|

市場調査レポート

商品コード

1801818

オートバイ・スクーターの市場機会、成長促進要因、産業動向分析、予測、2025年~2034年Motorcycle and Scooter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| オートバイ・スクーターの市場機会、成長促進要因、産業動向分析、予測、2025年~2034年 |

|

出版日: 2025年08月13日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

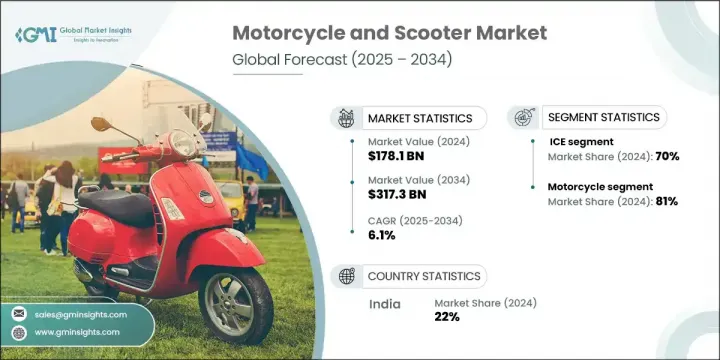

オートバイ・スクーターの世界市場規模は、2024年に1,781億米ドルとなり、CAGR 6.1%で成長し、2034年には3,173億米ドルに達すると予測されています。

この市場は、都市交通ニーズの進化、持続可能性に関する意識の高まり、若年層の嗜好の変化などにより、大きな変化を遂げつつあります。消費者が環境への配慮を優先し、グリーン交通を支援する政府の優遇措置の恩恵を受けているため、電気自動車は着実に普及しつつあります。都市の混雑と、コスト効率の高いコンパクトなモビリティオプションへのニーズが、二輪車需要に拍車をかけています。

メーカー各社は、GPS、モバイル接続、診断機能などの最新機能を組み込むことで、二輪車やスクーターの魅力を高めています。さらに、軽量構造、洗練された美観、人間工学に基づいたデザインの動向は、若い顧客層を引き寄せています。車両サブスクリプションサービスやライドシェアオプションのような新しいビジネスモデルは、大都市圏で人々がパーソナルモビリティを利用する方法を徐々に再構築しています。アフターマーケットも進化しており、ライダー固有のカスタマイズ、性能アップグレード、安全性強化部品への需要が高まり、二輪車セグメントへの消費者の関与をさらに促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,781億米ドル |

| 予測金額 | 3,173億米ドル |

| CAGR | 6.1% |

2024年の市場シェアは内燃機関(ICE)モデルが約70%を占め、2025年から2034年にかけてCAGR 5%以上で拡大すると予測されます。電動二輪車の人気は着実に高まっていますが、多くのライダーの間では従来型ガソリン車が依然として好まれています。給油インフラが広く利用可能であること、機械的信頼性が確立されていること、航続距離が長く乗り心地が優れていることなどが、内燃機関車が世界の販売台数の大半を占め続けている主な理由です。従来型エンジンの勢いは、今のところ、それが世界中の多くの消費者の期待に応え続けていることを示しています。

オートバイは2024年も引き続き主要製品カテゴリーであり、シェアは81%を占めます。この分野は2034年までCAGR 6%で成長すると予想されます。世界の多くの地域、特に新興経済国では、二輪車は最も実用的で経済的な日常の移動手段となっています。標準的なエンジン容量は100ccから250ccで、これらのバイクは何百万人もの通勤者にとって不可欠な移動手段となっています。世界生産の大部分はアジア太平洋地域で生産されており、手頃な価格と機能的な実用性が主な購買要因となっています。

インドのオートバイ・スクーター市場は22%のシェアを占め、2024年には296億米ドルを生み出しました。世界トップの二輪車メーカーであるインドは、世界の二輪車生産台数の約15~20%を占め、2024年度には約2,800万台が生産されます。二輪車がレクリエーションや贅沢品としての役割を果たすことが多い成熟市場とは異なり、インドの消費者は二輪車を日常使いにしています。インドでは、費用対効果、走行距離、メンテナンスのしやすさ、日々の信頼性などを考慮した上で、重要な購買決定が下されます。

