|

|

市場調査レポート

商品コード

1771254

自律走行車の4D画像レーダー市場 - 業界、市場、競合分析(2025年版)4D Imaging Radar in Autonomous Vehicles - Industry, Market, and Competition Analysis, Edition 2025 |

||||||

|

|||||||

|

|||||||

| 自律走行車の4D画像レーダー市場 - 業界、市場、競合分析(2025年版) |

|

出版日: 2025年06月09日

発行: M14 Intelligence

ページ情報: 英文 80 Pages

納期: お問合せ

|

全表示

- 概要

- 目次

ADASと自律走行車における4Dイメージングレーダーの車室内および車外センシング用途、60GHz、76-81GHz、140GHz帯、SAEレベル2+以上の用途、新興4D画像処理企業の競合評価

主なハイライト

- ADASとAVレーダーモジュール市場規模は2025年から2035年にかけて2.7倍に拡大し、11.7%のCAGRとなり、2025年の90億米ドルから2035年には250億米ドルに達する見込みです。

- 4Dイメージング・レーダー・モジュールは2035年までに56%以上普及すると予想され、現在の市場普及率から45%急増します。

- 2035年までには、自律走行車の台頭とコスト削減により、4Dレーダーが短・中距離を独占し、多くのADASおよびAVシステムで従来の3Dレーダーに取って代わる可能性があります。

- 乗員モニターや左子検知の車内用途は、EURO NCAPのような規制の義務化により、ニッチな分野として成長しています。

- TSMC、GlobalFoundries、imec別140GHzレーダー技術の開発は、屋内外用途の高解像度センシングに焦点を当てています。

- Continental、Bosch、Vayyar、Arbe、Uhnder、NXP、Teslaなどの主要企業がイノベーションを推進しており、最近のCES 2025やIAA Mobility 2025でのショーケースでは、解像度、効率、規制対応における進歩が強調されています。

- RFISee、RadSee、Smart Radar System、Zadar Labs、InnoSenT、Infineon、Ainsteinは、4Dイメージング・レーダー業界の著名な新興企業です。一方、Texas Instruments、NXP Semiconductors、STMicroelectronics、Xilinx、Analog Devicesは、ADAS(先進運転支援システム)やより高度な車両自動化をサポートする4D画像レーダー・ソリューションを積極的に開発しているシステムオンチップ(SoC)プロバイダーの大手です。

- ダイナミックな解像度を実現するAIを搭載したソフトウェア定義レーダーに注力するZendar Inc.、Qamcom GroupからスピンアウトしたSensrad AB、迅速な市場参入に注力するWaveye、ロボットタクシーや都市型AVへの早期導入を目指すAltos Radar、地域拡大のために中国のOEM(SAIC、Geelyなど)と提携するAltos Radar、自律走行シャトルや産業用アプリケーションなどのニッチ市場をターゲットとするXavveoなどの新興企業があります。

サンプルビュー

包括的範囲

M14インテリジェンスは、自律型、コネクテッド、電動、シェアードモビリティの主要動向を把握する能力を中核とし、4D画像レーダー技術に関する調査結果を発表しました。

- ADAS、自律走行車、ロボット車- 市場展望

- ADASとAV産業におけるレーダーセンサーの現状

- 自動化レベル(ADAS、レベル2/2+、レベル3、レベル4/5)、動作範囲(短距離、中長距離)、動作周波数帯域(60GHz、76~81GHz、140GHz)など、さまざまな観点からレーダー需要の潜在的変化と市場規模を把握

- 変調技術-FMCWとデジタルコード変調(DCM)

