|

市場調査レポート

商品コード

1666645

電気温水器市場の機会、成長促進要因、産業動向分析、2025~2034年の予測Electric Water Heater Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 電気温水器市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2024年12月04日

発行: Global Market Insights Inc.

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

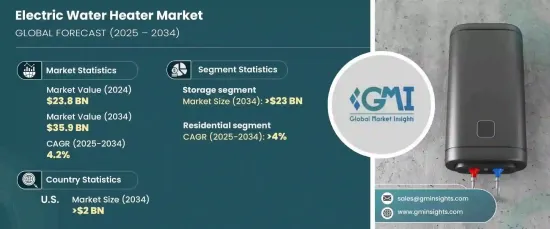

世界の電気温水器市場は2024年に238億米ドルと評価され、2025年から2034年にかけてCAGR 4.2%で成長すると予想されています。

電気温水器は、入浴、掃除、調理など、さまざまな家庭用および業務用の水を加熱するために電気エネルギーを使用します。これらの装置は通常、電気抵抗素子を使用して水を直接加熱するため、現代の家庭や企業にとって一般的な選択肢となっています。

電気温水器市場の成長を後押ししている要因はいくつかあります。競合価格と幅広い容量オプションは消費者にとって魅力的です。さらに、より多くの個人や企業がエネルギー効率の高いシステムにシフトするにつれて、電気温水器の需要が増加しています。暖房システムの電化や住宅・商業インフラへの再生可能エネルギー源の統合の動向の高まりも、電気温水器の採用を後押ししています。さらに、より厳しいエネルギー効率規制や、従来の効率の悪い給湯器からのアップグレードのためのインセンティブは、市場を再構築しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 238億米ドル |

| 予測金額 | 359億米ドル |

| CAGR | 4.2% |

二酸化炭素排出量削減に焦点を当てた開発政策が、インフラ整備への投資増加とともに、電気温水器の利用をさらに促進しています。古い建物の改築や近代化が進んでいるため、大容量給湯器の需要が増加しています。メーカー各社も、様々な商業・産業用途向けにカスタマイズされたソリューションを提供することで市場に対応しており、これが事業の成長を高めています。

同市場は、主に瞬間式給湯器と貯湯式給湯器の2つの製品タイプに分けられます。貯湯式給湯器セグメントは、2034年までに230億米ドルを生み出すと予想されています。エネルギー効率を向上させ、光熱費を削減するスマートな機能は、貯湯式給湯器の大きな推進力となっています。多世帯住宅や一戸建て住宅の増加に加え、ホテル、レストラン、病院などの施設におけるオンデマンド給湯の需要の高まりが、これらのユニットの需要をさらに煽っています。

電気温水器市場は用途別にも区分され、住宅用と商業用が主なカテゴリーです。住宅用セグメントは、住宅所有者がエネルギー代を削減するためにエネルギースター認証モデルを求めるようになっているため、2034年までCAGR 4%で成長すると予測されています。さらに、Wi-Fi接続やモバイルアプリ制御などのスマート給湯器技術の台頭が製品需要を押し上げ、住宅所有者が給湯器を遠隔管理できるようになっています。

米国の電気温水器市場は、2034年までに20億米ドルに達すると予測されています。エネルギー効率、環境持続可能性、給湯器の技術的進歩を重視する傾向が強まっていることが、この成長に寄与しています。より厳しいエネルギー効率基準が施行されるにつれて、より多くの消費者が高度な電気モデルを選択し、そのうちのいくつかは、さらにエネルギーコストを削減し、ソーラーパネルのような再生可能エネルギーシステムと統合されています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競争情勢

- イントロダクション

- 戦略ダッシュボード

- イノベーションと技術の展望

- 各社の市場シェア

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 瞬間式

- 貯湯式

第6章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 30リットル以下

- 30~100リットル

- 100~250リットル

- 250~400リットル

- 400リットル以上

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 住宅用

- 商業用

- 大学

- オフィス

- 官公庁/ビル

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- オーストリア

- スペイン

- オランダ

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- オマーン

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- メキシコ

第9章 企業プロファイル

- A. O. Smith

- Ariston Holding N.V.

- American Standard Water Heaters

- Bosch Thermotechnology Corp.

- Bradford White Corporation

- FERROLI

- GE Appliances

- Groupe Atlantic

- Haier

- Havells India

- Hubbell Heaters

- LINUO RITTER INTERNATIONAL

- Nihon Itomic Co., Ltd.

