|

|

市場調査レポート

商品コード

1397880

患者エンゲージメントソリューションの世界市場:コンポーネント別、ソフトウェア別、治療別、機能別、ユーザー別、アンメットニーズ、投資、購入基準 - 予測(~2028年)Patient Engagement Solutions Market by Component (Hardware), Software, Therapy, Functionality, User (Provider, Payer), Unmet Need, Investment, Buying Criteria - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 患者エンゲージメントソリューションの世界市場:コンポーネント別、ソフトウェア別、治療別、機能別、ユーザー別、アンメットニーズ、投資、購入基準 - 予測(~2028年) |

|

出版日: 2023年12月15日

発行: MarketsandMarkets

ページ情報: 英文 438 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

レポートの概要

| 調査範囲 | |

|---|---|

| 調査対象年 | 2021年~2028年 |

| 基準年 | 2022年 |

| 予測期間 | 2023年~2028年 |

| 単位 | 金額(100万米ドル) |

| セグメント | コンポーネント、デリバリー方式、治療領域、用途、機能、エンドユーザー、地域 |

| 対象地域 | 北米、欧州、アジア太平洋、ラテンアメリカ、中東・アフリカ |

世界の患者エンゲージメントソリューションの市場規模は、2023年に225億米ドル、2028年までに418億米ドルに達し、予測期間にCAGRで13.2%の成長が見込まれています。

患者エンゲージメントソリューションに対する需要の高まりや、モバイルヘルスアプリの利用の増加などの要因が、市場成長を促進しています。

しかし、医療インフラへの高い投資要件や、医療業界における熟練したIT専門家の不足が、予測期間に市場の成長を抑制する見込みです。

「サービスセグメントが2023年~2028年にもっとも高い成長率で伸びると予測されます。」

ソフトウェアセグメントが2022年に市場で最大のシェアを占めています。統合ソリューションセグメントが2022年に市場で大きなシェアを占め、また予測期間にもっとも高いCAGRで成長する見込みです。

とはいえ、サービスセグメントが2023年~2028年にもっとも高いCAGRを示すと予測されています。サービスセグメントの顕著な成長は、価値ベースの患者中心のケアを提供する革新的なサービスモデルの開発への投資が増加し、市場成長を促進していることなどに起因すると考えられます。

「オンプレミスソリューションセグメントが2023年に市場を独占すると予測されます。」

オンプレミスソリューションセグメントが2023年に市場で最大のシェアを占めると予測されています。しかし、2023年~2028年に、クラウドベース/Webベース方式セグメントがもっとも高いCAGRを示すと予測されています。このセグメントの大きなシェアは、市場における、クラウドベースソリューション固有の柔軟性、拡張性、手頃な価格という特徴によってもたらされる成長支援によるものと考えられます。

「2022年、用途別では健康管理セグメントが市場で最大のシェアを占めました。」

2023年、健康管理用途セグメントが市場で最大のシェアを占めます。健康状態に関する患者の意識の高まりが市場成長の促進要因となっています。

「2022年、治療領域別では慢性疾患が市場で最大のシェアを占めました。」

2022年、慢性疾患セグメントが市場を独占し、慢性疾患のうち心血管疾患セグメントが市場で最大のシェアを占めました。しかし、世界中で糖尿病の有病率と発症率が高いことから、糖尿病セグメントが予測期間にもっとも高いCAGRを記録する見込みです。

「機能別では患者/クライアントスケジューリングが市場で最大シェアを占めました。」

機能別では、患者/クライアントスケジューリングセグメントが2022年に市場で最大のシェアを占めています。患者/クライアントスケジューリングセグメントの大きなシェアは主に、医師による質の高い治療を低コストで患者に提供するための、患者エンゲージメントソフトウェアの採用を促進する政府の取り組みの増加に起因しています。

「エンドユーザー別では、提供者セグメントが2022年に最大のシェアを占めました。」

このセグメントの大きなシェアは、増大する医療コストを抑制し、価値ベースのケアを提供し、財務上の成果を拡大するための患者エンゲージメントソリューションの導入の増加によるものです。

「2022年、北米が患者エンゲージメントソリューション市場を独占する」

有利な政府の取り組みと規制、医療コストを削減する必要性、慢性疾患の増加、主要市場企業のプレゼンスなどの要因が、北米市場の成長に大きく寄与しています。

アジア太平洋市場は、2023年~2028年の予測期間にもっとも高いCAGRを達成する見込みです。この成長は、医療IT(HCIT)ソリューションの採用の拡大や、同地域における慢性疾患の流行に起因しています。患者数の増加と、正確でタイムリーな診断と治療に対するニーズの高まりは、予測されるアジア太平洋市場の成長にさらに寄与します。

当レポートでは、世界の患者エンゲージメントソリューション市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 患者エンゲージメントソリューション市場の企業にとって魅力的な機会

- 北米の患者エンゲージメントソリューション市場:デリバリー方式別、国別(2022年)

- 患者エンゲージメントソリューション市場:地理的な成長機会

- 患者エンゲージメントソリューション市場:地域の構成

- 患者エンゲージメントソリューション市場:先進国 VS. 新興経済国

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- クライアントのビジネスに影響を与える動向/混乱

- 産業動向

- エコシステム分析

- バリューチェーン分析

- 研究開発

- 材料となるコンポーネント

- メーカー、開発者

- 流通、販売

- 最終用途産業

- 販売後サービス

- 技術分析

- AI、ML

- VR、AR

- 遠隔モニタリング機器、ウェアラブル

- 関税と規制の分析

- 規制機関、政府機関、その他の組織

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 価格分析

- 価格の概要

- 主要企業の平均販売価格の動向:用途別

- 患者エンゲージメントソリューションの参考価格分析

- 貿易分析

- ポーターのファイブフォース分析

- 特許分析

- 主なステークホルダーと購入基準

- エンドユーザー分析

- アンメットニーズ

- エンドユーザーの期待

- 主な会議とイベント(2023年~2024年)

- 患者エンゲージメントソリューションの置換動向

- 患者エンゲージメントソリューションへの投資情勢

- 患者エンゲージメントソリューションのビジネスモデル

- 使用事例/ケーススタディ

第6章 患者エンゲージメントソリューション市場:コンポーネント別

- イントロダクション

- ハードウェア

- ソフトウェア

- サービス

第7章 患者エンゲージメントソリューション市場:デリバリー方式別

- イントロダクション

- オンプレミスモード

- クラウドベース/ウェブベース方式

第8章 患者エンゲージメントソリューション市場:用途別

- イントロダクション

- 健康管理

- 家庭健康管理

- 社会・行動管理

- 財務健全性管理

第9章 患者エンゲージメントソリューション市場:治療領域別

- イントロダクション

- 慢性疾患

- 心血管疾患(CVD)