- レーダーオンチップとMIMOアンテナ設計

- AIベースの処理

- 車内および世界に向けた車外センシング用4Dイメージング・レーダーオンチップ・センサーの市場浸透動向

- 地域ごとの周波数規制と割り当ての影響

- 4Dイメージング・レーダーのハードウェア・チップ・ソフトウェア・ソリューションと、センサー・スイート・ダイナミクスへの課題

- AI統合、レーダー・オン・チップ、センサー・フュージョンなど、市場を再構築する破壊的動向

- 高コストや統合の複雑さなどの課題と、半導体やソフトウェア定義レーダーの進歩がこれらのハードルにどのように対処しているか

- 自動車レーダー市場でソリューションを提供するチッププロバイダやティア1企業の戦略と市場開拓とともに、新興リーダー企業や新興企業の競合評価。

市場概要

自律走行車向け4D画像レーダー市場は、先進運転支援システム(ADAS)と自律走行車(AVs)の進化を促進し、自動車技術革新の最前線にあります。2024年の市場規模は約20億米ドル、2030年には100億米ドルに達すると予測され、CAGRは38%に達すると予測されています。これは、安全性向上に対する需要の高まり、規制の義務化、より高い自律走行レベル(SAEレベル4/5)の推進が要因となっています。

本レポートサマリーでは、ADASとAVにおけるレーダーセンサの採用、3Dレーダーに代わる4Dレーダーの普及、現在と将来のレーダー技術と周波数帯域、主要企業と新興企業、競合戦略、最近の動向、AVにおける4Dレーダーの重要な役割、ロボットタクシーとシャトルの市場開拓の可能性について、アジア太平洋などの将来性の高い地域を中心に調査しています。

ADASと自律走行車におけるレーダーセンサーの採用

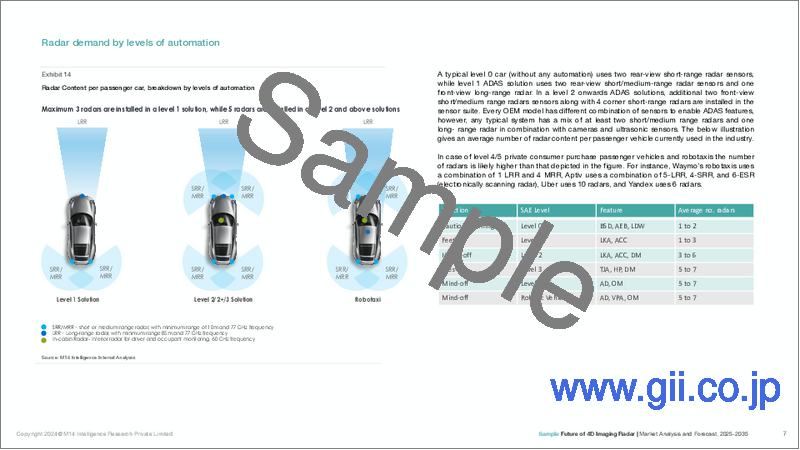

レーダーセンサーはADASとAVに不可欠であり、アダプティブ・クルーズ・コントロール(ACC)、自動緊急ブレーキ(AEB)、死角検知(BSD)、車線変更アシスト(LCA)、子供の存在検知(CPD)といった重要な機能を可能にします。カメラやLiDARとは異なり、レーダーは悪天候(霧、雨、雪など)や低照度下でも優れた性能を発揮し、信頼性の高い物体検出と測距を実現します。2024年には、世界で1億6,900万個以上のレーダー・センサが出荷され、2024年には車両1台当たり平均0.8個の長距離レーダーが搭載され、2030年には車両1台当たり1個に近づくと予想されています。Cruise(1台当たり21個のレーダー)やWaymo(6個の高性能4Dレーダー)などのRobotaxisは、レベル4/5の自律性のためにレーダーへの依存度が高いことを示しており、強固な環境認識を保証しています。安全性に対する消費者の要求と規制の義務化(EUの自動車一般安全規則、2024年7月など)に後押しされてADASの採用が増加しており、乗用車、商用トラック、自律走行シャトルへのレーダー配備が加速しています。

3Dレーダーに代わる4Dレーダー技術の普及

3Dレーダーのレンジ、方位、ドップラーデータに速度と高度を加えた4D画像レーダーは、解像度と精度が優れているため、急速に従来のレーダーに取って代わりつつあります。2025年までに、4Dレーダーは自動車レーダー市場の11.4%に浸透し、2~3年でニッチ技術から主流技術に移行すると予想されています。仰角分解能や複雑な物体分離(歩行者と車両の区別など)に苦戦する3Dレーダーとは異なり、4DレーダーはMassiveMIMO、DCM(Digital Code Modulation)、AI主導の処理を活用して高分解能の点群を生成し、一部の用途ではLiDARに匹敵します。例えば、ドライブパイロットを搭載したMercedes-BenzEQSや、ContinentalのARS540 4Dレーダーを搭載したヒュンダイIONIQ 5は、視界の悪い場所での性能向上を示しています。このシフトは、レベル3~5の自律走行における正確な知覚の必要性と、ジャンクション歩行者AEBのような高度な安全機能に対する規制要件によって推進されています。