世界のオートバイ・スクーター市場を形成する主要企業には、Classic Legends、Hero、TVS、Piaggio、Yamaha、Suzuki、Honda、Bajaj Motorcycles、OLA、ATHERなどがあります。オートバイ・スクーター業界のトップメーカーは、技術革新、ローカライゼーション、製品の多様化に注力することで、市場での地位を強化しています。これらのメーカーは、持続可能性の目標や、よりクリーンなモビリティに対する消費者の関心の高まりに合わせて、電気自動車のポートフォリオを拡大しています。スマートコネクティビティ機能や安全技術への投資は、各ブランドがユーザー体験やブランド差別化を強化するのに役立っています。多くの企業は、物流コストを削減し、現地の需要に効率的に対応するため、地域製造ハブを設立して、国内および輸出の足跡を強化しています。ハイテク企業やモビリティプラットフォームとの提携は、サブスクリプションモデルやシェアードモビリティソリューションを通じて新たな収益源を生み出しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 都市化と交通渋滞の進行

- eコマースとラストマイル配送の拡大

- 燃料価格の上昇

- 電動二輪車の急速な普及

- アジアにおける中流階級人口の増加

- 業界の潜在的リスク&課題

- 安全上の懸念と事故率の上昇

- 不十分な充電インフラ

- サプライチェーンの混乱

- 原材料費の上昇

- 市場機会

- 電動化とEVの普及

- コネクテッドでスマートなモビリティソリューション

- サブスクリプションとリースモデル

- アフリカと東南アジアでの市場拡大

- 配送プラットフォームとの戦略的パートナーシップ

- オートバイ・スクーター市場進化

- 市場開拓と成熟度分析

- 従来のモビリティソリューションから最新のモビリティソリューションへの移行

- 二輪車セグメントにおける技術導入ライフサイクル

- 市場統合と業界再編の動向

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーターの分析

- PESTEL分析

- 技術革新と高度な機能

- オートバイのADASと安全技術の統合

- コネクテッドバイクソリューションとIoT統合

- 高度なパワートレイン技術

- 自律および半自律機能の開発

- オートバイ・スクーター市場変換

- 電動二輪車技術の進化

- バッテリー技術と航続距離の最適化

- 充電インフラの開発とアクセシビリティ

- 政府のインセンティブと政策支援の分析

- 消費者行動と市場の嗜好

- 人口統計プロファイルとターゲット顧客分析

- 購入決定要因と購入プロセス

- 使用パターンと移動行動

- ブランドロイヤルティと乗り換えパターン

- 価格感度と価値認識分析

- 特許情勢

- 価格動向

- 国別

- 製品別

- コスト内訳分析

- 生産統計

- 輸入と輸出

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推定・予測:製品別、2021年~2034年

- 主要動向

- オートバイ

- クルーザーバイク

- スポーツバイク

- ツーリングバイク

- 標準/ネイキッドバイク

- アドベンチャー/デュアルスポーツバイク

- オフロード/ダートバイク

- スクーター

- 従来型ガソリンスクーター

- 電動スクーター

- マキシスクーター

- モペット型スクーター

第6章 市場推定・予測:推進別、2021年~2034年

- 主要動向

- 内燃機関(ICE)

- 電気自動車(EV)

