|

|

市場調査レポート

商品コード

1536659

拡張現実と仮想現実の世界市場:技術別、オファリング別、デバイスタイプ別、用途別、地域別 - 2029年までの予測Augmented and Virtual Reality Market by Enterprise, Technology (Augmented Reality, Virtual Reality), Offering (Hardware, Software), Device Type (HMDs, HUDs, Gesture Tracking Devices), Application and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 拡張現実と仮想現実の世界市場:技術別、オファリング別、デバイスタイプ別、用途別、地域別 - 2029年までの予測 |

|

出版日: 2024年08月02日

発行: MarketsandMarkets

ページ情報: 英文 308 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

拡張現実と仮想現実の市場規模は、2024年に221億2,000万米ドルになるとみられ、2024年~2029年のCAGRは34.2%で、2029年には963億2,000万米ドルに達すると予測されています。

拡張現実と仮想現実市場の成長を促進する主な要因には、AR開発者エコシステムの急増、予算に見合ったVR機器の存在などがあります。さらに、ARおよびVR技術の広範な採用、研究開発に向けた継続的な政府の取り組みと投資は、拡張現実と仮想現実市場の市場参入企業にいくつかの成長機会を提供すると期待されています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 検討単位 | 金額(10億米ドル) |

| セグメント別 | 技術別、オファリング別、デバイスタイプ別、用途別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

半没入型および完全没入型技術の仮想現実市場は、予測期間中に高いCAGRを記録すると予測されています。これは、シミュレーショントレーニングやバーチャルウォークスルーにおいて半没入型技術の採用が増加していること、また、ユーザーが物理的な周囲の環境を認識できなくなるほど完全にデジタル環境に没入できる高度なエンゲージメントを実現する完全没入型技術の需要が増加していることが要因であり、ハイエンドゲーム、医療シミュレーション、バーチャルツアー、建築設計において非常に好まれています。

拡張現実と仮想現実ソフトウェアは、予測期間中に最大の市場規模を持つ見込みです。これは、大規模な実装に移行しつつある新興プロジェクトに起因しています。IKEAやWalmartのような大手企業は、顧客のショッピング体験を向上させることを目的としたARプロトタイプを発表しており、これはこの分野での継続的な実験を反映しています。一方、VRソフトウェアは、大量消費主義によって加速しているソフトウェア開発キットの製造において重要な役割を果たしています。例えば、VR技術を高度にサポートするSDKには、REALITY SDK、Virtual Reality Tool Kit(VRTK)、PlayStation Virtual Reality(PSVR)開発キット、Oculus SDK、Google Virtual Reality SDKなどがあります。さらに、VRソフトウェアはクラウドベースのサービスも提供しており、撮影した画像をデータベースと比較し、関連する情報をモバイルデバイスに送り返し、検出、リサイズ、3D画像の生成などの画像処理を行います。

当レポートでは、世界の拡張現実と仮想現実市場について調査し、技術別、オファリング別、デバイスタイプ別、用途別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学:拡張現実市場

- 市場力学:仮想現実市場

- バリューチェーン分析

- エコシステム分析

- 投資と資金調達のシナリオ

- 顧客ビジネスに影響を与える動向/混乱

- 技術分析

- 価格分析

- ポーターのファイブフォース分析

- 主な利害関係者と購入基準

- AI/生成AIが拡張現実と仮想現実市場に与える影響

- ケーススタディ分析

- 貿易分析

- 特許分析

- 規制状況

- 主な会議とイベント、2024年~2025年

第6章 拡張現実と仮想現実の技術を開発する企業

- イントロダクション

- 中小企業

- 中規模企業

- 大規模企業

第7章 拡張現実と仮想現実市場、技術別

- イントロダクション

- 拡張現実

- 仮想現実

第8章 拡張現実と仮想現実市場、オファリング別

- イントロダクション

- ハードウェア

- ソフトウェア

第9章 拡張現実と仮想現実市場、デバイスタイプ別

- イントロダクション

- 拡張現実デバイス

- 仮想現実デバイス

第10章 拡張現実と仮想現実市場、用途別

- イントロダクション

- 拡張現実

- 仮想現実

第11章 拡張現実と仮想現実市場、地域別

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- その他の地域

第12章 競合情勢

- イントロダクション

- 主要戦略/有力企業、2019年~2024年

- 市場シェア分析、2023年

- 企業価値評価と財務指標

- ブランド/製品比較

- 収益分析、2020年~2023年

- 企業評価マトリックス:主要参入企業、2023年

- 企業評価マトリックス:スタートアップ/中小企業、2023年

- 競合シナリオ

第13章 企業プロファイル

- 主要参入企業

- META

- SONY CORPORATION

- APPLE INC.

- BYTEDANCE

- DPVR

- HTC CORPORATION

- MICROSOFT

- SAMSUNG

- PTC

- SEIKO EPSON CORPORATION

- LENOVO

- その他の企業

- EON REALITY

- MAXST CO., LTD.

- MAGIC LEAP, INC.

- BLIPPAR GROUP LIMITED

- ATHEER, INC.

- VUZIX

- NINTENDO

- ULTRALEAP

- PENUMBRA, INC.

- PSICO SMART APPS S.L.

- XIAOMI

- PANASONIC CORPORATION

- SCOPE AR

- CONTINENTAL AG

- VIRTUALLY LIVE

- INTEL CORPORATION

- CRAFTARS

- BIDON GAMES STUDIO

- APPENTUS TECHNOLOGIES

- 3D CLOUD

- WAYRAY AG

第14章 付録

List of Tables

- TABLE 1 AUGMENTED AND VIRTUAL REALITY MARKET FORECAST

- TABLE 2 AUGMENTED AND VIRTUAL REALITY MARKET: RESEARCH ASSUMPTIONS

- TABLE 3 AUGMENTED AND VIRTUAL REALITY MARKET: RISK ANALYSIS

- TABLE 4 ROLE OF COMPANIES IN AUGMENTED AND VIRTUAL REALITY ECOSYSTEM

- TABLE 5 AVERAGE SELLING PRICE TREND OF AUGMENTED REALITY DEVICES OFFERED BY KEY PLAYERS, 2020-2023 (USD)

- TABLE 6 AVERAGE SELLING PRICE TREND OF VIRTUAL REALITY DEVICES OFFERED BY KEY PLAYERS, 2020-2023 (USD)

- TABLE 7 AVERAGE SELLING PRICE TREND OF AUGMENTED REALITY DEVICES, 2020-2023 (USD)

- TABLE 8 AVERAGE SELLING PRICE TREND OF VIRTUAL REALITY DEVICES, 2020-2023 (USD)

- TABLE 9 AVERAGE SELLING PRICE TREND OF VR HEAD-MOUNTED DISPLAYS, BY REGION, 2020-2023 (USD)

