冷凍調理済みレディミール市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Frozen Cooked Ready Meals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801930

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

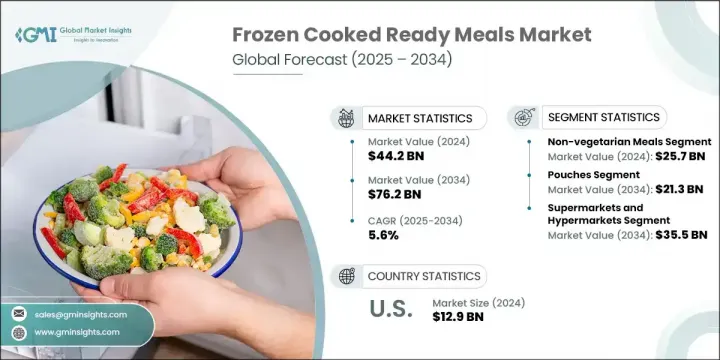

世界の冷凍調理済みレディミール市場は、2024年に442億米ドルと評価され、CAGR 5.6%で成長し、2034年には762億米ドルに達すると推定されています。

便利で迅速な食事ソリューションに対する消費者の嗜好の高まりが、市場の勢いを牽引し続けています。都市化、共働き世帯の増加、日常生活のペースの増大が、進化する健康基準にも適合するクイック調理食への需要を煽っています。先進パッケージング・フォーマットと高度な保存方法により、ブランドはより新鮮な味と栄養を保持した冷凍食品を提供できるようになっています。同時に、eコマースは消費者の買い物の仕方を変え、こうした食事をより身近なものにしています。

食生活の嗜好の変化、製品ラインナップの拡充、より健康的で時間節約につながる食品オプションへの消費者の支出意欲の高まりに支えられ、世界各地域で市場規模は2034年までにほぼ倍増すると予想されます。植物ベースの食習慣が成長をさらに後押ししており、持続可能で肉を使わない選択肢を求める消費者が増えています。各ブランドは、肉ベースの食事を植物性タンパク質の代替品へと進化させ、レンズ豆、大豆、エンドウ豆などの食材を取り入れて、倫理的で健康志向の買い物客にアピールしています。クリーンラベル、すぐに食べられるもの、バラエティに富んだ世界の料理への需要が高まる中、冷凍調理済みレディミールカテゴリーは現代の食事計画や食品消費パターンの中心的存在になりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 442億米ドル |

| 予測金額 | 762億米ドル |

| CAGR | 5.6% |

非ベジタリアンの冷凍食品セグメントは2024年に257億米ドルを占め、58.1%のシェアを獲得しました。このセグメントは、タンパク質が豊富で風味豊かな食事オプションへの需要が広がっているため、依然として支配的です。ベジタリアン・メニューが人気を集めているのは、植物由来の食事と健康に対する意識の高まりが主な理由であるが、非ベジタリアン食は、確立された消費者ベースと、多様性を損なうことなく利便性を追求する食欲の高まりから引き続き利益を得ています。消費者は、時間を節約しながら食事のニーズを満たせる食事に惹かれており、これは利便性が優先される都市環境では特に当てはまる。健康志向の高まりは、各ブランドがよりクリーンでバランスの取れた非ベジ食を提供するよう促し、成長をさらに後押ししています。

包装革新セグメントは2034年までに213億米ドルに達し、パウチは使いやすさ、持ち運びやすさ、保存効率の良さを提供します。これらの軽量オプションはペースの速いライフスタイルに対応し、市場の持続可能性へのシフトに合致しています。断熱性、リサイクル性、スマート包装機能を向上させた新しいパウチ・フォーマットは、製品の見せ方や保存方法に影響を与えています。