第7章 市場推定・予測:排気量別、2021年~2034年

- 主要動向

- 250cc以下

- 250cc~500cc

- 500cc~1000cc

- 1000cc超

第8章 市場推定・予測:流通チャネル別、2021年~2034年

- 主要動向

- オフライン

- オンライン

第9章 市場推定・予測:最終用途別、2021年~2034年

- 主要動向

- 個人

- 商業

第10章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Global Two-Wheeler OEMs

- Bajaj

- Hero

- Honda

- Piaggio

- Suzuki

- TVS

- Yamaha

- Premium Motorcycle Brands

- BMW Motorrad

- Ducati

- Harley-Davidson

- KTM

- Royal Enfield

- Kawasaki

- Electric Two-Wheeler Manufacturers

- Ather

- Ola Electric

- Revolt

- Ultraviolette

- Yadea

- Zero Motorcycles

- Niu Technologies

- Component and System Suppliers

- Bosch

- Brembo

- Continental

- Nissin

- ZF

- Connected Mobility and Software Providers

- MapmyIndia

- Ride Vision

- Sibros

- TomTom

- Vahan

The Global Motorcycle and Scooter Market was valued at USD 178.1 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 317.3 billion by 2034. This market is undergoing major changes due to evolving urban transportation needs, rising awareness around sustainability, and shifting preferences among younger demographics. Electric variants are gaining steady traction as consumers prioritize environmental consciousness and benefit from government incentives supporting green transportation. Urban congestion and the need for cost-efficient, compact mobility options are fueling demand for two-wheelers.

Manufacturers are enhancing the appeal of motorcycles and scooters by incorporating modern features such as GPS, mobile connectivity, and diagnostic capabilities. Additionally, trends in lightweight construction, sleek aesthetics, and ergonomic design are drawing in a younger customer base. New business models like vehicle subscription services and ridesharing options are slowly reshaping how people access personal mobility in metropolitan areas. The aftermarket is also evolving, with increasing demand for rider-specific customization, performance upgrades, and enhanced safety components, and further driving consumer engagement with the two-wheeler segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $178.1 Billion |

| Forecast Value | $317.3 Billion |

| CAGR | 6.1% |

In 2024, internal combustion engine (ICE) models held approximately 70% market share and are forecast to expand at a CAGR of over 5% from 2025 to 2034. While electric two-wheelers are steadily rising in popularity, traditional petrol-powered vehicles remain the preferred choice among many riders. The widespread availability of fueling infrastructure, well-established mechanical reliability, and superior range for longer rides are key reasons ICE vehicles continue to dominate global sales volumes. The momentum behind conventional engines demonstrates that, for now, they continue to meet the expectations of many consumers worldwide.

Motorcycles remained the leading product category in 2024, accounting for 81% share. This segment is expected to grow at a CAGR of 6% through 2034. In numerous global regions, particularly in emerging economies, motorcycles represent the most practical and economical means of daily transportation. With standard engine capacities ranging between 100cc and 250cc, these bikes serve as essential mobility tools for millions of commuters. A large share of global production originates from the Asia Pacific, where affordability and functional utility are major purchasing factors.

India Motorcycle and Scooter Market held 22% share and generated USD 29.6 billion in 2024. As the top global manufacturer of motorcycles, India contributes roughly 15-20% of worldwide two-wheeler production, with approximately 28 million units built in FY 2024. Unlike in mature markets, where motorcycles often serve recreational or luxury roles, Indian consumers rely on them for everyday use. Here, critical buying decisions are shaped by considerations like cost-efficiency, mileage, ease of maintenance, and day-to-day reliability.

Leading players shaping the Global Motorcycle and Scooter Market include Classic Legends, Hero, TVS, Piaggio, Yamaha, Suzuki, Honda, Bajaj Motorcycles, OLA, and ATHER. Top manufacturers in the motorcycle and scooter industry are reinforcing their market position by focusing on innovation, localization, and product diversification. They are expanding their electric vehicle portfolios to align with sustainability goals and growing consumer interest in cleaner mobility. Investment in smart connectivity features and safety technology is helping brands enhance user experience and brand differentiation. Many are strengthening their domestic and export footprints by establishing regional manufacturing hubs to reduce logistics costs and meet local demand efficiently. Partnerships with tech firms and mobility platforms are creating new revenue streams through subscription models and shared mobility solutions.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Propulsion

- 2.2.4 Engine Displacement

- 2.2.5 Distribution Channel

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising urbanization and traffic congestion

- 3.2.1.2 Expansion of e-commerce and last-mile delivery

- 3.2.1.3 Increasing fuel prices

- 3.2.1.4 Rapid adoption of electric two-wheelers

- 3.2.1.5 Growing middle-class population in Asia

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Safety concerns and rising accident rates