- 糖尿病

- 肥満

- その他の慢性疾患

- ウィメンズヘルス

- フィットネス

- その他の治療領域

第10章 患者エンゲージメントソリューション市場:機能別

- イントロダクション

- 患者/クライアントスケジューリング

- 遠隔医療

- 電子処方

- 文書管理

- 請求・決済

- 患者教育

- その他の機能

第11章 患者エンゲージメントソリューション市場:エンドユーザー別

- イントロダクション

- 提供者

- 保険者

- 患者

- その他のエンドユーザー

第12章 患者エンゲージメントソリューション市場:地域別

- イントロダクション

- 北米

- 景気後退の影響

- 米国

- カナダ

- 欧州

- 景気後退の影響

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 景気後退の影響

- 日本

- 中国

- インド

- その他のアジア太平洋

- ラテンアメリカ

- 景気後退の影響

- ブラジル

- メキシコ

- その他のラテンアメリカ

- 中東・アフリカ

- 景気後退の影響

- GCC諸国

- その他の中東・アフリカ

第13章 競合情勢

- 概要

- 主要企業戦略/有力企業

- 収益分析

- 市場シェア分析

- 企業の評価マトリクス

- スタートアップ/中小企業の評価マトリクス

- 競合状況、動向

第14章 企業プロファイル

- 主要企業

- MCKESSON CORPORATION

- ORACLE CORPORATION

- VERADIGM LLC

- ATHENAHEALTH

- ORION HEALTH

- GETWELLNETWORK, INC.

- LINCOR INC.

- COGNIZANT TECHNOLOGY SOLUTIONS CORPORATION

- GET REAL HEALTH

- ONEVIEW HEALTHCARE

- ADVANCEDMD, INC.

- EPIC SYSTEMS CORPORATION

- HARRIS HEALTHCARE

- MEDICAL INFORMATION TECHNOLOGY, INC.

- その他の企業

- KAREO, INC.

- ECLINICAL WORKS

- WELLSTACK

- IQVIA HOLDINGS INC.

- VIVIFY HEALTH

- MEDHOST

- LUMA HEALTH

- CUREMD HEALTHCARE

- SONIFI HEALTH

- ADVANTECH CO., LTD.

- BARCO

第15章 付録

Report Description

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2028 |

| Base Year | 2022 |

| Forecast Period | 2023-2028 |

| Units Considered | Value (USD) Million |

| Segments | Component, Delivery Mode, Therapeutic Area, Application, Functionality, End User, And Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America and Middle East & Africa |

The patient engagement solutions market is projected to reach USD 41.8 billion by 2028 from USD 22.5 billion in 2023, at a CAGR of 13.2% during the forecast period. Factors such as the growing demand for patient engagement solutions and the increasing utilization of m-health apps are driving the market growth.

However, high investment requirements for healthcare infrastructure and the scarcity of skilled IT professionals in the healthcare industry are expected to restrain the growth of this market during the forecast period.

"Services segment is expected to grow at the highest rate from 2023 to 2028."

By components, the patient engagement solutions market is divided into software, hardware, and services. The software segment holds the largest share of the global patient engagement solutions market in 2022. The hardware is further segmented into in-room televisions, integrated bedside terminals/assisted devices and tablets. The software market is further divided into standalone software and integrated software. In 2022, the integrated solutions segment holds the larger share of this market & is also projected to grow at the highest CAGR during the forecast period.

Nevertheless, the services segment is projected to exhibit the highest CAGR from 2023 to 2028. The notable growth in the services segment can be attributed to factors such as the increasing investments in the development of innovative service models that offer value-based, patient-centered care, driving the market growth for services.

"The on-premise solutions segment is anticipated to dominate the Patient Engagement Solutions market in 2023."

When considering delivery modes, the patient engagement solutions market is categorized into on-premise and cloud-based/web-based modes. In 2023, it is projected that the on-premise solutions segment will command the largest share of the global patient engagement solutions market. However, the cloud-based/web-based mode segment is forecasted to exhibit the highest CAGR from 2023 to 2028. The substantial share of this segment can be attributed to the growth support provided by the flexibility, scalability, and affordability features inherent in cloud-based solutions within the patient engagement solutions market.

"In 2022, the Health management segment accounted for the largest share of the global patient engagement solutions market, by applications."

By application, the patient engagement solutions market is divided into health management, home health management, social and behavioral management, and financial health management. In 2023, the health management applications segment accounts for the largest share of the global patient engagement solutions market. Health management includes a wide range of patient engagement tools that help patients engage with their providers and take initiatives to improve or maintain their health status and increased awareness among patients about health conditions are the factors driving market growth.

"In 2022, Chronic diseases accounted for the largest share of the global patient engagement solutions market by therapeutic area."

By therapeutic area, the patient engagement solutions market is divided into chronic diseases (cardiovascular disease, diabetes, obesity and other chronic diseases), women's health, fitness, and other therapeutic areas. The chronic diseases segment dominated this market in 2022. In 2022, the cardiovascular diseases segment accounted for the largest share of the patient engagement solutions market for chronic diseases. However, the diabetes segment is projected to register the highest CAGR during the forecast period, owing to the high prevalence and incidence of diabetes worldwide.

"Patient/client scheduling accounted for the largest share of the global patient engagement solutions market, by functionality."

By functionality, the patient engagement solutions market is divided into E-prescribing, document management, telehealth, patient/client scheduling, patient education, billing & payments and other functionalities. The patient/client scheduling segment accounted for the largest share of the patient engagement solutions market, by functionality, in 2022. The large share of the patient/client scheduling segment is mainly attributed to increasing government initiatives to boost patient engagement software adoption to provide quality care by physicians to their patients at lower costs.

"Providers' segment accounted for the largest share of the global patient engagement solutions market by end user in 2022."

By end users, the patient engagement solutions market is divided into providers, payers, patients, and other end users. The providers are further bifurcated into hospitals and healthcare systems, ambulatory care centers, home healthcare, and other providers. Moreover, the payers are further divided into private and public. By end users, the providers segment accounted for the largest share of the global patient engagement solutions market in 2022. The large share of this segment is due to the increasing implementation of patient engagement solutions to curtail mounting healthcare costs, offer value-based care, and expand financial outcomes are factors that are driving the growth of this segment.

"North America to dominate the patient engagement solutions market in 2022."

In 2022, North America dominated the global patient engagement solutions market by region. Factors such as favorable government initiatives and regulations, the imperative to reduce healthcare costs, the increasing prevalence of chronic diseases, and the presence of key market players contribute significantly to the growth of the patient engagement solutions market in North America.