競合戦略と地域市場機会

既存参入企業は、高解像度レーダーとLiDAR/カメラとのセンサー・フュージョンに焦点を当てた研究開発、世界なプレゼンス、OEMパートナーシップ(例えば、BoschとVolkswagenとの協業)を活用しています。一方、新興企業は費用対効果の高い設計(RadSeeのCOTS、UhnderのRoC)、AIの統合(Waveye、Zendar)、ニッチなアプリケーション(Sensradの産業用フォーカス)で差別化を図っています。ティア1やOEM(例 Arbe-BAIC)との提携という協業アプローチが、新規参入企業の市場参入を加速させています。

アジア太平洋地域は、中国のEVブームと政府のスマートシティ支援に牽引され、CAGRが最も高い急成長地域です。SAICやNIOのような企業は4Dレーダーを統合している(例えば、ZFとSAICの提携(2022年12月))。北米は、Ford、GM、TeslaなどのOEMがBlueCruise、Super Cruise、Autopilotに4Dレーダーを採用しており、米国が主導して最大の売上シェアを占めています。欧州は、厳しい安全規制(EUの2024年義務化など)により力強い成長を示しています。例えば、Mercedes-BenzとBMWはレベル2+/3システムでリードしており、その機会はプレミアム車とコンプライアンス主導の市場に明らかに反映されています。

市場の可能性

ロボットタクシーやシャトルを含むSAEレベル4/5のAV市場は、4Dレーダーの主要成長要因です。CruiseとWaymoは4Dレーダーを広範囲に展開しており、2024年にはフリートが1,000台を超え、商用ロボットタクシーサービスの台頭を示唆しています。世界の4Dレーダー市場は、レベル4/5のAVだけで2035年までに9億1,100万米ドルに達すると予測され、ロボットタクシーとシャトルが都市部や高速道路の自律走行に多額のレーダーユニットを消費します。

機会には以下が含まれます:

- 都市モビリティ:密集した環境をナビゲートするための高いレーダー需要(例えば、Waveye社の都市に特化したレーダー)。

- ラストマイル・デリバリー:安全のために4Dレーダーを採用する自律走行シャトルや配送車。

- 規制支援:AEBとCPDの義務化により、レベル4/5システムへのレーダー統合が進みます。

主な質問

- SAEレベル1~5の自律走行車への4D画像レーダーの普及速度と採用動向は?

- 2035年までの自動車用4D画像レーダー市場の現在の市場規模と成長の可能性は?

- 4Dレーダーに最も依存しているADAS機能(AEB、ACC、BSMなど)と、その安全性と性能の向上は?

- 4Dレーダーのコスト(77GHz、60GHz、140GHzなど)はどのように進化しているのか?

- 4Dレーダーと他のセンサー(LiDAR、カメラなど)を統合し、強固なセンサー・フュージョンを実現するための課題とは?

- 周波数規制(77GHz、60GHz、140GHzなど)は世界的にどのように異なり、4Dレーダーの配備にどのような影響を与えるのか?

- 4Dレーダーが乗員監視や左子検知といった車内監視で果たす役割は、どのように市場機会を生み出しているのか?

- 4Dレーダー市場を破壊している新興企業(Arbe、Uhnder、Zendarなど)とそのユニークな戦略とは?

- 4Dレーダー市場における既存企業(Continental、Bosch、NXPなど)と新興企業の競合優位性は?

- パートナーシップ、M&Aは4Dレーダー市場をどのように形成し、利害関係者にどのような機会をもたらすのか?

- 4Dレーダー市場の成長を支える投資や資金調達の動向と、利害関係者はそれをどのように活用できるのか?

