スマート交通の世界市場 (~2032年):交通モード (道路・鉄道・航空・海運)・エンドユーザー (政府・民間企業) 別

Smart Transportation Market by Transportation Mode (Roadways, Railways, Airways, Maritime), By End User (Government, Commercial Organizations) - Global Forecast to 2032- 発行日

- ページ情報

- 英文 463 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 2074464

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

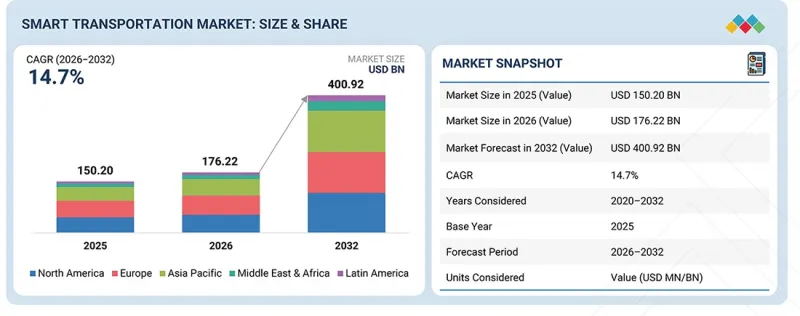

スマート交通の市場規模は、2026年の1,762億2,000万米ドルから、2032年には4,009億2,000万米ドルへと、CAGR 14.7%で拡大すると予測されています。

デジタルトランスフォーメーションの時代を迎え、さまざまな業界の企業が、AI、IoT、ビッグデータといった最先端技術を統合し、業務効率の向上や顧客体験の改善を図っています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2020年~2032年 |

| 基準年 | 2025年 |

| 予測期間 | 2026年~2032年 |

| 単位 | 金額 (米ドル) |

| セグメント | 交通モード、エンドユーザー、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、中東・アフリカ、ラテンアメリカ |

さらに、政府や組織が交通管理の最適化、渋滞の緩和、安全性の向上に注力するにつれ、よりスマートな交通ソリューションへの需要が急増しています。こうした進展により、道路、鉄道、航空分野におけるスマート交通技術の導入が促進され、世界的により持続可能で効率的な交通システムが構築されると予想されます。

「道路分野においては、予測期間中、交通管理ソリューションが最大の市場規模を占めると予想されます。」

交通管理ソリューションは、特に都市環境において、道路網の効率性と安全性を向上させるために不可欠なものです。これらは、AI、機械学習、IoTセンサー、ビッグデータ分析などの先進技術を活用して、交通の流れを最適化します。これらのシステムは、リアルタイムの交通状況を監視し、信号機のタイミングを管理し、渋滞を予測し、ボトルネックを緩和するための解決策を提供します。交通の監視と制御を自動化することで、これらのシステムは遅延や汚染を削減し、移動時間を短縮し、より持続可能な都市モビリティの実現に貢献します。例えば、Siemens Mobilityの交通管理ソリューションは、これらの先進技術を統合して信号を動的に調整し、公共交通機関の車両群を管理し、全体的な交通効率を向上させることで、世界各地の都市におけるより円滑な通勤・移動を実現しています。

「鉄道分野では、予測期間中に旅客情報ソリューションが最も高い成長率を示す見込みです。」

乗客情報ソリューションは、乗客にリアルタイムで実用的なデータを提供し、乗客が十分な情報に基づいて移動の判断を下せるよう支援します。これらのソリューションは通常、デジタルディスプレイ、モバイルアプリ、自動アナウンスによって構成されており、列車の運行スケジュール、遅延、運休、ホーム変更に関する最新情報を提供します。シームレスで快適な旅行体験への需要が高まる中、鉄道事業者は顧客満足度と業務効率の向上を図るため、これらの技術に投資しています。例えば、Alstomの旅客情報システムは、リアルタイムデータを活用して乗客に旅行情報の更新を通知し、旅程の調整を円滑に行えるようにしています。鉄道業界が顧客体験の向上と業務の効率化に注力する中、旅客情報システムは、旅行体験全体の向上、乗客の待ち時間の短縮、旅程の予測可能性を高める上で極めて重要な役割を果たしています。

