海洋音響センサ-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Marine Acoustic Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683852

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

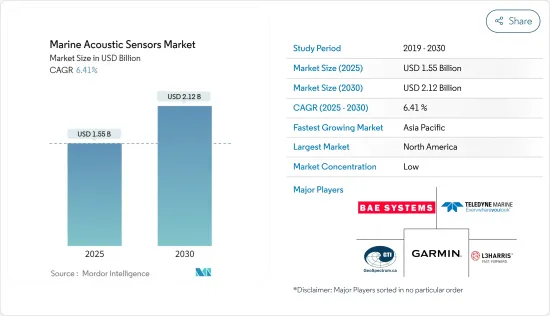

海洋音響センサ市場規模は2025年に15億5,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは6.41%で、2030年には21億2,000万米ドルに達すると予測されています。

海洋音響センサは、リアルタイムのデータ収集や環境モニタリングのために、様々な船型の小型装置で使用されています。これらのデバイスは、多数の用途を持つ多種多様な形態で提供されています。海洋音響センサは、海洋生物検出、モニタリング、その他の目的に使用されます。

主なハイライト

- モノのインターネット(IoT)技術は、最近の知的作業技術革命のコンセプトとして提示されています。海洋産業は、音響センサー技術アプリケーションの急速な増加ラッシュと、低コストのコンピューティングコンポーネントの能力により、幅広い機会にアクセスできるようになります。

- ドックは、世界な海洋技術におけるIoTの急速な採用により、そのクラウドベースのIoTをサポートするための孤独なネットワークで世界的にサポートされています。インテリジェントでスマートな港湾は、IoTスマートポートを介してすべてのデバイスが接続され、完全に自動化されていると表現することができます。これは、スマートポートの中央インフラを構成する音響センサーや無線デバイスを含むインテリジェントセンサーのネットワークで構成されます。

- 軍艦、潜水艦、船舶を警備し、リアルタイムの状況認識を与えるための、技術に基づく音響センサの台頭が、予測期間中の市場成長を後押ししています。

- 船舶用音響センサは、信号処理とセンサ機能を1つの製品に統合できます。しかし、音響センサは、不十分な安定性や信頼性のような運用上の課題に直面しており、その採用拡大に影響を与えています。

- 完全自律型船舶を拡大するため、世界的に大手造船会社やシステム開発会社による研究開発活動への投資が増加しており、海洋音響センサのニーズが高まっています。自律型船舶は、海洋産業にとって持続可能で安全かつ効率的なプロセスモードとして登場すると推定されています。

海洋音響センサ市場動向

水中トランスデューサが製品セグメントで主要シェアを占める

- 水中変換器とは、水中で1つのエネルギー形態を別の形態に変換する装置です。海洋技術では、電気信号を音波に変換する装置(アクチュエータ)や、音波を電気信号に変換する装置(センサ)を指すことが多いです。ハイドロフォンは音の検出に使われる特定のタイプの水中トランスデューサーであるが、他の水中トランスデューサーは、ソナー信号の放射や様々な用途のための振動の発生など、異なる目的を果たすことができます。

- 水中トランスミッションに関するいくつかの実験やプロジェクトが行われており、水中トランスデューサー分野をさらに牽引しています。例えば、2022年11月、日本電信電話株式会社、株式会社NTTドコモ、NTTコミュニケーションズ株式会社は、様々な海洋活動のための広帯域無線通信の実現に関する共同実験を行いました。水中音響通信を用いたフィールド実験で、浅い海域(水深30m程度)で1Mbps/300mの水中トランスミッションに成功しました。

- また、様々な製品の革新や開発、防衛分野との連携もこの調査セグメントを牽引しています。例えば、2023年5月、米国海軍と共同で、Teledyne Marine社はヘリコプターからの海中グライダー展開を初めて成功させ、航空機からの自律型海中ロボット(AUV)の打ち上げに初めて成功しました。テレダイン・スローカム・グライダーは、複数の永続的な作戦任務のための長期耐久型AUVです。海軍海洋局(NAVOCEANO)はLBSグライダーを操縦し、海軍の作戦をサポートする収集データを含みます。

- 2023年、SIPRIは米国の軍事費が世界の軍事費の37%を占めると報告しました。

北米が大きな市場シェアを占める

- へそくり防衛における水中通信の採用の増加、自律型水中航行体の増加、科学探査とデータ収集のニーズの急増は、北米の水中通信システム市場の成長を促進する主な要因であり、市場調査をさらに推進しています。

- 自律型水中車両は、軍、海軍、沿岸警備隊、特に海底作戦の主流となっています。米国海軍は、水雷対策(MCM)、情報、監視、偵察、識別(ID)、対潜水艦戦(ASW)など、さまざまな用途にこれらの乗り物を幅広く使用しています。海軍は、中国からの重大な課題に対抗するため、水中車両の早期購入に向けた取得戦略を加速させています。

- パンデミックのピーク時、米国海軍海システム司令部ワシントンは、海軍作戦をアップグレードするため、ボーイングと1,110万米ドル相当の契約を結びました。同社は、誘導制御、航行、状況認識、任務センサー、人口、基幹通信など、将来の海軍作戦のためのアップグレードを期待されていました。例えば、同時期に米国海軍は、超大型無人潜水艇(XLAUV)を開発するため、ボーイング社と4,300万米ドル相当の契約を締結しました。