The Asia Pacific market is expected to achieve the highest CAGR during the forecast period from 2023 to 2028. This growth is attributed to the escalating adoption of Healthcare Information Technology (HCIT) solutions and the increasing prevalence of chronic diseases in the region. The rising patient volume and the growing need for accurate and timely diagnosis and treatment further contribute to the anticipated growth of the patient engagement solutions market in the Asia Pacific region.

Breakdown of supply-side primary interviews by company type, designation, and region:

- By Company Type: Tier 1 (45%), Tier 2 (30%), and Tier 3 (25%)

- By Designation: C-level (44%), Director-level (35%), and Others (21%)

- By Region: North America (46%), Europe (26%), Asia Pacific (18%), Latin America (7%), and Middle East & Africa (10%)

McKesson Corporation (US), Veradigm (US), Oracle Corporation (US), Merative (US), Epic Systems Corporation (US), Orion Health (New Zealand), GetWellNetwork (US), athenahealth (US), Oneview Healthcare (Ireland), MEDITECH (US), IQVIA (US), Get Real Health (US), Cognizant (US), Harris Healthcare (US), Kareo (US), CureMD Healthcare (US), eClinicalWorks (US), and Lincor Solutions (US), AdvancedMD (US), Luma Health Inc. (US), WellStack(US), Vivify Health (US), Medhost (US), MEDISYSINC (US), and Patient point LLC (US). These players are increasingly focusing on new product launches and partnerships to expand their product offerings in the patient engagement solutions market.

Research Coverage

- The report studies the Patient Engagement Solutions market based on component, delivery mode, therapeutic area, application, functionality, end user, and region.

- The report analyzes factors (such as drivers, restraints, opportunities, and challenges) affecting the market growth.

- The report evaluates the opportunities and challenges in the market for stakeholders and provides details of the competitive landscape for market leaders.

- The report studies micro-markets with respect to their growth trends, prospects, and contributions to the total patient engagement solutions market.

- The report forecasts the revenue of market segments with respect to five majors regions.

Reasons to Buy the Report

- This report will enrich established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the below-mentioned strategies to strengthen their positions in the market.

This report provides insights on:

- Analysis of key drivers (implementation of government regulations and initiatives to promote patient centric care, increasing adoption of patient engagement solutions, rising number of collaborations and partnerships between stakeholders, increasing utilization of mobile health apps), restraints (large investment requirement for healthcare infrastructure, protection of patient information, inadequate interoperability across healthcare providers and shortage of skilled IT professionals in the healthcare industry ), opportunities (growth opportunities in emerging markets, wearable health technology, cloud computing solutions), and challenges (high deployment cost of healthcare IT systems, low levels of healthcare literacy) impacting the growth of the Telehealth and Telemedicine market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the patient engagement solutions market.

- Market Development: Comprehensive information on the lucrative emerging markets, components, delivery mode, therapeutic area, application, functionality, end user, and region

- Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the patient engagement solutions market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, company evaluation quadrant, and capabilities of leading players in the global Patient Engagement Market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 PATIENT ENGAGEMENT SOLUTIONS MARKET: INCLUSIONS & EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 REGIONAL SEGMENTATION

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

- 1.7 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY RESEARCH

- 2.1.3 PRIMARY SOURCES

- 2.1.4 KEY DATA FROM PRIMARY SOURCES

- 2.1.5 KEY INDUSTRY INSIGHTS

- FIGURE 2 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- 2.2 MARKET SIZE ESTIMATION METHODOLOGY

- FIGURE 3 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- 2.3 MARKET ESTIMATION

- 2.3.1 RESEARCH METHODOLOGY: MARKET ESTIMATION

- 2.3.2 APPROACH: END USER-BASED MARKET ESTIMATION

- FIGURE 4 RESEARCH METHODOLOGY: MARKET ESTIMATION

- 2.3.3 TOP-DOWN APPROACH: CONTRIBUTION-BASED MARKET SIZE ESTIMATION

- 2.3.4 TOP-DOWN APPROACH

- 2.3.5 BOTTOM-UP APPROACH

- FIGURE 5 CAGR PROJECTIONS FROM ANALYSIS OF DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN PATIENT ENGAGEMENT SOLUTIONS MARKET (2023-2028)

- FIGURE 6 CAGR PROJECTIONS: SUPPLY-SIDE ANALYSIS

- 2.4 MARKET DATA ESTIMATION AND TRIANGULATION

- FIGURE 7 DATA TRIANGULATION METHODOLOGY

- 2.5 ASSUMPTIONS

- 2.6 LIMITATIONS

- 2.6.1 SCOPE-RELATED LIMITATIONS

- 2.6.2 METHODOLOGY-RELATED LIMITATIONS

- 2.7 RISK ASSESSMENT

- TABLE 1 RISK ASSESSMENT: PATIENT ENGAGEMENT SOLUTIONS MARKET

- 2.8 PATIENT ENGAGEMENT SOLUTIONS MARKET: RECESSION IMPACT

3 EXECUTIVE SUMMARY

- FIGURE 8 SOFTWARE TO BE LARGEST SEGMENT DURING FORECAST PERIOD

- FIGURE 9 CLOUD-BASED/WEB-BASED MODE TO REGISTER HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 10 HEALTH MANAGEMENT TO DOMINATE PATIENT ENGAGEMENT SOLUTIONS MARKET DURING FORECAST PERIOD

- FIGURE 11 PROVIDER TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 12 GEOGRAPHICAL SNAPSHOT OF PATIENT ENGAGEMENT SOLUTIONS MARKET

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PATIENT ENGAGEMENT SOLUTIONS MARKET

- FIGURE 13 GOVERNMENT INITIATIVES FOR PATIENT-CENTRIC CARE TO DRIVE MARKET

- 4.2 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE & COUNTRY (2022)

- FIGURE 14 ON-PREMISE MODE ACCOUNTED FOR LARGEST SHARE OF NORTH AMERICAN MARKET IN 2022

- 4.3 PATIENT ENGAGEMENT SOLUTIONS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- FIGURE 15 ASIA PACIFIC TO REGISTER HIGHEST GROWTH RATE DURING FORECAST PERIOD

- 4.4 PATIENT ENGAGEMENT SOLUTIONS MARKET: REGIONAL MIX

- FIGURE 16 ASIA PACIFIC MARKET TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- 4.5 PATIENT ENGAGEMENT SOLUTIONS MARKET: DEVELOPED VS. EMERGING ECONOMIES

- FIGURE 17 EMERGING ECONOMIES TO REGISTER HIGHER GROWTH RATE DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 18 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN PATIENT ENGAGEMENT SOLUTIONS MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Implementation of government regulations and initiatives to promote patient-centric care