- TABLE 10 PORTER'S FIVE FORCES ANALYSIS

- TABLE 11 AUGMENTED AND VIRTUAL REALITY MARKET: INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP TWO APPLICATIONS (%)

- TABLE 12 AUGMENTED AND VIRTUAL REALITY MARKET: KEY BUYING CRITERIA FOR TOP TWO APPLICATIONS

- TABLE 13 IMPORT DATA FOR HS CODE 9004-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 14 EXPORT DATA FOR HS CODE 9004-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 15 NUMBER OF PATENTS APPLIED AND GRANTED, 2013-2023

- TABLE 16 LIST OF PATENTS, 2022-2023

- TABLE 17 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 21 LIST OF CONFERENCES AND EVENTS, 2024-2025

- TABLE 22 AUGMENTED AND VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 23 AUGMENTED AND VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 24 COMPARISON BETWEEN MARKER-BASED AND MARKERLESS AUGMENTED REALITY TECHNOLOGY

- TABLE 25 AUGMENTED REALITY MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 26 AUGMENTED REALITY MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 27 VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 28 VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 29 AUGMENTED REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 30 AUGMENTED REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 31 VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 32 VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 33 HARDWARE: AUGMENTED REALITY MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 34 HARDWARE: AUGMENTED REALITY MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- TABLE 35 HARDWARE: AUGMENTED REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 36 HARDWARE: AUGMENTED REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 37 HARDWARE: VIRTUAL REALITY MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 38 HARDWARE: VIRTUAL REALITY MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- TABLE 39 HARDWARE: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 40 HARDWARE: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 41 SOFTWARE: AUGMENTED REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 42 SOFTWARE: AUGMENTED REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 43 SOFTWARE: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 44 SOFTWARE: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 45 AUGMENTED REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 46 AUGMENTED REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- TABLE 47 AUGMENTED REALITY MARKET, BY DEVICE TYPE, 2020-2023 (THOUSAND UNITS)

- TABLE 48 AUGMENTED REALITY MARKET, BY DEVICE TYPE, 2024-2029 (THOUSAND UNITS)

- TABLE 49 VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 50 VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- TABLE 51 VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (THOUSAND UNITS)

- TABLE 52 VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (THOUSAND UNITS)

- TABLE 53 AUGMENTED REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 54 AUGMENTED REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 55 CONSUMER: AUGMENTED REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 56 CONSUMER: AUGMENTED REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 57 CONSUMER: AUGMENTED REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 58 CONSUMER: AUGMENTED REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 59 USE CASES OF AUGMENTED REALITY IN CONSUMER APPLICATIONS

- TABLE 60 COMMERCIAL: AUGMENTED REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 61 COMMERCIAL: AUGMENTED REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 62 COMMERCIAL: AUGMENTED REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 63 COMMERCIAL: AUGMENTED REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 64 USE CASES OF AUGMENTED REALITY IN COMMERCIAL APPLICATIONS

- TABLE 65 ENTERPRISE: AUGMENTED REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 66 ENTERPRISE: AUGMENTED REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 67 ENTERPRISE: AUGMENTED REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 68 ENTERPRISE: AUGMENTED REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 69 USE CASES OF AUGMENTED REALITY IN ENTERPRISE APPLICATIONS

- TABLE 70 HEALTHCARE: AUGMENTED REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 71 HEALTHCARE: AUGMENTED REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 72 HEALTHCARE: AUGMENTED REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 73 HEALTHCARE: AUGMENTED REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 74 USE CASES OF AUGMENTED REALITY IN HEALTHCARE APPLICATIONS

- TABLE 75 AEROSPACE & DEFENSE: AUGMENTED REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 76 AEROSPACE & DEFENSE: AUGMENTED REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 77 AEROSPACE & DEFENSE: AUGMENTED REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 78 AEROSPACE & DEFENSE: AUGMENTED REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 79 USE CASES OF AUGMENTED REALITY IN AEROSPACE & DEFENSE APPLICATIONS

- TABLE 80 ENERGY: AUGMENTED REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 81 ENERGY: AUGMENTED REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 82 ENERGY: AUGMENTED REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 83 ENERGY: AUGMENTED REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 84 USE CASES OF AUGMENTED REALITY IN ENERGY APPLICATIONS

- TABLE 85 AUTOMOTIVE: AUGMENTED REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 86 AUTOMOTIVE: AUGMENTED REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 87 AUTOMOTIVE: AUGMENTED REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 88 AUTOMOTIVE: AUGMENTED REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 89 USE CASES OF AUGMENTED REALITY IN AUTOMOTIVE APPLICATIONS

- TABLE 90 OTHER AR APPLICATIONS: AUGMENTED REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 91 OTHER AR APPLICATIONS: AUGMENTED REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 92 OTHER AR APPLICATIONS: AUGMENTED REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 93 OTHER AR APPLICATIONS: AUGMENTED REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 94 USE CASES OF AUGMENTED REALITY IN OTHER AR APPLICATIONS

- TABLE 95 VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 96 VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 97 CONSUMER: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 98 CONSUMER: VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 99 CONSUMER: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 100 CONSUMER: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 101 USE CASES OF VIRTUAL REALITY IN CONSUMER APPLICATIONS

- TABLE 102 COMMERCIAL: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 103 COMMERCIAL: VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 104 COMMERCIAL: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 105 COMMERCIAL: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 106 USE CASES OF VIRTUAL REALITY IN COMMERCIAL APPLICATIONS

- TABLE 107 ENTERPRISE: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 108 ENTERPRISE: VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 109 ENTERPRISE: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 110 ENTERPRISE: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 111 USE CASES OF VIRTUAL REALITY IN ENTERPRISE APPLICATIONS

- TABLE 112 HEALTHCARE: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 113 HEALTHCARE: VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 114 HEALTHCARE: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 115 HEALTHCARE: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 116 USE CASES OF VIRTUAL REALITY IN HEALTHCARE APPLICATIONS

- TABLE 117 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 118 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 119 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 120 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 121 USE CASES OF VIRTUAL REALITY IN AEROSPACE & DEFENSE APPLICATIONS

- TABLE 122 OTHER VR APPLICATIONS: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 123 OTHER VR APPLICATIONS: VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 124 OTHER VR APPLICATIONS: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 125 OTHER VR APPLICATIONS: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 126 USE CASES OF VIRTUAL REALITY IN OTHER APPLICATIONS

