|

市場調査レポート

商品コード

1699247

スマート交場市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Smart Transportation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| スマート交場市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月17日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

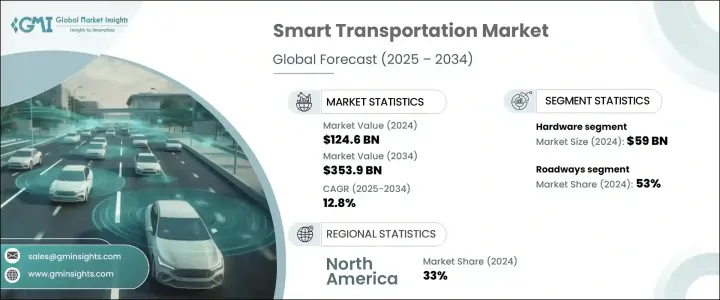

世界のスマート交通市場の2024年の市場規模は1,246億米ドルで、2025年から2034年にかけてCAGR 12.8%で成長すると予測されています。

世界の各都市が遅延の削減、排出ガスの削減、全体的な輸送効率の向上を目的とした高度なモビリティソリューションを求めているため、急速な都市化と交通渋滞の増加が市場拡大の主な要因となっています。コネクテッドカーや自律走行車(CAV)の採用拡大が市場成長に大きく影響しており、AI、IoT、5Gなどの技術がリアルタイムの交通管理やV2X(Vehicle-to-Everything)通信で重要な役割を果たしています。

これらの進歩は、交通安全の最適化、交通流の合理化、スマートシティインフラとの統合による交通網の強化に役立っています。政府や交通当局はインテリジェント交通システム(ITS)に多額の投資を行っており、スマート信号、自動料金徴収、車両追跡などの取り組みを支援しています。自動運転車や電気自動車が主流になるにつれて、AIを搭載したモビリティ・ソリューションの需要は高まり続け、スマート交通産業の拡大を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,246億米ドル |

| 予測金額 | 3,539億米ドル |

| CAGR | 12.8% |

市場はコンポーネントに基づいてハードウェア、ソフトウェア、サービスに区分されます。2024年はハードウェア分野が590億米ドルの収益を上げてリードし、予測期間中は約13.2%のCAGRで成長すると予測されます。主なハードウェア要素には、GPS、IoTセンサー、RFIDチップ、監視カメラ、自動料金徴収システム、V2X通信機器などがあります。これらの技術は、リアルタイムの交通モニタリング、コネクテッド・ビークル・システム、インテリジェント交通ソリューションに不可欠です。電子料金徴収やAI主導の交通管理など、都市モビリティ向けの組み込みシステムへの投資が、ハードウェアソリューションの需要をさらに強めています。

輸送モード別に見ると、市場は道路、鉄道、航空、海運に分けられます。道路は2024年に市場シェアの53%を占め、2034年までのCAGRは13%以上で成長すると予測されます。都市部の道路網の拡大と、電気自動車や自律走行車の普及が、高度な交通管制・予測システムの必要性を高めています。ライドヘイリングサービスや共有モビリティプラットフォームもスマート道路ソリューションの開発を加速させており、この分野の成長に寄与しています。

ソリューションの観点から、市場は交通管理、スマートチケッティング、駐車場管理、旅客情報システム、貨物管理に区分されます。交通管理分野は、道路を走る車両数の増加、都市部の渋滞の増加、効果的なモビリティ・ソリューションの必要性から優位を占めています。遅延や環境への影響を最小限に抑えながら道路性能を最適化するために、AI主導の交通制御、適応型信号、渋滞価格戦略が導入されています。リアルタイムの交通追跡、事故の自動検知、予測分析により、道路の安全性と効率性がさらに高まっています。

地域別では、北米が2024年の市場をリードし、世界シェアの約33%を占め、420億米ドルの収益を上げました。米国は依然として最前線にあり、政府の強力なイニシアチブ、技術の進歩、市場開拓が市場拡大に拍車をかけています。ITS、コネクテッド・モビリティ、AIを活用した交通ソリューションを促進する連邦政府の資金提供プログラムや政策が、大都市圏全域でスマート交通インフラの採用を加速させています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- テクノロジープロバイダー

- システムインテグレーター

- 交通インフラプロバイダー

- 自動車・車両メーカー

- データ&サービスプロバイダー

- 利益率分析

- テクノロジー&イノベーション情勢

- 特許分析

- 使用事例

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- 世界各都市の急速な都市化と渋滞

- 効率的で持続可能な輸送に対する需要の高まり

- IoT、AI、ビッグデータ分析における技術の進歩

- 政府の取り組みと投資の増加

- コネクテッドカーや自律走行車に対する需要の高まり

- 業界の潜在的リスク&課題

- 高い初期投資コスト

- データプライバシーとセキュリティに関する懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- センサー