- 2022年8月、国防総省の産業基盤政策室は、テキサス州オースティンのオースティン・センター・フォー・マニュファクチャリング・アンド・イノベーション(ACMI)と共に、国防生産法(DPA)タイトルIIIプログラムを通じて先駆的な製造パイロット・プログラムを開始しました。この世界初のパイロット・プログラムは、急速に生産規模を拡大できる商用および軍事用途の先端製造技術に焦点を当てることが期待されていました。このような軍事用途の開発も、この地域の市場研究を促進する可能性があります。

- 国防費の増加も市場を牽引する可能性があります。例えば、米国議会予算局によると、米国の国防費は2033年まで毎年増加すると予測されています。米国の国防費は2033年には1兆1,000億米ドルまで増加すると予測されています。

海洋音響センサー産業の概要

調査対象市場は、BAE Systems PLC、Garmin Ltd、Teledyne Marine Technologies(Teledyne Technologies Incorporated)、Ocean Sonics Ltd、Geospectrum Technologies Inc.などの大手企業が存在し、細分化されています。調査対象市場のプレーヤーは、製品提供を強化し、持続可能な競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年6月-ThalesはLa Spezia海軍基地に統合サービスセンターを新設し、イタリア海軍との連携を強化。このセンターは、掃海艇に搭載されたソナーシステムのメンテナンスと、ナポリとタラントの海軍基地で活動するフリゲート艦の水際支援において、海軍の独占サービスパートナーとしての役割を果たします。

- 2023年1月、同社はオランダ王立海洋研究所(NIOZ)が新型AUV「GaviaOsprey」を取得したことを発表しました。NIOZはオランダの国立海洋研究所で、オランダの海洋に関する主要な科学的疑問に取り組むため、学際的な応用海洋研究を実施しています。NIOZは、赤道から極点まで、大陸棚から深海まで、そして現在から過去まで、気候変動における海洋の役割を研究しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

第5章 市場力学

- 市場促進要因

- 水中測位のための音響ナビゲーションの導入拡大

- 各国における防衛費の増加

- 市場の課題

- 互換性と設置の問題、周波数帯域の制限

- KPI分析

第6章 市場セグメンテーション

- 製品別

- ハイドロフォン

- 水中トランスデューサ

- 音響曳航アレイ

- サイドスキャンソナー

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

第7章 用途分析

- 用途別

- 水深・水深測定

- 海洋イメージング

- 海洋生物検出

- 軍事

- 海洋調査とモニタリング

第8章 競合情勢

- 企業プロファイル

- BAE Systems PLC

- Garmin Ltd

- Teledyne Marine Technologies(Teledyne Technologies Incorporated)

- Ocean Sonics Ltd

- Geospectrum Technologies Inc.

- L3harris Technologies Inc.

- Hottinger Bruel & Kjaer(Spectris PLC)

- Cobham Ultra Seniorco S.a R.l.

- Thales Group

- CTS Corporation

第9章 市場展望

目次

The Marine Acoustic Sensors Market size is estimated at USD 1.55 billion in 2025, and is expected to reach USD 2.12 billion by 2030, at a CAGR of 6.41% during the forecast period (2025-2030).

Marine acoustic sensors are used in small devices in various ship types for real-time data collection and environmental monitoring. These devices come in a broad variety of forms with numerous uses. Marine acoustic sensors are used for marine life detection, monitoring, and other purposes.

Key Highlights

- The Internet of Things (IoT) technology has been presented as a recent intelligent work technical revolution concept. The marine industry will have access to a broad range of opportunities due to the rapidly increasing rush of acoustic sensor technology applications and the capabilities of low-cost computing components.

- Docks are being supported globally in solitary networks to support their cloud-based IoT due to the rapid adoption of IoT in global marine technology. An intelligent and smart port can be described as fully automated, with all devices connected via an IoT smart port. It comprises a network of intelligent sensors, including acoustic sensors and wireless devices that make the central infrastructure of a smart port.

- The rising technological-based acoustic sensors for military ships, submarines, and vessels to guard and give them real-time situational awareness are boosting the market growth during the forecast period.

- The marine acoustic sensors allow the integration of signal processing and sensor functions within one product. However, acoustic sensors have faced operational challenges like inadequate stability and reliability, impacting their adoption growth.

- Increased investments in R&D activities by leading shipbuilders and system developers globally for expanding fully autonomous ships have increased the need for marine acoustic sensors. Autonomous ships are estimated to launch as sustainable, safe, and efficient modes of process for the marine industry.

Marine Acoustic Sensors Market Trends

Underwater Transducer to Hold Major Share in the Product Segment

- An underwater transducer is a device that converts one form of energy to another underwater. Marine technology often refers to devices that can convert electrical signals into sound waves (actuators) or sound waves into electrical signals (sensors). While hydrophones are a specific type of underwater transducers used for sound detection, other underwater transducers can serve different purposes, such as emitting sonar signals or generating vibrations for various applications.