- 3.2.2.2 Inadequate charging infrastructure

- 3.2.2.3 Supply chain disruptions

- 3.2.2.4 Rising raw material costs

- 3.2.3 Market opportunities

- 3.2.3.1 Electrification and EV penetration

- 3.2.3.2 Connected and smart mobility solutions

- 3.2.3.3 Subscription and leasing models

- 3.2.3.4 Market expansion in Africa and Southeast Asia

- 3.2.3.5 Strategic partnerships with delivery platforms

- 3.2.4 Motorcycle and scooter market evolution

- 3.2.4.1 Historical market development and maturity analysis

- 3.2.4.2 Transition from traditional to modern mobility solutions

- 3.2.4.3 Technology adoption lifecycle in two-wheeler segment

- 3.2.4.4 Market consolidation and industry restructuring trends

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology innovation and advanced features

- 3.7.1 Motorcycle ADAS and safety technology integration

- 3.7.2 Connected motorcycle solutions and iot integration

- 3.7.3 Advanced powertrain technologies

- 3.7.4 Autonomous and semi-autonomous features development

- 3.8 Electric motorcycle and scooter market transformation

- 3.8.1 Electric two-wheeler technology evolution

- 3.8.2 Battery technology and range optimization

- 3.8.3 Charging infrastructure development and accessibility

- 3.8.4 Government incentives and policy support analysis

- 3.9 Consumer behavior and market preferences

- 3.9.1 Demographic profile and target customer analysis

- 3.9.2 Purchase decision factors and buying journey

- 3.9.3 Usage patterns and mobility behavior

- 3.9.4 Brand loyalty and switching patterns

- 3.9.5 Price sensitivity and value perception analysis

- 3.10 Patent landscape

- 3.11 Price trend

- 3.11.1 By country

- 3.11.2 By product

- 3.12 Cost breakdown analysis

- 3.13 Production statistics

- 3.13.1 Import and export

- 3.13.2 Major import countries

- 3.13.3 Major export countries

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Motorcycles

- 5.2.1 Cruiser motorcycles

- 5.2.2 Sport motorcycles

- 5.2.3 Touring motorcycles

- 5.2.4 Standard/naked motorcycles

- 5.2.5 Adventure/dual-sport motorcycles

- 5.2.6 Off-road/dirt motorcycles

- 5.3 Scooters

- 5.3.1 Traditional gasoline scooters

- 5.3.2 Electric scooters

- 5.3.3 Maxi scooters

- 5.3.4 Moped-style scooters

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Internal combustion engine (ICE)

- 6.3 Electric vehicles (EVs)

Chapter 7 Market Estimates & Forecast, By Engine Displacement, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Under 250cc

- 7.3 250cc-500cc

- 7.4 500cc-1000cc

- 7.5 Above 1000cc

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Offline

- 8.3 Online

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Personal

- 9.3 Commercial

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Two-Wheeler OEMs

- 11.1.1 Bajaj

- 11.1.2 Hero

- 11.1.3 Honda

- 11.1.4 Piaggio

- 11.1.5 Suzuki

- 11.1.6 TVS

- 11.1.7 Yamaha

- 11.2 Premium Motorcycle Brands

- 11.2.1 BMW Motorrad

- 11.2.2 Ducati

- 11.2.3 Harley-Davidson

- 11.2.4 KTM

- 11.2.5 Royal Enfield

- 11.2.6 Kawasaki

- 11.3 Electric Two-Wheeler Manufacturers

- 11.3.1 Ather

- 11.3.2 Ola Electric

- 11.3.3 Revolt

- 11.3.4 Ultraviolette

- 11.3.5 Yadea

- 11.3.6 Zero Motorcycles

- 11.3.7 Niu Technologies

- 11.4 Component and System Suppliers

- 11.4.1 Bosch

- 11.4.2 Brembo

- 11.4.3 Continental

- 11.4.4 Nissin

- 11.4.5 ZF

- 11.5 Connected Mobility and Software Providers

- 11.5.1 MapmyIndia

- 11.5.2 Ride Vision

- 11.5.3 Sibros

- 11.5.4 TomTom

- 11.5.5 Vahan