- 5.2.1.2 Increasing adoption of patient engagement solutions

- 5.2.1.3 Rising number of collaborations and partnerships between stakeholders

- TABLE 2 INDICATIVE LIST OF COLLABORATIONS BETWEEN ORGANIZATIONS FROM 2020 TO 2023

- 5.2.1.4 Increasing utilization of mobile health apps

- 5.2.1.5 Rising geriatric population and subsequent increase in prevalence of chronic diseases

- FIGURE 19 GERIATRIC POPULATION, BY REGION, 2010-2030 (% OF TOTAL POPULATION)

- 5.2.2 RESTRAINTS

- 5.2.2.1 Large investment requirements for healthcare infrastructure

- 5.2.2.2 Protection of patient information

- FIGURE 20 HEALTHCARE BREACHES REPORTED TO US DEPARTMENT OF HEALTH AND HUMAN SERVICES IN 2021

- 5.2.2.3 Inadequate interoperability across healthcare providers

- 5.2.2.4 Shortage of skilled IT professionals in healthcare industry

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growth opportunities in emerging markets

- 5.2.3.2 Wearable health technology

- 5.2.3.3 Cloud-computing solutions

- 5.2.4 CHALLENGES

- 5.2.4.1 High deployment costs of healthcare IT systems

- 5.2.4.2 Low levels of healthcare literacy

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 21 REVENUE SHIFTS AND NEW REVENUE POCKETS FOR PATIENT ENGAGEMENT SOLUTIONS MARKET

- 5.4 INDUSTRY TRENDS

- 5.4.1 AI-DRIVEN DIGITAL TRANSFORMATION TO DRIVE NEXT WAVE OF PATIENT ENGAGEMENT

- 5.4.2 REAL-TIME REMOTE DIAGNOSIS TO BE INTEGRAL PART OF PATIENT ENGAGEMENT

- 5.4.3 ROLE OF MHEALTH IN PATIENT ENGAGEMENT

- 5.4.4 GROWING ADOPTION OF TELEMEDICINE

- 5.4.5 RISE OF SMART HOSPITAL ROOMS AND BEDSIDE TABLETS

- 5.4.6 GROWING DEMAND FOR VALUE-BASED HEALTHCARE

- 5.5 ECOSYSTEM ANALYSIS

- FIGURE 22 PATIENT ENGAGEMENT SOLUTIONS MARKET: ECOSYSTEM ANALYSIS

- 5.6 VALUE CHAIN ANALYSIS

- 5.6.1 RESEARCH AND DEVELOPMENT

- 5.6.2 MATERIAL COMPONENTS

- 5.6.3 MANUFACTURERS AND DEVELOPERS

- 5.6.4 DISTRIBUTION AND SALES

- 5.6.5 END-USER INDUSTRIES

- 5.6.6 POST-SALE SERVICES

- FIGURE 23 PATIENT ENGAGEMENT SOLUTIONS MARKET: VALUE CHAIN ANALYSIS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 ARTIFICIAL INTELLIGENCE (AI) AND MACHINE LEARNING (ML)

- 5.7.2 VIRTUAL REALITY (VR) AND AUGMENTED REALITY (AR)

- 5.7.3 REMOTE MONITORING DEVICES AND WEARABLES

- 5.8 TARIFF AND REGULATORY ANALYSIS

- 5.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 3 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 4 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 5 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 6 REST OF THE WORLD: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.8.2 NORTH AMERICA

- 5.8.2.1 US

- 5.8.2.1.1 Health Insurance Portability and Accountability Act of 1996 (HIPAA)

- 5.8.2.1.2 Health Information Technology for Economic and Clinical Health Act of 2009 (HITECh)

- 5.8.2.1.3 Consumer Privacy Protection Act of 2017

- 5.8.2.1.4 Affordable Care Act, 2010

- 5.8.2.2 Canada

- 5.8.2.2.1 Personal Information Protection and Electronic Documents Act (PIPEDA)

- 5.8.2.1 US

- 5.8.3 EUROPE

- 5.8.3.1 General Data Protection Regulation (GDPR), European Union (EU)

- 5.8.3.2 EU Cybersecurity Act

- 5.8.3.3 Germany

- 5.8.3.3.1 German Data Protection Act (Bundesdatenschutzgesetz, BDSG)

- 5.8.3.4 France

- 5.8.3.4.1 French Data Protection Act

- 5.8.3.5 Italy

- 5.8.3.5.1 Personal Data Protection Code (Legislative Decree 196/2003)

- 5.8.4 ASIA PACIFIC

- 5.8.4.1 China

- 5.8.4.1.1 Cybersecurity Law of People's Republic of China

- 5.8.4.2 Japan

- 5.8.4.2.1 Act on Protection of Personal Information (APPI)

- 5.8.4.3 India

- 5.8.4.3.1 The Information Technology Act, 2000

- 5.8.4.1 China

- 5.8.5 LATIN AMERICA

- 5.8.5.1 Protection of Personal Information Act

- 5.8.6 MIDDLE EAST & AFRICA

- 5.8.6.1 Private Cloud Computing Regulatory Framework

- 5.9 PRICING ANALYSIS

- 5.9.1 PRICING OVERVIEW

- FIGURE 24 PATIENT ENGAGEMENT SOLUTIONS MARKET: PRICING COMPONENTS

- 5.9.2 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION

- FIGURE 25 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION

- TABLE 7 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION

- 5.9.3 INDICATIVE PRICING ANALYSIS OF PATIENT ENGAGEMENT SOLUTIONS

- TABLE 8 INDICATIVE PRICING ANALYSIS OF PATIENT ENGAGEMENT SOLUTIONS

- 5.10 TRADE ANALYSIS

- FIGURE 26 EXPORT DATA FOR HS CODE 854231 FOR TOP COUNTRIES IN PATIENT ENGAGEMENT SOLUTIONS MARKET, 2022 (USD THOUSAND)

- FIGURE 27 IMPORT DATA FOR HS CODE 854231 FOR TOP COUNTRIES IN PATIENT ENGAGEMENT SOLUTIONS MARKET, 2022 (USD THOUSAND)

- 5.11 PORTER'S FIVE FORCES ANALYSIS

- TABLE 9 PATIENT ENGAGEMENT SOLUTIONS MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.11.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.11.2 BARGAINING POWER OF SUPPLIERS

- 5.11.3 BARGAINING POWER OF BUYERS

- 5.11.4 THREAT OF NEW ENTRANTS

- 5.11.5 THREAT OF SUBSTITUTES

- 5.12 PATENT ANALYSIS

- 5.12.1 PATENT PUBLICATION TRENDS FOR PATIENT ENGAGEMENT SOLUTIONS

- FIGURE 28 PATENT PUBLICATION TRENDS (JANUARY 2012-NOVEMBER 2023)