- カメラ

- RFIDチップ

- GPSデバイス

- その他

- ソフトウェア

- 交通管理システム

- 車両管理ソフトウェア

- その他

- サービス

- コンサルティング

- 導入と統合

- サポート&メンテナンス

第6章 市場推計・予測:輸送モード別、2021年~2034年

- 主要動向

- 道路

- 鉄道

- 空路

- 海路

第7章 市場推計・予測:ソリューション別、2021年~2034年

- 主要動向

- 交通管理

- スマートチケッティング

- 駐車場管理

- 旅客情報システム

- 貨物管理

第8章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- IoT

- AIと機械学習

- ビッグデータ分析

- クラウドコンピューティング

- ブロックチェーン

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 政府機関

- 民間企業

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Alstom

- Bentley

- Cisco

- Conduent

- Cubic

- Hitachi

- Huawei Technologies

- IBM

- Indra Sistema

- Kapsch TrafficCom

- Lyft

- NEC

- Qualcomm

- Robert Bosch

- SAP

- Siemens Mobility

- Thales

- TomTom

- Trimble

- Uber Technologies

The Global Smart Transportation Market was valued at USD 124.6 billion in 2024 and is expected to grow at a CAGR of 12.8% from 2025 to 2034. Rapid urbanization and rising traffic congestion are key factors driving market expansion as cities worldwide seek advanced mobility solutions to reduce delays, lower emissions, and enhance overall transportation efficiency. The growing adoption of connected and autonomous vehicles (CAVs) is significantly influencing market growth, with technologies like AI, IoT, and 5G playing a crucial role in real-time traffic management and vehicle-to-everything (V2X) communication.

These advancements help optimize road safety, streamline traffic flow, and enhance transport networks by integrating with smart city infrastructure. Governments and transport authorities are heavily investing in intelligent transportation systems (ITS), supporting initiatives such as smart signals, automated tolling, and vehicle tracking. As self-driving and electric vehicles become more mainstream, demand for AI-powered mobility solutions continues to rise, reinforcing the expansion of the smart transportation industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $124.6 Billion |

| Forecast Value | $353.9 Billion |

| CAGR | 12.8% |

The market is segmented based on components into hardware, software, and services. The hardware segment led in 2024, generating USD 59 billion in revenue, and is projected to grow at a CAGR of approximately 13.2% during the forecast period. Key hardware elements include GPS, IoT sensors, RFID chips, surveillance cameras, automated fare collection systems, and V2X communication devices. These technologies are critical for real-time traffic monitoring, connected vehicle systems, and intelligent transport solutions. Investment in embedded systems for urban mobility, including electronic toll collection and AI-driven traffic management, is further strengthening the demand for hardware solutions.

By transportation mode, the market is divided into roadways, railways, airways, and maritime. Roadways accounted for 53% of the market share in 2024 and are anticipated to grow at a CAGR of over 13% through 2034. Expanding urban road networks and the increasing adoption of electric and autonomous vehicles are boosting the need for advanced traffic control and forecasting systems. Ride-hailing services and shared mobility platforms are also accelerating the development of smart roadway solutions, contributing to the sector's growth.

In terms of solutions, the market is segmented into traffic management, smart ticketing, parking management, passenger information systems, and freight management. The traffic management segment dominates due to the rising number of vehicles on roads, increasing urban congestion, and the need for effective mobility solutions. AI-driven traffic control, adaptive signaling, and congestion pricing strategies are being implemented to optimize road performance while minimizing delays and environmental impact. Real-time traffic tracking, automatic incident detection, and predictive analytics are further enhancing road safety and efficiency.

Regionally, North America led the market in 2024, accounting for around 33% of the global share and generating USD 42 billion in revenue. The United States remains at the forefront, with strong government initiatives, technological advancements, and urban development fueling market expansion. Federal funding programs and policies promoting ITS, connected mobility, and AI-powered transportation solutions are accelerating the adoption of smart transport infrastructure across major metropolitan areas.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology providers

- 3.2.2 System integrators

- 3.2.3 Transportation infrastructure providers

- 3.2.4 Automotive & vehicle manufacturers

- 3.2.5 Data & service providers

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Use cases

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rapid urbanization and congestion in cities across the world

- 3.9.1.2 Growing demand for efficient and sustainable transportation

- 3.9.1.3 Technological advancements in IoT, AI, and big data analytics

- 3.9.1.4 Rising government initiatives and investments

- 3.9.1.5 Growing demand for connected and autonomous vehicles

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial investment costs

- 3.9.2.2 Data privacy and security concerns

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.2 Cameras

- 5.2.3 RFID chips

- 5.2.4 GPS device

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Traffic management systems

- 5.3.2 Fleet management software

- 5.3.3 Others

- 5.4 Services

- 5.4.1 Consulting

- 5.4.2 Deployment & integration

- 5.4.3 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Transportation Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Roadways

- 6.3 Railways

- 6.4 Airways

- 6.5 Maritime

Chapter 7 Market Estimates & Forecast, By Solution, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Traffic management

- 7.3 Smart ticketing

- 7.4 Parking management

- 7.5 Passenger information systems

- 7.6 Freight management

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 IoT

- 8.3 AI & machine learning

- 8.4 Big data analytics

- 8.5 Cloud computing

- 8.6 Blockchain

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Government agencies

- 9.3 Commercial businesses

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Alstom

- 11.2 Bentley

- 11.3 Cisco

- 11.4 Conduent

- 11.5 Cubic

- 11.6 Hitachi

- 11.7 Huawei Technologies

- 11.8 IBM

- 11.9 Indra Sistema

- 11.10 Kapsch TrafficCom

- 11.11 Lyft

- 11.12 NEC

- 11.13 Qualcomm

- 11.14 Robert Bosch

- 11.15 SAP

- 11.16 Siemens Mobility

- 11.17 Thales

- 11.18 TomTom

- 11.19 Trimble

- 11.20 Uber Technologies