4Dイメージングレーダー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

4D Imaging Radar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797813

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

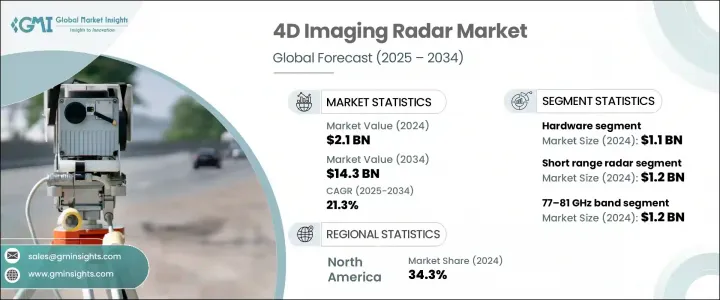

4Dイメージングレーダーの世界市場規模は、2024年に21億米ドルとなり、CAGR 21.3%で成長し、2034年には143億米ドルに達すると予測されています。

同産業は2025年から2034年にかけてCAGR 21.3%で成長すると見られています。この力強い成長の背景には、自律走行への関心の高まり、スマートモビリティソリューションの展開拡大、ADASへの投資拡大、軍事システム、無人航空機(UAV)、産業オートメーションにおける使用事例の拡大があります。4Dイメージングレーダーは、距離、仰角、速度、方位角をリアルタイムで解析できるため、セーフティ・クリティカルなアプリケーションで高い価値を発揮します。これらのレーダーは、高解像度の環境マッピング、正確な物体追跡、霧、煙、暗闇などの悪条件下での信頼性の高いパフォーマンスを可能にします。BVLOS運用への対応が進むにつれ、UAVやドローンへのこれらのシステムの統合が加速しており、より安全で自律的な飛行が可能になっています。

さらに、製造業やロジスティクスで自動化がますます推進されているため、特に視覚ベースのシステムが苦戦するような困難で動的な環境では、ロボット工学におけるレーダー強化知覚の需要が高まっています。従来の光学システムは、低照度、埃、霧、煙が充満した条件下ではしばしば限界に直面し、性能低下や安全上のリスクにつながります。これに対して4Dイメージングレーダーは、環境の制約に関係なく、高解像度の空間マッピングと物体追跡で安定した性能を発揮します。この機能は、自動フォークリフト、倉庫用ロボット、自律型配送システムなど、精度と信頼性が不可欠なアプリケーションにおいて非常に重要です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 21億米ドル |

| 予測金額 | 143億米ドル |

| CAGR | 21.3% |

2024年、ハードウェア分野は11億米ドルの評価額で世界の4Dイメージングレーダー市場をリードしました。この優位性は、アンテナアーキテクチャの躍進、特にMIMOシステムやフェーズドアレイ技術の採用によって支えられています。レーダーと、ビジョンシステムやライダーなどの補完的なセンシング技術を統合する必要性の高まりが、高度なモジュラー・ハードウェア・ソリューションの複雑さと需要に拍車をかけています。自動車やドローンベースの防衛アプリケーションの進化する需要に応えるため、ハードウェアメーカーはスケーラブルなMIMOベースのアーキテクチャと機械学習主導の校正方法に注力しています。

短距離レーダー分野は2024年に12億米ドルを生み出しました。近距離レーダーが好まれるのは、近接検知、死角監視、車載ジェスチャー認識などの機能を実現する上で重要な役割を果たすからです。同分野は、レーダー分解能とターゲット追跡能力の最近の向上から恩恵を受け、これらの小型モジュールは近距離での高精度タスクに最適です。さらに、小型化努力と効率的な電力使用により、幅広い民生用および産業用システムに簡単に組み込むことができる、コスト効率の高いレーダー・ユニットが誕生しています。

米国の4Dイメージングレーダー市場は2024年に6億4,620万米ドルを生み出し、2034年までCAGR 21%で力強い勢いを維持すると予想されます。ADAS(先進運転支援システム)の急速な展開と、大都市圏での自律走行車テストプログラムの進化が、この成長に寄与しています。次世代プラットフォームに低遅延・高精度のレーダー・システムを統合することへの注目が高まっており、技術プロバイダーはシステム・レベルでの技術革新を進めています。都市部のロボットタクシー・プログラムやフリート・オペレーターは、要求される応答時間と高い角度精度を満たすことができる4Dレーダー・ソリューションを優先しています。