4Dイメージングレーダー業界における最も興味深い質問に対する回答を得ることができます!

企業リスト

|

|

目次

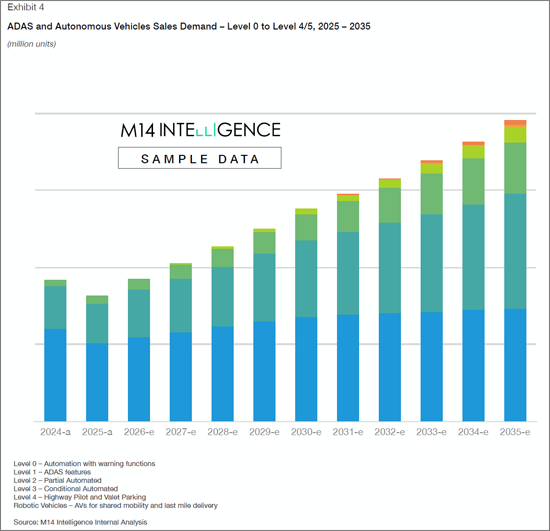

乗用車販売- 市場見通し

- 世界の乗用車販売台数(2019年~2024年)

- 乗用車販売の内訳(自動化レベル別、L1~L5)

- ADASおよび自動運転車市場の売上と予測、2025年~2035年

- 中国が市場を独占し、欧州は高い成長の可能性を秘めている

- 都市交通、ラストマイル配送、規制支援が新たな収益源となる

自動車レーダー産業の現状- 市場展望、数量と価値、2025年~2035年

- 車両あたりのレーダーセンサー要件

- レーダーの平均販売価格と予想される価格下落

- 自動化レベル別のレーダー需要

- 運用範囲別のレーダー需要(LRR、MRR/SRR、キャビン内)

- 周波数別のレーダー需要

- 周波数別のレーダー市場浸透率

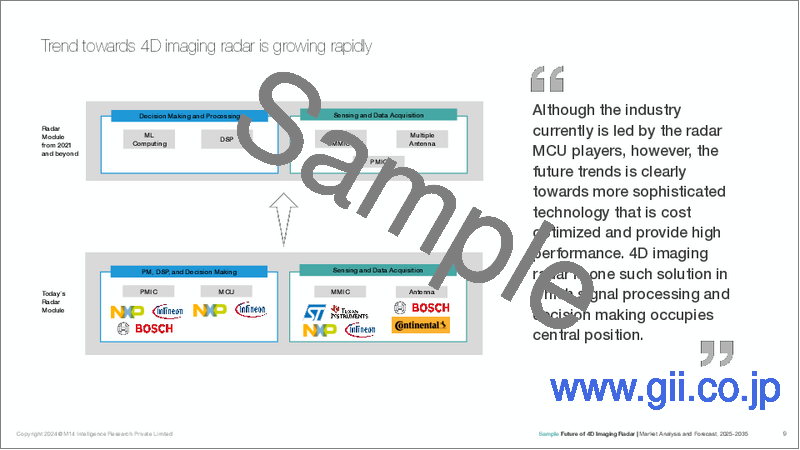

- 4Dイメージングレーダーのトレンドが急速に拡大

自動車用4Dレーダー産業- 市場展望、数量と価値、2025年~2035年

- 4Dレーダー市場- 自動化レベル別

- 4Dレーダー市場-ADASとAVアプリケーション別

- 外部センシングアプリケーション向け4Dイメージングレーダー

- 車内アプリケーション向け4Dイメージングレーダー

自動車4Dレーダー業界-競合評価

- 自動車向け4Dレーダー応用における新興企業プロファイル

- 製品の比較とベンチマーク

- パートナーシップマッピングとサプライヤー分析

- 4Dレーダー事業におけるOEM、Tier 1、センサーサプライヤー

- 主要企業別研究開発への投資

- 4Dレーダー事業におけるスタートアップ企業の資金調達・投資分析

In-cabin and Exterior Sensing Applications of 4D imaging radar in ADAS and Autonomous Vehicles; 60 GHz, 76-81 GHz, and 140 GHz Band, SAE Level 2+ and above applications, Emerging 4D imaging players competition assessment.