- TABLE 127 AUGMENTED REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 128 AUGMENTED REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 129 VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 130 VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 131 NORTH AMERICA: AUGMENTED REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 132 NORTH AMERICA: AUGMENTED REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 133 NORTH AMERICA: AUGMENTED REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 134 NORTH AMERICA: AUGMENTED REALITY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 135 NORTH AMERICA: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 136 NORTH AMERICA: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 137 NORTH AMERICA: VIRTUAL REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 138 NORTH AMERICA: VIRTUAL REALITY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 139 EUROPE: AUGMENTED REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 140 EUROPE: AUGMENTED REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 141 EUROPE: AUGMENTED REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 142 EUROPE: AUGMENTED REALITY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 143 EUROPE: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 144 EUROPE: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 145 EUROPE: VIRTUAL REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 146 EUROPE: VIRTUAL REALITY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 147 ASIA PACIFIC: AUGMENTED REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 148 ASIA PACIFIC: AUGMENTED REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 149 ASIA PACIFIC: AUGMENTED REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 150 ASIA PACIFIC: AUGMENTED REALITY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 151 ASIA PACIFIC: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 152 ASIA PACIFIC: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 153 ASIA PACIFIC: VIRTUAL REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 154 ASIA PACIFIC: VIRTUAL REALITY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 155 ROW: AUGMENTED REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 156 ROW: AUGMENTED REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 157 ROW: AUGMENTED REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 158 ROW: AUGMENTED REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 159 MIDDLE EAST & AFRICA: AUGMENTED REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 160 MIDDLE EAST & AFRICA: AUGMENTED REALITY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 161 ROW: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 162 ROW: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 163 ROW: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 164 ROW: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 165 MIDDLE EAST & AFRICA: VIRTUAL REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 166 MIDDLE EAST & AFRICA: VIRTUAL REALITY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 167 AUGMENTED AND VIRTUAL REALITY MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, 2019-2024

- TABLE 168 MARKET SHARE ANALYSIS OF KEY COMPANIES OFFERING AUGMENTED AND VIRTUAL REALITY TECHNOLOGIES, 2023

- TABLE 169 AUGMENTED AND VIRTUAL REALITY MARKET: TECHNOLOGY FOOTPRINT

- TABLE 170 AUGMENTED AND VIRTUAL REALITY MARKET: OFFERING FOOTPRINT

- TABLE 171 AUGMENTED AND VIRTUAL REALITY MARKET: DEVICE TYPE FOOTPRINT

- TABLE 172 AUGMENTED AND VIRTUAL REALITY MARKET: APPLICATION FOOTPRINT

- TABLE 173 AUGMENTED AND VIRTUAL REALITY MARKET: REGION FOOTPRINT

- TABLE 174 AUGMENTED AND VIRTUAL REALITY MARKET: DETAILED LIST OF KEY STARTUP/SMES

- TABLE 175 AUGMENTED AND VIRTUAL REALITY MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 176 AUGMENTED AND VIRTUAL REALITY MARKET: PRODUCT LAUNCHES, DECEMBER 2019-JUNE 2024

- TABLE 177 AUGMENTED AND VIRTUAL REALITY MARKET: DEALS, DECEMBER 2019-JUNE 2024

- TABLE 178 AUGMENTED AND VIRTUAL REALITY MARKET: EXPANSIONS, DECEMBER 2019-JUNE 2024

- TABLE 179 AUGMENTED AND VIRTUAL REALITY MARKET: OTHERS, DECEMBER 2019-JUNE 2024

- TABLE 180 META: COMPANY OVERVIEW

- TABLE 181 META: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 182 META: PRODUCT LAUNCHES

- TABLE 183 META: DEALS

- TABLE 184 SONY CORPORATION: COMPANY OVERVIEW

- TABLE 185 SONY CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 186 SONY CORPORATION: PRODUCT LAUNCHES

- TABLE 187 SONY CORPORATION: DEALS

- TABLE 188 SONY CORPORATION: EXPANSIONS

- TABLE 189 APPLE INC.: COMPANY OVERVIEW

- TABLE 190 APPLE INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 191 APPLE INC.: PRODUCT LAUNCHES

- TABLE 192 BYTEDANCE: COMPANY OVERVIEW

- TABLE 193 BYTEDANCE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 194 BYTEDANCE: PRODUCT LAUNCHES

- TABLE 195 BYTEDANCE: DEALS

- TABLE 196 DPVR: COMPANY OVERVIEW

- TABLE 197 DPVR: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 198 DPVR: PRODUCT LAUNCHES

- TABLE 199 DPVR: DEALS

- TABLE 200 HTC CORPORATION: COMPANY OVERVIEW

- TABLE 201 HTC CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 202 HTC CORPORATION: PRODUCT LAUNCHES

- TABLE 203 HTC CORPORATION: DEALS

- TABLE 204 GOOGLE: COMPANY OVERVIEW

- TABLE 205 GOOGLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 206 GOOGLE: PRODUCT LAUNCHES

- TABLE 207 GOOGLE: DEALS

- TABLE 208 MICROSOFT: COMPANY OVERVIEW

- TABLE 209 MICROSOFT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 210 MICROSOFT: PRODUCT LAUNCHES

- TABLE 211 MICROSOFT: DEALS

- TABLE 212 MICROSOFT: OTHERS

- TABLE 213 SAMSUNG: COMPANY OVERVIEW

- TABLE 214 SAMSUNG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 215 SAMSUNG: PRODUCT LAUNCHES

- TABLE 216 SAMSUNG: DEALS

- TABLE 217 PTC: COMPANY OVERVIEW

- TABLE 218 PTC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 219 PTC: DEALS

- TABLE 220 SEIKO EPSON CORPORATION: COMPANY OVERVIEW

- TABLE 221 SEIKO EPSON CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 222 SEIKO EPSON CORPORATION: PRODUCT LAUNCHES

- TABLE 223 LENOVO: COMPANY OVERVIEW

- TABLE 224 LENOVO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 225 LENOVO: PRODUCT LAUNCHES

- TABLE 226 LENOVO: DEALS

List of Figures

- FIGURE 1 AUGMENTED REALITY MARKET SEGMENTATION

- FIGURE 2 VIRTUAL REALITY MARKET SEGMENTATION

- FIGURE 3 AUGMENTED REALITY MARKET: RESEARCH DESIGN

- FIGURE 4 VIRTUAL REALITY MARKET: RESEARCH DESIGN

- FIGURE 5 AUGMENTED AND VIRTUAL REALITY MARKET: BOTTOM-UP APPROACH

- FIGURE 6 AUGMENTED AND VIRTUAL REALITY MARKET: TOP-DOWN APPROACH

- FIGURE 7 AUGMENTED AND VIRTUAL REALITY MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE ANALYSIS (APPROACH 1)

- FIGURE 8 AUGMENTED AND VIRTUAL REALITY MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE ANALYSIS (APPROACH 2)

- FIGURE 9 AUGMENTED AND VIRTUAL REALITY MARKET: DATA TRIANGULATION

- FIGURE 10 AUGMENTED REALITY MARKET SNAPSHOT

- FIGURE 11 VIRTUAL REALITY MARKET SNAPSHOT

- FIGURE 12 SOFTWARE SEGMENT TO DOMINATE AUGMENTED REALITY MARKET BETWEEN 2024 AND 2029

- FIGURE 13 SOFTWARE SEGMENT TO ACCOUNT FOR LARGER SHARE OF VIRTUAL REALITY MARKET IN 2024

- FIGURE 14 AUGMENTED REALITY SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE IN 2029