「航空分野では、予測期間中、航空交通管理ソリューションが最大の市場シェアを占めると予想されます。」

航空交通管理 (ATM) システムは、航空旅行の安全性、効率性、円滑な運航を確保する上で極めて重要です。航空交通を管理するため、これらのシステムはAI、レーダー、衛星航法、リアルタイムデータ分析など、さまざまな先進技術を活用しています。飛行ルートの最適化、遅延の削減、空域容量の拡大を通じて、ATMシステムは航空機が安全かつ効率的に、環境への影響を最小限に抑えて飛行できるようにします。世界の航空交通量の増加に伴い、これらのシステムは混雑の管理や飛行の安全性の向上において、ますます重要な役割を果たしています。例えば、Thalesの航空交通管理ソリューションは、予測分析とリアルタイムのデータ共有を取り入れ、航空交通の流れと意思決定を強化することで、航空交通管制官の業務効率を向上させ、空域の利用を最適化しています。これにより、混雑が激化する空域において、遅延の削減、より円滑な運航、そして安全性の向上が図られます。

当レポートでは、世界のスマート交通の市場を調査し、市場概要、市場成長への各種影響因子の分析、技術・特許の動向、法規制環境、ケーススタディ、市場規模の推移・予測、各種区分・地域/主要国別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要考察

第4章 市場概要と業界動向

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 関連市場・異業種との分野横断的機会

- ティア1/2/3企業による戦略的な動き

第5章 業界動向

- ポーターのファイブフォース分析

- マクロ経済指標

- GDPの動向と予測

- インテリジェント都市モビリティおよび交通管理業界の動向

- スマートロジスティクスと貨物輸送業界の動向

- サプライチェーン分析

- エコシステム分析

- 価格設定モデル分析

- 2026年~2027年の主な会議およびイベント

- 顧客企業の事業に影響を与える動向/ディスラプション

- 投資と資金調達のシナリオ

- ケーススタディ分析

- 2025年米国関税の影響:スマート交通市場

第6章 戦略的破壊:デジタルとAIの導入

- 主要な新興技術

- 車車間通信 (V2X)

- AIと機械学習

- 自動運転車

- GIS

- 隣接技術

- 補完的技術

- スマート交通市場向け技術/製品ロードマップ

- 短期ロードマップ (2023年~2025年)

- 中期ロードマップ (2026年~2028年)

- 長期ロードマップ (2029年~2032年)

- 特許分析

- AI/汎用AIがスマート交通市場に与える影響

第7章 規制状況

- 規制機関、政府機関、その他の組織

- 業界標準

第8章 顧客情勢と購買行動

- 意思決定プロセス

- 主要ステークホルダーと購入基準

- 導入における障壁と内部課題

- 様々なエンドユーザー産業におけるアンメットニーズ

第9章 スマート交通市場:交通モード別

- 道路

- ソリューション

- サービス

- 鉄道

- ソリューション

- サービス

- 航空

- ソリューション

- サービス

- 海運

- ソリューション

- サービス

第10章 スマート交通市場:エンドユーザー別

- 政府

- 商業組織

第11章 スマート交通市場:地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他

- アジア太平洋

- 中国

- 日本

- インド

- その他

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他

- ラテンアメリカ

- ブラジル

- メキシコ

- その他

第12章 競合情勢

- 主要参入企業の戦略/強み

- 市場シェア分析

- 主要企業の収益分析

- ブランド/製品比較

- 企業評価と財務指標

- 企業評価マトリックス:道路

- 企業評価マトリックス:鉄道

- 企業評価マトリックス:航空

- 企業評価マトリックス:海運

- 競合シナリオ

第13章 企業プロファイル

- 主要企業

- THALES GROUP

- HUAWEI

- SIEMENS

- ALSTOM

- HITACHI

- CISCO

- DNV

- CUBIC

- TOSHIBA

- VESON NAUTICAL

- ALMAVIVA

- NEC CORPORATION

- BENTLEY SYSTEMS

- INDRA

- TRIMBLE

- TOMTOM

- CONDUENT

- KAPSCH

- DESCARTES

- WARTSILA

- BOSCH

- IEI INTEGRATION CORP.

- SCHNEIDER ELECTRIC

- TRANSCORE

- その他の企業

- BASSNET

- EKE-ELECTRONICS

- AITEK

- INRIX

- TAGMASTER

- ATSUKE

- PARK+

- APPYWAY

- EFFTRONICS SYSTEMS

第14章 調査手法

第15章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 463 Pages

- 納期

- 即納可能