- Several experiments and projects in underwater transmission are happening, further driving the underwater transducer segment. For instance, in November 2022, the NTT Corporation, NTT DOCOMO, INC, and NTT Communications Corporation performed a joint experiment on achieving broadband wireless communication for various marine activities. It succeeded at 1-Mbps/300-m underwater transmission in a shallow sea area (water depth of about 30 m) using underwater acoustic communication in field experiments.

- Various product innovations, developments, and collaborations with the defense sector are also driving the studied segment. For instance, in May 2023, In collaboration with the US Navy, Teledyne Marine completed the first-ever successful undersea glider deployment from a helicopter, marking the first time an autonomous underwater vehicle (AUV) was successfully launched from an aircraft. The Teledyne Slocum glider is a long-endurance AUV for multiple persistent operational missions. The Naval Oceanographic Office (NAVOCEANO) pilots the LBS gliders and includes collected data supporting Navy operations.

- In 2023, SIPRI reported that the United States' military expenditure made up 37 percent of global military expenditure.

North America Holds Significant Market Share

- An increase in the adoption of underwater communication in navel defense, an increase in autonomous underwater vehicles, and a surge in the need for scientific exploration and data collection are the key factors driving the growth of the underwater communication systems market in North America, further driving the market studied.

- Autonomous underwater vehicles have become mainstream for the military, navy, and coastal security forces, especially subsea operations. The US Navy extensively uses these vehicles for various applications, such as mine countermeasures (MCM), intelligence, surveillance and reconnaissance, identification (ID), and anti-submarine warfare (ASW). The Navy has accelerated acquisition strategies for the faster purchase of underwater vehicles to counter significant challenges from China.

- During the peak time of the pandemic, US Naval Sea Systems Command Washington signed a contract worth USD 11.1 million with Boeing to upgrade naval operations. The company was expected to upgrade for future naval operations such as guidance and control, navigation, situational awareness, mission sensors, population, and core communication. For instance, at the same time, the US Navy signed a contract worth USD 43 million with Boeing to develop an Orca Extra Large Unmanned Undersea Vehicle (XLAUV).

- In August 2022, the Department of Defense's Industrial Base Policy Office launched a pioneering manufacturing pilot program through the Defense Production Act (DPA) Title III Program with the Austin Center for Manufacturing and Innovation (ACMI) in Austin, Texas. The first-of-its-kind pilot program was expected to focus on advanced manufacturing technology for commercial and military applications that can be rapidly scaled to production. These developments in military applications may also drive the market studied for the region.

- The increase in defense expenses may also drive the market studied. For instance, according to the US Congressional Budget Office, defense spending in the United States is predicted to increase yearly until 2033. Defense outlays in the United States are expected to increase up to USD 1.1 trillion in 2033.

Marine Acoustic Sensors Industry Overview

The market studied is fragmented with the presence of major players like BAE Systems PLC, Garmin Ltd, Teledyne Marine Technologies (Teledyne Technologies Incorporated), Ocean Sonics Ltd, and Geospectrum Technologies Inc. Players in the market studied are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- June 2023 - Thales reinforced its collaboration with the Italian Navy by inaugurating a new integrated service center at the La Spezia naval base. This center will serve as the exclusive service partner of the Navy for the upkeep of sonar systems installed on minesweeper vessels and the waterfront support of frigate vessels operating in the Naval Bases of Naples and Taranto.

- In January 2023, the company announced the acquisition of a new GaviaOsprey AUV by the Royal Netherlands Institute for Sea Research (NIOZ). NIOZ is the Netherlands' national oceanographic institute conducting multidisciplinary applied marine research to address major scientific questions about the company's oceans and seas. NIOZ studies the ocean's role in changing climate from equator to pole, from the continental shelf to the deep ocean, and from present to past.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Deployment of Acoustic Navigation for Underwater Positioning

- 5.1.2 Rising Defense Spending in Several Countries

- 5.2 Market Challenges

- 5.2.1 Compatibility and Installation Issues and the Presence of a Limited Frequency Band

- 5.3 KPI Analysis

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Hydrophones

- 6.1.2 Underwater Transducer

- 6.1.3 Acoustic Towed Array

- 6.1.4 Side-scan Sonar

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

7 APPLICATION ANALYSIS

- 7.1 By Application

- 7.1.1 Water Depth and Bathymetry

- 7.1.2 Marine Imaging

- 7.1.3 Marine Life Detection

- 7.1.4 Military

- 7.1.5 Marine Research and Monitoring

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 BAE Systems PLC

- 8.1.2 Garmin Ltd

- 8.1.3 Teledyne Marine Technologies (Teledyne Technologies Incorporated)

- 8.1.4 Ocean Sonics Ltd

- 8.1.5 Geospectrum Technologies Inc.

- 8.1.6 L3harris Technologies Inc.

- 8.1.7 Hottinger Bruel & Kjaer (Spectris PLC)

- 8.1.8 Cobham Ultra Seniorco S.a R.l.

- 8.1.9 Thales Group

- 8.1.10 CTS Corporation

9 MARKET OUTLOOK

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日