- FIGURE 15 HEAD-MOUNTED DISPLAYS SEGMENT TO REGISTER HIGHER CAGR IN AUGMENTED REALITY MARKET DURING FORECAST PERIOD

- FIGURE 16 GESTURE-TRACKING DEVICES SEGMENT TO EXHIBIT HIGHEST CAGR IN VIRTUAL REALITY MARKET DURING FORECAST PERIOD

- FIGURE 17 ENTERPRISE SEGMENT TO ACCOUNT FOR LARGEST SHARE OF AUGMENTED REALITY MARKET IN 2029

- FIGURE 18 CONSUMER SEGMENT TO DOMINATE VIRTUAL REALITY MARKET FROM 2024 TO 2029

- FIGURE 19 NORTH AMERICA HELD LARGEST SHARE OF AUGMENTED REALITY MARKET IN 2023

- FIGURE 20 ASIA PACIFIC TO EXHIBIT HIGHEST CAGR IN VIRTUAL REALITY MARKET DURING FORECAST PERIOD

- FIGURE 21 RAPID ADVANCEMENT IN GAMING TECHNOLOGIES TO CONTRIBUTE TO AUGMENTED REALITY MARKET GROWTH

- FIGURE 22 RISING NEED FOR INNOVATIVE TECHNOLOGIES TO SUPPORT REMOTE WORK TO DRIVE VIRTUAL REALITY MARKET

- FIGURE 23 ENTERPRISE SEGMENT TO ACCOUNT FOR LARGEST SHARE OF AUGMENTED REALITY MARKET IN 2029

- FIGURE 24 CONSUMER SEGMENT TO HOLD LARGEST SHARE OF VIRTUAL REALITY MARKET IN 2024

- FIGURE 25 SOFTWARE SEGMENT TO ACCOUNT FOR LARGEST SHARE OF AUGMENTED REALITY MARKET IN 2029

- FIGURE 26 SOFTWARE SEGMENT TO DOMINATE VIRTUAL REALITY MARKET DURING FORECAST PERIOD

- FIGURE 27 HEAD-MOUNTED DISPLAYS SEGMENT TO ACCOUNT FOR LARGEST SHARE OF AUGMENTED REALITY MARKET IN 2024

- FIGURE 28 HEAD-MOUNTED DISPLAYS SEGMENT TO DOMINATE VIRTUAL REALITY MARKET BETWEEN 2024 AND 2029

- FIGURE 29 AUGMENTED REALITY SEGMENT TO HOLD LARGER MARKET SHARE IN 2029

- FIGURE 30 ENTERPRISE AND CHINA TO HOLD LARGEST SHARES OF AUGMENTED REALITY MARKET IN ASIA PACIFIC IN 2024

- FIGURE 31 CONSUMER AND CHINA TO ACCOUNT FOR LARGEST SHARES OF VIRTUAL REALITY MARKET IN ASIA PACIFIC IN 2024

- FIGURE 32 AUGMENTED REALITY MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 33 AUGMENTED REALITY MARKET IMPACT ANALYSIS: DRIVERS

- FIGURE 34 AUGMENTED REALITY MARKET IMPACT ANALYSIS: RESTRAINTS

- FIGURE 35 AUGMENTED REALITY MARKET IMPACT ANALYSIS: OPPORTUNITIES

- FIGURE 36 AUGMENTED REALITY MARKET IMPACT ANALYSIS: CHALLENGES

- FIGURE 37 VIRTUAL REALITY MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 38 VIRTUAL REALITY MARKET IMPACT ANALYSIS: DRIVERS

- FIGURE 39 VIRTUAL REALITY MARKET IMPACT ANALYSIS: RESTRAINTS

- FIGURE 40 VIRTUAL REALITY MARKET IMPACT ANALYSIS: OPPORTUNITIES

- FIGURE 41 VIRTUAL REALITY MARKET IMPACT ANALYSIS: CHALLENGES

- FIGURE 42 AUGMENTED AND VIRTUAL REALITY MARKET: VALUE CHAIN ANALYSIS

- FIGURE 43 AUGMENTED AND VIRTUAL REALITY ECOSYSTEM

- FIGURE 44 INVESTMENT AND FUNDING SCENARIO, 2019-2024 (USD MILLION)

- FIGURE 45 AUGMENTED AND VIRTUAL REALITY MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 46 AVERAGE SELLING PRICE TREND OF AUGMENTED REALITY DEVICES OFFERED BY KEY PLAYERS (USD)

- FIGURE 47 AVERAGE SELLING PRICE TREND OF VIRTUAL REALITY DEVICES OFFERED BY KEY PLAYERS (USD)

- FIGURE 48 AVERAGE SELLING PRICE TREND OF AUGMENTED REALITY DEVICES, 2020-2023 (USD)

- FIGURE 49 AVERAGE SELLING PRICE TREND OF VIRTUAL REALITY DEVICES, 2020-2023 (USD)

- FIGURE 50 AVERAGE SELLING PRICE TREND OF VR HEAD-MOUNTED DISPLAYS, BY REGION, 2020-2023 (USD)

- FIGURE 51 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 52 IMPACT OF PORTER'S FIVE FORCES ON AUGMENTED AND VIRTUAL REALITY MARKET, 2023

- FIGURE 53 AUGMENTED AND VIRTUAL REALITY MARKET: INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP TWO APPLICATIONS

- FIGURE 54 AUGMENTED AND VIRTUAL REALITY MARKET: KEY BUYING CRITERIA FOR TOP TWO APPLICATIONS

- FIGURE 55 IMPACT OF AI/GEN AI ON AUGMENTED AND VIRTUAL REALITY MARKET

- FIGURE 56 IMPORT DATA FOR HS CODE 9004-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023

- FIGURE 57 EXPORT DATA FOR HS CODE 9004-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023

