採用、革新的な薬剤の出現などが挙げられます。

例えば、2022年8月、医療機器イノベーションコンソーシアムは、体細胞参照サンプル(SRS)イニシアチブのパイロットプロジェクトを開始しました。このプロジェクトは、次世代シーケンシング(NGS)を利用したがん診断薬のバリデーションと規制審査プロセスを改良することを目的としています。NGSは、診断と治療における新たな道を開く、変革的な技術として際立っています。しかし、これらの診断検査が臨床的に実行可能であるためには、厳密なバリデーションを受ける必要があり、このプロセスは参照サンプルに大きく依存しています。

さらに、市場各社は提携、合併、買収、製品発売などの戦略的策略に取り組んでおり、これらすべてが同分野の拡大に拍車をかけると予想されます。例えば、2023年11月、イルミナは低・中所得国における病原体シーケンシングをターゲットとしたGlobal Health Access Initiativeを発表しました。このイニシアチブでは、さまざまなシーケンスアプリケーションを割引価格で提供しています。これには、結核の薬剤耐性プロファイリング、進化・再興ウイルスを監視するための全ゲノムシーケンス、インフルエンザ様疾患サーベイランスのための呼吸器病原体検出、病原体を追跡するための環境モニタリング(廃水分析など)、集団レベルの抗菌薬耐性の監視などが含まれます。

このようなダイナミクスを考えると、個別化医療分野は今後数年で大きく成長する可能性があります。

北米は予測期間中に大幅な成長が見込まれる

北米は、収益の面で主要な地域市場として際立っています。全エクソームシーケンシング市場の成長を促進する主な要因としては、がんなどの遺伝性疾患や慢性疾患の有病率の上昇、高齢化、標的医療や個別化医療に対する需要の増加、政府の支援策などが挙げられます。2022年10月にHIV.govが報告したように、米国では約120万人がHIVに感染しています。このことは、感染症の負担が増加していることを裏付けており、診断薬に対する需要の高まりが予測され、予測期間中の市場成長を後押しするものと思われます。

主要企業間の合併、買収、製品上市、提携は、この地域の市場ダイナミクスをさらに活性化させる。注目すべき例としては、QIAGENが2023年1月にカリフォルニアを拠点とする人口ゲノミクスのリーダーであるHelix社と独占的戦略提携を結んだことが挙げられます。この提携は遺伝性疾患のコンパニオン診断の開発を促進するものです。高度なNGSとPCR技術を駆使した統合サービスは、迅速な患者募集、実臨床でのエビデンス、包括的な診断ソリューションを約束します。

感染症の有病率の上昇や積極的な製品上市など、これらの力学を考慮すると、北米市場は今後数年で大幅な成長が見込まれます。

全エクソームシーケンシング業界の概要

全エクソームシーケンシング市場は、世界的および地域的に事業を展開する企業が数社存在するため、その性質上、適度に統合されています。競合情勢には、Eurofins Scientific Group、Bio-Rad Laboratories Inc.、F. Hoffmann-La Roche AG、illumine Inc.、Thermo Fisher Scientific Inc.など、市場シェアを持ち知名度の高い国内外の企業の分析が含まれます。コニカミノルタ株式会社(Ambry Genetics)、Beijing Genomics Institute、Azenta Inc.、Psomagen Inc.(Macrogen Inc.)、PerkinElmer Inc.、GENEYX GENOMEX、CD Genomics、QIAGEN Inc.

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 臨床診断におけるアプリケーションの増加と希少疾患の診断需要の増加

- ゲノミクスおよび次世代シーケンサー分野における研究開発の増加

- 個別化医療への需要の高まり

- 市場抑制要因

- 技術の複雑さと熟練者の不足

- 全エクソームシーケンシングに関連する法的・倫理的問題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- システム

- キット

- サービス

- 技術別

- 第2世代シーケンシング

- 合成によるシーケンシング(SBS)

- ハイブリダイゼーションおよびライゲーションによるシーケンシング(SBL)

- 第3世代シーケンシング

- 第2世代シーケンシング

- 用途別

- 診断

- 創薬および開発

- 個別化医療

- その他の用途(農業、動物調査など)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Konica Minolta Inc.(Ambry Genetics)

- Beijing Genomics Institute

- Bio-Rad Laboratories Inc.