- 5.12.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- FIGURE 29 TOP APPLICANTS AND OWNERS (COMPANIES/INSTITUTES) FOR PATIENT ENGAGEMENT SOLUTIONS (JANUARY 2012-NOVEMBER 2023)

- FIGURE 30 TOP APPLICANT COUNTRIES/REGIONS FOR PATIENT ENGAGEMENT SOLUTIONS PATENTS DOCUMENTS

- TABLE 10 PATIENT ENGAGEMENT SOLUTIONS MARKET: LIST OF MAJOR PATENTS

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- TABLE 11 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR PATIENT ENGAGEMENT SOLUTIONS

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR PATIENT ENGAGEMENT SOLUTIONS

- TABLE 12 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS (%) FOR PATIENT ENGAGEMENT SOLUTIONS

- 5.13.2 BUYING CRITERIA

- FIGURE 32 KEY BUYING CRITERIA FOR PATIENT ENGAGEMENT SOLUTIONS

- TABLE 13 KEY BUYING CRITERIA FOR PATIENT ENGAGEMENT SOLUTION COMPONENTS

- 5.14 END USER ANALYSIS

- 5.14.1 UNMET NEEDS

- TABLE 14 UNMET NEEDS IN PATIENT ENGAGEMENT SOLUTIONS MARKET

- 5.14.2 END USER EXPECTATIONS

- TABLE 15 END USER EXPECTATIONS IN PATIENT ENGAGEMENT SOLUTIONS MARKET

- 5.15 KEY CONFERENCES & EVENTS IN 2023-2024

- TABLE 16 PATIENT ENGAGEMENT SOLUTIONS: DETAILED LIST OF CONFERENCES & EVENTS

- 5.16 REPLACEMENT TRENDS FOR PATIENT ENGAGEMENT SOLUTIONS

- 5.17 PATIENT ENGAGEMENT SOLUTIONS INVESTMENT LANDSCAPE

- FIGURE 33 INVESTOR DEALS AND FUNDING IN PATIENT ENGAGEMENT SOLUTIONS SOARED IN 2022

- FIGURE 34 MOST VALUED PATIENT ENGAGEMENT SOLUTION FIRMS IN 2022 (USD BILLION)

- 5.18 PATIENT ENGAGEMENT SOLUTIONS BUSINESS MODELS

- 5.18.1 SUBSCRIPTION-BASED MODEL

- 5.18.2 LICENSING MODEL

- 5.18.3 HYBRID MODEL

- 5.18.4 FREEMIUM MODEL

- 5.18.5 VALUE-BASED PRICING MODEL

- 5.18.6 DATA MONETIZATION

- 5.18.7 CUSTOM DEVELOPMENT/CONSULTING MODEL

- 5.18.8 INTEGRATION WITH EXISTING SYSTEMS

- 5.18.9 PARTNERSHIPS WITH HEALTHCARE PROVIDERS

- 5.18.10 WHITE-LABEL SOLUTIONS

- 5.18.11 OPEN-SOURCE SOFTWARE

- 5.19 USE CASES/CASE STUDIES

- 5.19.1 FOCUS ON REDUCING READMISSION RATES AND IMPROVING CARE

- 5.19.1.1 Use case 1: Need to reduce patient hospital stays

- 5.19.2 IMPROVE OUTPATIENT COMMUNICATION

- 5.19.2.1 Case 2: Rising need to curb miscommunication with discharged patients

- 5.19.3 PATIENT ENGAGEMENT STRATEGY

- 5.19.3.1 Use case 3: Post-discharge care

- 5.19.4 AN EMR-AGNOSTIC PATIENT ENGAGEMENT PLATFORM WITH COMPREHENSIVE BUILT-IN CAPABILITIES

- 5.19.4.1 Use case 4: To improve patient engagement, giving patients ability to access all their medical information in one place

- 5.19.1 FOCUS ON REDUCING READMISSION RATES AND IMPROVING CARE

6 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT

- 6.1 INTRODUCTION

- TABLE 17 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- 6.2 HARDWARE

- 6.2.1 INTERACTIVE EXPERIENCE FOR PATIENTS & FAMILIES

- TABLE 18 HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 19 HARDWARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 20 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HARDWARE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 21 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HARDWARE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 22 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HARDWARE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 23 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HARDWARE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 24 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HARDWARE, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.2 IN-ROOM TELEVISIONS

- 6.2.2.1 Increase in adoption of in-room televisions by hospitals

- TABLE 25 IN-ROOM TELEVISIONS MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 26 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR IN-ROOM TELEVISIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 27 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR IN-ROOM TELEVISIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 28 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR IN-ROOM TELEVISIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 29 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR IN-ROOM TELEVISIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 30 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR IN-ROOM TELEVISIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.3 INTEGRATED BEDSIDE TERMINALS/ASSISTED DEVICES

- 6.2.3.1 Integrated bedside terminals enhance patient experience

- TABLE 31 INTEGRATED BEDSIDE TERMINALS/ASSISTED DEVICES MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 32 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR INTEGRATED BEDSIDE TERMINALS/ASSISTED DEVICES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 33 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR INTEGRATED BEDSIDE TERMINALS/ASSISTED DEVICES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 34 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR INTEGRATED BEDSIDE TERMINALS/ASSISTED DEVICES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 35 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR INTEGRATED BEDSIDE TERMINALS/ASSISTED DEVICES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 36 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR INTEGRATED BEDSIDE TERMINALS/ASSISTED DEVICES, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.2.4 TABLETS

- 6.2.4.1 Portability and cost-effectiveness of tablets support growth

- TABLE 37 TABLETS MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 38 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TABLETS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 39 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TABLETS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 40 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TABLETS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 41 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TABLETS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 42 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TABLETS, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.3 SOFTWARE

- TABLE 43 SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 44 SOFTWARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 45 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SOFTWARE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 46 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SOFTWARE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 47 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SOFTWARE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 48 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SOFTWARE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 49 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SOFTWARE, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.3.1 STANDALONE SOFTWARE

- 6.3.1.1 Standalone software refers to traditional software installed in client systems

- TABLE 50 STANDALONE SOLUTIONS MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 51 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR STANDALONE SOLUTIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 52 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR STANDALONE SOLUTIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 53 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR STANDALONE SOLUTIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 54 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR STANDALONE SOLUTIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 55 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR STANDALONE SOLUTIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.3.2 INTEGRATED SOFTWARE