- FIGURE 58 AUGMENTED AND VIRTUAL REALITY MARKET: PATENTS APPLIED AND GRANTED, 2013-2023

- FIGURE 59 AUGMENTED REALITY SEGMENT TO CAPTURE MAJORITY OF MARKET SHARE IN 2029

- FIGURE 60 MARKERLESS SEGMENT TO DOMINATE AUGMENTED REALITY MARKET FROM 2024 TO 2029

- FIGURE 61 SEMI & FULLY IMMERSIVE SEGMENT TO DOMINATE VIRTUAL REALITY MARKET BETWEEN 2024 AND 2029

- FIGURE 62 HARDWARE SEGMENT TO EXHIBIT HIGHER CAGR IN AUGMENTED REALITY MARKET BETWEEN 2024 AND 2029

- FIGURE 63 SOFTWARE SEGMENT TO DOMINATE VIRTUAL REALITY MARKET DURING FORECAST PERIOD

- FIGURE 64 DISPLAYS & PROJECTORS SEGMENT TO HOLD LARGEST SHARE OF AUGMENTED REALITY MARKET IN 2029

- FIGURE 65 DISPLAYS & PROJECTORS SEGMENT TO RECORD HIGHEST CAGR IN VIRTUAL REALITY MARKET DURING FORECAST PERIOD

- FIGURE 66 HEAD-MOUNTED DISPLAYS SEGMENT TO ACCOUNT FOR LARGER SHARE OF AUGMENTED REALITY MARKET IN 2029

- FIGURE 67 GESTURE-TRACKING DEVICES SEGMENT TO REGISTER HIGHEST CAGR IN VIRTUAL REALITY MARKET FROM 2024 TO 2029

- FIGURE 68 CONSUMER SEGMENT TO EXHIBIT HIGHEST CAGR IN AUGMENTED REALITY MARKET DURING FORECAST PERIOD

- FIGURE 69 CONSUMER SEGMENT TO CAPTURE LARGEST SHARE OF VIRTUAL REALITY MARKET IN 2024

- FIGURE 70 INDIA TO EXHIBIT HIGHEST CAGR IN GLOBAL AUGMENTED REALITY MARKET DURING FORECAST PERIOD

- FIGURE 71 CHINA TO RECORD HIGHEST CAGR IN GLOBAL VIRTUAL REALITY MARKET BETWEEN 2024 AND 2029

- FIGURE 72 NORTH AMERICA: AUGMENTED REALITY MARKET SNAPSHOT

- FIGURE 73 NORTH AMERICA: VIRTUAL REALITY MARKET SNAPSHOT

- FIGURE 74 EUROPE: AUGMENTED REALITY MARKET SNAPSHOT

- FIGURE 75 EUROPE: VIRTUAL REALITY MARKET SNAPSHOT

- FIGURE 76 ASIA PACIFIC: AUGMENTED REALITY MARKET SNAPSHOT

- FIGURE 77 ASIA PACIFIC: VIRTUAL REALITY MARKET SNAPSHOT

- FIGURE 78 AUGMENTED AND VIRTUAL REALITY MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, 2019-2024

- FIGURE 79 MARKET SHARE ANALYSIS OF KEY COMPANIES OFFERING AUGMENTED AND VIRTUAL REALITY TECHNOLOGIES, 2023

- FIGURE 80 COMPANY VALUATION, 2023 (USD MILLION)

- FIGURE 81 FINANCIAL METRICS, 2024 (EV/EBITDA)

- FIGURE 82 BRAND/PRODUCT COMPARISON

- FIGURE 83 AUGMENTED AND VIRTUAL REALITY MARKET: REVENUE ANALYSIS OF THREE KEY PLAYERS, 2020-2023 (USD BILLION)

- FIGURE 84 AUGMENTED AND VIRTUAL REALITY MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- FIGURE 85 AUGMENTED AND VIRTUAL REALITY MARKET: COMPANY FOOTPRINT

- FIGURE 86 AUGMENTED AND VIRTUAL REALITY MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

- FIGURE 87 META: COMPANY SNAPSHOT

- FIGURE 88 SONY CORPORATION: COMPANY SNAPSHOT

- FIGURE 89 APPLE INC.: COMPANY SNAPSHOT

- FIGURE 90 HTC CORPORATION: COMPANY SNAPSHOT

- FIGURE 91 GOOGLE: COMPANY SNAPSHOT

- FIGURE 92 MICROSOFT: COMPANY SNAPSHOT

- FIGURE 93 SAMSUNG: COMPANY SNAPSHOT

- FIGURE 94 PTC: COMPANY SNAPSHOT

- FIGURE 95 SEIKO EPSON CORPORATION: COMPANY SNAPSHOT

- FIGURE 96 LENOVO: COMPANY SNAPSHOT

The Augmented and Virtual Reality Market was valued at USD 22.12 billion in 2024 and is expected to reach USD $96.32 billion by 2029, at a CAGR of 34.2% during the 2024-2029 period. The major factors driving the growth of augmented and virtual reality market includes the surging AR developer ecosystem, and presence of budget-friendly VR devices. Moreover, the ongoing government initiatives and investments towards the wide adoption, and research and development of AR and VR technologies is expected to provide several growth opportunities for market players in the augmented and virtual reality market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion) |

| Segments | By Enterprise, Technology, Offering, Application and Region |

| Regions covered | North America, Europe, APAC, RoW |

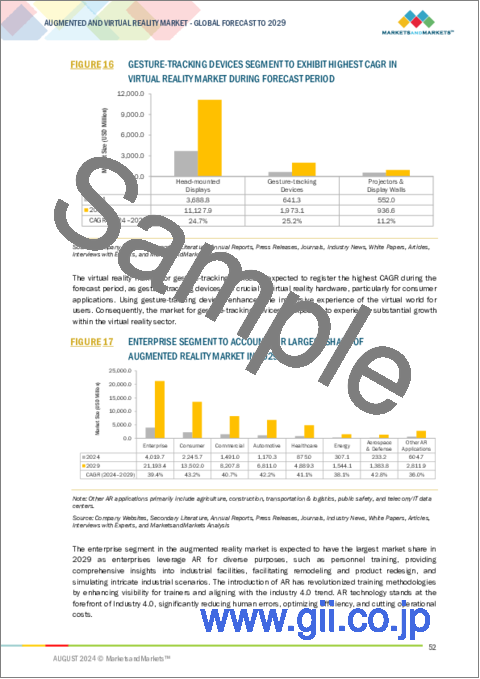

Semi & Fully immersive technology is expected to register higher CAGR in the virtual reality market during the forecast period

The virtual reality market for semi & fully immersive technology is expected to register higher CAGR during the forecast period which is attributed to the increasing adoption of semi immersive technology in simulation training and virtual walkthroughs, and the increasing demand for fully immersive technology as they deliver high level of engagement which completely transports users into a digital environment to an extent that they lose awareness of their physical surroundings, which is highly preferrable in high-end gaming, medical simulations, virtual tours and architectural designs.

Software segment is expected to have the largest market size during the forecast period

The augmented and virtual reality software is expected to have the largest market size during the forecast period. This is attributed to the emerging projects that are transitioning into large-scale implementations. Major companies like IKEA and Walmart have launched their AR prototypes that aims at enhancing customer shopping experiences which reflects the ongoing experimentation in this sector. On the other hand, VR software plays a crucial role in manufacturing software development kits which is accelerated by mass consumerism. For instance, SDKs that highly support VR technology are REALITY SDK, Virtual Reality Tool Kit (VRTK), PlayStation Virtual Reality (PSVR) dev kit, Oculus SDK, and Google Virtual Reality SDK. Furthermore, VR software also provides cloud-based services that are used to compare captured images with a database, delivering relevant information back to the mobile device, which then handles image processing, including detection, resizing, and generating 3D images.