4Dイメージングレーダー産業の競合情勢を形成している主な企業には、Renesas Electronics Corporation、Aptiv PLC、ZF Friedrichshafen AG、Mobileye、Robert Bosch GmbH、Infineon Technologies AG、Oculii、Texas Instruments Incorporated、Continental AG、Arbe Robotics Ltd.、Hella Aglaia Mobile Vision GmbH、Metawave Corporation、NXP Semiconductors、Ainstein、Vayyar Imaging Ltd.などがあります。これらの主要企業は、さまざまなモビリティとオートメーションのエコシステムにわたって、技術革新をリードし、レーダー統合のための将来の標準を形成し続けています。4Dイメージングレーダー市場の主要企業は、特にAI主導の信号処理、スケーラブルなハードウェアモジュール、適応ビームフォーミング技術への戦略的研究開発投資を通じて、システム能力の向上に注力しています。市場への浸透を強化するため、企業は自動車OEM、UAVメーカー、ロボット企業と業界横断的な提携を結び、レーダー・ソリューションを新たなモビリティ・プラットフォームに統合しようとしています。短距離ロボット工学や長距離防衛アプリケーションなど、用途固有のニーズに合わせたカスタマイズは、ベンダーの差別化に役立っています。IPポートフォリオを拡大し、市場投入までの時間を短縮するために、M&Aも活用されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- 影響要因

- 促進要因

- 新しい電子機器の価格上昇

- 持続可能性と電子廃棄物に関する懸念

- 家電製品の拡大

- 産業機器および医療機器の使用の増加

- サードパーティ修理業者の成長

- 業界の潜在的リスク&課題

- 急速な技術陳腐化

- OEM部品およびツールへのアクセスが制限される

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 消費者感情分析

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 市場集中分析

- 地域別

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- トランシーバーモジュール

- アンテナおよびビームフォーミングユニット

- 信号プロセッサ

- その他

- ソフトウェア

- 物体検出ソフトウェア

- センサーフュージョンソフトウェア

- レーダー画像およびマッピングソフトウェア

- その他

- サービス

第6章 市場推計・予測:レーダー距離別、2021年~2034年

- 主要動向

- 短距離レーダー

- 中距離レーダー

- 長距離レーダー

第7章 市場推計・予測:周波数帯域別、2021年~2034年

- 主要動向

- 24GHz帯

- 60GHz帯

- 77~81GHz帯

- その他

第8章 市場推計・予測:展開プラットフォーム別、2021年~2034年

- 主要動向

- 地上車両

- 乗用車

- 商用車

- その他

- 高所作業車

- ドローンと無人航空機

- 有人航空機

- 海洋プラットフォーム

- 海軍艦艇

- 商船

- その他

- その他

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ADAS(先進運転支援システム)(ADAS)

- 監視とセキュリティ

- 産業オートメーション

- スマートインフラ

- ヘルスケアモニタリング

- その他

第10章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 自動車

- 航空宇宙および防衛

- ヘルスケア

- 産業

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- 世界の主要企業

- Aptiv PLC

- Continental AG

- NXP Semiconductors

- Texas Instruments Incorporated

- ZF Friedrichshafen AG

- 地域の主要企業

- 北米

- Mobileye (Intel)

- Uhnder

- Magna International

- 欧州

- Hella Aglaia Mobile Vision GmbH

- Robert Bosch GmbH

- Infineon Technologies AG

- アジア太平洋地域

- Renesas Electronics Corporation

- Huawei

- Smart Radar System

- 北米

- ディスラプター/ニッチ企業

- Ainstein

- Arbe Robotics Ltd.

- Metawave Corporation

- Oculii

- Vayyar Imaging Ltd.

目次

The Global 4D Imaging Radar Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 21.3% to reach USD 14.3 billion by 2034. The industry is set to grow at a CAGR of 21.3% between 2025 and 2034. This robust growth is fueled by rising interest in autonomous driving, increased deployment of smart mobility solutions, expanded investment in ADAS, and widening use cases in military systems, unmanned aerial vehicles (UAVs), and industrial automation. The ability of 4D imaging radar to deliver real-time analysis of range, elevation, velocity, and azimuth makes it highly valuable for safety-critical applications. These radars enable high-resolution environmental mapping, precise object tracking, and reliable performance in adverse visibility conditions like fog, smoke, or darkness. Increasing support for BVLOS operations is accelerating the integration of these systems in UAVs and drones, allowing for safer and more autonomous flights.

Moreover, the increasing push toward automation across manufacturing and logistics is driving demand for radar-enhanced perception in robotics, especially in challenging, dynamic environments where vision-based systems struggle. Traditional optical systems often face limitations in low-light, dusty, foggy, or smoke-filled conditions, leading to performance drops and safety risks. In contrast, 4D imaging radar delivers consistent performance with high-resolution spatial mapping and object tracking, regardless of environmental constraints. This capability is critical in applications such as automated forklifts, warehouse robots, and autonomous delivery systems, where precision and reliability are essential.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 billion |

| Forecast Value | $14.3 billion |

| CAGR | 21.3% |

In 2024, the hardware segment led the global 4D imaging radar market with a valuation of USD 1.1 billion. This dominance is supported by breakthroughs in antenna architecture, particularly the adoption of MIMO systems and phased array technologies, which significantly boost range, precision, and detection clarity. The growing need to integrate radar with complementary sensing technologies, such as vision systems and lidar, is adding to the complexity and demand for advanced modular hardware solutions. To cater to the evolving demands of automotive and drone-based defense applications, hardware manufacturers are focusing on scalable MIMO-based architectures and machine-learning-driven calibration methods.