- 6.3.2.1 Reduction in time spent on data management to drive growth

- TABLE 56 INTEGRATED SOLUTIONS MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 57 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR INTEGRATED SOLUTIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 58 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR INTEGRATED SOLUTIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 59 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR INTEGRATED SOLUTIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 60 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR INTEGRATED SOLUTIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 61 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR INTEGRATED SOLUTIONS, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.4 SERVICES

- TABLE 62 SERVICES MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 63 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SERVICES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 64 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SERVICES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 65 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SERVICES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 66 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SERVICES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 67 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SERVICES, BY COUNTRY, 2021-2028 (USD MILLION)

7 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE

- 7.1 INTRODUCTION

- TABLE 68 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- 7.2 ON-PREMISE MODE

- 7.2.1 PATIENT DATA SAFETY AND COST BENEFITS TO DRIVE MARKET

- TABLE 69 ON-PREMISE MODE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 70 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR ON-PREMISE MODE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 71 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR ON-PREMISE MODE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 72 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR ON-PREMISE MODE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 73 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR ON-PREMISE MODE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 74 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR ON-PREMISE MODE, BY COUNTRY, 2021-2028 (USD MILLION)

- 7.3 CLOUD-BASED/ WEB-BASED MODE

- 7.3.1 REGULATORY REQUIREMENTS DRIVE HEALTHCARE PROVIDERS TO ADOPT CLOUD-BASED SOLUTIONS

- TABLE 75 CLOUD-BASED/WEB-BASED MODE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 76 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CLOUD-BASED MODE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 77 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CLOUD-BASED MODE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 78 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CLOUD-BASED MODE, BY COUNTRY, 2021-2028 (USD MILLION)

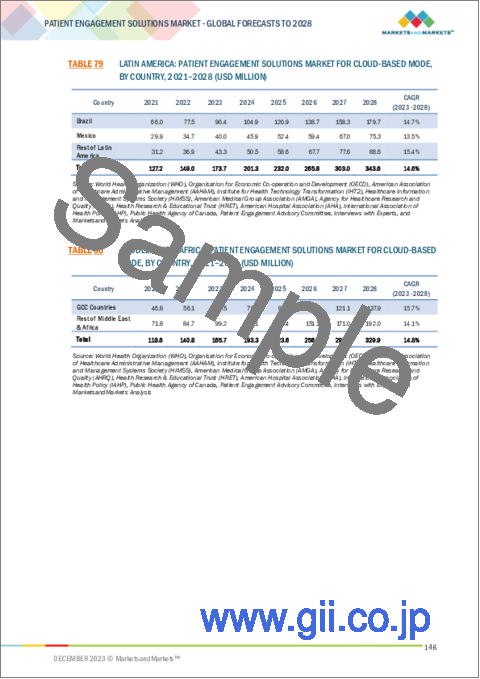

- TABLE 79 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CLOUD-BASED MODE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 80 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CLOUD-BASED MODE, BY COUNTRY, 2021-2028 (USD MILLION)

8 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- TABLE 81 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- 8.2 HEALTH MANAGEMENT

- 8.2.1 HEALTH MANAGEMENT PLAYS CRUCIAL TOOL IN GUIDING PATIENTS IN SELF-CARE

- TABLE 82 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HEALTH MANAGEMENT, BY REGION, 2021-2028 (USD MILLION)

- TABLE 83 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 84 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 85 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 86 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 87 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.3 HOME HEALTH MANAGEMENT

- 8.3.1 GROWING PREFERENCE FOR HOME HEALTHCARE TO SUPPORT MARKET GROWTH

- TABLE 88 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME HEALTH MANAGEMENT, BY REGION, 2021-2028 (USD MILLION)

- TABLE 89 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 90 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 91 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 92 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 93 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.4 SOCIAL & BEHAVIORAL MANAGEMENT

- 8.4.1 GROWING POPULARITY OF SOCIAL MEDIA TO DRIVE MARKET GROWTH

- TABLE 94 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SOCIAL & BEHAVIORAL MANAGEMENT, BY REGION, 2021-2028 (USD MILLION)

- TABLE 95 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SOCIAL & BEHAVIORAL MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 96 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SOCIAL & BEHAVIORAL MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 97 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SOCIAL & BEHAVIORAL MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 98 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SOCIAL & BEHAVIORAL MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 99 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR SOCIAL & BEHAVIORAL MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.5 FINANCIAL HEALTH MANAGEMENT

- 8.5.1 FINANCIAL ENGAGEMENT SOLUTIONS HELP PROVIDERS MANAGE PATIENT PAYMENTS

- TABLE 100 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FINANCIAL HEALTH MANAGEMENT, BY REGION, 2021-2028 (USD MILLION)

- TABLE 101 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FINANCIAL HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 102 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FINANCIAL HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 103 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FINANCIAL HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 104 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FINANCIAL HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 105 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FINANCIAL HEALTH MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

9 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA

- 9.1 INTRODUCTION

- TABLE 106 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- 9.2 CHRONIC DISEASES

- TABLE 107 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY REGION, 2021-2028 (USD MILLION)

- TABLE 108 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 109 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 110 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 111 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 112 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 113 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CHRONIC DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.2.1 CARDIOVASCULAR DISEASES (CVD)

- 9.2.1.1 Leading cause of death worldwide

- TABLE 114 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CARDIOVASCULAR DISEASES, BY REGION, 2021-2028 (USD MILLION)

- TABLE 115 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CARDIOVASCULAR DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 116 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CARDIOVASCULAR DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 117 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CARDIOVASCULAR DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 118 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CARDIOVASCULAR DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 119 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR CARDIOVASCULAR DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.2.2 DIABETES

- 9.2.2.1 High incidence of diabetes worldwide drives growth

- TABLE 120 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DIABETES, BY REGION, 2021-2028 (USD MILLION)

- TABLE 121 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DIABETES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 122 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DIABETES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 123 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DIABETES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 124 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DIABETES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 125 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DIABETES, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.2.3 OBESITY

- 9.2.3.1 Rising prevalence of obesity to drive growth

- TABLE 126 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OBESITY, BY REGION, 2021-2028 (USD MILLION)

- TABLE 127 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OBESITY, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 128 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OBESITY, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 129 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OBESITY, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 130 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OBESITY, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 131 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OBESITY, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.2.4 OTHER CHRONIC DISEASES

- TABLE 132 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER CHRONIC DISEASES, BY REGION, 2021-2028 (USD MILLION)

- TABLE 133 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER CHRONIC DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 134 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER CHRONIC DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 135 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER CHRONIC DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 136 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER CHRONIC DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 137 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER CHRONIC DISEASES, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.3 WOMEN'S HEALTH