Key Highlights

- ADAS and AV radar module market size anticipated to grow 2.7x times between 2025 to 2035, accounting $25 billion in 2035 from $9 billion by 2025 at a CAGR of 11.7 percent

- 4D imaging radar modules expected to penetrate over 56 percent by 2035, a jump of 45% from the current market penetration

- By 2035, with the rise of autonomous vehicles and cost reductions, 4D radar could dominate short- and medium-range applications, potentially replacing conventional 3D radar in many ADAS and AV systems

- The in-cabin applications of occupant monitoring and left-child detection is a growing niche due to regulatory mandates like those from EURO NCAP

- Development of 140 GHz radar technology by TSMC, GlobalFoundries, and imec focuses on high-resolution sensing for both interior and exterior applications, though not yet commercialized, the technology is expected to strongly compete with 77GHz system by 2035

- Leading companies like Continental, Bosch, Vayyar, Arbe, Uhnder, NXP, and Tesla are driving innovation, with recent showcases at CES 2025 and IAA Mobility 2025 highlighting advancements in resolution, efficiency, and regulatory compliance.

- RFISee, RadSee, Smart Radar System, Zadar Labs, InnoSenT, Infineon, and Ainstein are prominent emerging players in the 4D imaging radar industry. Meanwhile, Texas Instruments, NXP Semiconductors, STMicroelectronics, Xilinx, and Analog Devices are leading System-on-Chip (SoC) providers actively developing 4D imaging radar solutions to support Advanced Driver Assistance Systems (ADAS) and higher levels of vehicle automation.

- Emerging start-ups such as Zendar Inc. focusing on software-defined radar with AI for dynamic resolution, Sensrad AB is a spin-out from Qamcom Group, focusing on rapid market entry, Waveye is targeting early adoption in robotaxis and urban AVs, Altos Radar partnering with Chinese OEMs (e.g., SAIC, Geely) for regional expansion, Xavveo is targeting niche markets like autonomous shuttles and industrial applications

SAMPLE VIEW

Countries Covered: Global (China, India, Japan, South Korea, US, Canada, South America, Germany, France, Italy, UK, Israel, others).

Exhaustive Coverage

M14 Intelligence with its core capabilities in understanding the key trends of autonomous, connected, electric, and shared mobility published the research on 4D imaging radar technology which talks about following important factors of the market.

- ADAS, Autonomous and Robotic Vehicles - Market Outlook

- Status of radar sensors in the ADAS and AV industry

- Understanding the potential change in the radar demand and its market size from different perspectives including - automation levels (ADAS, Level 2/2+, Level 3 and Level 4/5), range of operations (short, medium-long), and frequency band of operation (60 GHz, 76-81 GHz , and 140GHz)

- Modulation Techniques- FMCW and Digital Code Modulation (DCM)

- Radar-on-Chip and MIMO antenna design

- AI-based processing

- Market penetration trend of 4D imaging radar-on-chip sensors for in-cabin and world-facing exterior sensing applications

- Impact of frequency regulations and allocations across different geographies

- 4D imaging radar hardware chip and software solutions and how it is expected to challenge the sensor suite dynamics

- Disruptive trends like AI integration, radar-on-chip, and sensor fusion that will reshape the market

- Challenges like high costs and integration complexities, and how advancements in semiconductors and software-defined radar are addressing these hurdles

- Competition assessment of emerging leaders and start-ups, along with the strategies and developments of chip providers and tier-1s offering solutions in automotive radar market.

Market Overview

The 4D imaging radar market for autonomous vehicles is at the forefront of automotive innovation, driving the evolution of Advanced Driver Assistance Systems (ADAS) and autonomous vehicles (AVs) . Valued at approximately USD 2 billion in 2024, the market is projected to reach USD 10 billion by 2030, with a CAGR of 38%, fueled by the increasing demand for enhanced safety, regulatory mandates, and the push for higher autonomy levels (SAE Level 4/5).

This report summary explores the adoption of radar sensors in ADAS and AVs, the penetration of 4D radar replacing 3D radar, current and future radar technologies and frequency bands, leading and emerging players, competitive strategies, recent developments, the critical role of 4D radar in AVs, and market potential for robotaxis and shuttles, with a focus on high-potential regions like Asia-Pacific.