The short-range radar segment generated USD 1.2 billion in 2024. The preference for short-range radar is driven by its critical role in enabling features such as proximity detection, blind spot monitoring, and in-vehicle gesture recognition. The segment benefits from recent improvements in radar resolution and target tracking capabilities, making these compact modules ideal for high-precision tasks at close distances. Additionally, miniaturization efforts and efficient power usage have resulted in cost-effective radar units that are easily embedded into a wide array of consumer and industrial systems.

U.S. 4D Imaging Radar Market generated USD 646.2 million in 2024 and is expected to maintain strong momentum at a CAGR of 21% throughout 2034. Rapid deployment of advanced driver-assistance systems and evolving autonomous vehicle testing programs across major metropolitan areas are contributing to this growth. The increasing focus on integrating low-latency and high-accuracy radar systems in next-generation platforms is pushing technology providers to innovate at the system level. Urban robotaxi programs and fleet operators are prioritizing 4D radar solutions capable of meeting demanding response times and high angular accuracy.

Major players shaping the competitive landscape of the 4D Imaging Radar Industry include Renesas Electronics Corporation, Aptiv PLC, ZF Friedrichshafen AG, Mobileye, Robert Bosch GmbH, Infineon Technologies AG, Oculii, Texas Instruments Incorporated, Continental AG, Arbe Robotics Ltd., Hella Aglaia Mobile Vision GmbH, Metawave Corporation, NXP Semiconductors, Ainstein, and Vayyar Imaging Ltd. These companies continue to lead innovation and shape future standards for radar integration across a variety of mobility and automation ecosystems. Leading companies in the 4D imaging radar market are focusing on advancing system capabilities through strategic R&D investments, especially in AI-driven signal processing, scalable hardware modules, and adaptive beamforming techniques. To enhance market penetration, firms are forming cross-industry alliances with automotive OEMs, UAV manufacturers, and robotics companies to integrate radar solutions into new mobility platforms. Customization for use-specific needs, such as short-range robotics or long-range defense applications, helps vendors differentiate. Mergers and acquisitions are also being leveraged to expand IP portfolios and accelerate time-to-market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Radar range trends

- 2.2.3 Frequency band trends

- 2.2.4 Deployment platform trends

- 2.2.5 Application trends

- 2.2.6 End use trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising cost of new electronics

- 3.2.1.2 Sustainability and e-waste concerns

- 3.2.1.3 Expansion of consumer electronics

- 3.2.1.4 Increasing industrial and medical device usage

- 3.2.1.5 Growth of third-party repair providers

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Rapid technological obsolescence

- 3.2.2.2 Limited access to OEM parts and tools

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Sustainability measures

- 3.11 Consumer sentiment analysis

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Transceiver modules

- 5.2.2 Antenna & beamforming units

- 5.2.3 Signal processors

- 5.2.4 Others

- 5.3 Software

- 5.3.1 Object detection software

- 5.3.2 Sensor fusion software

- 5.3.3 Radar imaging & mapping software

- 5.3.4 Others

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Radar Range, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Short-range radar

- 6.3 Medium-range radar

- 6.4 Long-range radar

Chapter 7 Market Estimates & Forecast, By Frequency Band, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 24 GHz band

- 7.3 60 GHz band

- 7.4 77-81 GHz band

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Deployment Platform, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Ground Vehicles

- 8.2.1 Passenger Vehicles

- 8.2.2 Commercial Vehicles

- 8.2.3 Others

- 8.3 Aerial Platforms

- 8.3.1 Drones & UAVs

- 8.3.2 Manned Aircraft

- 8.4 Marine Platforms

- 8.4.1 Naval Vessels

- 8.4.2 Commercial Ships

- 8.4.3 Others

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 Advanced driver assistance systems (ADAS)

- 9.3 Surveillance & security

- 9.4 Industrial automation

- 9.5 Smart infrastructure

- 9.6 Healthcare monitoring

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion)

- 10.1 Key trends

- 10.2 Automotive

- 10.3 Aerospace and Defense

- 10.4 Healthcare

- 10.5 Industrial

- 10.6 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Aptiv PLC

- 12.1.2 Continental AG

- 12.1.3 NXP Semiconductors

- 12.1.4 Texas Instruments Incorporated

- 12.1.5 ZF Friedrichshafen AG

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 Mobileye (Intel)

- 12.2.1.2 Uhnder

- 12.2.1.3 Magna International

- 12.2.2 Europe

- 12.2.2.1 Hella Aglaia Mobile Vision GmbH

- 12.2.2.2 Robert Bosch GmbH

- 12.2.2.3 Infineon Technologies AG

- 12.2.3 Asia-Pacific

- 12.2.3.1 Renesas Electronics Corporation

- 12.2.3.2 Huawei

- 12.2.3.3 Smart Radar System

- 12.2.1 North America

- 12.3 Disruptors / Niche Players

- 12.3.1 Ainstein

- 12.3.2 Arbe Robotics Ltd.

- 12.3.3 Metawave Corporation

- 12.3.4 Oculii

- 12.3.5 Vayyar Imaging Ltd.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日