- Noritz Corporation

- Parker Boiler Company

- Racold

- Rheem Manufacturing Company

- Rinnai Corporation

- State Industries

- STIEBEL ELTRON

- Vaillant

- Viessmann

- Westinghouse Electric Corporation

- Whirlpool Corporation

- Watts

- Zenith Water Heaters

The Global Electric Water Heater Market was valued at USD 23.8 billion in 2024 and is expected to grow at 4.2% CAGR from 2025 to 2034. Electric water heaters use electrical energy to heat water for a variety of domestic and commercial purposes, such as bathing, cleaning, and cooking. These devices typically use electrical resistance elements to directly heat water, making them a common choice for modern households and businesses.

Several factors are driving the growth of the electric water heater market. Competitive pricing, along with a wide range of capacity options, is appealing to consumers. Additionally, as more individuals and businesses shift toward energy-efficient systems, the demand for electric water heaters is increasing. The growing trend to electrify heating systems and the integration of renewable energy sources into residential and commercial infrastructure is also boosting the adoption of electric water heaters. Furthermore, stricter energy efficiency regulations and incentives for upgrading from traditional, less efficient water heaters are reshaping the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.8 Billion |

| Forecast Value | $35.9 Billion |

| CAGR | 4.2% |

Government policies focused on reducing carbon emissions, along with increased investments in infrastructure development, are further promoting the use of electric water heaters. The demand for high-capacity water heaters is on the rise due to the ongoing renovation and modernization of older buildings. Manufacturers are also responding to the market by offering customized solutions for various commercial and industrial applications, which is enhancing business growth.

The market is divided into two main product types: instant and storage water heaters. The storage water heater segment is expected to generate USD 23 billion by 2034. Smart features that improve energy efficiency and reduce utility costs are a significant driver for storage water heaters. The increasing number of multi-family and single-family homes, along with the growing demand for on-demand hot water in institutions like hotels, restaurants, and hospitals, is further fueling the demand for these units.

The electric water heater market is also segmented by application, with residential and commercial being the primary categories. The residential segment is forecasted to grow at a CAGR of 4% through 2034 as homeowners increasingly seek Energy Star-certified models to reduce energy bills. Additionally, the rise in smart water heater technologies, such as Wi-Fi connectivity and mobile app controls, is boosting product demand, allowing homeowners to manage their water heaters remotely.

U.S. electric water heater market is projected to reach USD 2 billion by 2034. The growing emphasis on energy efficiency, environmental sustainability, and technological advancements in water heaters are contributing to this growth. As stricter energy efficiency standards are enforced, more consumers are opting for advanced electric models, some of which integrate with renewable energy systems like solar panels, further reducing energy costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

- 4.4 Company market share

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 Instant

- 5.3 Storage

Chapter 6 Market Size and Forecast, By Capacity, 2021 – 2034 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Below 30 liters

- 6.3 30 – 100 liters

- 6.4 100 – 250 liters

- 6.5 250 – 400 liters

- 6.6 >400 liters

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.3.1 College/University

- 7.3.2 Offices

- 7.3.3 Government/Building

- 7.3.4 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Italy

- 8.3.5 Austria

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Kuwait

- 8.5.5 Oman

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Mexico

Chapter 9 Company Profiles

- 9.1 A. O. Smith

- 9.2 Ariston Holding N.V.

- 9.3 American Standard Water Heaters

- 9.4 Bosch Thermotechnology Corp.

- 9.5 Bradford White Corporation

- 9.6 FERROLI

- 9.7 GE Appliances

- 9.8 Groupe Atlantic

- 9.9 Haier

- 9.10 Havells India

- 9.11 Hubbell Heaters

- 9.12 LINUO RITTER INTERNATIONAL

- 9.13 Nihon Itomic Co., Ltd.

- 9.14 Noritz Corporation

- 9.15 Parker Boiler Company

- 9.16 Racold

- 9.17 Rheem Manufacturing Company

- 9.18 Rinnai Corporation

- 9.19 State Industries

- 9.20 STIEBEL ELTRON

- 9.21 Vaillant

- 9.22 Viessmann

- 9.23 Westinghouse Electric Corporation

- 9.24 Whirlpool Corporation

- 9.25 Watts

- 9.26 Zenith Water Heaters