米国冷凍調理済みレディミール市場は80.1%のシェアを占め、2024年には129億米ドルを創出します。同地域は、成熟した小売インフラと、製品の多様性におけるイノベーションを求める消費者の一貫した需要により、力強い成長を示しています。共働き世帯の増加や時間に制約のある消費者といったライフスタイルの変化が、市場を拡大し続ける利便性の文化を生み出しました。伝統的な食料品店と大型小売店は依然として不可欠なチャネルであるが、オンライン食料品宅配プラットフォームは冷凍食品の認知度とアクセシビリティを大幅に高めています。消費者の食生活が健康とウェルネスにシフトする中、米国の各ブランドは、主力商品である肉類を補完する植物性食品の選択肢を着実に増やしています。

世界の冷凍調理済みレディミール市場を形成している主要企業には、Dr. Oetker、General Mills、Frosta、Kerry Group、Conagra Brandsなどがあります。冷凍調理済みレディミール市場で競争力を確保するため、大手ブランドは多様な消費者ニーズをターゲットとした継続的な製品イノベーションに注力しています。各社は、健康志向やフレキシタリアン志向の消費者にアピールするため、植物由来やクリーンラベルのポートフォリオを拡大しています。研究開発に投資することで、人工的な保存料を使用せずに味覚プロファイルを改善し、賞味期限を延ばすことができます。現地のサプライヤーとの戦略的パートナーシップは、より迅速な製品発売と原材料の管理を可能にしています。リサイクル可能なパウチや電子レンジ対応容器など、パッケージング・ソリューションの強化も優先課題となっています。各ブランドは、オンライン食料品プラットフォームや消費者直販チャネルを重視するオムニチャネル小売戦略を通じて、市場での足跡をさらに強化しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 迅速、便利、そして時間を節約できる食事ソリューションに対する消費者の需要の高まり

- 都市化の進展と共働き世帯の調理時間の減少

- 味、食感、栄養を保存する冷凍技術の進歩

- 組織化された小売およびeコマースの食料品プラットフォームの浸透の増加

- 業界の潜在的リスク&課題

- 冷凍食品は新鮮な食品よりも健康的ではないという消費者の認識

- 生鮮食事キットやレストランの配達サービスとの激しい競合

- 市場機会

- 植物由来およびクリーンラベルの冷凍食品の需要増加

- 中流階級人口の増加に伴う新興市場への進出

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ベジタリアン料理

- 非ベジタリアン料理

第6章 市場推計・予測:包装形態別、2021年~2034年

- 主要動向

- パウチ

- トレイ

- バッグ

- ボックス

第7章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア

- オンライン小売

- 専門店

- 食品サービス/レストラン

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

8.3.1ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- その他中東・アフリカ地域

第9章 企業プロファイル

- Ajinomoto Co., Inc.

- Bellisio Foods

- Conagra Brands

- Dr. Oetker

- Frosta AG

- General Mills

- Iceland Foods

- Kerry Group

- Kraft Heinz

- McCain Foods

- MTR Foods

- Nestle

- Nomad Foods

- Seara Foods(JBS)

- Tyson Foods

目次

The Global Frozen Cooked Ready Meals Market was valued at USD 44.2 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 76.2 billion by 2034. Rising consumer preference for convenient and fast meal solutions continues to drive market momentum. Urbanization, increasing dual-income households, and the growing pace of everyday life are fueling the demand for quick-prep meals that also meet evolving health standards. Enhanced packaging formats and advanced preservation methods are enabling brands to deliver fresher-tasting, nutrient-retaining frozen meals. Simultaneously, e-commerce is reshaping how consumers shop, making these meals more accessible.

Across global regions, market volumes are expected to nearly double by 2034, supported by changing dietary preferences, expanded product offerings, and growing consumer willingness to spend more on healthier, time-saving food options. Plant-based eating habits are further propelling growth, with more consumers seeking sustainable, meat-free choices. Brands are evolving meat-based meals into plant protein alternatives, incorporating ingredients like lentils, soy, and peas to appeal to ethical and health-conscious shoppers. With demand rising for clean-label, ready-to-serve, and varied global cuisines, the frozen cooked ready meals category is becoming a central part of modern meal planning and food consumption patterns.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $44.2 Billion |

| Forecast Value | $76.2 Billion |

| CAGR | 5.6% |

The non-vegetarian frozen meals segment accounted for USD 25.7 billion in 2024, capturing 58.1% share. This segment remains dominant due to the widespread demand for protein-rich and flavorful meal options. While vegetarian options are gaining traction, largely because of increased awareness around plant-based diets and health, non-vegetarian meals continue to benefit from an established consumer base and growing appetite for convenience without compromising variety. Consumers are drawn to meals that meet dietary needs while saving time, and this is especially true in urban environments where convenience is a priority. The rise in health consciousness is pushing brands to offer cleaner, better-balanced non-veg meals, further boosting growth.

