グラウトとアンカーの市場機会と促進要因、業界動向分析、2025~2034年予測

Grouts and Anchors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801864

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

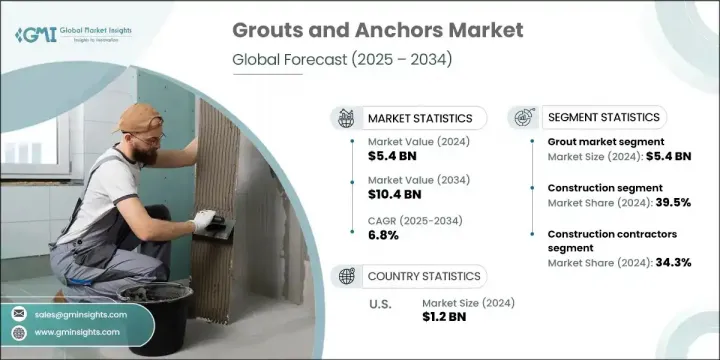

グラウトとアンカーの世界市場規模は、2024年に54億米ドルとなり、CAGR 6.8%で成長し、2034年には104億米ドルに達すると推定されます。

市場の拡大は、都市化の進展、建設活動の急増、インフラの強靭性重視の高まりと強く結びついています。グラウトとアンカーは、基礎を安定させ、建具を固定し、最新の建設プロジェクトと改修プロジェクトの両方で隙間を埋めることによって、構造の完全性を確保するために不可欠な材料です。これらの部材は、商業ビル、橋梁、トンネルなどの土木インフラの安全性と長寿命化の基礎となっています。

住宅、商業施設、公共インフラへの世界の投資が加速するにつれ、高性能で耐久性のある建設資材への需要も高まっています。また、技術的に先進的で施工が容易なアンカーやグラウティングのソリューションに対する嗜好の高まりも、産業を形成しています。さらに、進化する建築基準法や安全規制への準拠を求める動きも、先進経済諸国と新興経済諸国の両方で市場の勢いを増し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 54億米ドル |

| 予測金額 | 104億米ドル |

| CAGR | 6.8% |

グラウトは、構造物の安定化、空洞の充填、荷重分布の改善に広く使用されています。グラウトはその強度と適応性で知られ、構造修復、基礎補強、耐久性と精度を必要とする厳しい建設作業に不可欠です。その長期的な信頼性により、小規模な補修から大規模なインフラプロジェクトまで、グラウトは最適なソリューションとなっています。

住宅、工業、商業開発の世界の需要が絶えないことから、2024年の建設セグメントのシェアは39.5%でした。建設業者は、より長持ちし、法令に準拠した建物を目指しているため、性能と安全性の期待に応える高品質のグラウト・アンカーリング製品に注目しています。また、サステイナブル建設資材へのシフトも、近代的な建築プラクティスにおける先進的グラウトとアンカーの使用を強化する役割を果たしています。

米国のグラウトとアンカー市場は88.7%のシェアを占め、2024年には12億米ドルを創出しました。この主導的地位は、全米におけるインフラのアップグレードと新築への大規模投資によるものです。現在進行中の連邦政府のインフラ構想は、強度、耐用年数、回復力の向上を提供する信頼性の高いグラウト・アンカー材への需要を支えています。インフラが老朽化し、気候変動への耐性が重要になるにつれ、建設業者は進化する構造上の要求に沿った高性能製品を求め続けています。

世界のグラウトとアンカー市場を形成している主要企業は、Hilti AG、MAPEI S.p.A.、Sika AG、BASF SE、Fosroc Internationaなどです。市場ポジションを強化するため、グラウトとアンカーセグメントの主要企業はいくつかの戦略的イニシアティブに注力しています。これには、より速い硬化時間、より高い耐久性、持続可能性を備えた革新的な材料を開発するための研究開発の拡大が含まれます。多くの企業は、特定の建設用途のニーズを満たすため、製品のカスタマイズや先進的化学配合に投資しています。戦略的合併、地域的提携、買収も、地理的足跡を広げるための一般的なアプローチです。さらに各社は、製品の採用を促進し、適切な適用を確実にするために、建設業者向けの研修プログラムを重視する一方、正確な配合提案とプロジェクト計画のためにデジタルツールを統合しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主要動向

- 一次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- サステイナブル建設への移行

- ハイブリッド技術とスマート技術の採用

- 注入型接着アンカーが成長を牽引

- 産業の潜在的リスク・課題

- 原料供給の不安定さ

- 規制遵守の圧力

- 市場機会

- モジュール型とプレハブ式建設の増加

- カスタマイズと特注品

- 建設技術企業との連携

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画と資金調達

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- グラウト市場

- セメント系グラウト

- エポキシグラウト

- 化学グラウト

- その他のグラウトタイプ

- ポリウレタングラウト

- アクリルグラウト

- アンカー市場

- 機械式アンカー

- 化学式アンカー

- 接着アンカー

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 建設

- 家庭用

- 商用

- 産業用

- インフラ

- 輸送

- 橋と高速道路

- トンネルと地下

- 鉄道インフラ

- 空港建設

- 公益事業

- 水と廃水

- 発電

- 通信

- エネルギーインフラ

- 輸送

- 海洋とオフショア

- 港湾建設

- オフショアプラットフォーム

- 沿岸保護

- 船舶修理とメンテナンス

- 鉱業と地下用途

- 鉱山支援システム

- 地下掘削

- トンネルの安定化

- 地盤改良

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 建設請負業者

- ゼネコン

- 専門業者

- インフラ開発者

- 産業最終用途

- 販売業者と小売業者

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他の中東・アフリカ

第9章 企業プロファイル

- Arkema Group(via Bostik)

- BASF SE(Master Builders Solutions)

- Fosroc International Limited

- H.B. Fuller Company

- Henkel AG & Co. KGaA(Loctite brand)

- Hilti AG

- Laticrete International

- MAPEI S.p.A.