- Eurofins Scientific Group

- F. Hoffmann-La Roche AG

- Azenta, Inc.

- Illumina Inc.

- Psomagen Inc.(Macrogen Inc.)

- PerkinElmer Inc.

- Thermo Fisher Scientific Inc.

- GENEYX GENOMEX

- CD Genomics

- QIAGEN Inc.

第7章 市場機会と今後の動向

目次

The Whole Exome Sequencing Market size is estimated at USD 2.35 billion in 2025, and is expected to reach USD 5.34 billion by 2030, at a CAGR of 17.89% during the forecast period (2025-2030).

Key factors propelling the global whole exome sequencing market include its rising applications in clinical diagnostics, heightened demand for rare disease diagnoses, intensified R&D efforts in genomics and next-generation sequencing, and an increasing appetite for personalized medicine. For example, a March 2022 article in the British Medical Journal highlighted that whole exome sequencing is routinely available for a select group of patients diagnosed with rare childhood genetic diseases. The article further emphasized that next-generation sequencing can rapidly sequence hundreds or even thousands of genes at a significantly reduced cost. Given these advantages, the market for whole exome sequencing is poised for growth in the coming years.

Additionally, whole exome sequencing plays a pivotal role in testing the genomes of viruses linked to diseases like HIV, cancer, and COVID-19. As the prevalence of these diseases rises, so does the demand for whole-exome sequencing. For instance, according to the World Health Organization (WHO) HIV Statistics, around 39.9 million people globally were living with HIV in 2023. Such genomic sequencing methods shed light on genetic variants that may lead to diseases, further amplifying the demand for RNA sequencing.

Moreover, the surge in R&D within genomics and next-generation sequencing is fueling market growth. For instance, in May 2022, NanoString Technologies Inc. unveiled a cloud-based workflow designed to enhance spatial data analysis for users of the Illumina NextSeq 1000, NextSeq 2000 sequencing systems, and the GeoMx Digital Spatial Profiler. This innovation streamlines the spatial analysis of whole transcriptomes in tandem with proteome analytes due to its integrated, user-friendly run planning tool. Such advancements are expected to bolster the market further.

In conclusion, the aforementioned factors indicate a robust growth trajectory for the market. The intricate nature of the technique, a pressing need for skilled professionals, and the legal and ethical dilemmas surrounding whole exome sequencing may restrain the market's expansion.

Whole Exome Sequencing Market Trends

Personalized Medicine Segment is Expected to Witness Significant Growth Over the Forecast Period

Personalized medicine tailors therapies to individual patients based on the molecular underpinnings of their diseases. This approach has gained traction in recent years. Often referred to as "individualized medicine," precision medicine diverges from traditional methods by emphasizing each patient's distinct genetic profile. With advancements in genetics and a deeper comprehension of human genetic makeup, especially how it influences health, development, and drug responses, medical professionals are crafting safer, more effective treatments for a myriad of health conditions. The benefits of precision medicine are manifold, enhancing both health and healthcare.

Factors propelling the personalized medicine segment include the rising prevalence of various cancers, the affordability of personalized therapies for cancer and other diseases, reduced side effects from tailored treatments, widespread adoption in developed markets, and the emergence of innovative drugs.

For example, in August 2022, the Medical Device Innovation Consortium initiated a pilot project under its Somatic Reference Sample (SRS) Initiative. This project aims to refine the validation and regulatory review processes for cancer diagnostics utilizing next-generation sequencing (NGS). NGS stands out as a transformative technology, unlocking new avenues in diagnostics and therapeutics. However, for these diagnostic tests to be clinically viable, they must undergo rigorous validation, a process heavily reliant on reference samples.