The break-up of profile of primary participants in the augmented and virtual reality market-

- By Company Type: Tier 1 - 15%, Tier 2 - 50%, Tier 3 - 20%

- By Designation Type: C Level - 45%, Director Level - 35%, Others - 20%

- By Region Type: North America - 45%, Europe - 35%, Asia Pacific - 12%, Rest of the World (RoW) - 8%

The major players of the augmented and virtual reality market are Meta. (US), Sony Group Corporation (Japan), Apple Inc. (US), ByteDance (China), and DPVR (China) among others.

Research Coverage

The report segments the augmented and virtual reality market and forecasts its size based on technology, offering, device type, application, and region. The report also provides a comprehensive review of drivers, restraints, opportunities, and challenges influencing market growth. The report also covers qualitative aspects in addition to the quantitative aspects of the market.

Reasons to buy the report:

The report will help the market leaders/new entrants in this market with information on the closest approximate revenues for the overall augmented and virtual reality market and related segments. This report will help stakeholders understand the competitive landscape and gain more insights to strengthen their position in the market and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (surging AR developer ecosystem, and presence of budget-friendly VR devices), restraints (high costs of AR technology, and presence of technological limitations), opportunities (ongoing government initiatives and investments towards the wide adoption, and research and development of AR and VR technologies), and challenges (display latency issues in AR and VR, high energy consumption in VR and limited field of vision in AR) influencing the growth of the augmented and virtual reality market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches, product development, partnerships, collaborations, contracts, joint investments, strategic supplier relationships, and expansions in the augmented and virtual reality market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the augmented and virtual reality market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the augmented and virtual reality market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and product offerings of leading players like Meta. (US), Sony Group Corporation (Japan), Apple Inc. (US), ByteDance (China), and DPVR (China).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 REGIONAL SCOPE

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.3.4 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 List of primary interview participants

- 2.1.2.2 Breakdown of primaries

- 2.1.2.3 Key data from primary sources

- 2.1.2.4 Key industry insights

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION METHODOLOGY

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 FORECAST

- 2.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUGMENTED REALITY MARKET

- 4.2 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN VIRTUAL REALITY MARKET

- 4.3 AUGMENTED REALITY MARKET, BY APPLICATION

- 4.4 VIRTUAL REALITY MARKET, BY APPLICATION

- 4.5 AUGMENTED REALITY MARKET, BY OFFERING

- 4.6 VIRTUAL REALITY MARKET, BY OFFERING

- 4.7 AUGMENTED REALITY MARKET, BY DEVICE TYPE

- 4.8 VIRTUAL REALITY MARKET, BY DEVICE TYPE

- 4.9 AUGMENTED AND VIRTUAL REALITY MARKET, BY TECHNOLOGY

- 4.10 AUGMENTED REALITY MARKET IN ASIA PACIFIC, BY APPLICATION AND COUNTRY

- 4.11 VIRTUAL REALITY MARKET IN ASIA PACIFIC, BY APPLICATION AND COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS: AUGMENTED REALITY MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Rising integration of virtual game elements to foster real-world interactions

- 5.2.1.2 Growing emphasis on providing immersive shopping experiences

- 5.2.1.3 Increasing use of AR technology in industrial sectors

- 5.2.2 RESTRAINTS

- 5.2.2.1 High implementation costs of AR technology

- 5.2.2.2 Security and privacy concerns

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Surging deployment of AR devices to improve medical procedures

- 5.2.3.2 Increasing spending on in-car technologies with surging demand for safer vehicles

- 5.2.4 CHALLENGES

- 5.2.4.1 Display latency and limited field of view

- 5.2.4.2 Flexibility and compatibility issues

- 5.2.1 DRIVERS

- 5.3 MARKET DYNAMICS: VIRTUAL REALITY MARKET

- 5.3.1 DRIVERS

- 5.3.1.1 Rising integration of advanced haptic feedback tools to improve VR experiences

- 5.3.1.2 Growing focus on improving collaboration and communication

- 5.3.1.3 Increasing availability of budget-friendly VR devices

- 5.3.2 RESTRAINTS

- 5.3.2.1 Weight distribution and ergonomic design flaws

- 5.3.3 OPPORTUNITIES

- 5.3.3.1 Rising popularity of remote medical consultations and telemedicine

- 5.3.3.2 Surging investments in VR hardware components

- 5.3.4 CHALLENGES

- 5.3.4.1 High energy consumption

- 5.3.4.2 Display resolution issues

- 5.3.1 DRIVERS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 INVESTMENT AND FUNDING SCENARIO

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 AR smart glasses

- 5.8.1.2 VR-based microdisplays

- 5.8.1.3 Mobile AR

- 5.8.1.4 Near-eye displays

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 AR-powered displays

- 5.8.2.2 AR/VR-based monitors

- 5.8.2.3 Web-based AR

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Metaverse

- 5.8.1 KEY TECHNOLOGIES

- 5.9 PRICING ANALYSIS

- 5.9.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY DEVICE TYPE

- 5.9.2 AVERAGE SELLING PRICE TREND, BY DEVICE TYPE

- 5.9.3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.10 PORTER'S FIVE FORCES ANALYSIS

- 5.10.1 THREAT OF NEW ENTRANTS

- 5.10.2 THREAT OF SUBSTITUTES

- 5.10.3 BARGAINING POWER OF SUPPLIERS

- 5.10.4 BARGAINING POWER OF BUYERS

- 5.10.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.11 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.11.2 BUYING CRITERIA

- 5.12 IMPACT OF AI/GEN AI ON AUGMENTED AND VIRTUAL REALITY MARKET

- 5.13 CASE STUDY ANALYSIS

- 5.13.1 HTC CORPORATION SUPPORTS FLAIM TRAINER VR SIMULATION TO REDUCE COSTS OF TRAINING FIREFIGHTERS

- 5.13.2 VOLKSWAGEN LEVERAGES AR AND VR TECHNOLOGIES TO ADDRESS CHALLENGES ASSOCIATED WITH IN-PERSON COLLABORATION

- 5.13.3 HTC CORPORATION IMPLEMENTS IMMERSIVE VR SOLUTION TO ENABLE REMOTE COLLABORATION OF AUTOMOTIVE DESIGN TEAMS

- 5.13.4 META COLLABORATES WITH BMW TO REVOLUTIONIZE IN-CAR EXPERIENCES IN SMART VEHICLES

- 5.14 TRADE ANALYSIS

- 5.14.1 IMPORT SCENARIO (HS CODE 9004)

- 5.14.2 EXPORT SCENARIO (HS CODE 9004)

- 5.15 PATENT ANALYSIS

- 5.16 REGULATORY LANDSCAPE

- 5.16.1 REGULATORY BODY, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.16.2 REGULATIONS