- 9.3.1 INCREASING SELF-AWARENESS FOR MANAGEMENT OF DISEASES TO DRIVE MARKET

- TABLE 138 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR WOMEN'S HEALTH, BY REGION, 2021-2028 (USD MILLION)

- TABLE 139 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR WOMEN'S HEALTH, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 140 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR WOMEN'S HEALTH, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 141 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR WOMEN'S HEALTH, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 142 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR WOMEN'S HEALTH, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 143 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR WOMEN'S HEALTH, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.4 FITNESS

- 9.4.1 GROWING PREFERENCE FOR HEALTHY LIFESTYLE TO SUPPORT MARKET GROWTH

- TABLE 144 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FITNESS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 145 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FITNESS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 146 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FITNESS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 147 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FITNESS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 148 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FITNESS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 149 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR FITNESS, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.5 OTHER THERAPEUTIC AREAS

- TABLE 150 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER THERAPEUTIC AREAS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 151 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER THERAPEUTIC AREAS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 152 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER THERAPEUTIC AREAS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 153 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER THERAPEUTIC AREAS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 154 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER THERAPEUTIC AREAS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 155 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER THERAPEUTIC AREAS, BY COUNTRY, 2021-2028 (USD MILLION)

10 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY

- 10.1 INTRODUCTION

- TABLE 156 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- 10.2 PATIENT/CLIENT SCHEDULING

- 10.2.1 STREAMLINING OF WORKFLOWS AND EFFICIENT MANAGEMENT OF PATIENT SCHEDULES

- TABLE 157 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT/CLIENT SCHEDULING, BY REGION, 2021-2028 (USD MILLION)

- TABLE 158 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT/CLIENT SCHEDULING, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 159 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT/CLIENT SCHEDULING, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 160 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT/CLIENT SCHEDULING, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 161 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT/CLIENT SCHEDULING, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 162 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT/CLIENT SCHEDULING, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.3 TELEHEALTH

- 10.3.1 FLEXIBILITY IN TREATMENT OPTIONS DUE TO REMOTE MONITORING

- TABLE 163 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TELEHEALTH, BY REGION, 2021-2028 (USD MILLION)

- TABLE 164 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TELEHEALTH, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 165 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TELEHEALTH, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 166 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TELEHEALTH, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 167 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TELEHEALTH, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 168 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR TELEHEALTH, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.4 E-PRESCRIBING

- 10.4.1 COST-EFFECTIVE METHOD TO ENHANCE DECISION-MAKING

- TABLE 169 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR E-PRESCRIBING, BY REGION, 2021-2028 (USD MILLION)

- TABLE 170 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR E-PRESCRIBING, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 171 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR E-PRESCRIBING, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 172 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR E-PRESCRIBING, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 173 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR E-PRESCRIBING, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 174 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR E-PRESCRIBING, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.5 DOCUMENT MANAGEMENT

- 10.5.1 EFFECTIVE MANAGEMENT OF PATIENT DOCUMENTS CRUCIAL FOR HEALTHCARE PROVIDERS

- TABLE 175 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DOCUMENT MANAGEMENT, BY REGION, 2021-2028 (USD MILLION)

- TABLE 176 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DOCUMENT MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 177 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DOCUMENT MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 178 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DOCUMENT MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 179 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DOCUMENT MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 180 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR DOCUMENT MANAGEMENT, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.6 BILLING & PAYMENTS

- 10.6.1 DEMAND FOR STREAMLINED PROCESSES TO DRIVE MARKET GROWTH

- TABLE 181 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR BILLING & PAYMENTS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 182 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR BILLING & PAYMENTS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 183 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR BILLING & PAYMENTS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 184 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR BILLING & PAYMENTS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 185 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR BILLING & PAYMENTS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 186 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR BILLING & PAYMENTS, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.7 PATIENT EDUCATION

- 10.7.1 RISING DEMAND FOR INFORMED HEALTHCARE TO DRIVE MARKET GROWTH

- TABLE 187 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT EDUCATION, BY REGION, 2021-2028 (USD MILLION)

- TABLE 188 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT EDUCATION, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 189 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT EDUCATION, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 190 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT EDUCATION, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 191 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT EDUCATION, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 192 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENT EDUCATION, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.8 OTHER FUNCTIONALITIES

- TABLE 193 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER FUNCTIONALITIES, BY REGION, 2021-2028 (USD MILLION)

- TABLE 194 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER FUNCTIONALITIES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 195 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER FUNCTIONALITIES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 196 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER FUNCTIONALITIES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 197 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER FUNCTIONALITIES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 198 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER FUNCTIONALITIES, BY COUNTRY, 2021-2028 (USD MILLION)

11 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER

- 11.1 INTRODUCTION

- TABLE 199 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- 11.2 PROVIDERS

- 11.2.1 LARGEST END USERS OF PATIENT ENGAGEMENT SOLUTIONS

- TABLE 200 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 201 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 202 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 203 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 204 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 205 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 206 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PROVIDERS, BY COUNTRY, 2021-2028 (USD MILLION)

- 11.2.2 HOSPITALS & HEALTHCARE SYSTEMS

- 11.2.2.1 Hospitals and healthcare systems contribute highest share

- TABLE 207 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOSPITALS & HEALTHCARE SYSTEMS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 208 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOSPITALS & HEALTHCARE SYSTEMS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 209 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOSPITALS & HEALTHCARE SYSTEMS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 210 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOSPITALS & HEALTHCARE SYSTEMS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 211 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOSPITALS & HEALTHCARE SYSTEMS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 212 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOSPITALS & HEALTHCARE SYSTEMS, BY COUNTRY, 2021-2028 (USD MILLION)

- 11.2.3 AMBULATORY CARE CENTERS

- 11.2.3.1 Gradual shift of patient care from inpatient to outpatient settings to drive growth

- TABLE 213 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR AMBULATORY CARE CENTERS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 214 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR AMBULATORY CARE CENTERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 215 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR AMBULATORY CARE CENTERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 216 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR AMBULATORY CARE CENTERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 217 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR AMBULATORY CARE CENTERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 218 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR AMBULATORY CARE CENTERS, BY COUNTRY, 2021-2028 (USD MILLION)

- 11.2.4 HOME CARE CENTERS

- 11.2.4.1 Rise in global geriatric population requiring long-term care to support market growth

- TABLE 219 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME CARE CENTERS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 220 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME CARE CENTERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 221 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME CARE CENTERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 222 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME CARE CENTERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 223 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME CARE CENTERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 224 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR HOME CARE CENTERS, BY COUNTRY, 2021-2028 (USD MILLION)