Furthermore, market players are engaging in strategic maneuvers like partnerships, mergers, acquisitions, and product launches, all of which are expected to fuel the segment's expansion. For instance, in November 2023, Illumina unveiled its Global Health Access Initiative, targeting pathogen sequencing in low- and middle-income countries. This initiative offers discounted rates on a range of sequencing applications. These include drug resistance profiling for tuberculosis, whole-genome sequencing to monitor evolving and reemerging viruses, respiratory pathogen detection for influenza-like illness surveillance, environmental monitoring (like wastewater analysis) to track pathogens, and overseeing population-level antimicrobial resistance.

Given these dynamics, the personalized medicine segment is poised for substantial growth in the coming years.

North America is Expected to Witness a Significant Growth Over the Forecast Period

North America stands out as a leading regional market in terms of revenue. Key drivers fueling the growth of the whole-exome sequencing market include the rising prevalence of genetic and chronic disorders like cancer, an aging population, an increasing demand for targeted and personalized medicine, and supportive government initiatives. As reported by HIV.gov in October 2022, approximately 1.2 million individuals in the United States were affected by HIV. This underscores a rising burden of infectious diseases, which is expected to register a heightened demand for diagnostics and bolster market growth during the forecast period.

Mergers, acquisitions, product launches, and partnerships among key players further energize market dynamics in the region. A notable example is QIAGEN's exclusive strategic partnership with California-based Helix, a population genomics leader established in January 2023. This collaboration is set to advance the development of companion diagnostics for hereditary diseases. The integrated services, powered by advanced NGS and PCR technologies, promise rapid patient recruitment, real-world evidence, and comprehensive diagnostic solutions.

Given these dynamics, including the rising prevalence of infectious diseases and active product launches, the North American market is poised for substantial growth in the coming years.

Whole Exome Sequencing Industry Overview

The whole exome sequencing market is moderately consolidated in nature due to the presence of a few companies operating globally as well as regionally. The competitive landscape includes an analysis of some international and domestic companies that hold market shares and are well known, including Eurofins Scientific Group, Bio-Rad Laboratories Inc., F. Hoffmann-La Roche AG, illumine Inc., and Thermo Fisher Scientific Inc. Konica Minolta Inc. (Ambry Genetics), Beijing Genomics Institute, Azenta Inc., Psomagen Inc. (Macrogen Inc.), PerkinElmer Inc., GENEYX GENOMEX, and CD Genomics, QIAGEN Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Applications in the Clinical Diagnosis and Growing Demand for the Diagnosis of Rare Diseases

- 4.2.2 Increasing R&D in the Field of Genomics and Next-generation Sequencing

- 4.2.3 Increasing Demand for Personalized Medicine

- 4.3 Market Restraints

- 4.3.1 High Complexity of Technique and Lack of Skilled Personnel

- 4.3.2 Legal and Ethical Issues Associated with Whole Exome Sequencing

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value in USD)

- 5.1 By Product Type

- 5.1.1 System

- 5.1.2 Kits

- 5.1.3 Services

- 5.2 By Technology

- 5.2.1 Second-Generation Sequencing

- 5.2.1.1 Sequencing by Synthesis (SBS)

- 5.2.1.2 Sequencing by Hybridization and Ligation (SBL)

- 5.2.2 Third-generation Sequencing

- 5.2.1 Second-Generation Sequencing

- 5.3 By Application

- 5.3.1 Diagnostics

- 5.3.2 Drug Discovery and Development

- 5.3.3 Personalized Medicine

- 5.3.4 Other Applications (Agriculture, Animal Research, etc.)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Konica Minolta Inc. (Ambry Genetics)

- 6.1.2 Beijing Genomics Institute

- 6.1.3 Bio-Rad Laboratories Inc.

- 6.1.4 Eurofins Scientific Group

- 6.1.5 F. Hoffmann-La Roche AG

- 6.1.6 Azenta, Inc.

- 6.1.7 Illumina Inc.

- 6.1.8 Psomagen Inc. (Macrogen Inc.)

- 6.1.9 PerkinElmer Inc.

- 6.1.10 Thermo Fisher Scientific Inc.

- 6.1.11 GENEYX GENOMEX

- 6.1.12 CD Genomics

- 6.1.13 QIAGEN Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 160 Pages

- 納期

- 2~3営業日