- 5.17 KEY CONFERENCES AND EVENTS, 2024-2025

6 ENTERPRISES DEVELOPING AUGMENTED AND VIRTUAL REALITY TECHNOLOGIES

- 6.1 INTRODUCTION

- 6.2 SMALL-SIZED ENTERPRISES

- 6.3 MEDIUM-SIZED ENTERPRISES

- 6.4 LARGE ENTERPRISES

7 AUGMENTED AND VIRTUAL REALITY MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- 7.2 AUGMENTED REALITY

- 7.2.1 MARKER-BASED

- 7.2.1.1 Increasing need for cost-effective and reliable technology to drive market

- 7.2.1.2 Passive marker

- 7.2.1.3 Active marker

- 7.2.2 MARKERLESS

- 7.2.2.1 Mounting demand for smartphones and tablets to fuel segmental growth

- 7.2.2.2 Model-based tracking

- 7.2.2.3 Image processing-based tracking

- 7.2.3 ANCHOR-BASED

- 7.2.3.1 Growing need to effectively overlay virtual images for real-world detection to augment segmental growth

- 7.2.1 MARKER-BASED

- 7.3 VIRTUAL REALITY

- 7.3.1 NON-IMMERSIVE

- 7.3.1.1 Cost-effectiveness and ease of implementation to expedite segmental growth

- 7.3.2 SEMI & FULLY IMMERSIVE

- 7.3.2.1 Adoption in high-end gaming and medical simulations to fuel segmental growth

- 7.3.1 NON-IMMERSIVE

8 AUGMENTED AND VIRTUAL REALITY MARKET, BY OFFERING

- 8.1 INTRODUCTION

- 8.2 HARDWARE

- 8.2.1 SENSORS

- 8.2.1.1 Rising emphasis on seamless interaction between users and virtual environments to augment segmental growth

- 8.2.2 SEMICONDUCTOR COMPONENTS

- 8.2.2.1 Increasing adoption of controllers in smartphones and tablets to deliver immersive interactions to boost segmental growth

- 8.2.3 DISPLAYS & PROJECTORS

- 8.2.3.1 Rapid advancement in optical technology to contribute to segmental growth

- 8.2.4 POSITION/ROOM TRACKERS

- 8.2.4.1 Growing emphasis on obtaining accurate and stable object monitoring results to fuel segmental growth

- 8.2.5 CAMERAS

- 8.2.5.1 Rising need to measure depth and amplitude of objects in virtual spaces to accelerate segmental growth

- 8.2.6 OTHER HARDWARE COMPONENTS

- 8.2.1 SENSORS

- 8.3 SOFTWARE

- 8.3.1 INCREASING FOCUS ON SEAMLESSLY INTEGRATING DIGITAL INFORMATION WITH REAL-WORLD ENVIRONMENTS TO FOSTER SEGMENTAL GROWTH

- 8.3.2 BY FUNCTION

- 8.3.2.1 Remote collaboration

- 8.3.2.2 Workflow optimization

- 8.3.2.3 Documentation

- 8.3.2.4 Visualization

- 8.3.2.5 3D modeling

- 8.3.2.6 Navigation

9 AUGMENTED AND VIRTUAL REALITY MARKET, BY DEVICE TYPE

- 9.1 INTRODUCTION

- 9.2 AUGMENTED REALITY DEVICES

- 9.2.1 HEAD-MOUNTED DISPLAYS

- 9.2.1.1 Use in navigation and gaming to provide interactive experiences to foster segmental growth

- 9.2.1.2 Smart glasses

- 9.2.1.3 Smart helmets

- 9.2.2 HEAD-UP DISPLAYS

- 9.2.2.1 Integration into automobiles to provide safety alerts to contribute to segmental growth

- 9.2.1 HEAD-MOUNTED DISPLAYS

- 9.3 VIRTUAL REALITY DEVICES

- 9.3.1 HEAD-MOUNTED DISPLAYS

- 9.3.1.1 Demand for immersive entertainment and gaming experiences to boost segmental growth

- 9.3.2 GESTURE-TRACKING DEVICES

- 9.3.2.1 Utilization in rehabilitation and physical therapy to accelerate segmental growth

- 9.3.2.1.1 Data gloves

- 9.3.2.1.2 Other gesture-tracking devices

- 9.3.2.1 Utilization in rehabilitation and physical therapy to accelerate segmental growth

- 9.3.3 PROJECTORS & DISPLAY WALLS

- 9.3.3.1 Adoption to create large-scale visualizations to fuel segmental growth

- 9.3.1 HEAD-MOUNTED DISPLAYS

10 AUGMENTED AND VIRTUAL REALITY MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 AUGMENTED REALITY APPLICATIONS

- 10.2.1 CONSUMER

- 10.2.1.1 Emphasis on creating impressive visual effects in gaming and sports broadcasts to augment segmental growth

- 10.2.1.2 Gaming

- 10.2.1.3 Sports & entertainment

- 10.2.1.3.1 Archaeological sites

- 10.2.1.3.2 Theme parks

- 10.2.1.3.3 Art galleries & exhibitions

- 10.2.2 COMMERCIAL

- 10.2.2.1 Rise in internet access and online sales to contribute to segmental growth

- 10.2.2.2 Retail & e-commerce

- 10.2.2.2.1 Jewelry

- 10.2.2.2.2 Beauty & cosmetics

- 10.2.2.2.3 Apparel fitting

- 10.2.2.2.4 Grocery shopping

- 10.2.2.2.5 Footwear

- 10.2.2.2.6 Furniture & lighting design

- 10.2.2.3 Travel & tourism

- 10.2.2.4 E-learning

- 10.2.3 ENTERPRISE

- 10.2.3.1 Adoption to enhance training by reducing human errors and optimizing efficiency to expedite segmental growth

- 10.2.4 HEALTHCARE

- 10.2.4.1 Increased demand for advanced imaging equipment to boost segmental growth

- 10.2.4.2 Surgery

- 10.2.4.3 Fitness management

- 10.2.4.4 Patient care management

- 10.2.4.5 Pharmacy management

- 10.2.4.6 Medical training & education

- 10.2.4.7 Other healthcare applications

- 10.2.5 AEROSPACE & DEFENSE

- 10.2.5.1 Need for quick identification of aircraft defects and damage to augment segmental growth

- 10.2.6 ENERGY

- 10.2.6.1 Strong focus on ensuring compliance with safety regulations to foster segmental growth

- 10.2.7 AUTOMOTIVE

- 10.2.7.1 Adoption of advanced driver-assistance systems to enhance road safety to drive market