- 11.2.5 OTHER PROVIDERS

- TABLE 225 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER PROVIDERS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 226 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER PROVIDERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 227 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER PROVIDERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 228 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER PROVIDERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 229 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER PROVIDERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 230 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER PROVIDERS, BY COUNTRY, 2021-2028 (USD MILLION)

- 11.3 PAYERS

- 11.3.1 PATIENT ENGAGEMENT SOLUTIONS HELP HEALTHCARE PAYERS MINIMIZE ERRORS

- TABLE 231 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 232 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 233 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 234 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 235 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 236 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 237 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- 11.3.2 PRIVATE

- 11.3.2.1 Private payers partnering with telehealth vendors for seamless healthcare solutions

- TABLE 238 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PRIVATE PAYERS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 239 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PRIVATE PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 240 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PRIVATE PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 241 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PRIVATE PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 242 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PRIVATE PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 243 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PRIVATE PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- 11.3.3 PUBLIC

- 11.3.3.1 Investments made by public payers to support market

- TABLE 244 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PUBLIC PAYERS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 245 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PUBLIC PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 246 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PUBLIC PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 247 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PUBLIC PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 248 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PUBLIC PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 249 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PUBLIC PAYERS, BY COUNTRY, 2021-2028 (USD MILLION)

- 11.4 PATIENTS

- 11.4.1 PATIENT ENGAGEMENT SOLUTIONS MOTIVATE INDIVIDUALS TO MONITOR AND IMPROVE HEALTH OUTCOMES

- TABLE 250 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENTS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 251 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENTS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 252 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENTS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 253 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENTS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 254 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENTS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 255 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR PATIENTS, BY COUNTRY, 2021-2028 (USD MILLION)

- 11.5 OTHER END USERS

- TABLE 256 PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER END USERS, BY REGION, 2021-2028 (USD MILLION)

- TABLE 257 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER END USERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 258 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER END USERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 259 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER END USERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 260 LATIN AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER END USERS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 261 MIDDLE EAST & AFRICA: PATIENT ENGAGEMENT SOLUTIONS MARKET FOR OTHER END USERS, BY COUNTRY, 2021-2028 (USD MILLION)

12 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY REGION

- 12.1 INTRODUCTION

- TABLE 262 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY REGION, 2021-2028 (USD MILLION)

- 12.2 NORTH AMERICA

- FIGURE 35 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET SNAPSHOT

- 12.2.1 RECESSION IMPACT

- TABLE 263 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 264 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 265 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 266 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 267 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 268 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 269 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 270 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 271 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 272 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 273 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 274 NORTH AMERICA: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.2.2 US

- 12.2.2.1 High healthcare expenditure and affordable costs to drive market

- TABLE 275 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 276 US: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 277 US: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 278 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 279 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 280 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 281 US: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 282 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 283 US: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 284 US: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 285 US: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.2.3 CANADA

- 12.2.3.1 Growing need for cost containment to drive market

- TABLE 286 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 287 CANADA: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 288 CANADA: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 289 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 290 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 291 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 292 CANADA: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 293 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 294 CANADA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 295 CANADA: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 296 CANADA: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.3 EUROPE

- 12.3.1 RECESSION IMPACT

- TABLE 297 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 298 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 299 EUROPE: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 300 EUROPE: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 301 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 302 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 303 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 304 EUROPE: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 305 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 306 EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 307 EUROPE: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 308 EUROPE: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.3.2 GERMANY

- 12.3.2.1 Growing demand for effective patient records management to drive market

- TABLE 309 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 310 GERMANY: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 311 GERMANY: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 312 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 313 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 314 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 315 GERMANY: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 316 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 317 GERMANY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 318 GERMANY: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 319 GERMANY: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.3.3 FRANCE

- 12.3.3.1 Digital health insurance startups to drive market

- TABLE 320 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 321 FRANCE: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 322 FRANCE: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 323 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 324 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 325 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 326 FRANCE: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 327 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 328 FRANCE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 329 FRANCE: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 330 FRANCE: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.3.4 UK

- 12.3.4.1 Favorable government initiatives promoting healthcare to drive market

- TABLE 331 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 332 UK: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 333 UK: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 334 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 335 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 336 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 337 UK: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 338 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 339 UK: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 340 UK: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 341 UK: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.3.5 SPAIN

- 12.3.5.1 Enhanced ability for monitoring patients and chronic illnesses to drive market

- TABLE 342 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 343 SPAIN: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 344 SPAIN: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 345 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 346 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 347 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 348 SPAIN: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 349 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 350 SPAIN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 351 SPAIN: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 352 SPAIN: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.3.6 ITALY

- 12.3.6.1 Growing burden of chronic diseases and shortage of healthcare workers to drive market

- TABLE 353 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 354 ITALY: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 355 ITALY: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 356 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 357 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 358 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 359 ITALY: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 360 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 361 ITALY: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 362 ITALY: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 363 ITALY: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.3.7 REST OF EUROPE

- TABLE 364 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 365 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 366 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 367 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 368 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 369 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 370 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 371 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 372 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 373 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 374 REST OF EUROPE: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.4 ASIA PACIFIC

- 12.4.1 RECESSION IMPACT

- FIGURE 36 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET SNAPSHOT

- TABLE 375 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 376 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 377 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 378 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 379 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 380 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 381 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 382 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 383 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 384 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 385 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 386 ASIA PACIFIC: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.4.2 JAPAN

- 12.4.2.1 Rising geriatric population to drive market

- TABLE 387 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 388 JAPAN: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 389 JAPAN: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 390 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 391 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 392 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 393 JAPAN: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 394 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 395 JAPAN: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 396 JAPAN: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 397 JAPAN: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.4.3 CHINA

- 12.4.3.1 Implementation of EMR solutions by government to drive market

- TABLE 398 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 399 CHINA: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 400 CHINA: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 401 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 402 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 403 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 404 CHINA: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 405 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)

- TABLE 406 CHINA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 407 CHINA: PATIENT ENGAGEMENT SOLUTION PROVIDERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 408 CHINA: PATIENT ENGAGEMENT SOLUTION PAYERS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 12.4.4 INDIA

- 12.4.4.1 High burden of chronic diseases to drive market

- TABLE 409 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 410 INDIA: PATIENT ENGAGEMENT SOLUTIONS HARDWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 411 INDIA: PATIENT ENGAGEMENT SOLUTIONS SOFTWARE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 412 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE, 2021-2028 (USD MILLION)

- TABLE 413 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 414 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA, 2021-2028 (USD MILLION)

- TABLE 415 INDIA: PATIENT ENGAGEMENT SOLUTIONS CHRONIC DISEASE MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 416 INDIA: PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY, 2021-2028 (USD MILLION)