Packaging innovation segment will reach USD 21.3 billion by 2034, pouches offer ease of use, portability, and better storage efficiency. These lightweight options cater to fast-paced lifestyles and align with the market's shift toward sustainability. New pouch formats with improved insulation, recyclability, and smart-packaging features are influencing how products are presented and preserved.

U.S. Frozen Cooked Ready Meals Market held 80.1% share and generated USD 12.9 billion in 2024. The region shows strong growth thanks to mature retail infrastructure and consistent consumer demand for innovation in product variety. Lifestyle changes such as the growth of dual-income homes and time-constrained consumers have created a culture of convenience that continues to expand the market. Traditional grocery stores and large-format retailers remain essential channels, though online grocery delivery platforms have significantly boosted visibility and accessibility of frozen meals. As consumer diets shift toward health and wellness, brands in the U.S. are steadily adding plant-based options to complement their core meat-based lines.

The key players shaping the Global Frozen Cooked Ready Meals Market include Dr. Oetker, General Mills, Frosta, Kerry Group, and Conagra Brands. To secure a competitive position in the frozen cooked ready meals market, leading brands are focusing on continuous product innovation, targeting diverse consumer needs. Companies are expanding their plant-based and clean-label portfolios to appeal to health-conscious and flexitarian consumers. Investing in R&D helps improve taste profiles and extend shelf life without artificial preservatives. Strategic partnerships with local suppliers allow faster product launches and better control over ingredients. Enhanced packaging solutions, including recyclable pouches and microwave-safe containers, are also a priority. Brands are further strengthening their market footprint through omnichannel retail strategies, emphasizing online grocery platforms and direct-to-consumer channels.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Packaging type

- 2.2.3 Distribution channel

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing consumer demand for quick, convenient, and time-saving meal solutions

- 3.2.1.2 Rising urbanization and dual-income households with less cooking time

- 3.2.1.3 Advancements in freezing technology preserving taste, texture, and nutrition

- 3.2.1.4 Increasing penetration of organized retail and e-commerce grocery platforms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Consumer perception of frozen meals as less healthy than fresh alternatives

- 3.2.2.2 Intense competition from fresh meal kits and restaurant delivery services

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for plant-based and clean-label frozen meal options

- 3.2.3.2 Expansion into emerging markets with growing middle-class population

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Bn, Tons)

- 5.1 Key trends

- 5.2 Vegetarian meals

- 5.3 Non-vegetarian meals

Chapter 6 Market Estimates & Forecast, By Packaging Type, 2021 - 2034 (USD Bn, Tons)

- 6.1 Key trends

- 6.2 Pouches

- 6.3 Trays

- 6.4 Bags

- 6.5 Boxes

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Bn, Tons)

- 7.1 Key trends

- 7.2 Supermarkets/hypermarkets

- 7.3 Convenience stores

- 7.4 Online retail

- 7.5 Specialty stores

- 7.6 Foodservice/restaurants

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest Of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Egypt

- 8.6.5 Rest of MEA

Chapter 9 Company Profiles

- 9.1 Ajinomoto Co., Inc.

- 9.2 Bellisio Foods

- 9.3 Conagra Brands

- 9.4 Dr. Oetker

- 9.5 Frosta AG

- 9.6 General Mills

- 9.7 Iceland Foods

- 9.8 Kerry Group

- 9.9 Kraft Heinz

- 9.10 McCain Foods

- 9.11 MTR Foods

- 9.12 Nestle

- 9.13 Nomad Foods

- 9.14 Seara Foods (JBS)

- 9.15 Tyson Foods

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日