- Saint-Gobain Weber

- Sika AG

- Stanley Black & Decker

- Wurth Group

目次

The Global Grouts and Anchors Market was valued at USD 5.4 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 10.4 billion by 2034. Market expansion is strongly tied to increased urbanization, a surge in construction activity, and the growing emphasis on infrastructure resilience. Grouts and anchors are essential materials that ensure structural integrity by stabilizing foundations, securing fixtures, and filling gaps across both modern construction and retrofitting projects. These components are foundational to the safety and longevity of civil infrastructure, including commercial buildings, bridges, tunnels, and more.

As global investments in residential, commercial, and public infrastructure accelerate, so does the demand for high-performance and durable construction materials. The growing preference for technologically advanced and easy-to-apply anchoring and grouting solutions is also shaping the industry. Additionally, the push for compliance with evolving building codes and safety regulations continues to drive market momentum across both developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.4 Billion |

| Forecast Value | $10.4 Billion |

| CAGR | 6.8% |

The grouts segment dominated with a 54.3% market share in 2024, as these materials are widely used to stabilize structures, fill cavities, and improve load distribution. Known for their strength and adaptability, grouts are essential for structural rehabilitation, foundation reinforcements, and demanding construction tasks requiring durability and precision. Their long-term reliability makes them the go-to solution in both small-scale repairs and large-scale infrastructure projects.

The construction segment held a 39.5% share in 2024, owing to constant global demand for residential, industrial, and commercial developments. As builders aim for longer-lasting, code-compliant buildings, they are turning to high-quality grouting and anchoring products to meet performance and safety expectations. The shift toward sustainable construction materials is also playing a role in reinforcing the use of advanced grouts and anchors in modern building practices.

U.S. Grouts and Anchors Market held an 88.7% share and generated USD 1.2 billion in 2024. This leadership position stems from large-scale investments in infrastructure upgrades and new construction across the country. Ongoing federal infrastructure initiatives are sustaining the demand for reliable grouting and anchoring materials that offer strength, longevity, and improved resilience. As infrastructure ages and climate resilience becomes critical, builders continue to seek high-performance products that align with evolving structural demands.

Key players shaping the Global Grouts and Anchors Market include Hilti AG, MAPEI S.p.A., Sika AG, BASF SE, and Fosroc International. To strengthen their market position, leading companies in the grouts and anchors space are focusing on several strategic initiatives. These include expanding R&D to develop innovative materials with faster curing times, higher durability, and sustainability features. Many are investing in product customization and advanced chemical formulations to meet the needs of specific construction applications. Strategic mergers, regional partnerships, and acquisitions are also common approaches to widen their geographical footprint. Furthermore, companies are emphasizing on training programs for contractors to boost product adoption and ensure proper application, while integrating digital tools for precise formulation recommendations and project planning.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward sustainable construction

- 3.2.1.2 Adoption of hybrid and smart technologies

- 3.2.1.3 Injectable adhesive anchors leading growth

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material supply instability

- 3.2.2.2 Regulatory compliance pressure

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in modular and prefabricated construction

- 3.2.3.2 Customization and specialty products

- 3.2.3.3 Collaboration with construction technology firms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Grouts market

- 5.2.1 Cementitious grouts

- 5.2.2 Epoxy grouts

- 5.2.3 Chemical grouts

- 5.2.4 Other grout types

- 5.2.4.1 Polyurethane grouts

- 5.2.4.2 Acrylic grouts

- 5.3 Anchors market

- 5.3.1 Mechanical anchors

- 5.3.2 Chemical anchors

- 5.3.3 Adhesive anchors

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Construction

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.3 Infrastructure

- 6.3.1 Transportation

- 6.3.1.1 Bridges and highways

- 6.3.1.2 Tunnels and underground

- 6.3.1.3 Railway infrastructure

- 6.3.1.4 Airport construction

- 6.3.2 Utilities

- 6.3.2.1 Water and wastewater

- 6.3.2.2 Power generation

- 6.3.2.3 Telecommunications

- 6.3.2.4 Energy infrastructure

- 6.3.1 Transportation

- 6.4 Marine and offshore

- 6.4.1 Port and harbor construction

- 6.4.2 Offshore platforms

- 6.4.3 Coastal protection

- 6.4.4 Marine repair and maintenance

- 6.5 Mining and underground applications

- 6.5.1 Mine support systems

- 6.5.2 Underground excavation

- 6.5.3 Tunnel stabilization

- 6.5.4 Ground improvement

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Construction Contractors

- 7.2.1 General Contractors

- 7.2.2 Specialty Contractors

- 7.3 Infrastructure Developers

- 7.4 Industrial End Use

- 7.5 Distributors and Retailers

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of MEA

Chapter 9 Company Profiles

- 9.1 Arkema Group (via Bostik)

- 9.2 BASF SE (Master Builders Solutions)

- 9.3 Fosroc International Limited

- 9.4 H.B. Fuller Company

- 9.5 Henkel AG & Co. KGaA (Loctite brand)

- 9.6 Hilti AG

- 9.7 Laticrete International

- 9.8 MAPEI S.p.A.

- 9.9 Saint-Gobain Weber

- 9.10 Sika AG

- 9.11 Stanley Black & Decker

- 9.12 Wurth Group

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日