Adoption of Radar Sensors in ADAS and Autonomous Vehicles

Radar sensors are integral to ADAS and AVs, enabling critical features like Adaptive Cruise Control (ACC), Automatic Emergency Braking (AEB), Blind Spot Detection (BSD), Lane Change Assist (LCA), and Child Presence Detection (CPD) . Unlike cameras and LiDAR, radar excels in adverse weather conditions (e.g., fog, rain, snow) and low-light scenarios, providing reliable object detection and ranging. In 2024, over 169 million radar sensors were shipped globally, with an average of 0.8 long-range radars per vehicle in 2024, expected to approach 1 per vehicle by 2030. Robotaxis, such as Cruise (21 radars per vehicle) and Waymo (six high-performance 4D radars), demonstrate heavy reliance on radar for Level 4/5 autonomy, ensuring robust environmental perception. The rising adoption of ADAS, driven by consumer demand for safety and regulatory mandates (e.g., EU's Vehicle General Safety Regulations, July 2024), is accelerating radar deployment across passenger vehicles, commercial trucks, and autonomous shuttles.

Penetration of 4D Radar Technology Replacing 3D Radars

4D imaging radar, which adds velocity and elevation to the range, azimuth, and Doppler data of 3D radar, is rapidly replacing its predecessor due to superior resolution and accuracy. By 2025, 4D radar is expected to penetrate 11.4% of the automotive radar market, transitioning from a niche to a mainstream technology within 2-3 years. Unlike 3D radar, which struggles with elevation resolution and complex object separation (e.g., distinguishing a pedestrian from a vehicle), 4D radar leverages Massive MIMO, Digital Code Modulation (DCM) , and AI-driven processing to create high-resolution point clouds, rivaling LiDAR in some applications. For instance, Mercedes-Benz EQS with Drive Pilot and Hyundai IONIQ 5 with Continental's ARS540 4D radar showcase enhanced performance in poor visibility. The shift is driven by the need for precise perception in Level 3-5 autonomy and regulatory requirements for advanced safety features like Junction Pedestrian AEB.

Competitive Strategies and regional market opportunities

Established players leverage R&D, global presence, and OEM partnerships (e.g., Bosch's collaboration with Volkswagen) focusing on high-resolution radar and sensor fusion with LiDAR/cameras. On the other hand, start-ups differentiate through cost-effective designs (RadSee's COTS, Uhnder's RoC), AI integration (Waveye, Zendar), and niche applications (Sensrad's industrial focus). A collaborative approach is wherein partnership with Tier 1s and OEMs (e.g., Arbe-BAIC) is accelerating market entry for new players.

Asia-Pacific is the fastest-growing region with the highest CAGR, driven by China's EV boom and government support for smart cities. Companies like SAIC and NIO integrate 4D radar (e.g., ZF's partnership with SAIC, Dec 2022). Opportunities lie in mass-market EVs and robotaxi fleets in urban centers like Shanghai. North America holds largest revenue share, led by the US with OEMs like Ford, GM, and Tesla adopting 4D radar for BlueCruise, Super Cruise, and Autopilot. Europe shows strong growth due to stringent safety regulations (e.g., EU's 2024 mandates). For instance, Mercedes-Benz and BMW lead with Level 2+/3 systems and opportunities are evidently reflected in premium vehicles and compliance-driven markets.

Market Potential

The market for SAE Level 4/5 AVs, including robotaxis and shuttles, is a key growth driver for 4D radar. By 2035, the AV segment is expected to exhibit the highest CAGR (127%) from 2025 to 2035 within the 4D radar market, driven by the need for multiple high-performance radars (6-21 per vehicle). Cruise and Waymo deploy 4D radar extensively, with fleets exceeding 1,000 vehicles in 2024, signaling commercial robotaxi services' rise. The global 4D radar market is projected to reach USD 911 million by 2035 for Level 4/5 AVs alone, with robotaxis and shuttles consuming significant radar units for urban and highway autonomy.

Opportunities include:

- Urban Mobility: High radar demand for navigating dense environments (e.g., Waveye's urban-focused radar).