- 10.2.8 OTHER AR APPLICATIONS

- 10.2.8.1 Agriculture

- 10.2.8.2 Construction

- 10.2.8.3 Transportation & logistics

- 10.2.8.4 Public safety

- 10.2.8.5 Telecom/IT data centers

- 10.2.1 CONSUMER

- 10.3 VIRTUAL REALITY APPLICATIONS

- 10.3.1 CONSUMER

- 10.3.1.1 Increasing focus on enhancing user experiences by gaming & entertainment companies to boost segmental growth

- 10.3.1.2 Gaming & entertainment

- 10.3.1.3 Sports

- 10.3.2 COMMERCIAL

- 10.3.2.1 Rising emphasis on effective marketing and advertising to contribute to segmental growth

- 10.3.2.1.1 Retail & e-commerce

- 10.3.2.1.2 Education & training

- 10.3.2.1.3 Travel & tourism

- 10.3.2.1.4 Advertising

- 10.3.2.1 Rising emphasis on effective marketing and advertising to contribute to segmental growth

- 10.3.3 ENTERPRISE

- 10.3.3.1 Increasing requirement for advanced technologies to support training and simulation to accelerate segmental growth

- 10.3.4 HEALTHCARE

- 10.3.4.1 Growing emphasis on enhancing surgical planning, training, and skill developments to fuel segmental growth

- 10.3.4.1.1 Surgery

- 10.3.4.1.2 Patient care management

- 10.3.4.1.3 Fitness management

- 10.3.4.1.4 Pharmacy management

- 10.3.4.1.5 Medical training & education

- 10.3.4.1 Growing emphasis on enhancing surgical planning, training, and skill developments to fuel segmental growth

- 10.3.5 AEROSPACE & DEFENSE

- 10.3.5.1 Surging adoption of advanced technologies to enhance cockpit design and testing to augment segmental growth

- 10.3.6 OTHER VR APPLICATIONS

- 10.3.6.1 Automotive

- 10.3.6.2 Real estate

- 10.3.6.3 Geospatial mining

- 10.3.1 CONSUMER

11 AUGMENTED AND VIRTUAL REALITY MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 11.2.2 US

- 11.2.2.1 Rising deployment of innovative technologies for marketing and promotional campaigns to drive market

- 11.2.3 CANADA

- 11.2.3.1 Burgeoning tourism and hospitality sectors to contribute to market growth

- 11.2.4 MEXICO

- 11.2.4.1 Increasing development of VR-powered training centers to combat crime to fuel market growth

- 11.3 EUROPE

- 11.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 11.3.2 GERMANY

- 11.3.2.1 Increasing development of virtual car dealerships to boost market growth

- 11.3.3 FRANCE

- 11.3.3.1 Escalating adoption of digital displays to accelerate market growth

- 11.3.4 UK

- 11.3.4.1 Rapid digital transformation to contribute to market growth

- 11.3.5 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 11.4.2 CHINA

- 11.4.2.1 Growing population and smartphone adoption to foster market growth

- 11.4.3 INDIA

- 11.4.3.1 Rise in online robotics education to augment market growth

- 11.4.4 JAPAN

- 11.4.4.1 Increasing deployment of advanced technologies in healthcare sector to drive market

- 11.4.5 SOUTH KOREA

- 11.4.5.1 Rising emphasis on streamlining grocery shopping experience to boost market growth

- 11.4.6 REST OF ASIA PACIFIC

- 11.5 ROW

- 11.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 11.5.2 MIDDLE EAST & AFRICA

- 11.5.2.1 Increasing focus on promoting cultural heritage and attracting tourists to accelerate market growth

- 11.5.2.2 GCC countries

- 11.5.2.3 Africa & Rest of Middle East

- 11.5.3 SOUTH AMERICA

- 11.5.3.1 Expansion of consumer sector to expedite market growth

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY STRATEGIES/RIGHT TO WIN, 2019-2024

- 12.3 MARKET SHARE ANALYSIS, 2023

- 12.4 COMPANY VALUATION AND FINANCIAL METRICS

- 12.5 BRAND/PRODUCT COMPARISON

- 12.6 REVENUE ANALYSIS, 2020-2023

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

- 12.7.5.1 Company footprint

- 12.7.5.2 Technology footprint

- 12.7.5.3 Offering footprint

- 12.7.5.4 Device type footprint

- 12.7.5.5 Application footprint

- 12.7.5.6 Region footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

- 12.9.4 OTHERS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 META

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths/Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses/Competitive threats

- 13.1.2 SONY CORPORATION

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths/Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses/Competitive threats

- 13.1.3 APPLE INC.

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths/Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses/Competitive threats

- 13.1.4 BYTEDANCE

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths/Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses/Competitive threats

- 13.1.5 DPVR

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches

- 13.1.5.3.2 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Key strengths/Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses/Competitive threats

- 13.1.6 HTC CORPORATION

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches

- 13.1.6.3.2 Deals

- 13.1.6.4 MnM view

- 13.1.6.4.1 Key strengths/Right to win

- 13.1.6.4.2 Strategic choices

- 13.1.6.4.3 Weaknesses/Competitive threats

- 13.1.7 GOOGLE

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches

- 13.1.7.3.2 Deals

- 13.1.8 MICROSOFT

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches

- 13.1.8.3.2 Deals

- 13.1.8.3.3 Others

- 13.1.9 SAMSUNG

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches

- 13.1.9.3.2 Deals

- 13.1.10 PTC

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Deals

- 13.1.11 SEIKO EPSON CORPORATION

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Solutions/Services offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product launches

- 13.1.12 LENOVO

- 13.1.12.1 Business overview

- 13.1.12.2 Products/Solutions/Services offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Product launches

- 13.1.12.3.2 Deals

- 13.1.1 META

- 13.2 OTHER PLAYERS

- 13.2.1 EON REALITY

- 13.2.2 MAXST CO., LTD.

- 13.2.3 MAGIC LEAP, INC.

- 13.2.4 BLIPPAR GROUP LIMITED

- 13.2.5 ATHEER, INC.

- 13.2.6 VUZIX

- 13.2.7 NINTENDO

- 13.2.8 ULTRALEAP

- 13.2.9 PENUMBRA, INC.

- 13.2.10 PSICO SMART APPS S.L.

- 13.2.11 XIAOMI

- 13.2.12 PANASONIC CORPORATION

- 13.2.13 SCOPE AR

- 13.2.14 CONTINENTAL AG

- 13.2.15 VIRTUALLY LIVE

- 13.2.16 INTEL CORPORATION

- 13.2.17 CRAFTARS

- 13.2.18 BIDON GAMES STUDIO

- 13.2.19 APPENTUS TECHNOLOGIES

- 13.2.20 3D CLOUD

- 13.2.21 WAYRAY AG

14 APPENDIX

- 14.1 INSIGHTS FROM INDUSTRY EXPERTS

- 14.2 DISCUSSION GUIDE

- 14.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.4 CUSTOMIZATION OPTIONS

- 14.5 RELATED REPORTS

- 14.6 AUTHOR DETAILS