- Last-Mile Delivery: Autonomous shuttles and delivery vehicles adopting 4D radar for safety.

- Regulatory Support: Mandates for AEB and CPD boost radar integration in Level 4/5 systems.

Key Questions Answered:

- How rapidly is 4D imaging radar penetrating autonomous vehicles across SAE Levels 1-5, and what are the adoption trends?

- What is the current market size and growth potential of the 4D imaging radar market for automotive applications through 2035?

- Which ADAS features (e.g., AEB, ACC, BSM) are most reliant on 4D radar, and how do they enhance safety and performance?

- How are 4D radar costs (e.g., 77 GHz, 60 GHz, 140 GHz) evolving, and what factors drive cost erosion for mass production?

- What are the challenges of integrating 4D radar with other sensors (e.g., LiDAR, cameras) for robust sensor fusion?

- How do frequency regulations (e.g., 77 GHz, 60 GHz, 140 GHz) vary globally, and what impact do they have on 4D radar deployment?

- How 4D radar's role in in-cabin monitoring applications of occupant monitoring and left-child detection is creating market opportunity?

- Which emerging startups (e.g., Arbe, Uhnder, Zendar) are disrupting the 4D radar market, and what are their unique strategies?

- What are the competitive advantages of established players (e.g., Continental, Bosch, NXP) versus emerging startups in the 4D radar market?

- How are partnerships, mergers, and acquisitions shaping the 4D radar market, and what opportunities do they create for stakeholders?

- What investment and funding trends are supporting the growth of the 4D radar market, and how can stakeholders capitalize on them?

Get answers to the most intriguing questions in the 4D imaging radar industry!

List of Companies

|

|

Table of Contents

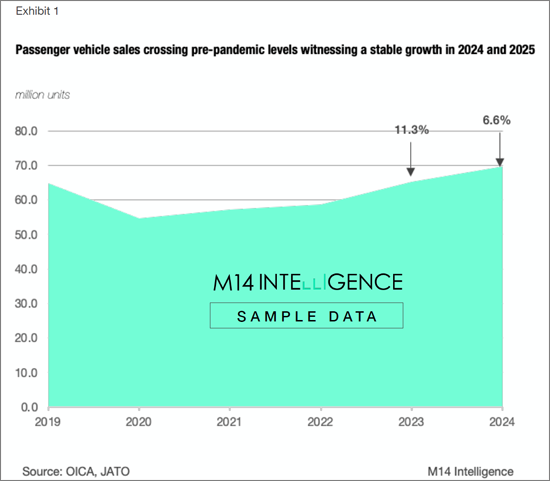

Passenger Vehicle Sales - Market Outlook

- Global Passenger Vehicle Sales, 2019-2024

- Passenger Vehicle Sales Breakdown, by Level of Automation, L1 to L5

- ADAS and Autonomous Vehicle Market sales and forecast, 2025-2035

- China dominating the market while Europe holds strong growth potential

- Urban mobility, last-mile delivery and regulatory support will be the new revenue pockets

Status of Automotive Radar Industry - Market Outlook Volume & Value, 2025-2035

- Radar Sensor requirement per vehicle

- ASP of Radar and Expected Price Erosion

- Radar Demand by Levels of Automation

- Radar Demand by Range of Operation (LRR, MRR/SRR, In-cabin)

- Radar Demand by Frequency

- Radar Market Penetration by Frequency

- Trend towards 4D Imaging Radar is Growing Rapidly

Automotive 4D Radar Industry - Market Outlook Volume & Value, 2025-2035

- 4D Radar Market - Split by Levels of Automation

- 4D Radar Market - Split by ADAS and AV Applications

- 4D Imaging Radar for Exterior Sensing Application

- 4D Imaging Radar for In-cabin Application

Automotive 4D Radar Industry - Competition Assessment

- Profiles of Emerging Companies in Automotive 4D Radar Application

- Product Comparison and Benchmarking

- Partnership Mapping and Supplier Analysis

- OEMs, Tier-1s, and Sensor Suppliers in 4D Radar Business

- Investment in R&D by leading players

- Funding and Investment Analysis of Start-ups in 4D Radar Business